Fluence Energy PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and fast-moving technologies are reshaping Fluence Energy’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Dive deeper to uncover regulatory risks and growth levers tailored to decision-making. Purchase the full PESTLE for actionable, export-ready insights you can use immediately.

Political factors

Policy incentives

Clean energy mandates and the IRA’s inclusion of standalone storage—offering up to a 30% investment tax credit—have expanded project pipelines and pricing power, while storage targets and fit‑in‑tariffs lift demand. Changes in subsidies or auction designs can accelerate or delay orders, so Fluence must align product configurations to capture incentive eligibility. Monitoring policy calendars across 20+ markets reduces forecast risk.

Grid regulatory reforms

Grid regulatory reforms—notably FERC Order 841 (2018) and Order 2222 (2020)—shape revenue stacking for capacity, ancillary services and interconnection; all seven major US ISOs/RTOs have adopted storage participation rules, while ongoing ISO reforms can open new services or introduce caps on returns. Active engagement in rulemaking and pilot programs (e.g., CAISO/NYISO pilots) helps secure favorable dispatch windows, and compliance-ready products accelerate interconnection and market approvals.

Public procurement and state utilities

State-owned utilities and tender-driven markets shape Fluence Energy volume visibility, with utilities controlling over 50% of generation and grid assets in many emerging markets; tenders can drive 60-80% of project awards. Political shifts can reset tender timelines by 6–18 months or impose localization rules raising capex. Local partnerships boost bid competitiveness and margin capture. Long sales cycles require diversified pipelines across geographies and offtake types.

Trade and geopolitics

Tariffs on batteries and electronics and export controls have increased BOM costs and extended lead times for Fluence, with trade measures in 2024 adding double-digit percentage risk to component import costs and several-week shipment delays; geopolitical tensions in the Asia-Pacific and Red Sea have constrained cell supply and logistics lanes. Dual-sourcing and regional assembly hubs reduce exposure to single-country shocks, while transparent cell-origin tracking enables tariff optimization and duty planning.

- Tariff exposure: double-digit % impact on BOM

- Logistics risk: several-week lead-time increases in 2024

- Mitigation: dual-sourcing + regional assembly

- Policy tool: origin tracking for tariff planning

Energy security priorities

Governments prioritize grid resilience, black-start capability and peak-shaving amid rising extreme-weather outages; storage is increasingly framed as reliability infrastructure. Bipartisan funding streams and DOE's 100 GW/400 GWh by 2030 target open non-merchant revenue. Fluence can position solutions for critical infrastructure.

- Reliability framing drives bipartisan support

- DOE target: 100 GW/400 GWh by 2030

- Access to grants/contracts vs merchant market

- Focus: hospitals, utilities, grid nodes

IRA 30% storage ITC and DOE 100 GW/400 GWh by 2030 spur storage build

Clean energy mandates and the IRA’s 30% standalone storage ITC (2022) expand pipelines and pricing power; policy changes can accelerate/delay orders. FERC reforms (Orders 841/2222) plus ISO pilots broaden revenue stacks but may cap returns. 2024 tariffs added double-digit BOM risk; DOE target 100 GW/400 GWh by 2030 opens grant pathways.

