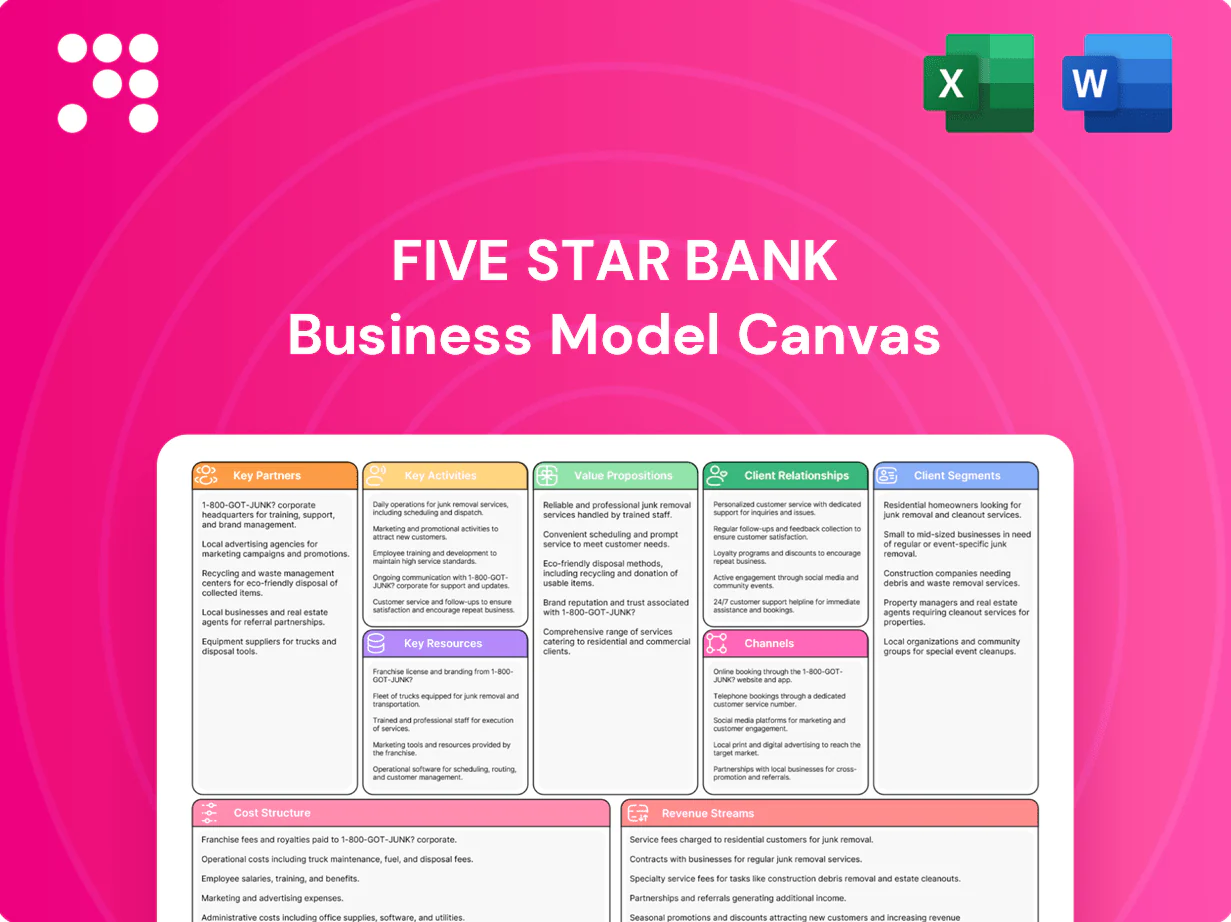

Five Star Bank Business Model Canvas

Business Model Canvas for a leading regional bank - Word and Excel ready

Unlock the full strategic blueprint behind Five Star Bank with our complete Business Model Canvas — three to five detailed sentences condense its value propositions, key partners, revenue streams, and growth levers into actionable insights. Ideal for investors, consultants, and founders, the downloadable Word and Excel files are ready for benchmarking and strategy work. Purchase now to see every section, metrics, and tactical recommendations.

Partnerships

Local business networks

Partnerships with chambers of commerce and industry associations extend Five Star Bank’s reach into regional businesses, driving referrals and joint educational events that deepen customer pipelines. These alliances reinforce the bank’s community presence and credibility. They also surface early intelligence on local economic trends, critical given that 99.9% of US firms are small businesses (SBA 2024).

