Fiten PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, social trends, and technological advances are shaping Fiten’s strategy and risk profile in our concise PESTLE overview. Packed with actionable insights for investors and strategists, this analysis highlights opportunities and threats you can act on today. Purchase the full PESTLE to access the complete, downloadable breakdown and ready-to-use recommendations.

Political factors

EU Green Deal and Fit for 55 alignment

EU decarbonization via the Green Deal and Fit for 55 (55% GHG cut by 2030 vs 1990) drives supportive policies that boost solar deployment across member states. Access to EU funds such as NextGenerationEU (EUR 750bn) and national RRF allocations can lower project costs and expand markets. Policy continuity reduces planning risk for commercial and residential clients, enabling Fiten to tailor offerings to evolving compliance and subsidy criteria.

National renewable energy auctions and incentives

Poland’s technology-specific renewable auctions and grant schemes shape demand timing and pricing, so Fiten must align project bids with announced auction calendars and eligibility rules to optimize revenue. Incentive availability materially shortens payback periods and lifts adoption rates, especially where regional support supplements national programs. Continuous monitoring of local grants and EU funds can reveal niche pipeline opportunities.

Energy security and diversification priorities

Geopolitical pressures since 2022 have strengthened political will for domestic renewables, exemplified by the EU REPowerEU plan to diversify away from fossil fuel imports. Global cumulative solar PV capacity surpassed 1 TW by 2023 (IEA), boosting momentum for distributed PV to cut import dependence. Policymakers are fast-tracking permitting and grid access in many markets, shortening approval timelines and improving connection terms. Fiten can foreground resilience and on-site generation benefits to win policy and customer support.

Local government zoning and permitting stance

Regional authorities show wide variance in rooftop and ground-mount PV permitting: top jurisdictions process permits in 15–30 days while slower areas exceed 90 days (NREL/LBNL data through 2024). Favorable municipalities shorten sales cycles and can cut soft costs; active engagement with officials speeds approvals and interconnections. Site selection should prioritize procedural predictability to avoid 2–3 month delays.

Public utility and grid operator policies

DSO and TSO rules determine connection feasibility and curtailment exposure for Fiten; global solar PV capacity surpassed ~1,000 GW by 2023 (IEA), increasing grid stress and curtailment events. Net-billing designs directly affect prosumer revenue certainty; regulatory shifts (eg FERC Order 2222 enabling DER participation) and changing inverter/metering standards force Fiten to update designs and tariff models.

- DSO/TSO: connection queues and curtailment

- Net-billing: revenue certainty for prosumers

- Standards: inverter/metering updates

- Action: adapt designs to evolving grid codes & tariffs

EU policy and grid rules accelerate PV rollout; permitting variance shapes payback timelines

EU Fit for 55 (55% GHG cut by 2030) and NextGenerationEU (EUR 750bn) sustain subsidies and stable policy; Poland auctions/timeframes drive project timing; REPowerEU and >1 TW global PV (2023) fast-track permitting and grid priority; permitting variance (15–30 vs 90+ days) and DSO/TSO rules shape connection risk and payback timelines.

