Fiskars Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Fiskars faces moderate supplier power but benefits from strong brand equity and diversified retail channels, while competitors and substitutes exert steady pressure in mature home & garden markets. Scale and distribution make new entrants unlikely, yet digital disruption and price sensitivity remain risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fiskars’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Material concentration and specs

Core inputs for Fiskars include specialty steels, ceramics, glass, plastics and wood produced to tight tolerances for cutting tools and premium tableware, which concentrates buying power among a few qualified suppliers for high-grade steel and glass, raising leverage and lead times.

Fiskars’ global scale and multi-year sourcing agreements reduce single-vendor dependence, while dual-sourcing and regionalization of supply chains mitigate disruption risk and blunt price spikes.

Brand pull offsets supplier leverage

Fiskars brands Iittala, Waterford and Gerber deliver steady volumes and global visibility through presence in over 100 countries and distribution via major retail partners, which gives suppliers predictable demand and lowers their risk. Predictability improves procurement terms as vendors trade price for stable orders and co-branding with a Nasdaq Helsinki-listed group. This brand-driven leverage helps temper raw-material volatility for Fiskars.

Sustainability and compliance requirements

Responsible sourcing, traceability, and 2030 emissions commitments narrow Fiskars’ approved supplier pool as EU CSRD reporting phased in from 2024 increases documentation needs; certified vendors (eg ISO 14001, >300,000 certificates globally) can capture premium pricing and shift bargaining power. Standardized ESG frameworks and supplier scorecards restore competitive bidding among compliant firms, while long-term partnerships balance cost, quality and sustainability trade-offs.

Logistics and regional exposure

Fiskars global footprint exposes it to freight volatility, port congestion and currency swings that can raise COGS and delay seasonal launches; localizing inputs and nearshoring have reduced supplier and transport leverage by shortening lead times and lowering exposure to long-haul disruptions.

Switching costs moderate to high

Requalifying steel grades, molds, glazes and finishes for Fiskars often requires months and six-figure capex, while tooling transfer and QA validation create operational friction that favors incumbent suppliers and raises switching costs to moderate–high.

- Requalification timeframe: months; capex: six-figure

- Tooling & QA favor incumbents, limiting rapid moves

- Category breadth enables selective tenders; SRM keeps power balanced

Specialist-material suppliers hold leverage; ISO 14001 and 2030 ESG targets narrow vendors

Fiskars relies on specialist steels, glass, ceramics and wood with long requalification (months) and six-figure tooling capex, giving incumbent suppliers moderate–high leverage. Global scale, multi-year contracts, dual-sourcing and presence in over 100 countries provide demand predictability that reduces supplier power. ESG/2030 targets and ISO 14001 requirements narrow approved vendors, shifting pricing to compliant suppliers.

| Metric | Fact |

|---|---|

| Geographic reach | >100 countries |

| Requalification time | months |

| Tooling capex | six-figure |

| ISO 14001 certificates | >300,000 (global) |

| Listing | Nasdaq Helsinki |

| Emissions target | 2030 commitments |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Fiskars that uncovers competitive intensity, supplier and buyer influence on pricing and profitability, and evaluates substitution threats and barriers deterring new entrants. It highlights disruptive market forces and strategic levers Fiskars can use to defend market share and enhance margins.