Fintech and core vendors

Relationships with core banking, payments, and cybersecurity providers power Five Star Bank’s digital services, enabling online lending, card processing, and 24/7 fraud monitoring. Vendors support integrations for treasury, ACH, and remote deposit capture, connecting bank workflows to industry rails. Joint roadmaps improve reliability and user experience and, per Deloitte 2024, 78% of banks cite third‑party partnerships as critical to digital transformation. They let the bank scale securely without owning all tech.

Correspondent banks

Correspondent banks enable syndications, participations and specialized services, letting Five Star Bank originate larger credits while sharing risk through partners; global syndicated loan activity was about $1.2 trillion in 2023 per Refinitiv. They expand lending capacity for bigger borrowers without diluting client relationship ownership. Correspondents supply liquidity and foreign-exchange rails—SWIFT processed ~40 million messages/day in 2024—extending product breadth.

Government & SBA programs

Partnering with SBA and state programs gives Five Star Bank access to government-guaranteed lending—SBA 7(a) guarantees up to 85% for loans ≤150,000 and 75% for loans >150,000, with 7(a) max loan size $5,000,000 and CDC/504 up to $5,500,000—reducing credit risk and improving loan economics. Clients receive more favorable terms and advisory support from SBA resources, while the bank deepens its role with growth-stage businesses.

- Guarantees: SBA 85%/75%

- Max loan sizes: 7(a) $5M, 504 $5.5M

- Benefit: lower risk, better pricing

- Outcome: stronger ties with growth-stage firms

Appraisers, brokers, advisors

Alliances with CRE appraisers, brokers, CPAs and attorneys streamline Five Star Bank deal execution, improving underwriting quality and reducing time-to-close; broker-originated deals accounted for about 60% of CRE loan flow in 2024, accelerating origination pipelines. Trusted advisors channel qualified leads and reduce credit risk, contributing to faster, higher-confidence approvals and stronger end-to-end client solutions.

- 60% 2024 broker-originated CRE loan flow

- Improved underwriting speed and quality

- Trusted advisors = higher-quality referrals

Partnerships, SBA guarantees and vendors drive SME pipelines, scale and lower credit risk

Five Star’s partnerships with chambers, advisors and SBA programs expand SME pipelines and lower credit risk (99.9% US firms small, SBA 2024; SBA 7(a) guarantees 85%/75%, max $5M/$5.5M). Tech and security vendors enable scalable digital services (78% banks cite third‑party critical, Deloitte 2024). Correspondents and brokers boost capacity and originations (syndicated loans ~$1.2T 2023; 60% CRE broker originations 2024).

| Partner | Key stat | Benefit |

|---|---|---|

| SBA | 85%/75% guarantees; $5M/$5.5M caps | Lower risk, better pricing |

| Vendors | 78% banks rely on them (2024) | Scale digital services |

| Correspondents/Brokers | $1.2T syndicated (2023); 60% CRE (2024) | Capacity, originations |

What is included in the product

A comprehensive Business Model Canvas for Five Star Bank, organized into the 9 classic blocks with detailed value propositions, customer segments, channels, revenue streams, and operational insights. Includes competitive analysis and SWOT-linked recommendations, ideal for presentations, investor discussions, and strategic validation using real-world bank data.

Condenses Five Star Bank's strategy into a digestible one-page Business Model Canvas with editable cells, saving hours of formatting and structuring your own model. Great for quick board-ready summaries, team collaboration, and comparing multiple banking models side-by-side.

Activities

Commercial credit origination

Commercial credit origination at Five Star Bank covers prospecting, underwriting, and closing for SMBs and middle-market firms across C&I, owner-occupied CRE, investor CRE, and SBA products, with emphasis on prudent structuring and timely decisions. Underwriters apply risk-adjusted pricing and covenant design to preserve capital. Ongoing portfolio monitoring, stress testing, and regular reviews maintain credit health and early remediation.

Treasury and cash management

Treasury and cash management delivers ACH, wires, lockbox, RDC and liquidity solutions to optimize clients’ working capital and payments; U.S. ACH volumes surpassed 33.4 billion transactions in 2024, underscoring digital payment scale. These services can accelerate cash conversion by 2–4 days, while layered controls and MFA reduce fraud risk substantially. Packages are tailored by industry and cash-flow profile.