| Policy | Metric | Impact |

|---|---|---|

| Fit for 55 | 55% by 2030 | Subsidy stability |

| NextGenerationEU | EUR 750bn | Lower project costs |

What is included in the product

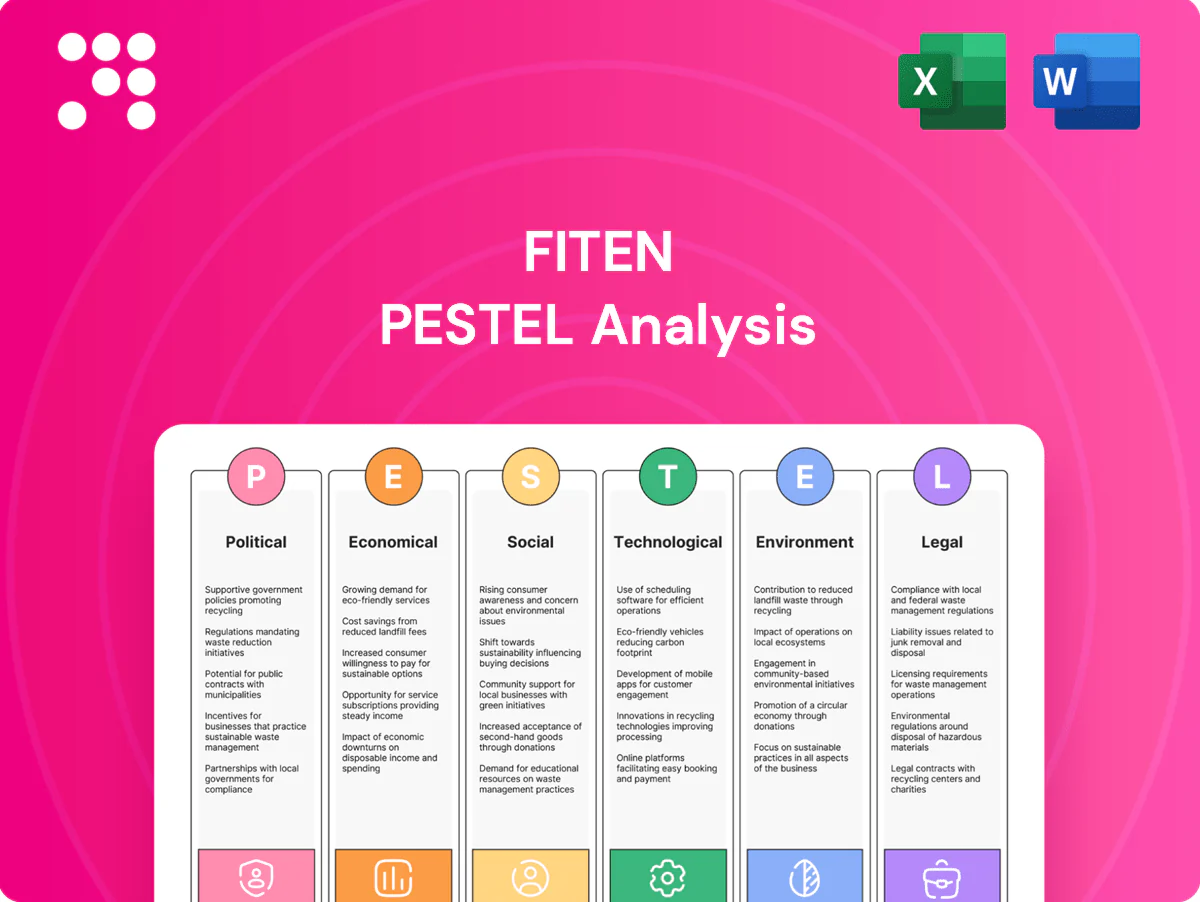

Explores how macro-environmental forces uniquely affect the Fiten across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region- and industry-specific examples. Designed for executives and investors, it offers forward-looking insights, scenario inputs, and ready-to-use findings for strategy, funding, and risk mitigation.

A concise, visually segmented Fiten PESTLE summary that's easily shared and editable, enabling quick alignment across teams, supporting external risk discussions, and ready to drop into presentations or strategy packs.

Economic factors

Electricity price volatility and savings potential

High wholesale volatility (day-ahead peaks >€200/MWh in 2022–24) and average EU household retail prices near €0.30–0.35/kWh in 2024 materially strengthen PV ROI for clients. Time-of-use tariffs lift value of self-consumption and storage, increasing savings by ~20–30%. Sales messaging should quantify bill-hedging and payback across scenarios (typical paybacks 4–8 years). EPC offerings can bundle optimization and batteries to lock 10–30% extra savings.

Module and component cost trends

Global PV module prices have fallen to roughly $0.16–0.19/W in 2024 but remain cyclical, with short-term spikes during supply shocks. Inverter and battery pack costs (battery ~$120–135/kWh in 2024), plus logistics and FX swings, compress margins. Strategic procurement, hedging and inventory smoothing protect pricing. Clients gain from transparent cost pass-through models that align incentives.