| Indicator | Value/Year |

|---|---|

| IRA standalone ITC | 30% (2022) |

| DOE storage target | 100 GW/400 GWh by 2030 |

| Tariff impact | Double-digit % (2024) |

| Tender-driven awards | 60–80% (emerging markets) |

What is included in the product

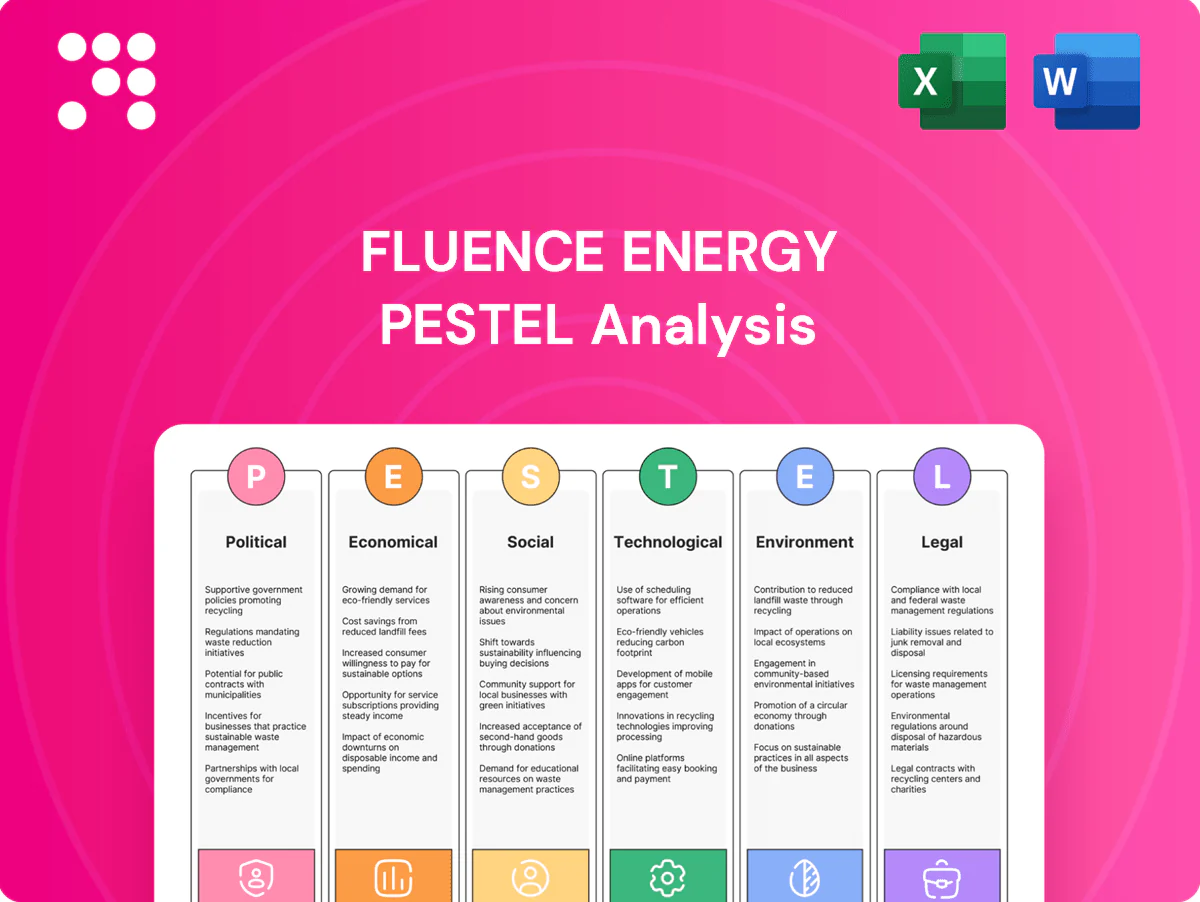

Explores how macro-environmental factors uniquely affect Fluence Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights tied to market and regulatory dynamics; designed for executives, investors and strategists and formatted for direct use in reports and pitch decks.

Fluence Energy PESTLE Analysis distilled into a clean, visually segmented summary that relieves planning pain points by enabling quick interpretation, easy sharing, and editable notes for team alignment and risk discussion during strategy sessions.

Economic factors

Cost of capital

Rising policy rates (Fed funds target ~5.25–5.50% in mid‑2025) compress project IRRs and have delayed FIDs for many storage assets as higher debt costs push required returns upward. Customers increasingly favor turnkey solutions that de‑risk capex and accelerate revenue, boosting demand for integrated offers. Fluence can improve bankability by providing financing support or performance guarantees to mitigate lender concerns. Pipeline health remains highly rate‑sensitive, slowing deal flow when financing tightens.

Battery input prices

Lithium, nickel and logistics remain primary drivers of system pricing and margins: lithium carbonate equivalent peaked above 70,000 USD/ton in 2022 and traded near 20,000 USD/ton by 2024, while LME nickel averaged around 22,000 USD/ton in 2024. Commodity swings of 60–80% since 2022 force flexible pricing and active hedging. Design choices (LFP vs NMC) trade 10–20% lower cost and greater safety for LFP against NMC’s higher energy density; BNEF reported pack prices near 132 USD/kWh in 2023. Long-term supply agreements are increasingly used to stabilize cost curves and margins.