Deposit gathering

Acquire and retain operating and savings balances by targeting low-cost, stable funding from businesses and individuals; in 2024 Five Star Bank prioritized relationship pricing, fee waivers, and digital onboarding to deepen balances. Pricing, enhanced treasury services, and mobile tools are used to convert transaction balances into long-term deposits. Deposit mix is actively aligned with asset growth to manage funding cost and liquidity.

Risk, compliance, and AML

Five Star Bank conducts KYC, BSA/AML screening and ongoing risk assessments, maintains quarterly regulatory reporting and annual external audits, and enforces credit, liquidity, and interest rate risk frameworks aligned with supervisory guidance; staff receive mandatory compliance training and controls are monitored continuously to detect anomalies.

- KYC/BSA/AML ongoing monitoring

- Quarterly regulatory reporting & annual audits

- Credit, liquidity & interest-rate risk frameworks

- Continuous controls monitoring & staff training

Relationship development

Relationship development combines high-touch coverage by experienced bankers with frequent check-ins, portfolio reviews and targeted cross-sell; community involvement raises visibility and trust while data-driven outreach boosts share of wallet—community banks held about 20% of U.S. deposits in 2024 (FDIC).

- High-touch coverage — experienced bankers

- Frequent check-ins & reviews

- Cross-sell driven by CRM analytics

- Community events to build trust

Commercial lending and treasury speed cash conversion 2-4 days; ACH 33.4B, community banks 20%

Five Star Bank originates commercial credit across C&I, owner/investor CRE and SBA with risk-adjusted pricing and portfolio stress testing; ongoing monitoring and remediation preserve asset quality. Treasury delivers ACH, wires, lockbox and RDC to speed cash conversion 2–4 days; U.S. ACH volumes hit 33.4B in 2024. Relationship managers drive deposits via pricing, fee waivers and digital onboarding; community banks held 20% of U.S. deposits in 2024.

| Metric | 2024 |

|---|---|

| U.S. ACH volume | 33.4B |

| Cash conversion improvement | 2–4 days |

| Community bank deposit share | 20% |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview shown here is the exact Five Star Bank document you’ll receive—this is not a mockup or teaser. When you purchase, you’ll get the same complete, professionally formatted file (editable Word and Excel) ready to present, edit, and share. We deliver no surprises—what you see is what you own.

Business Model Canvas for a leading regional bank - Word and Excel ready

Unlock the full strategic blueprint behind Five Star Bank with our complete Business Model Canvas — three to five detailed sentences condense its value propositions, key partners, revenue streams, and growth levers into actionable insights. Ideal for investors, consultants, and founders, the downloadable Word and Excel files are ready for benchmarking and strategy work. Purchase now to see every section, metrics, and tactical recommendations.

Partnerships

Local business networks

Partnerships with chambers of commerce and industry associations extend Five Star Bank’s reach into regional businesses, driving referrals and joint educational events that deepen customer pipelines. These alliances reinforce the bank’s community presence and credibility. They also surface early intelligence on local economic trends, critical given that 99.9% of US firms are small businesses (SBA 2024).

Fintech and core vendors

Relationships with core banking, payments, and cybersecurity providers power Five Star Bank’s digital services, enabling online lending, card processing, and 24/7 fraud monitoring. Vendors support integrations for treasury, ACH, and remote deposit capture, connecting bank workflows to industry rails. Joint roadmaps improve reliability and user experience and, per Deloitte 2024, 78% of banks cite third‑party partnerships as critical to digital transformation. They let the bank scale securely without owning all tech.

Correspondent banks

Correspondent banks enable syndications, participations and specialized services, letting Five Star Bank originate larger credits while sharing risk through partners; global syndicated loan activity was about $1.2 trillion in 2023 per Refinitiv. They expand lending capacity for bigger borrowers without diluting client relationship ownership. Correspondents supply liquidity and foreign-exchange rails—SWIFT processed ~40 million messages/day in 2024—extending product breadth.