Interest rates and financing availability

Rising policy rates (many central banks ranged about 3–5% in H1 2025) push SME/household loan costs to roughly 6–12%, materially raising system LCOE—roughly a 1 percentage-point finance cost change can shift LCOE ~3%–4%. Partnerships with banks and leasing firms unlock latent demand; in practice point-of-sale financing can shorten sales cycles by ~20–30% and widen eligibility. Sensitivity analyses on pricing and tenor must guide offers and risk-adjusted terms.

Corporate decarbonization and ESG budgets

Companies increasingly allocate capital to meet ESG and Scope 2 targets, using onsite PV and PPAs to achieve verifiable emissions reductions and improve ESG ratings; demand concentrates in electricity‑intensive sectors such as data centers, manufacturing and logistics. Fiten can design B2B packages mapped to ESG reporting frameworks and Scope 2 accounting to capture corporate procurement budgets.

- Scope 2 alignment

- Onsite PV + PPAs

- Target: high‑intensity sectors

- B2B ESG reporting packs

Labor market and installation capacity

Skilled electrician availability directly shapes project timelines and costs; BLS projects 7% employment growth for electricians 2022–32 and median wage was 61,550 USD in May 2023, increasing labor cost pressure and training needs. Workforce planning and certification/apprenticeship programs raise throughput and scalability, while robust subcontractor networks provide 24–48 hour capacity relief during demand spikes.

- Labor supply: 7% projected growth 2022–32 (BLS)

- Median wage: 61,550 USD (May 2023, BLS)

- Training: certifications/apprenticeships improve throughput

- Subcontractors: flexible surge capacity

EU policy and grid rules accelerate PV rollout; permitting variance shapes payback timelines

High retail prices (~€0.30–0.35/kWh in 2024) and day‑ahead peaks >€200/MWh (2022–24) boost PV ROI; typical paybacks 4–8 years. Module $0.16–0.19/W, battery $120–135/kWh (2024) compress margins; financing (rates ~3–5% central banks, loan costs 6–12% H1 2025) raises LCOE ~3–4%/pp. ESG demand from data centers/manufacturing lifts commercial uptake.

| Metric | Value |

|---|---|

| Retail price | €0.30–0.35/kWh (2024) |

| Module cost | $0.16–0.19/W (2024) |

| Battery | $120–135/kWh (2024) |

| Loan costs | 6–12% (H1 2025) |

What You See Is What You Get

Fiten PESTLE Analysis

The preview shown here is the exact Fiten PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. Purchase delivers this exact, professionally structured document instantly.

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, social trends, and technological advances are shaping Fiten’s strategy and risk profile in our concise PESTLE overview. Packed with actionable insights for investors and strategists, this analysis highlights opportunities and threats you can act on today. Purchase the full PESTLE to access the complete, downloadable breakdown and ready-to-use recommendations.

Political factors

EU Green Deal and Fit for 55 alignment

EU decarbonization via the Green Deal and Fit for 55 (55% GHG cut by 2030 vs 1990) drives supportive policies that boost solar deployment across member states. Access to EU funds such as NextGenerationEU (EUR 750bn) and national RRF allocations can lower project costs and expand markets. Policy continuity reduces planning risk for commercial and residential clients, enabling Fiten to tailor offerings to evolving compliance and subsidy criteria.

National renewable energy auctions and incentives

Poland’s technology-specific renewable auctions and grant schemes shape demand timing and pricing, so Fiten must align project bids with announced auction calendars and eligibility rules to optimize revenue. Incentive availability materially shortens payback periods and lifts adoption rates, especially where regional support supplements national programs. Continuous monitoring of local grants and EU funds can reveal niche pipeline opportunities.

Energy security and diversification priorities

Geopolitical pressures since 2022 have strengthened political will for domestic renewables, exemplified by the EU REPowerEU plan to diversify away from fossil fuel imports. Global cumulative solar PV capacity surpassed 1 TW by 2023 (IEA), boosting momentum for distributed PV to cut import dependence. Policymakers are fast-tracking permitting and grid access in many markets, shortening approval timelines and improving connection terms. Fiten can foreground resilience and on-site generation benefits to win policy and customer support.