Scale economies

Manufacturing scale lowers $/kWh and BOS costs—battery pack prices fell to about $132/kWh in 2023 (BNEF), expanding Fluence’s addressable market. Standardized platforms cut engineering hours and commissioning time, accelerating deployments. Service and software ARR provide recurring revenue to smooth project cyclicality. Utilization of a global supply base via the AES/Siemens Energy joint venture enhances cost competitiveness.

Demand from renewables buildout

Solar and wind additions—roughly 120 GW and 90 GW globally in 2024—raise storage attach rates to firm intermittent output, reducing curtailment and capturing negative-price events that improve revenue streams. Over 70% of recent U.S. IRPs now include multi-hour storage; Fluence IQ optimizes fleet dispatch to maximize arbitrage and capacity revenues.

- Higher renewables → more storage attach

- Curtailment/negative prices boost storage value

- Multi-hour storage in >70% of recent IRPs

- Fluence IQ unlocks fleet-level revenue optimization

Currency and emerging markets

FX swings materially alter cross-border project economics and reported results for Fluence (reported revenue $1.07B in 2023), compressing margins on USD-reported contracts and capex. Emerging markets offer faster storage demand growth but higher counterparty and political risk; local content rules raise costs while enabling market access. Risk-adjusted pricing and project insurance are key to protect margins.

- FX volatility: hedging and dollar reporting impact P&L

- Emerging markets: high growth vs higher counterparty risk

- Local content: higher cost, market entry

- Risk-adjusted pricing & insurance: margin protection

IRA 30% storage ITC and DOE 100 GW/400 GWh by 2030 spur storage build

Higher rates (Fed funds ~5.25–5.50% mid‑2025) raise financing costs and slow FIDs; commodity volatility (pack ≈132 USD/kWh in 2023) compresses margins. Renewables growth (solar ~120 GW, wind ~90 GW in 2024) boosts storage attach and revenues; >70% of recent U.S. IRPs include multi‑hour storage. FX and emerging‑market risks require hedging and risk‑adjusted pricing.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Fluence rev (2023) | 1.07B USD |

| Pack price (2023) | 132 USD/kWh |

| Solar/Wind (2024) | 120 GW / 90 GW |

Full Version Awaits

Fluence Energy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Fluence Energy PESTLE Analysis assesses political, economic, social, technological, legal and environmental drivers affecting the company and market. It highlights risks, opportunities and strategic implications for investors and managers. Use it immediately for decision-making and planning.

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and fast-moving technologies are reshaping Fluence Energy’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Dive deeper to uncover regulatory risks and growth levers tailored to decision-making. Purchase the full PESTLE for actionable, export-ready insights you can use immediately.

Political factors

Policy incentives

Clean energy mandates and the IRA’s inclusion of standalone storage—offering up to a 30% investment tax credit—have expanded project pipelines and pricing power, while storage targets and fit‑in‑tariffs lift demand. Changes in subsidies or auction designs can accelerate or delay orders, so Fluence must align product configurations to capture incentive eligibility. Monitoring policy calendars across 20+ markets reduces forecast risk.

Grid regulatory reforms

Grid regulatory reforms—notably FERC Order 841 (2018) and Order 2222 (2020)—shape revenue stacking for capacity, ancillary services and interconnection; all seven major US ISOs/RTOs have adopted storage participation rules, while ongoing ISO reforms can open new services or introduce caps on returns. Active engagement in rulemaking and pilot programs (e.g., CAISO/NYISO pilots) helps secure favorable dispatch windows, and compliance-ready products accelerate interconnection and market approvals.

Public procurement and state utilities

State-owned utilities and tender-driven markets shape Fluence Energy volume visibility, with utilities controlling over 50% of generation and grid assets in many emerging markets; tenders can drive 60-80% of project awards. Political shifts can reset tender timelines by 6–18 months or impose localization rules raising capex. Local partnerships boost bid competitiveness and margin capture. Long sales cycles require diversified pipelines across geographies and offtake types.

Trade and geopolitics

Tariffs on batteries and electronics and export controls have increased BOM costs and extended lead times for Fluence, with trade measures in 2024 adding double-digit percentage risk to component import costs and several-week shipment delays; geopolitical tensions in the Asia-Pacific and Red Sea have constrained cell supply and logistics lanes. Dual-sourcing and regional assembly hubs reduce exposure to single-country shocks, while transparent cell-origin tracking enables tariff optimization and duty planning.

