Five Star Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

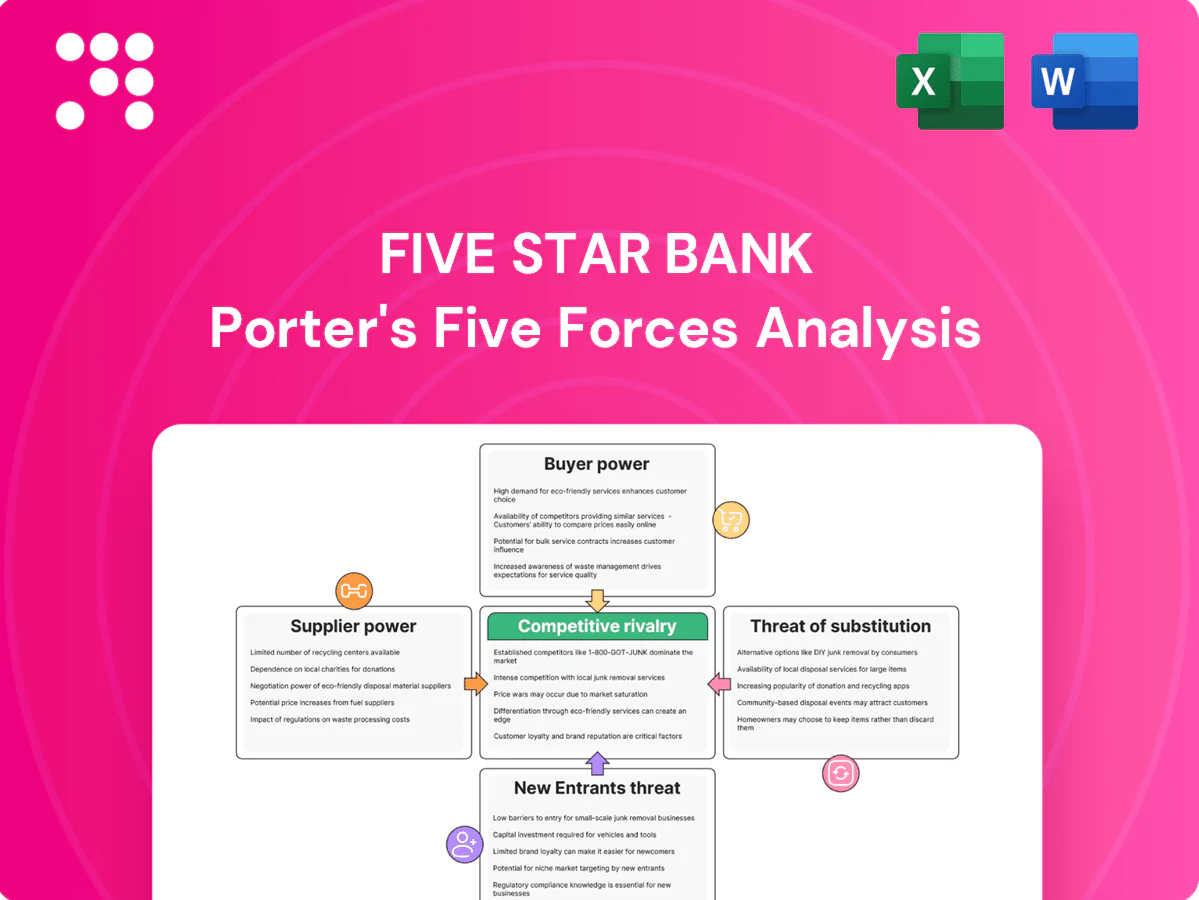

Five Star Bank faces moderate buyer power, intense regional rivalry, low supplier leverage, and entry barriers driven by regulation and capital needs. This snapshot outlines core competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Five Star Bank.