Local government zoning and permitting stance

Regional authorities show wide variance in rooftop and ground-mount PV permitting: top jurisdictions process permits in 15–30 days while slower areas exceed 90 days (NREL/LBNL data through 2024). Favorable municipalities shorten sales cycles and can cut soft costs; active engagement with officials speeds approvals and interconnections. Site selection should prioritize procedural predictability to avoid 2–3 month delays.

Public utility and grid operator policies

DSO and TSO rules determine connection feasibility and curtailment exposure for Fiten; global solar PV capacity surpassed ~1,000 GW by 2023 (IEA), increasing grid stress and curtailment events. Net-billing designs directly affect prosumer revenue certainty; regulatory shifts (eg FERC Order 2222 enabling DER participation) and changing inverter/metering standards force Fiten to update designs and tariff models.

- DSO/TSO: connection queues and curtailment

- Net-billing: revenue certainty for prosumers

- Standards: inverter/metering updates

- Action: adapt designs to evolving grid codes & tariffs

EU policy and grid rules accelerate PV rollout; permitting variance shapes payback timelines

EU Fit for 55 (55% GHG cut by 2030) and NextGenerationEU (EUR 750bn) sustain subsidies and stable policy; Poland auctions/timeframes drive project timing; REPowerEU and >1 TW global PV (2023) fast-track permitting and grid priority; permitting variance (15–30 vs 90+ days) and DSO/TSO rules shape connection risk and payback timelines.

| Policy | Metric | Impact |

|---|---|---|

| Fit for 55 | 55% by 2030 | Subsidy stability |

| NextGenerationEU | EUR 750bn | Lower project costs |

What is included in the product

Explores how macro-environmental forces uniquely affect the Fiten across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region- and industry-specific examples. Designed for executives and investors, it offers forward-looking insights, scenario inputs, and ready-to-use findings for strategy, funding, and risk mitigation.

A concise, visually segmented Fiten PESTLE summary that's easily shared and editable, enabling quick alignment across teams, supporting external risk discussions, and ready to drop into presentations or strategy packs.

Economic factors

Electricity price volatility and savings potential

High wholesale volatility (day-ahead peaks >€200/MWh in 2022–24) and average EU household retail prices near €0.30–0.35/kWh in 2024 materially strengthen PV ROI for clients. Time-of-use tariffs lift value of self-consumption and storage, increasing savings by ~20–30%. Sales messaging should quantify bill-hedging and payback across scenarios (typical paybacks 4–8 years). EPC offerings can bundle optimization and batteries to lock 10–30% extra savings.

Module and component cost trends

Global PV module prices have fallen to roughly $0.16–0.19/W in 2024 but remain cyclical, with short-term spikes during supply shocks. Inverter and battery pack costs (battery ~$120–135/kWh in 2024), plus logistics and FX swings, compress margins. Strategic procurement, hedging and inventory smoothing protect pricing. Clients gain from transparent cost pass-through models that align incentives.

Interest rates and financing availability

Rising policy rates (many central banks ranged about 3–5% in H1 2025) push SME/household loan costs to roughly 6–12%, materially raising system LCOE—roughly a 1 percentage-point finance cost change can shift LCOE ~3%–4%. Partnerships with banks and leasing firms unlock latent demand; in practice point-of-sale financing can shorten sales cycles by ~20–30% and widen eligibility. Sensitivity analyses on pricing and tenor must guide offers and risk-adjusted terms.

Corporate decarbonization and ESG budgets

Companies increasingly allocate capital to meet ESG and Scope 2 targets, using onsite PV and PPAs to achieve verifiable emissions reductions and improve ESG ratings; demand concentrates in electricity‑intensive sectors such as data centers, manufacturing and logistics. Fiten can design B2B packages mapped to ESG reporting frameworks and Scope 2 accounting to capture corporate procurement budgets.

- Scope 2 alignment

- Onsite PV + PPAs

- Target: high‑intensity sectors

- B2B ESG reporting packs

Labor market and installation capacity

Skilled electrician availability directly shapes project timelines and costs; BLS projects 7% employment growth for electricians 2022–32 and median wage was 61,550 USD in May 2023, increasing labor cost pressure and training needs. Workforce planning and certification/apprenticeship programs raise throughput and scalability, while robust subcontractor networks provide 24–48 hour capacity relief during demand spikes.