- Tariff exposure: double-digit % impact on BOM

- Logistics risk: several-week lead-time increases in 2024

- Mitigation: dual-sourcing + regional assembly

- Policy tool: origin tracking for tariff planning

Energy security priorities

Governments prioritize grid resilience, black-start capability and peak-shaving amid rising extreme-weather outages; storage is increasingly framed as reliability infrastructure. Bipartisan funding streams and DOE's 100 GW/400 GWh by 2030 target open non-merchant revenue. Fluence can position solutions for critical infrastructure.

- Reliability framing drives bipartisan support

- DOE target: 100 GW/400 GWh by 2030

- Access to grants/contracts vs merchant market

- Focus: hospitals, utilities, grid nodes

IRA 30% storage ITC and DOE 100 GW/400 GWh by 2030 spur storage build

Clean energy mandates and the IRA’s 30% standalone storage ITC (2022) expand pipelines and pricing power; policy changes can accelerate/delay orders. FERC reforms (Orders 841/2222) plus ISO pilots broaden revenue stacks but may cap returns. 2024 tariffs added double-digit BOM risk; DOE target 100 GW/400 GWh by 2030 opens grant pathways.

| Indicator | Value/Year |

|---|---|

| IRA standalone ITC | 30% (2022) |

| DOE storage target | 100 GW/400 GWh by 2030 |

| Tariff impact | Double-digit % (2024) |

| Tender-driven awards | 60–80% (emerging markets) |

What is included in the product

Explores how macro-environmental factors uniquely affect Fluence Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights tied to market and regulatory dynamics; designed for executives, investors and strategists and formatted for direct use in reports and pitch decks.

Fluence Energy PESTLE Analysis distilled into a clean, visually segmented summary that relieves planning pain points by enabling quick interpretation, easy sharing, and editable notes for team alignment and risk discussion during strategy sessions.

Economic factors

Cost of capital

Rising policy rates (Fed funds target ~5.25–5.50% in mid‑2025) compress project IRRs and have delayed FIDs for many storage assets as higher debt costs push required returns upward. Customers increasingly favor turnkey solutions that de‑risk capex and accelerate revenue, boosting demand for integrated offers. Fluence can improve bankability by providing financing support or performance guarantees to mitigate lender concerns. Pipeline health remains highly rate‑sensitive, slowing deal flow when financing tightens.

Battery input prices

Lithium, nickel and logistics remain primary drivers of system pricing and margins: lithium carbonate equivalent peaked above 70,000 USD/ton in 2022 and traded near 20,000 USD/ton by 2024, while LME nickel averaged around 22,000 USD/ton in 2024. Commodity swings of 60–80% since 2022 force flexible pricing and active hedging. Design choices (LFP vs NMC) trade 10–20% lower cost and greater safety for LFP against NMC’s higher energy density; BNEF reported pack prices near 132 USD/kWh in 2023. Long-term supply agreements are increasingly used to stabilize cost curves and margins.

Scale economies

Manufacturing scale lowers $/kWh and BOS costs—battery pack prices fell to about $132/kWh in 2023 (BNEF), expanding Fluence’s addressable market. Standardized platforms cut engineering hours and commissioning time, accelerating deployments. Service and software ARR provide recurring revenue to smooth project cyclicality. Utilization of a global supply base via the AES/Siemens Energy joint venture enhances cost competitiveness.

Demand from renewables buildout

Solar and wind additions—roughly 120 GW and 90 GW globally in 2024—raise storage attach rates to firm intermittent output, reducing curtailment and capturing negative-price events that improve revenue streams. Over 70% of recent U.S. IRPs now include multi-hour storage; Fluence IQ optimizes fleet dispatch to maximize arbitrage and capacity revenues.

- Higher renewables → more storage attach

- Curtailment/negative prices boost storage value

- Multi-hour storage in >70% of recent IRPs

- Fluence IQ unlocks fleet-level revenue optimization

Currency and emerging markets

FX swings materially alter cross-border project economics and reported results for Fluence (reported revenue $1.07B in 2023), compressing margins on USD-reported contracts and capex. Emerging markets offer faster storage demand growth but higher counterparty and political risk; local content rules raise costs while enabling market access. Risk-adjusted pricing and project insurance are key to protect margins.