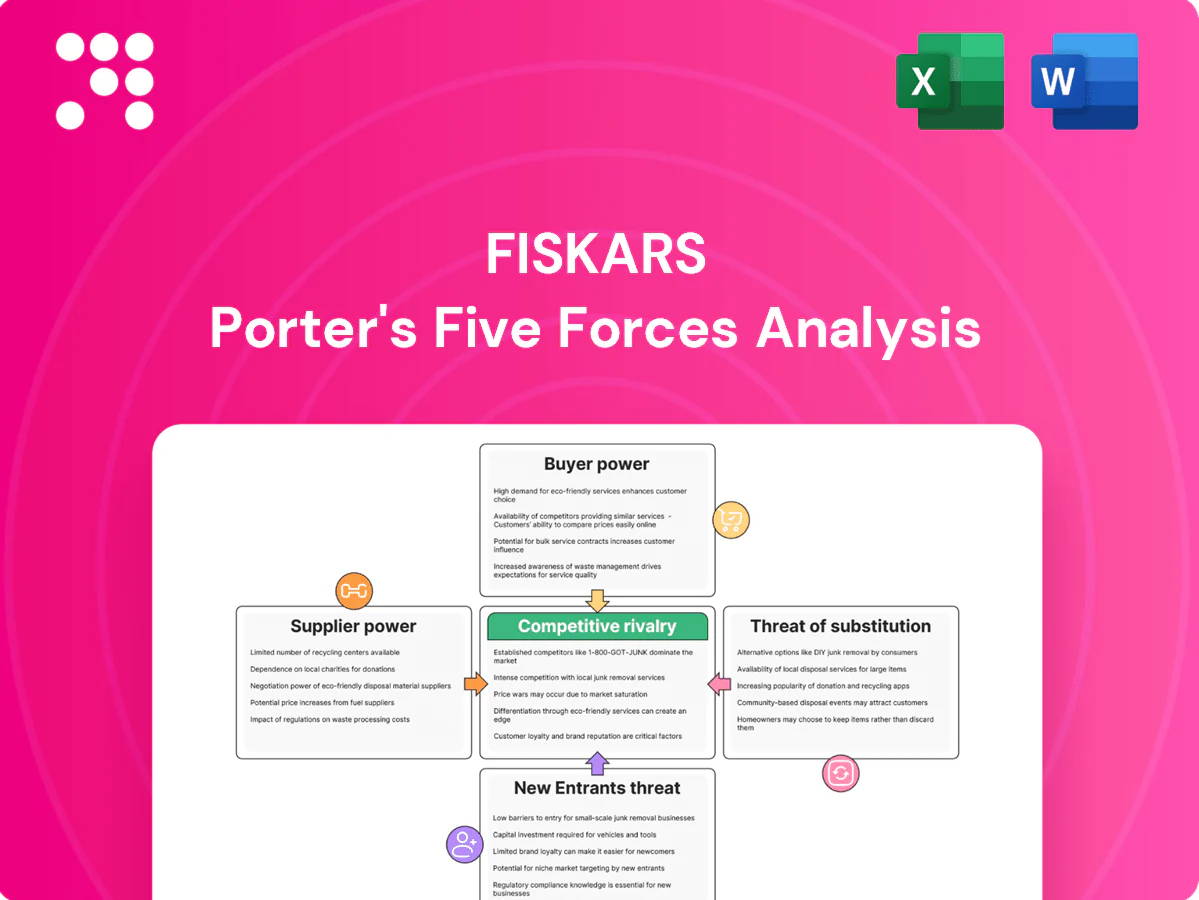

A clear, one-sheet Porter's Five Forces assessment for Fiskars—visualizing supplier, buyer, entrant, substitute and competitive pressures to speed strategic decisions and simplify boardroom discussions.

Customers Bargaining Power

Concentrated retail partners

Concentrated retail partners like Home Depot and Lowe's (combined ~60% of US home improvement sales) and major mass merchants can demand pricing, slotting, and promotional support, elevating buyer power in tools and tableware. Private-label penetration pressures margins and intensifies negotiations. Fiskars offsets this through brand-led pull, differentiated SKUs and premium positioning, protecting ASPs and shelf presence.

Omnichannel and DTC balance

E-commerce and DTC channels let Fiskars diversify revenue mix and reclaim margin from wholesale; Fiskars Group reported net sales of EUR 1,274 million in 2023, underscoring scale for channel investment. DTC data improves pricing and assortment decisions with retailers by feeding real-world purchase signals. Marketplace transparency boosts price comparisons and thus buyer power. Exclusive online bundles and personalization (76% of customers expect personalization per Salesforce 2023) offset discount pressure.