- Labor supply: 7% projected growth 2022–32 (BLS)

- Median wage: 61,550 USD (May 2023, BLS)

- Training: certifications/apprenticeships improve throughput

- Subcontractors: flexible surge capacity

EU policy and grid rules accelerate PV rollout; permitting variance shapes payback timelines

High retail prices (~€0.30–0.35/kWh in 2024) and day‑ahead peaks >€200/MWh (2022–24) boost PV ROI; typical paybacks 4–8 years. Module $0.16–0.19/W, battery $120–135/kWh (2024) compress margins; financing (rates ~3–5% central banks, loan costs 6–12% H1 2025) raises LCOE ~3–4%/pp. ESG demand from data centers/manufacturing lifts commercial uptake.

| Metric | Value |

|---|---|

| Retail price | €0.30–0.35/kWh (2024) |

| Module cost | $0.16–0.19/W (2024) |

| Battery | $120–135/kWh (2024) |

| Loan costs | 6–12% (H1 2025) |

What You See Is What You Get

Fiten PESTLE Analysis

The preview shown here is the exact Fiten PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. Purchase delivers this exact, professionally structured document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, social trends, and technological advances are shaping Fiten’s strategy and risk profile in our concise PESTLE overview. Packed with actionable insights for investors and strategists, this analysis highlights opportunities and threats you can act on today. Purchase the full PESTLE to access the complete, downloadable breakdown and ready-to-use recommendations.

Political factors

EU Green Deal and Fit for 55 alignment

EU decarbonization via the Green Deal and Fit for 55 (55% GHG cut by 2030 vs 1990) drives supportive policies that boost solar deployment across member states. Access to EU funds such as NextGenerationEU (EUR 750bn) and national RRF allocations can lower project costs and expand markets. Policy continuity reduces planning risk for commercial and residential clients, enabling Fiten to tailor offerings to evolving compliance and subsidy criteria.

National renewable energy auctions and incentives

Poland’s technology-specific renewable auctions and grant schemes shape demand timing and pricing, so Fiten must align project bids with announced auction calendars and eligibility rules to optimize revenue. Incentive availability materially shortens payback periods and lifts adoption rates, especially where regional support supplements national programs. Continuous monitoring of local grants and EU funds can reveal niche pipeline opportunities.

Energy security and diversification priorities

Geopolitical pressures since 2022 have strengthened political will for domestic renewables, exemplified by the EU REPowerEU plan to diversify away from fossil fuel imports. Global cumulative solar PV capacity surpassed 1 TW by 2023 (IEA), boosting momentum for distributed PV to cut import dependence. Policymakers are fast-tracking permitting and grid access in many markets, shortening approval timelines and improving connection terms. Fiten can foreground resilience and on-site generation benefits to win policy and customer support.

Local government zoning and permitting stance

Regional authorities show wide variance in rooftop and ground-mount PV permitting: top jurisdictions process permits in 15–30 days while slower areas exceed 90 days (NREL/LBNL data through 2024). Favorable municipalities shorten sales cycles and can cut soft costs; active engagement with officials speeds approvals and interconnections. Site selection should prioritize procedural predictability to avoid 2–3 month delays.

Public utility and grid operator policies

DSO and TSO rules determine connection feasibility and curtailment exposure for Fiten; global solar PV capacity surpassed ~1,000 GW by 2023 (IEA), increasing grid stress and curtailment events. Net-billing designs directly affect prosumer revenue certainty; regulatory shifts (eg FERC Order 2222 enabling DER participation) and changing inverter/metering standards force Fiten to update designs and tariff models.