Suppliers Bargaining Power

Core tech vendors

Five Star Bank depends on concentrated core banking and payment vendors (Fiserv $17.3B 2023 revenue, FIS $13.9B 2023) and card networks (Visa/Mastercard ~85% global card volume), giving suppliers pricing leverage; core migrations typically take 12–36 months and cost millions, raising switching costs and risk. Multi-vendor strategies and staggered contract cycles can dilute leverage, while OCC/FDIC/Fed third‑party risk rules and heightened 2024 supervisory scrutiny limit supplier behavior.

Deposit funding base

Depositors are key funding suppliers; with the fed funds target at 5.25–5.50% in 2024, rate-sensitive balances forced higher deposit yields, raising interest expense and compressing NIM. Local business relationship deposits are stickier and reduce funding volatility. Diversification by segment and product limits single-source dependence and beta exposure.

Wholesale and FHLB lines

Access to FHLB advances and brokered deposits gives Five Star Bank contingent liquidity but at market-driven costs tied to policy rates; the fed funds target was 5.25–5.50% in 2024, lifting wholesale funding spreads. In stress, FHLB haircuts and brokered-deposit pricing can widen, increasing supplier power. Prudent collateral management, multi-counterparty lines and liquidity buffers reduce reliance and concentration risk.

Talent and specialized lenders

Experienced relationship bankers and credit underwriters are scarce in California, where 2024 BLS data shows financial managers averaged about 165,010 USD and loan officers near 99,000 USD, driving competition for talent and raising compensation and retention costs, which strengthens supplier power. Culture, equity incentives and clear career pathways can mitigate leverage, while automation lowers workload but cannot fully replace judgment-intensive credit expertise.

- Scarcity: experienced underwriters concentrated in CA

- Cost: 2024 avg compensation for financial managers ~165,010 USD

- Mitigation: equity, culture, career ladders

- Automation: reduces pressure but not expert judgment

Payment networks and data providers

Payment networks and data providers wield significant supplier power: the card duopoly (Visa + Mastercard) handles roughly 80% of global card volume, NACHA processed over 30 billion ACH payments in 2023, and the three credit bureaus supply >90% of consumer credit data, leaving few substitutes. Compliance, certification and integration costs raise switching barriers for Five Star Bank, though volume rebates and consortium purchasing can soften fees. Open banking and RTP growth in 2024 provide modest countervailing power but have not displaced core rails.

- Card duopoly ~80% share

- NACHA >30B ACH (2023)

- 3 bureaus >90% data

- High integration/compliance costs

- Rebates/consortia lower fees

- Open banking/RTP = modest counterweight

Card duopoly ~85%, supplier power; swaps 12–36 months

Five Star faces strong supplier power from core vendors (Fiserv/FIS) and card rails (Visa/Mastercard ~85% volume), raising switching costs; core swaps cost $m–$10s m and take 12–36 months. Depositor funding (fed funds 5.25–5.50% in 2024) and FHLB/brokered markets lift funding costs. CA talent scarcity (2024 avg mgr comp ~165,010 USD) increases labor pressure.

| Item | 2024 Metric |

|---|---|

| Card duopoly share | ~85% |

| Fed funds | 5.25–5.50% |

| Mgr avg comp CA | 165,010 USD |

What is included in the product

Tailored Porter’s Five Forces analysis for Five Star Bank uncovering competitive drivers, buyer/supplier power, substitute threats, and entry barriers; includes strategic commentary on disruptive entrants and market dynamics to inform investor materials and internal strategy.

Concise Porter's Five Forces for Five Star Bank—translates competitive pressures into clear ratings and a radar chart for instant strategic insight, ready to drop into decks or dashboards.

Customers Bargaining Power

Commercial clients

Middle-market commercial clients, with ticket sizes often >$1m, exert strong bargaining power in 2024 and can negotiate rates and covenant flexibility. Bundling treasury and payments increases stickiness but typically requires fee or rate concessions. Competitors readily provide rapid quotes, raising buyer leverage. Deep relationships and local decisioning remain key defenses of margin.