Government & SBA programs

Partnering with SBA and state programs gives Five Star Bank access to government-guaranteed lending—SBA 7(a) guarantees up to 85% for loans ≤150,000 and 75% for loans >150,000, with 7(a) max loan size $5,000,000 and CDC/504 up to $5,500,000—reducing credit risk and improving loan economics. Clients receive more favorable terms and advisory support from SBA resources, while the bank deepens its role with growth-stage businesses.

- Guarantees: SBA 85%/75%

- Max loan sizes: 7(a) $5M, 504 $5.5M

- Benefit: lower risk, better pricing

- Outcome: stronger ties with growth-stage firms

Appraisers, brokers, advisors

Alliances with CRE appraisers, brokers, CPAs and attorneys streamline Five Star Bank deal execution, improving underwriting quality and reducing time-to-close; broker-originated deals accounted for about 60% of CRE loan flow in 2024, accelerating origination pipelines. Trusted advisors channel qualified leads and reduce credit risk, contributing to faster, higher-confidence approvals and stronger end-to-end client solutions.

- 60% 2024 broker-originated CRE loan flow

- Improved underwriting speed and quality

- Trusted advisors = higher-quality referrals

Partnerships, SBA guarantees and vendors drive SME pipelines, scale and lower credit risk

Five Star’s partnerships with chambers, advisors and SBA programs expand SME pipelines and lower credit risk (99.9% US firms small, SBA 2024; SBA 7(a) guarantees 85%/75%, max $5M/$5.5M). Tech and security vendors enable scalable digital services (78% banks cite third‑party critical, Deloitte 2024). Correspondents and brokers boost capacity and originations (syndicated loans ~$1.2T 2023; 60% CRE broker originations 2024).

| Partner | Key stat | Benefit |

|---|---|---|

| SBA | 85%/75% guarantees; $5M/$5.5M caps | Lower risk, better pricing |

| Vendors | 78% banks rely on them (2024) | Scale digital services |

| Correspondents/Brokers | $1.2T syndicated (2023); 60% CRE (2024) | Capacity, originations |

What is included in the product

A comprehensive Business Model Canvas for Five Star Bank, organized into the 9 classic blocks with detailed value propositions, customer segments, channels, revenue streams, and operational insights. Includes competitive analysis and SWOT-linked recommendations, ideal for presentations, investor discussions, and strategic validation using real-world bank data.

Condenses Five Star Bank's strategy into a digestible one-page Business Model Canvas with editable cells, saving hours of formatting and structuring your own model. Great for quick board-ready summaries, team collaboration, and comparing multiple banking models side-by-side.

Activities

Commercial credit origination

Commercial credit origination at Five Star Bank covers prospecting, underwriting, and closing for SMBs and middle-market firms across C&I, owner-occupied CRE, investor CRE, and SBA products, with emphasis on prudent structuring and timely decisions. Underwriters apply risk-adjusted pricing and covenant design to preserve capital. Ongoing portfolio monitoring, stress testing, and regular reviews maintain credit health and early remediation.

Treasury and cash management

Treasury and cash management delivers ACH, wires, lockbox, RDC and liquidity solutions to optimize clients’ working capital and payments; U.S. ACH volumes surpassed 33.4 billion transactions in 2024, underscoring digital payment scale. These services can accelerate cash conversion by 2–4 days, while layered controls and MFA reduce fraud risk substantially. Packages are tailored by industry and cash-flow profile.

Deposit gathering

Acquire and retain operating and savings balances by targeting low-cost, stable funding from businesses and individuals; in 2024 Five Star Bank prioritized relationship pricing, fee waivers, and digital onboarding to deepen balances. Pricing, enhanced treasury services, and mobile tools are used to convert transaction balances into long-term deposits. Deposit mix is actively aligned with asset growth to manage funding cost and liquidity.

Risk, compliance, and AML

Five Star Bank conducts KYC, BSA/AML screening and ongoing risk assessments, maintains quarterly regulatory reporting and annual external audits, and enforces credit, liquidity, and interest rate risk frameworks aligned with supervisory guidance; staff receive mandatory compliance training and controls are monitored continuously to detect anomalies.

- KYC/BSA/AML ongoing monitoring

- Quarterly regulatory reporting & annual audits

- Credit, liquidity & interest-rate risk frameworks

- Continuous controls monitoring & staff training

Relationship development

Relationship development combines high-touch coverage by experienced bankers with frequent check-ins, portfolio reviews and targeted cross-sell; community involvement raises visibility and trust while data-driven outreach boosts share of wallet—community banks held about 20% of U.S. deposits in 2024 (FDIC).