- DSO/TSO: connection queues and curtailment

- Net-billing: revenue certainty for prosumers

- Standards: inverter/metering updates

- Action: adapt designs to evolving grid codes & tariffs

EU policy and grid rules accelerate PV rollout; permitting variance shapes payback timelines

EU Fit for 55 (55% GHG cut by 2030) and NextGenerationEU (EUR 750bn) sustain subsidies and stable policy; Poland auctions/timeframes drive project timing; REPowerEU and >1 TW global PV (2023) fast-track permitting and grid priority; permitting variance (15–30 vs 90+ days) and DSO/TSO rules shape connection risk and payback timelines.

| Policy | Metric | Impact |

|---|---|---|

| Fit for 55 | 55% by 2030 | Subsidy stability |

| NextGenerationEU | EUR 750bn | Lower project costs |

What is included in the product

Explores how macro-environmental forces uniquely affect the Fiten across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region- and industry-specific examples. Designed for executives and investors, it offers forward-looking insights, scenario inputs, and ready-to-use findings for strategy, funding, and risk mitigation.

A concise, visually segmented Fiten PESTLE summary that's easily shared and editable, enabling quick alignment across teams, supporting external risk discussions, and ready to drop into presentations or strategy packs.

Economic factors

Electricity price volatility and savings potential

High wholesale volatility (day-ahead peaks >€200/MWh in 2022–24) and average EU household retail prices near €0.30–0.35/kWh in 2024 materially strengthen PV ROI for clients. Time-of-use tariffs lift value of self-consumption and storage, increasing savings by ~20–30%. Sales messaging should quantify bill-hedging and payback across scenarios (typical paybacks 4–8 years). EPC offerings can bundle optimization and batteries to lock 10–30% extra savings.

Module and component cost trends

Global PV module prices have fallen to roughly $0.16–0.19/W in 2024 but remain cyclical, with short-term spikes during supply shocks. Inverter and battery pack costs (battery ~$120–135/kWh in 2024), plus logistics and FX swings, compress margins. Strategic procurement, hedging and inventory smoothing protect pricing. Clients gain from transparent cost pass-through models that align incentives.

Interest rates and financing availability

Rising policy rates (many central banks ranged about 3–5% in H1 2025) push SME/household loan costs to roughly 6–12%, materially raising system LCOE—roughly a 1 percentage-point finance cost change can shift LCOE ~3%–4%. Partnerships with banks and leasing firms unlock latent demand; in practice point-of-sale financing can shorten sales cycles by ~20–30% and widen eligibility. Sensitivity analyses on pricing and tenor must guide offers and risk-adjusted terms.

Corporate decarbonization and ESG budgets

Companies increasingly allocate capital to meet ESG and Scope 2 targets, using onsite PV and PPAs to achieve verifiable emissions reductions and improve ESG ratings; demand concentrates in electricity‑intensive sectors such as data centers, manufacturing and logistics. Fiten can design B2B packages mapped to ESG reporting frameworks and Scope 2 accounting to capture corporate procurement budgets.

- Scope 2 alignment

- Onsite PV + PPAs

- Target: high‑intensity sectors

- B2B ESG reporting packs

Labor market and installation capacity

Skilled electrician availability directly shapes project timelines and costs; BLS projects 7% employment growth for electricians 2022–32 and median wage was 61,550 USD in May 2023, increasing labor cost pressure and training needs. Workforce planning and certification/apprenticeship programs raise throughput and scalability, while robust subcontractor networks provide 24–48 hour capacity relief during demand spikes.

- Labor supply: 7% projected growth 2022–32 (BLS)

- Median wage: 61,550 USD (May 2023, BLS)

- Training: certifications/apprenticeships improve throughput

- Subcontractors: flexible surge capacity

EU policy and grid rules accelerate PV rollout; permitting variance shapes payback timelines

High retail prices (~€0.30–0.35/kWh in 2024) and day‑ahead peaks >€200/MWh (2022–24) boost PV ROI; typical paybacks 4–8 years. Module $0.16–0.19/W, battery $120–135/kWh (2024) compress margins; financing (rates ~3–5% central banks, loan costs 6–12% H1 2025) raises LCOE ~3–4%/pp. ESG demand from data centers/manufacturing lifts commercial uptake.

| Metric | Value |

|---|---|

| Retail price | €0.30–0.35/kWh (2024) |

| Module cost | $0.16–0.19/W (2024) |

| Battery | $120–135/kWh (2024) |

| Loan costs | 6–12% (H1 2025) |

What You See Is What You Get

Fiten PESTLE Analysis

The preview shown here is the exact Fiten PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. Purchase delivers this exact, professionally structured document instantly.