Fluor Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

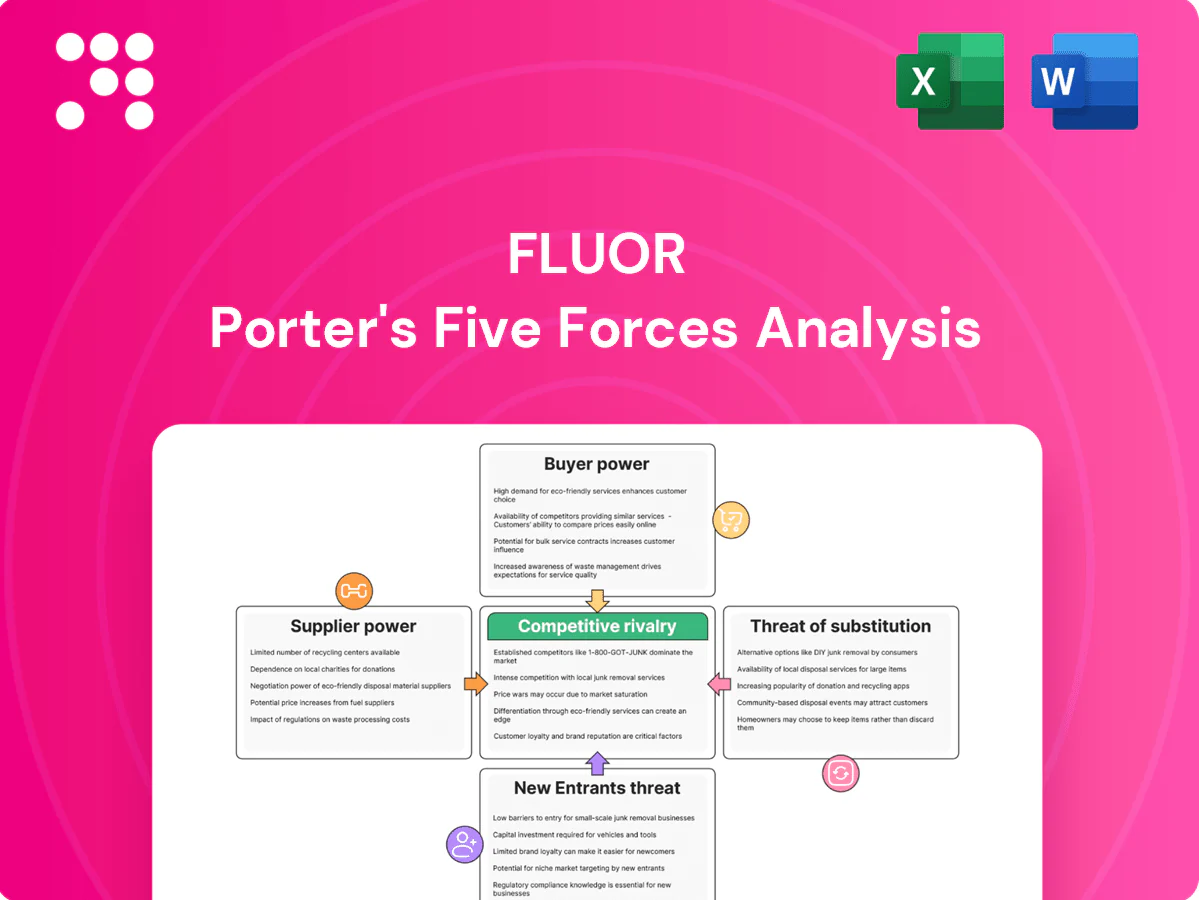

Fluor's Porter's Five Forces snapshot highlights supplier concentration, project-based buyer power, barriers from scale and contracts, and competitive rivalry in engineering and construction. Understanding these dynamics clarifies where margin pressure and strategic opportunity lie. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized equipment and material vendors

Critical items like reactors, turbines and large valves are sourced from a concentrated OEM pool—top gas‑turbine manufacturers (GE, Siemens Energy, Mitsubishi) held about 70% of global market share in 2024—giving suppliers pricing and delivery leverage; typical turbine lead times of 12–36 months and strict qualification raise dependence. Fluor offsets risk via early procurement, framework agreements and dual‑sourcing where feasible, but client single‑source specs can lock choices and sustain supplier power.