- High-touch coverage — experienced bankers

- Frequent check-ins & reviews

- Cross-sell driven by CRM analytics

- Community events to build trust

Commercial lending and treasury speed cash conversion 2-4 days; ACH 33.4B, community banks 20%

Five Star Bank originates commercial credit across C&I, owner/investor CRE and SBA with risk-adjusted pricing and portfolio stress testing; ongoing monitoring and remediation preserve asset quality. Treasury delivers ACH, wires, lockbox and RDC to speed cash conversion 2–4 days; U.S. ACH volumes hit 33.4B in 2024. Relationship managers drive deposits via pricing, fee waivers and digital onboarding; community banks held 20% of U.S. deposits in 2024.

| Metric | 2024 |

|---|---|

| U.S. ACH volume | 33.4B |

| Cash conversion improvement | 2–4 days |

| Community bank deposit share | 20% |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview shown here is the exact Five Star Bank document you’ll receive—this is not a mockup or teaser. When you purchase, you’ll get the same complete, professionally formatted file (editable Word and Excel) ready to present, edit, and share. We deliver no surprises—what you see is what you own.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas for a leading regional bank - Word and Excel ready

Unlock the full strategic blueprint behind Five Star Bank with our complete Business Model Canvas — three to five detailed sentences condense its value propositions, key partners, revenue streams, and growth levers into actionable insights. Ideal for investors, consultants, and founders, the downloadable Word and Excel files are ready for benchmarking and strategy work. Purchase now to see every section, metrics, and tactical recommendations.

Partnerships

Local business networks

Partnerships with chambers of commerce and industry associations extend Five Star Bank’s reach into regional businesses, driving referrals and joint educational events that deepen customer pipelines. These alliances reinforce the bank’s community presence and credibility. They also surface early intelligence on local economic trends, critical given that 99.9% of US firms are small businesses (SBA 2024).

Fintech and core vendors

Relationships with core banking, payments, and cybersecurity providers power Five Star Bank’s digital services, enabling online lending, card processing, and 24/7 fraud monitoring. Vendors support integrations for treasury, ACH, and remote deposit capture, connecting bank workflows to industry rails. Joint roadmaps improve reliability and user experience and, per Deloitte 2024, 78% of banks cite third‑party partnerships as critical to digital transformation. They let the bank scale securely without owning all tech.

Correspondent banks

Correspondent banks enable syndications, participations and specialized services, letting Five Star Bank originate larger credits while sharing risk through partners; global syndicated loan activity was about $1.2 trillion in 2023 per Refinitiv. They expand lending capacity for bigger borrowers without diluting client relationship ownership. Correspondents supply liquidity and foreign-exchange rails—SWIFT processed ~40 million messages/day in 2024—extending product breadth.

Government & SBA programs

Partnering with SBA and state programs gives Five Star Bank access to government-guaranteed lending—SBA 7(a) guarantees up to 85% for loans ≤150,000 and 75% for loans >150,000, with 7(a) max loan size $5,000,000 and CDC/504 up to $5,500,000—reducing credit risk and improving loan economics. Clients receive more favorable terms and advisory support from SBA resources, while the bank deepens its role with growth-stage businesses.

- Guarantees: SBA 85%/75%

- Max loan sizes: 7(a) $5M, 504 $5.5M

- Benefit: lower risk, better pricing

- Outcome: stronger ties with growth-stage firms

Appraisers, brokers, advisors

Alliances with CRE appraisers, brokers, CPAs and attorneys streamline Five Star Bank deal execution, improving underwriting quality and reducing time-to-close; broker-originated deals accounted for about 60% of CRE loan flow in 2024, accelerating origination pipelines. Trusted advisors channel qualified leads and reduce credit risk, contributing to faster, higher-confidence approvals and stronger end-to-end client solutions.