Brand loyalty and performance

Fiskars iconic orange-handled scissors (launched 1967) and heritage tableware brands Iittala and Arabia (brought into Fiskars in 2007) reduce price elasticity by anchoring loyalty and perceived durability. Professional and enthusiast segments prioritize performance, lowering switching even at higher price points. Gifting demand sustains premiums for luxury glass and crystal lines. Reviews and influencers, however, can partially lift buyer power.

Category substitutability and seasonality

Garden and outdoor seasonality concentrates roughly 60% of annual sales into spring/summer, prompting retailers to push inventory-risk sharing and tighter buy terms with Fiskars during promotional windows, increasing buyer leverage. Counter-season innovation and evergreen lines reduced Fiskars' seasonal volatility in 2024, smoothing order profiles. Broad assortment across categories lets Fiskars reallocate volume to negotiate better terms.

- seasonality: ~60% spring/summer

- risk-sharing: retailer inventory demands

- mitigation: counter-season + evergreen

- leverage: assortment breadth aids negotiation

Service levels and lead times

Retailers value OTIF performance (retailer targets typically ≥95%), customization and sustainability credentials, and superior service from Fiskars reduces buyers credible switching options by tightening operational integration. Vendor-managed inventory and forecasting partnerships curb markdown risk and improve shelf availability, while penalties for OTIF or lead-time misses (commonly 1–5% of invoice) can amplify buyer bargaining if performance falters.

- OTIF target ≥95%

- Customization & sustainability raise switching costs

- VMI/forecasting reduces markdowns and stockouts

- Performance penalties (1–5%) increase buyer leverage

Concentrated retailers boost buyer power; strong brands, DTC growth and assortment protect margins

Concentrated retail partners, private-label pressure and marketplace transparency raise buyer power vs Fiskars, but brand strength (Iittala, Arabia), DTC growth (Fiskars Group net sales EUR 1,274m in 2023) and assortment breadth mitigate margin loss; seasonality, OTIF targets and performance penalties remain negotiation levers.

| Metric | Value |

|---|---|

| US big-box share | ~60% |

| 2023 net sales | EUR 1,274m |

| Seasonality | ~60% spring/summer |

| OTIF target | ≥95% |

Preview the Actual Deliverable

Fiskars Porter's Five Forces Analysis

This preview shows the exact Fiskars Porter's Five Forces Analysis you'll receive after purchase—fully written, formatted, and ready to download. No samples or placeholders; the content here is the final deliverable. Buy once and gain instant access to this same complete file.

Don't Miss the Bigger Picture

Fiskars faces moderate supplier power but benefits from strong brand equity and diversified retail channels, while competitors and substitutes exert steady pressure in mature home & garden markets. Scale and distribution make new entrants unlikely, yet digital disruption and price sensitivity remain risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fiskars’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Material concentration and specs

Core inputs for Fiskars include specialty steels, ceramics, glass, plastics and wood produced to tight tolerances for cutting tools and premium tableware, which concentrates buying power among a few qualified suppliers for high-grade steel and glass, raising leverage and lead times.

Fiskars’ global scale and multi-year sourcing agreements reduce single-vendor dependence, while dual-sourcing and regionalization of supply chains mitigate disruption risk and blunt price spikes.

Brand pull offsets supplier leverage

Fiskars brands Iittala, Waterford and Gerber deliver steady volumes and global visibility through presence in over 100 countries and distribution via major retail partners, which gives suppliers predictable demand and lowers their risk. Predictability improves procurement terms as vendors trade price for stable orders and co-branding with a Nasdaq Helsinki-listed group. This brand-driven leverage helps temper raw-material volatility for Fiskars.

Sustainability and compliance requirements

Responsible sourcing, traceability, and 2030 emissions commitments narrow Fiskars’ approved supplier pool as EU CSRD reporting phased in from 2024 increases documentation needs; certified vendors (eg ISO 14001, >300,000 certificates globally) can capture premium pricing and shift bargaining power. Standardized ESG frameworks and supplier scorecards restore competitive bidding among compliant firms, while long-term partnerships balance cost, quality and sustainability trade-offs.