- FX volatility: hedging and dollar reporting impact P&L

- Emerging markets: high growth vs higher counterparty risk

- Local content: higher cost, market entry

- Risk-adjusted pricing & insurance: margin protection

IRA 30% storage ITC and DOE 100 GW/400 GWh by 2030 spur storage build

Higher rates (Fed funds ~5.25–5.50% mid‑2025) raise financing costs and slow FIDs; commodity volatility (pack ≈132 USD/kWh in 2023) compresses margins. Renewables growth (solar ~120 GW, wind ~90 GW in 2024) boosts storage attach and revenues; >70% of recent U.S. IRPs include multi‑hour storage. FX and emerging‑market risks require hedging and risk‑adjusted pricing.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Fluence rev (2023) | 1.07B USD |

| Pack price (2023) | 132 USD/kWh |

| Solar/Wind (2024) | 120 GW / 90 GW |

Full Version Awaits

Fluence Energy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Fluence Energy PESTLE Analysis assesses political, economic, social, technological, legal and environmental drivers affecting the company and market. It highlights risks, opportunities and strategic implications for investors and managers. Use it immediately for decision-making and planning.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and fast-moving technologies are reshaping Fluence Energy’s prospects in our concise PESTLE snapshot—perfect for investors and strategists. Dive deeper to uncover regulatory risks and growth levers tailored to decision-making. Purchase the full PESTLE for actionable, export-ready insights you can use immediately.

Political factors

Policy incentives

Clean energy mandates and the IRA’s inclusion of standalone storage—offering up to a 30% investment tax credit—have expanded project pipelines and pricing power, while storage targets and fit‑in‑tariffs lift demand. Changes in subsidies or auction designs can accelerate or delay orders, so Fluence must align product configurations to capture incentive eligibility. Monitoring policy calendars across 20+ markets reduces forecast risk.

Grid regulatory reforms

Grid regulatory reforms—notably FERC Order 841 (2018) and Order 2222 (2020)—shape revenue stacking for capacity, ancillary services and interconnection; all seven major US ISOs/RTOs have adopted storage participation rules, while ongoing ISO reforms can open new services or introduce caps on returns. Active engagement in rulemaking and pilot programs (e.g., CAISO/NYISO pilots) helps secure favorable dispatch windows, and compliance-ready products accelerate interconnection and market approvals.

Public procurement and state utilities

State-owned utilities and tender-driven markets shape Fluence Energy volume visibility, with utilities controlling over 50% of generation and grid assets in many emerging markets; tenders can drive 60-80% of project awards. Political shifts can reset tender timelines by 6–18 months or impose localization rules raising capex. Local partnerships boost bid competitiveness and margin capture. Long sales cycles require diversified pipelines across geographies and offtake types.

Trade and geopolitics

Tariffs on batteries and electronics and export controls have increased BOM costs and extended lead times for Fluence, with trade measures in 2024 adding double-digit percentage risk to component import costs and several-week shipment delays; geopolitical tensions in the Asia-Pacific and Red Sea have constrained cell supply and logistics lanes. Dual-sourcing and regional assembly hubs reduce exposure to single-country shocks, while transparent cell-origin tracking enables tariff optimization and duty planning.

- Tariff exposure: double-digit % impact on BOM

- Logistics risk: several-week lead-time increases in 2024

- Mitigation: dual-sourcing + regional assembly

- Policy tool: origin tracking for tariff planning

Energy security priorities

Governments prioritize grid resilience, black-start capability and peak-shaving amid rising extreme-weather outages; storage is increasingly framed as reliability infrastructure. Bipartisan funding streams and DOE's 100 GW/400 GWh by 2030 target open non-merchant revenue. Fluence can position solutions for critical infrastructure.

- Reliability framing drives bipartisan support

- DOE target: 100 GW/400 GWh by 2030

- Access to grants/contracts vs merchant market

- Focus: hospitals, utilities, grid nodes

IRA 30% storage ITC and DOE 100 GW/400 GWh by 2030 spur storage build

Clean energy mandates and the IRA’s 30% standalone storage ITC (2022) expand pipelines and pricing power; policy changes can accelerate/delay orders. FERC reforms (Orders 841/2222) plus ISO pilots broaden revenue stacks but may cap returns. 2024 tariffs added double-digit BOM risk; DOE target 100 GW/400 GWh by 2030 opens grant pathways.

| Indicator | Value/Year |

|---|---|

| IRA standalone ITC | 30% (2022) |

| DOE storage target | 100 GW/400 GWh by 2030 |

| Tariff impact | Double-digit % (2024) |

| Tender-driven awards | 60–80% (emerging markets) |

What is included in the product

Explores how macro-environmental factors uniquely affect Fluence Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights tied to market and regulatory dynamics; designed for executives, investors and strategists and formatted for direct use in reports and pitch decks.