Rate-sensitive depositors

Rate-sensitive depositors can switch for higher APYs with low friction; top online savings APYs reached about 4.60% in 2024 while the national average sat near 0.40% (Bankrate/2024), amplifying outflows risk for Five Star. Digital comparison tools are used by roughly 60% of savers (2024 surveys), increasing transparency and bargaining power. Offering value-added services and behavioral segmentation enables targeted pricing to reduce pure rate shopping.

Credit quality tiers

Prime borrowers attract multiple offers, compressing spreads and fee income as lenders compete in a market where the US prime rate stood at 8.5% in 2024. Weaker credits have fewer alternatives but demand higher monitoring and provisioning, raising marginal servicing costs. Five Star uses risk-adjusted pricing to limit concessions and applies portfolio limits to curb adverse selection and concentration risk.

Institutional and public entities

Institutional and public entities exert strong bargaining power over Five Star Bank as municipal and institutional deposits commonly require collateralization and fee waivers, and RFP-driven procurement increases buyer leverage; winning mandates raises deposit balances but typically compresses yields due to negotiated pricing and service credits.

- Collateralization requirements

- RFPs increase leverage

- Mandates boost balances, lower yields

- Differentiation: reliability and compliance

Switching costs and UX

Digital onboarding and treasury integration at Five Star reduce switching friction by enabling same-day migration of cash workflows, while API connectivity can lock in client processes and raise stickiness; superior client service often offsets price sensitivity. Data portability rules such as the EU Data Act (2024) increase buyer power over time by mandating wider access to account and transaction data.

- Low switching friction: digital onboarding, treasury links

- High stickiness: API workflow lock-in

- Service balance: reduces churn despite price gaps

- Regulatory risk: EU Data Act 2024 boosts portability

Deposit power: 4.60% top APY; ~60% use digital tools; prime 8.5% compresses spreads

Middle-market clients (>1m) and institutional depositors exert strong bargaining power in 2024, negotiating rates and covenants. Rate-sensitive savers can switch for top online APYs near 4.60% versus national avg 0.40% (Bankrate/2024). Prime at 8.5% compresses spreads; ~60% of savers use digital comparison tools (2024 surveys).

| Metric | 2024 value |

|---|---|

| Top online savings APY | 4.60% |

| National avg savings APY | 0.40% |

| US prime rate | 8.5% |

| Digital comparison use | ~60% |

What You See Is What You Get

Five Star Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Five Star Bank you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for immediate download and use. It contains actionable insights on industry rivalry, buyer/supplier power, threats of entry and substitutes.

A Must-Have Tool for Decision-Makers

Five Star Bank faces moderate buyer power, intense regional rivalry, low supplier leverage, and entry barriers driven by regulation and capital needs. This snapshot outlines core competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Five Star Bank.

Suppliers Bargaining Power

Core tech vendors

Five Star Bank depends on concentrated core banking and payment vendors (Fiserv $17.3B 2023 revenue, FIS $13.9B 2023) and card networks (Visa/Mastercard ~85% global card volume), giving suppliers pricing leverage; core migrations typically take 12–36 months and cost millions, raising switching costs and risk. Multi-vendor strategies and staggered contract cycles can dilute leverage, while OCC/FDIC/Fed third‑party risk rules and heightened 2024 supervisory scrutiny limit supplier behavior.

Deposit funding base

Depositors are key funding suppliers; with the fed funds target at 5.25–5.50% in 2024, rate-sensitive balances forced higher deposit yields, raising interest expense and compressing NIM. Local business relationship deposits are stickier and reduce funding volatility. Diversification by segment and product limits single-source dependence and beta exposure.

Wholesale and FHLB lines

Access to FHLB advances and brokered deposits gives Five Star Bank contingent liquidity but at market-driven costs tied to policy rates; the fed funds target was 5.25–5.50% in 2024, lifting wholesale funding spreads. In stress, FHLB haircuts and brokered-deposit pricing can widen, increasing supplier power. Prudent collateral management, multi-counterparty lines and liquidity buffers reduce reliance and concentration risk.