Logistics and regional exposure

Fiskars global footprint exposes it to freight volatility, port congestion and currency swings that can raise COGS and delay seasonal launches; localizing inputs and nearshoring have reduced supplier and transport leverage by shortening lead times and lowering exposure to long-haul disruptions.

Switching costs moderate to high

Requalifying steel grades, molds, glazes and finishes for Fiskars often requires months and six-figure capex, while tooling transfer and QA validation create operational friction that favors incumbent suppliers and raises switching costs to moderate–high.

- Requalification timeframe: months; capex: six-figure

- Tooling & QA favor incumbents, limiting rapid moves

- Category breadth enables selective tenders; SRM keeps power balanced

Specialist-material suppliers hold leverage; ISO 14001 and 2030 ESG targets narrow vendors

Fiskars relies on specialist steels, glass, ceramics and wood with long requalification (months) and six-figure tooling capex, giving incumbent suppliers moderate–high leverage. Global scale, multi-year contracts, dual-sourcing and presence in over 100 countries provide demand predictability that reduces supplier power. ESG/2030 targets and ISO 14001 requirements narrow approved vendors, shifting pricing to compliant suppliers.

| Metric | Fact |

|---|---|

| Geographic reach | >100 countries |

| Requalification time | months |

| Tooling capex | six-figure |

| ISO 14001 certificates | >300,000 (global) |

| Listing | Nasdaq Helsinki |

| Emissions target | 2030 commitments |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Fiskars that uncovers competitive intensity, supplier and buyer influence on pricing and profitability, and evaluates substitution threats and barriers deterring new entrants. It highlights disruptive market forces and strategic levers Fiskars can use to defend market share and enhance margins.

A clear, one-sheet Porter's Five Forces assessment for Fiskars—visualizing supplier, buyer, entrant, substitute and competitive pressures to speed strategic decisions and simplify boardroom discussions.

Customers Bargaining Power

Concentrated retail partners

Concentrated retail partners like Home Depot and Lowe's (combined ~60% of US home improvement sales) and major mass merchants can demand pricing, slotting, and promotional support, elevating buyer power in tools and tableware. Private-label penetration pressures margins and intensifies negotiations. Fiskars offsets this through brand-led pull, differentiated SKUs and premium positioning, protecting ASPs and shelf presence.

Omnichannel and DTC balance

E-commerce and DTC channels let Fiskars diversify revenue mix and reclaim margin from wholesale; Fiskars Group reported net sales of EUR 1,274 million in 2023, underscoring scale for channel investment. DTC data improves pricing and assortment decisions with retailers by feeding real-world purchase signals. Marketplace transparency boosts price comparisons and thus buyer power. Exclusive online bundles and personalization (76% of customers expect personalization per Salesforce 2023) offset discount pressure.

Brand loyalty and performance

Fiskars iconic orange-handled scissors (launched 1967) and heritage tableware brands Iittala and Arabia (brought into Fiskars in 2007) reduce price elasticity by anchoring loyalty and perceived durability. Professional and enthusiast segments prioritize performance, lowering switching even at higher price points. Gifting demand sustains premiums for luxury glass and crystal lines. Reviews and influencers, however, can partially lift buyer power.

Category substitutability and seasonality

Garden and outdoor seasonality concentrates roughly 60% of annual sales into spring/summer, prompting retailers to push inventory-risk sharing and tighter buy terms with Fiskars during promotional windows, increasing buyer leverage. Counter-season innovation and evergreen lines reduced Fiskars' seasonal volatility in 2024, smoothing order profiles. Broad assortment across categories lets Fiskars reallocate volume to negotiate better terms.

- seasonality: ~60% spring/summer

- risk-sharing: retailer inventory demands

- mitigation: counter-season + evergreen

- leverage: assortment breadth aids negotiation

Service levels and lead times

Retailers value OTIF performance (retailer targets typically ≥95%), customization and sustainability credentials, and superior service from Fiskars reduces buyers credible switching options by tightening operational integration. Vendor-managed inventory and forecasting partnerships curb markdown risk and improve shelf availability, while penalties for OTIF or lead-time misses (commonly 1–5% of invoice) can amplify buyer bargaining if performance falters.