Process technology licensors

Proprietary process licensors in petrochemicals and refining exert high power via IP control, royalties (commonly 1–4% of production value) and mandated vendor packages; top licensors (UOP, Lummus, Axens) held roughly 60% of major process licenses in 2024, frequently limiting EPC negotiation room. Integration risks and performance guarantees tether Fluor to licensor terms, and while co‑development or alliance models can reduce costs, they rarely eliminate licensor leverage.

Skilled labor and specialty subcontractors

Scarcity of specialized trades and stringent welding qualifications—with the American Welding Society estimating a shortfall of about 400,000 welders by 2024—pushes rates and schedule risk for Fluor. Regional craft rates climbed roughly 5–12% in 2023–24, and peak-cycle demand tightens capacity, giving niche subs pricing power. Fluor offsets this through global talent pools, in-house craft training and preferred-sub networks. Local content rules in some markets still constrain choice and elevate supplier influence.

Commodity inputs and logistics

Steel, cement and bulk electricals are highly commoditized, which limits individual supplier pricing power for Fluor; however, freight, fuel and geopolitical shocks in 2024 continued to drive episodic cost swings and supply interruptions. Fluor offsets this via bulk purchasing, strategic logistics planning and index-linked contracts to pass or hedge cost exposure, though port or corridor disruptions can temporarily raise supplier leverage.

- Commoditized inputs reduce supplier margin influence

- 2024 freight/fuel/geopolitics cause episodic cost spikes

- Mitigation: bulk buys, logistics planning, index-linked contracts

- Port/corridor disruptions temporarily increase supplier power

Digital tools and data platforms

Dependence on major design software and cloud collaboration vendors (Autodesk, Bentley, AWS, Azure) creates switching costs for Fluor; licensing changes or interoperability limits in 2024 can shift bargaining power to these providers. Fluor mitigates risk with multi-tool proficiency, internal data standards, and negotiated data ownership clauses to limit vendor leverage and maintain project control.

- Vendor concentration: Autodesk, Bentley, major cloud and cybersecurity vendors

- Fluor defenses: multi-tool skills, internal standards

- Contract levers: data ownership clauses, interoperability requirements

Supplier power, welder shortfalls and freight shocks squeeze costs and schedules

Supplier power is high for critical OEMs (top gas turbines ~70% share in 2024) and proprietary licensors (~60% of major process licenses), raising price and delivery leverage. Skilled craft scarcity (≈400,000 welder shortfall in 2024) and 5–12% regional rate rises tighten schedules. Commodities are commoditized but freight/geopolitics cause episodic spikes; Fluor mitigates via early buys, dual‑sourcing, contracts.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| OEM turbines | 70% market | High price/leadtimes | Early procurement |

| Licensors | 60% licenses | IP royalties | Alliances |

| Skilled craft | -400k welders | Rate/schedule risk | Training/networks |

What is included in the product

Condensed Porter’s Five Forces analysis tailored for Fluor, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal strategic pressures, emerging disruptors, and implications for pricing, margins, and long-term positioning.

A concise, one-sheet Fluor Porter's Five Forces summary with adjustable pressure levels and radar chart—easy to drop into decks or Excel dashboards, no macros required for quick strategic decisions.

Customers Bargaining Power

Sophisticated mega-cap clients

IOCs, NOCs, miners and sovereign clients run sophisticated procurement teams and benchmark bids on multi-billion-dollar projects (mega projects often exceed $1 billion), giving them high bargaining power. They demand competitive bidding, transparency and stringent performance and payment terms tied to KPIs and safety records. Fluor defends margins by selling track record, safety credentials and total lifecycle value, yet strategic accounts still extract concessions on price and contract terms due to deal scale.