Fluence Energy PESTLE Analysis distilled into a clean, visually segmented summary that relieves planning pain points by enabling quick interpretation, easy sharing, and editable notes for team alignment and risk discussion during strategy sessions.

Economic factors

Cost of capital

Rising policy rates (Fed funds target ~5.25–5.50% in mid‑2025) compress project IRRs and have delayed FIDs for many storage assets as higher debt costs push required returns upward. Customers increasingly favor turnkey solutions that de‑risk capex and accelerate revenue, boosting demand for integrated offers. Fluence can improve bankability by providing financing support or performance guarantees to mitigate lender concerns. Pipeline health remains highly rate‑sensitive, slowing deal flow when financing tightens.

Battery input prices

Lithium, nickel and logistics remain primary drivers of system pricing and margins: lithium carbonate equivalent peaked above 70,000 USD/ton in 2022 and traded near 20,000 USD/ton by 2024, while LME nickel averaged around 22,000 USD/ton in 2024. Commodity swings of 60–80% since 2022 force flexible pricing and active hedging. Design choices (LFP vs NMC) trade 10–20% lower cost and greater safety for LFP against NMC’s higher energy density; BNEF reported pack prices near 132 USD/kWh in 2023. Long-term supply agreements are increasingly used to stabilize cost curves and margins.

Scale economies

Manufacturing scale lowers $/kWh and BOS costs—battery pack prices fell to about $132/kWh in 2023 (BNEF), expanding Fluence’s addressable market. Standardized platforms cut engineering hours and commissioning time, accelerating deployments. Service and software ARR provide recurring revenue to smooth project cyclicality. Utilization of a global supply base via the AES/Siemens Energy joint venture enhances cost competitiveness.

Demand from renewables buildout

Solar and wind additions—roughly 120 GW and 90 GW globally in 2024—raise storage attach rates to firm intermittent output, reducing curtailment and capturing negative-price events that improve revenue streams. Over 70% of recent U.S. IRPs now include multi-hour storage; Fluence IQ optimizes fleet dispatch to maximize arbitrage and capacity revenues.

- Higher renewables → more storage attach

- Curtailment/negative prices boost storage value

- Multi-hour storage in >70% of recent IRPs

- Fluence IQ unlocks fleet-level revenue optimization

Currency and emerging markets

FX swings materially alter cross-border project economics and reported results for Fluence (reported revenue $1.07B in 2023), compressing margins on USD-reported contracts and capex. Emerging markets offer faster storage demand growth but higher counterparty and political risk; local content rules raise costs while enabling market access. Risk-adjusted pricing and project insurance are key to protect margins.

- FX volatility: hedging and dollar reporting impact P&L

- Emerging markets: high growth vs higher counterparty risk

- Local content: higher cost, market entry

- Risk-adjusted pricing & insurance: margin protection

IRA 30% storage ITC and DOE 100 GW/400 GWh by 2030 spur storage build

Higher rates (Fed funds ~5.25–5.50% mid‑2025) raise financing costs and slow FIDs; commodity volatility (pack ≈132 USD/kWh in 2023) compresses margins. Renewables growth (solar ~120 GW, wind ~90 GW in 2024) boosts storage attach and revenues; >70% of recent U.S. IRPs include multi‑hour storage. FX and emerging‑market risks require hedging and risk‑adjusted pricing.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Fluence rev (2023) | 1.07B USD |

| Pack price (2023) | 132 USD/kWh |

| Solar/Wind (2024) | 120 GW / 90 GW |

Full Version Awaits

Fluence Energy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Fluence Energy PESTLE Analysis assesses political, economic, social, technological, legal and environmental drivers affecting the company and market. It highlights risks, opportunities and strategic implications for investors and managers. Use it immediately for decision-making and planning.