- OTIF target ≥95%

- Customization & sustainability raise switching costs

- VMI/forecasting reduces markdowns and stockouts

- Performance penalties (1–5%) increase buyer leverage

Concentrated retailers boost buyer power; strong brands, DTC growth and assortment protect margins

Concentrated retail partners, private-label pressure and marketplace transparency raise buyer power vs Fiskars, but brand strength (Iittala, Arabia), DTC growth (Fiskars Group net sales EUR 1,274m in 2023) and assortment breadth mitigate margin loss; seasonality, OTIF targets and performance penalties remain negotiation levers.

| Metric | Value |

|---|---|

| US big-box share | ~60% |

| 2023 net sales | EUR 1,274m |

| Seasonality | ~60% spring/summer |

| OTIF target | ≥95% |

Preview the Actual Deliverable

Fiskars Porter's Five Forces Analysis

This preview shows the exact Fiskars Porter's Five Forces Analysis you'll receive after purchase—fully written, formatted, and ready to download. No samples or placeholders; the content here is the final deliverable. Buy once and gain instant access to this same complete file.

Description

Don't Miss the Bigger Picture

Fiskars faces moderate supplier power but benefits from strong brand equity and diversified retail channels, while competitors and substitutes exert steady pressure in mature home & garden markets. Scale and distribution make new entrants unlikely, yet digital disruption and price sensitivity remain risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fiskars’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Material concentration and specs

Core inputs for Fiskars include specialty steels, ceramics, glass, plastics and wood produced to tight tolerances for cutting tools and premium tableware, which concentrates buying power among a few qualified suppliers for high-grade steel and glass, raising leverage and lead times.

Fiskars’ global scale and multi-year sourcing agreements reduce single-vendor dependence, while dual-sourcing and regionalization of supply chains mitigate disruption risk and blunt price spikes.

Brand pull offsets supplier leverage

Fiskars brands Iittala, Waterford and Gerber deliver steady volumes and global visibility through presence in over 100 countries and distribution via major retail partners, which gives suppliers predictable demand and lowers their risk. Predictability improves procurement terms as vendors trade price for stable orders and co-branding with a Nasdaq Helsinki-listed group. This brand-driven leverage helps temper raw-material volatility for Fiskars.

Sustainability and compliance requirements

Responsible sourcing, traceability, and 2030 emissions commitments narrow Fiskars’ approved supplier pool as EU CSRD reporting phased in from 2024 increases documentation needs; certified vendors (eg ISO 14001, >300,000 certificates globally) can capture premium pricing and shift bargaining power. Standardized ESG frameworks and supplier scorecards restore competitive bidding among compliant firms, while long-term partnerships balance cost, quality and sustainability trade-offs.

Logistics and regional exposure

Fiskars global footprint exposes it to freight volatility, port congestion and currency swings that can raise COGS and delay seasonal launches; localizing inputs and nearshoring have reduced supplier and transport leverage by shortening lead times and lowering exposure to long-haul disruptions.

Switching costs moderate to high

Requalifying steel grades, molds, glazes and finishes for Fiskars often requires months and six-figure capex, while tooling transfer and QA validation create operational friction that favors incumbent suppliers and raises switching costs to moderate–high.

- Requalification timeframe: months; capex: six-figure

- Tooling & QA favor incumbents, limiting rapid moves

- Category breadth enables selective tenders; SRM keeps power balanced

Specialist-material suppliers hold leverage; ISO 14001 and 2030 ESG targets narrow vendors

Fiskars relies on specialist steels, glass, ceramics and wood with long requalification (months) and six-figure tooling capex, giving incumbent suppliers moderate–high leverage. Global scale, multi-year contracts, dual-sourcing and presence in over 100 countries provide demand predictability that reduces supplier power. ESG/2030 targets and ISO 14001 requirements narrow approved vendors, shifting pricing to compliant suppliers.

| Metric | Fact |

|---|---|

| Geographic reach | >100 countries |

| Requalification time | months |

| Tooling capex | six-figure |

| ISO 14001 certificates | >300,000 (global) |

| Listing | Nasdaq Helsinki |

| Emissions target | 2030 commitments |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Fiskars that uncovers competitive intensity, supplier and buyer influence on pricing and profitability, and evaluates substitution threats and barriers deterring new entrants. It highlights disruptive market forces and strategic levers Fiskars can use to defend market share and enhance margins.