Talent and specialized lenders

Experienced relationship bankers and credit underwriters are scarce in California, where 2024 BLS data shows financial managers averaged about 165,010 USD and loan officers near 99,000 USD, driving competition for talent and raising compensation and retention costs, which strengthens supplier power. Culture, equity incentives and clear career pathways can mitigate leverage, while automation lowers workload but cannot fully replace judgment-intensive credit expertise.

- Scarcity: experienced underwriters concentrated in CA

- Cost: 2024 avg compensation for financial managers ~165,010 USD

- Mitigation: equity, culture, career ladders

- Automation: reduces pressure but not expert judgment

Payment networks and data providers

Payment networks and data providers wield significant supplier power: the card duopoly (Visa + Mastercard) handles roughly 80% of global card volume, NACHA processed over 30 billion ACH payments in 2023, and the three credit bureaus supply >90% of consumer credit data, leaving few substitutes. Compliance, certification and integration costs raise switching barriers for Five Star Bank, though volume rebates and consortium purchasing can soften fees. Open banking and RTP growth in 2024 provide modest countervailing power but have not displaced core rails.

- Card duopoly ~80% share

- NACHA >30B ACH (2023)

- 3 bureaus >90% data

- High integration/compliance costs

- Rebates/consortia lower fees

- Open banking/RTP = modest counterweight

Card duopoly ~85%, supplier power; swaps 12–36 months

Five Star faces strong supplier power from core vendors (Fiserv/FIS) and card rails (Visa/Mastercard ~85% volume), raising switching costs; core swaps cost $m–$10s m and take 12–36 months. Depositor funding (fed funds 5.25–5.50% in 2024) and FHLB/brokered markets lift funding costs. CA talent scarcity (2024 avg mgr comp ~165,010 USD) increases labor pressure.

| Item | 2024 Metric |

|---|---|

| Card duopoly share | ~85% |

| Fed funds | 5.25–5.50% |

| Mgr avg comp CA | 165,010 USD |

What is included in the product

Tailored Porter’s Five Forces analysis for Five Star Bank uncovering competitive drivers, buyer/supplier power, substitute threats, and entry barriers; includes strategic commentary on disruptive entrants and market dynamics to inform investor materials and internal strategy.

Concise Porter's Five Forces for Five Star Bank—translates competitive pressures into clear ratings and a radar chart for instant strategic insight, ready to drop into decks or dashboards.

Customers Bargaining Power

Commercial clients

Middle-market commercial clients, with ticket sizes often >$1m, exert strong bargaining power in 2024 and can negotiate rates and covenant flexibility. Bundling treasury and payments increases stickiness but typically requires fee or rate concessions. Competitors readily provide rapid quotes, raising buyer leverage. Deep relationships and local decisioning remain key defenses of margin.

Rate-sensitive depositors

Rate-sensitive depositors can switch for higher APYs with low friction; top online savings APYs reached about 4.60% in 2024 while the national average sat near 0.40% (Bankrate/2024), amplifying outflows risk for Five Star. Digital comparison tools are used by roughly 60% of savers (2024 surveys), increasing transparency and bargaining power. Offering value-added services and behavioral segmentation enables targeted pricing to reduce pure rate shopping.

Credit quality tiers

Prime borrowers attract multiple offers, compressing spreads and fee income as lenders compete in a market where the US prime rate stood at 8.5% in 2024. Weaker credits have fewer alternatives but demand higher monitoring and provisioning, raising marginal servicing costs. Five Star uses risk-adjusted pricing to limit concessions and applies portfolio limits to curb adverse selection and concentration risk.

Institutional and public entities

Institutional and public entities exert strong bargaining power over Five Star Bank as municipal and institutional deposits commonly require collateralization and fee waivers, and RFP-driven procurement increases buyer leverage; winning mandates raises deposit balances but typically compresses yields due to negotiated pricing and service credits.

- Collateralization requirements

- RFPs increase leverage

- Mandates boost balances, lower yields

- Differentiation: reliability and compliance

Switching costs and UX

Digital onboarding and treasury integration at Five Star reduce switching friction by enabling same-day migration of cash workflows, while API connectivity can lock in client processes and raise stickiness; superior client service often offsets price sensitivity. Data portability rules such as the EU Data Act (2024) increase buyer power over time by mandating wider access to account and transaction data.