Contracting models and risk transfer

Lump-sum turnkey contracts with liquidated damages transfer cost and schedule risk to the contractor, increasing buyer leverage while EPCM and reimbursable models balance risk but impose tighter KPIs and oversight.

Fluor prices transferred risk into bid contingencies and escalation clauses and increasingly pursues collaborative delivery and integrated project teams to recalibrate bargaining power.

Market cycles—tightening procurement windows in downturns versus vendor-heavy demand in booms—determine how much risk buyers can realistically offload.

Ability to unbundle scopes

Owners increasingly unbundle engineering, procurement, construction and commissioning, allowing split awards that heighten competition and compress margins on each package. Unbundling can push package margins down by double digits in some projects, prompting Fluor to emphasize integrated solutions and rigorous interface management to justify bundled awards. Fluor cites framework agreements and phase-gate continuity to reduce buyer switching and protect overall margin.

Project pipeline cyclicality

Energy and mining capex cycles drive EPC utilization swings, shifting bargaining power to buyers during downcycles when backlogs thin and price competition intensifies; industry bid margins can compress several hundred basis points in soft markets (2024 industry reports note higher margin pressure vs 2022–23).

Fluor’s diversified end-market mix (energy, infrastructure, mining, and government) buffers cyclicality, yet large buyers can strategically time tenders to exploit soft periods, extracting concessions and longer payment terms from contractors.

- Downcycles: thinner backlogs → stronger buyer leverage

- Price pressure: margin compression several hundred bps (2024)

- Diversification: Fluor offsets but does not eliminate buyer timing risk

Technical specs and approved vendor lists

Buyer-defined specs and approved vendor lists constrain EPC flexibility, preserving client bargaining power and often driving higher margins and limited value-engineering; studies show early design input can cut change orders by up to 30% and lower total installed cost materially (industry 2024 front-end loading data).

- AVL constraints limit sourcing options

- Clients control acceptance/standards

- Fluor embeds constructability in FEED

- Early engagement rebalances authority

Buyers extract concessions on mega-projects >$1bn as bid margins compress

Large IOC/NOC/sovereign buyers run expert procurement on mega-projects (>$1bn) and extract concessions on price, terms and KPIs; lump-sum contracts raise buyer leverage while EPCM shifts oversight. Fluor defends via safety/track record, integrated delivery and framework agreements, yet 2024 saw bid margins compress several hundred bps vs 2022–23. Unbundling and AVL constraints sustain buyer power; early FEED reduces change orders materially.

| Metric | 2024 Data |

|---|---|

| Typical mega-project size | >$1bn |

| Margin compression | Several hundred bps (2024 vs 2022–23) |

| Buyer leverage | High (procurement teams, AVL control) |

Full Version Awaits

Fluor Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Fluor that you'll receive immediately after purchase—fully formatted, no placeholders. The document displayed is the final deliverable, ready to download and use the moment you buy. No mockups, no samples.

Go Beyond the Preview—Access the Full Strategic Report

Fluor's Porter's Five Forces snapshot highlights supplier concentration, project-based buyer power, barriers from scale and contracts, and competitive rivalry in engineering and construction. Understanding these dynamics clarifies where margin pressure and strategic opportunity lie. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized equipment and material vendors

Critical items like reactors, turbines and large valves are sourced from a concentrated OEM pool—top gas‑turbine manufacturers (GE, Siemens Energy, Mitsubishi) held about 70% of global market share in 2024—giving suppliers pricing and delivery leverage; typical turbine lead times of 12–36 months and strict qualification raise dependence. Fluor offsets risk via early procurement, framework agreements and dual‑sourcing where feasible, but client single‑source specs can lock choices and sustain supplier power.