A clear, one-sheet Porter's Five Forces assessment for Fiskars—visualizing supplier, buyer, entrant, substitute and competitive pressures to speed strategic decisions and simplify boardroom discussions.

Customers Bargaining Power

Concentrated retail partners

Concentrated retail partners like Home Depot and Lowe's (combined ~60% of US home improvement sales) and major mass merchants can demand pricing, slotting, and promotional support, elevating buyer power in tools and tableware. Private-label penetration pressures margins and intensifies negotiations. Fiskars offsets this through brand-led pull, differentiated SKUs and premium positioning, protecting ASPs and shelf presence.

Omnichannel and DTC balance

E-commerce and DTC channels let Fiskars diversify revenue mix and reclaim margin from wholesale; Fiskars Group reported net sales of EUR 1,274 million in 2023, underscoring scale for channel investment. DTC data improves pricing and assortment decisions with retailers by feeding real-world purchase signals. Marketplace transparency boosts price comparisons and thus buyer power. Exclusive online bundles and personalization (76% of customers expect personalization per Salesforce 2023) offset discount pressure.

Brand loyalty and performance

Fiskars iconic orange-handled scissors (launched 1967) and heritage tableware brands Iittala and Arabia (brought into Fiskars in 2007) reduce price elasticity by anchoring loyalty and perceived durability. Professional and enthusiast segments prioritize performance, lowering switching even at higher price points. Gifting demand sustains premiums for luxury glass and crystal lines. Reviews and influencers, however, can partially lift buyer power.

Category substitutability and seasonality

Garden and outdoor seasonality concentrates roughly 60% of annual sales into spring/summer, prompting retailers to push inventory-risk sharing and tighter buy terms with Fiskars during promotional windows, increasing buyer leverage. Counter-season innovation and evergreen lines reduced Fiskars' seasonal volatility in 2024, smoothing order profiles. Broad assortment across categories lets Fiskars reallocate volume to negotiate better terms.

- seasonality: ~60% spring/summer

- risk-sharing: retailer inventory demands

- mitigation: counter-season + evergreen

- leverage: assortment breadth aids negotiation

Service levels and lead times

Retailers value OTIF performance (retailer targets typically ≥95%), customization and sustainability credentials, and superior service from Fiskars reduces buyers credible switching options by tightening operational integration. Vendor-managed inventory and forecasting partnerships curb markdown risk and improve shelf availability, while penalties for OTIF or lead-time misses (commonly 1–5% of invoice) can amplify buyer bargaining if performance falters.

- OTIF target ≥95%

- Customization & sustainability raise switching costs

- VMI/forecasting reduces markdowns and stockouts

- Performance penalties (1–5%) increase buyer leverage

Concentrated retailers boost buyer power; strong brands, DTC growth and assortment protect margins

Concentrated retail partners, private-label pressure and marketplace transparency raise buyer power vs Fiskars, but brand strength (Iittala, Arabia), DTC growth (Fiskars Group net sales EUR 1,274m in 2023) and assortment breadth mitigate margin loss; seasonality, OTIF targets and performance penalties remain negotiation levers.

| Metric | Value |

|---|---|

| US big-box share | ~60% |

| 2023 net sales | EUR 1,274m |

| Seasonality | ~60% spring/summer |

| OTIF target | ≥95% |

Preview the Actual Deliverable

Fiskars Porter's Five Forces Analysis

This preview shows the exact Fiskars Porter's Five Forces Analysis you'll receive after purchase—fully written, formatted, and ready to download. No samples or placeholders; the content here is the final deliverable. Buy once and gain instant access to this same complete file.