- Low switching friction: digital onboarding, treasury links

- High stickiness: API workflow lock-in

- Service balance: reduces churn despite price gaps

- Regulatory risk: EU Data Act 2024 boosts portability

Deposit power: 4.60% top APY; ~60% use digital tools; prime 8.5% compresses spreads

Middle-market clients (>1m) and institutional depositors exert strong bargaining power in 2024, negotiating rates and covenants. Rate-sensitive savers can switch for top online APYs near 4.60% versus national avg 0.40% (Bankrate/2024). Prime at 8.5% compresses spreads; ~60% of savers use digital comparison tools (2024 surveys).

| Metric | 2024 value |

|---|---|

| Top online savings APY | 4.60% |

| National avg savings APY | 0.40% |

| US prime rate | 8.5% |

| Digital comparison use | ~60% |

What You See Is What You Get

Five Star Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Five Star Bank you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for immediate download and use. It contains actionable insights on industry rivalry, buyer/supplier power, threats of entry and substitutes.

Description

A Must-Have Tool for Decision-Makers

Five Star Bank faces moderate buyer power, intense regional rivalry, low supplier leverage, and entry barriers driven by regulation and capital needs. This snapshot outlines core competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Five Star Bank.

Suppliers Bargaining Power

Core tech vendors

Five Star Bank depends on concentrated core banking and payment vendors (Fiserv $17.3B 2023 revenue, FIS $13.9B 2023) and card networks (Visa/Mastercard ~85% global card volume), giving suppliers pricing leverage; core migrations typically take 12–36 months and cost millions, raising switching costs and risk. Multi-vendor strategies and staggered contract cycles can dilute leverage, while OCC/FDIC/Fed third‑party risk rules and heightened 2024 supervisory scrutiny limit supplier behavior.

Deposit funding base

Depositors are key funding suppliers; with the fed funds target at 5.25–5.50% in 2024, rate-sensitive balances forced higher deposit yields, raising interest expense and compressing NIM. Local business relationship deposits are stickier and reduce funding volatility. Diversification by segment and product limits single-source dependence and beta exposure.

Wholesale and FHLB lines

Access to FHLB advances and brokered deposits gives Five Star Bank contingent liquidity but at market-driven costs tied to policy rates; the fed funds target was 5.25–5.50% in 2024, lifting wholesale funding spreads. In stress, FHLB haircuts and brokered-deposit pricing can widen, increasing supplier power. Prudent collateral management, multi-counterparty lines and liquidity buffers reduce reliance and concentration risk.

Talent and specialized lenders

Experienced relationship bankers and credit underwriters are scarce in California, where 2024 BLS data shows financial managers averaged about 165,010 USD and loan officers near 99,000 USD, driving competition for talent and raising compensation and retention costs, which strengthens supplier power. Culture, equity incentives and clear career pathways can mitigate leverage, while automation lowers workload but cannot fully replace judgment-intensive credit expertise.

- Scarcity: experienced underwriters concentrated in CA

- Cost: 2024 avg compensation for financial managers ~165,010 USD

- Mitigation: equity, culture, career ladders

- Automation: reduces pressure but not expert judgment

Payment networks and data providers

Payment networks and data providers wield significant supplier power: the card duopoly (Visa + Mastercard) handles roughly 80% of global card volume, NACHA processed over 30 billion ACH payments in 2023, and the three credit bureaus supply >90% of consumer credit data, leaving few substitutes. Compliance, certification and integration costs raise switching barriers for Five Star Bank, though volume rebates and consortium purchasing can soften fees. Open banking and RTP growth in 2024 provide modest countervailing power but have not displaced core rails.