- 60% 2024 broker-originated CRE loan flow

- Improved underwriting speed and quality

- Trusted advisors = higher-quality referrals

Partnerships, SBA guarantees and vendors drive SME pipelines, scale and lower credit risk

Five Star’s partnerships with chambers, advisors and SBA programs expand SME pipelines and lower credit risk (99.9% US firms small, SBA 2024; SBA 7(a) guarantees 85%/75%, max $5M/$5.5M). Tech and security vendors enable scalable digital services (78% banks cite third‑party critical, Deloitte 2024). Correspondents and brokers boost capacity and originations (syndicated loans ~$1.2T 2023; 60% CRE broker originations 2024).

| Partner | Key stat | Benefit |

|---|---|---|

| SBA | 85%/75% guarantees; $5M/$5.5M caps | Lower risk, better pricing |

| Vendors | 78% banks rely on them (2024) | Scale digital services |

| Correspondents/Brokers | $1.2T syndicated (2023); 60% CRE (2024) | Capacity, originations |

What is included in the product

A comprehensive Business Model Canvas for Five Star Bank, organized into the 9 classic blocks with detailed value propositions, customer segments, channels, revenue streams, and operational insights. Includes competitive analysis and SWOT-linked recommendations, ideal for presentations, investor discussions, and strategic validation using real-world bank data.

Condenses Five Star Bank's strategy into a digestible one-page Business Model Canvas with editable cells, saving hours of formatting and structuring your own model. Great for quick board-ready summaries, team collaboration, and comparing multiple banking models side-by-side.

Activities

Commercial credit origination

Commercial credit origination at Five Star Bank covers prospecting, underwriting, and closing for SMBs and middle-market firms across C&I, owner-occupied CRE, investor CRE, and SBA products, with emphasis on prudent structuring and timely decisions. Underwriters apply risk-adjusted pricing and covenant design to preserve capital. Ongoing portfolio monitoring, stress testing, and regular reviews maintain credit health and early remediation.

Treasury and cash management

Treasury and cash management delivers ACH, wires, lockbox, RDC and liquidity solutions to optimize clients’ working capital and payments; U.S. ACH volumes surpassed 33.4 billion transactions in 2024, underscoring digital payment scale. These services can accelerate cash conversion by 2–4 days, while layered controls and MFA reduce fraud risk substantially. Packages are tailored by industry and cash-flow profile.

Deposit gathering

Acquire and retain operating and savings balances by targeting low-cost, stable funding from businesses and individuals; in 2024 Five Star Bank prioritized relationship pricing, fee waivers, and digital onboarding to deepen balances. Pricing, enhanced treasury services, and mobile tools are used to convert transaction balances into long-term deposits. Deposit mix is actively aligned with asset growth to manage funding cost and liquidity.

Risk, compliance, and AML

Five Star Bank conducts KYC, BSA/AML screening and ongoing risk assessments, maintains quarterly regulatory reporting and annual external audits, and enforces credit, liquidity, and interest rate risk frameworks aligned with supervisory guidance; staff receive mandatory compliance training and controls are monitored continuously to detect anomalies.

- KYC/BSA/AML ongoing monitoring

- Quarterly regulatory reporting & annual audits

- Credit, liquidity & interest-rate risk frameworks

- Continuous controls monitoring & staff training

Relationship development

Relationship development combines high-touch coverage by experienced bankers with frequent check-ins, portfolio reviews and targeted cross-sell; community involvement raises visibility and trust while data-driven outreach boosts share of wallet—community banks held about 20% of U.S. deposits in 2024 (FDIC).

- High-touch coverage — experienced bankers

- Frequent check-ins & reviews

- Cross-sell driven by CRM analytics

- Community events to build trust

Commercial lending and treasury speed cash conversion 2-4 days; ACH 33.4B, community banks 20%

Five Star Bank originates commercial credit across C&I, owner/investor CRE and SBA with risk-adjusted pricing and portfolio stress testing; ongoing monitoring and remediation preserve asset quality. Treasury delivers ACH, wires, lockbox and RDC to speed cash conversion 2–4 days; U.S. ACH volumes hit 33.4B in 2024. Relationship managers drive deposits via pricing, fee waivers and digital onboarding; community banks held 20% of U.S. deposits in 2024.

| Metric | 2024 |

|---|---|

| U.S. ACH volume | 33.4B |

| Cash conversion improvement | 2–4 days |

| Community bank deposit share | 20% |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview shown here is the exact Five Star Bank document you’ll receive—this is not a mockup or teaser. When you purchase, you’ll get the same complete, professionally formatted file (editable Word and Excel) ready to present, edit, and share. We deliver no surprises—what you see is what you own.