- Card duopoly ~80% share

- NACHA >30B ACH (2023)

- 3 bureaus >90% data

- High integration/compliance costs

- Rebates/consortia lower fees

- Open banking/RTP = modest counterweight

Card duopoly ~85%, supplier power; swaps 12–36 months

Five Star faces strong supplier power from core vendors (Fiserv/FIS) and card rails (Visa/Mastercard ~85% volume), raising switching costs; core swaps cost $m–$10s m and take 12–36 months. Depositor funding (fed funds 5.25–5.50% in 2024) and FHLB/brokered markets lift funding costs. CA talent scarcity (2024 avg mgr comp ~165,010 USD) increases labor pressure.

| Item | 2024 Metric |

|---|---|

| Card duopoly share | ~85% |

| Fed funds | 5.25–5.50% |

| Mgr avg comp CA | 165,010 USD |

What is included in the product

Tailored Porter’s Five Forces analysis for Five Star Bank uncovering competitive drivers, buyer/supplier power, substitute threats, and entry barriers; includes strategic commentary on disruptive entrants and market dynamics to inform investor materials and internal strategy.

Concise Porter's Five Forces for Five Star Bank—translates competitive pressures into clear ratings and a radar chart for instant strategic insight, ready to drop into decks or dashboards.

Customers Bargaining Power

Commercial clients

Middle-market commercial clients, with ticket sizes often >$1m, exert strong bargaining power in 2024 and can negotiate rates and covenant flexibility. Bundling treasury and payments increases stickiness but typically requires fee or rate concessions. Competitors readily provide rapid quotes, raising buyer leverage. Deep relationships and local decisioning remain key defenses of margin.

Rate-sensitive depositors

Rate-sensitive depositors can switch for higher APYs with low friction; top online savings APYs reached about 4.60% in 2024 while the national average sat near 0.40% (Bankrate/2024), amplifying outflows risk for Five Star. Digital comparison tools are used by roughly 60% of savers (2024 surveys), increasing transparency and bargaining power. Offering value-added services and behavioral segmentation enables targeted pricing to reduce pure rate shopping.

Credit quality tiers

Prime borrowers attract multiple offers, compressing spreads and fee income as lenders compete in a market where the US prime rate stood at 8.5% in 2024. Weaker credits have fewer alternatives but demand higher monitoring and provisioning, raising marginal servicing costs. Five Star uses risk-adjusted pricing to limit concessions and applies portfolio limits to curb adverse selection and concentration risk.

Institutional and public entities

Institutional and public entities exert strong bargaining power over Five Star Bank as municipal and institutional deposits commonly require collateralization and fee waivers, and RFP-driven procurement increases buyer leverage; winning mandates raises deposit balances but typically compresses yields due to negotiated pricing and service credits.

- Collateralization requirements

- RFPs increase leverage

- Mandates boost balances, lower yields

- Differentiation: reliability and compliance

Switching costs and UX

Digital onboarding and treasury integration at Five Star reduce switching friction by enabling same-day migration of cash workflows, while API connectivity can lock in client processes and raise stickiness; superior client service often offsets price sensitivity. Data portability rules such as the EU Data Act (2024) increase buyer power over time by mandating wider access to account and transaction data.

- Low switching friction: digital onboarding, treasury links

- High stickiness: API workflow lock-in

- Service balance: reduces churn despite price gaps

- Regulatory risk: EU Data Act 2024 boosts portability

Deposit power: 4.60% top APY; ~60% use digital tools; prime 8.5% compresses spreads

Middle-market clients (>1m) and institutional depositors exert strong bargaining power in 2024, negotiating rates and covenants. Rate-sensitive savers can switch for top online APYs near 4.60% versus national avg 0.40% (Bankrate/2024). Prime at 8.5% compresses spreads; ~60% of savers use digital comparison tools (2024 surveys).

| Metric | 2024 value |

|---|---|

| Top online savings APY | 4.60% |

| National avg savings APY | 0.40% |

| US prime rate | 8.5% |

| Digital comparison use | ~60% |

What You See Is What You Get

Five Star Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Five Star Bank you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for immediate download and use. It contains actionable insights on industry rivalry, buyer/supplier power, threats of entry and substitutes.