Process technology licensors

Proprietary process licensors in petrochemicals and refining exert high power via IP control, royalties (commonly 1–4% of production value) and mandated vendor packages; top licensors (UOP, Lummus, Axens) held roughly 60% of major process licenses in 2024, frequently limiting EPC negotiation room. Integration risks and performance guarantees tether Fluor to licensor terms, and while co‑development or alliance models can reduce costs, they rarely eliminate licensor leverage.

Skilled labor and specialty subcontractors

Scarcity of specialized trades and stringent welding qualifications—with the American Welding Society estimating a shortfall of about 400,000 welders by 2024—pushes rates and schedule risk for Fluor. Regional craft rates climbed roughly 5–12% in 2023–24, and peak-cycle demand tightens capacity, giving niche subs pricing power. Fluor offsets this through global talent pools, in-house craft training and preferred-sub networks. Local content rules in some markets still constrain choice and elevate supplier influence.

Commodity inputs and logistics

Steel, cement and bulk electricals are highly commoditized, which limits individual supplier pricing power for Fluor; however, freight, fuel and geopolitical shocks in 2024 continued to drive episodic cost swings and supply interruptions. Fluor offsets this via bulk purchasing, strategic logistics planning and index-linked contracts to pass or hedge cost exposure, though port or corridor disruptions can temporarily raise supplier leverage.

- Commoditized inputs reduce supplier margin influence

- 2024 freight/fuel/geopolitics cause episodic cost spikes

- Mitigation: bulk buys, logistics planning, index-linked contracts

- Port/corridor disruptions temporarily increase supplier power

Digital tools and data platforms

Dependence on major design software and cloud collaboration vendors (Autodesk, Bentley, AWS, Azure) creates switching costs for Fluor; licensing changes or interoperability limits in 2024 can shift bargaining power to these providers. Fluor mitigates risk with multi-tool proficiency, internal data standards, and negotiated data ownership clauses to limit vendor leverage and maintain project control.

- Vendor concentration: Autodesk, Bentley, major cloud and cybersecurity vendors

- Fluor defenses: multi-tool skills, internal standards

- Contract levers: data ownership clauses, interoperability requirements

Supplier power, welder shortfalls and freight shocks squeeze costs and schedules

Supplier power is high for critical OEMs (top gas turbines ~70% share in 2024) and proprietary licensors (~60% of major process licenses), raising price and delivery leverage. Skilled craft scarcity (≈400,000 welder shortfall in 2024) and 5–12% regional rate rises tighten schedules. Commodities are commoditized but freight/geopolitics cause episodic spikes; Fluor mitigates via early buys, dual‑sourcing, contracts.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| OEM turbines | 70% market | High price/leadtimes | Early procurement |

| Licensors | 60% licenses | IP royalties | Alliances |

| Skilled craft | -400k welders | Rate/schedule risk | Training/networks |

What is included in the product

Condensed Porter’s Five Forces analysis tailored for Fluor, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal strategic pressures, emerging disruptors, and implications for pricing, margins, and long-term positioning.

A concise, one-sheet Fluor Porter's Five Forces summary with adjustable pressure levels and radar chart—easy to drop into decks or Excel dashboards, no macros required for quick strategic decisions.

Customers Bargaining Power

Sophisticated mega-cap clients

IOCs, NOCs, miners and sovereign clients run sophisticated procurement teams and benchmark bids on multi-billion-dollar projects (mega projects often exceed $1 billion), giving them high bargaining power. They demand competitive bidding, transparency and stringent performance and payment terms tied to KPIs and safety records. Fluor defends margins by selling track record, safety credentials and total lifecycle value, yet strategic accounts still extract concessions on price and contract terms due to deal scale.

Contracting models and risk transfer

Lump-sum turnkey contracts with liquidated damages transfer cost and schedule risk to the contractor, increasing buyer leverage while EPCM and reimbursable models balance risk but impose tighter KPIs and oversight.

Fluor prices transferred risk into bid contingencies and escalation clauses and increasingly pursues collaborative delivery and integrated project teams to recalibrate bargaining power.

Market cycles—tightening procurement windows in downturns versus vendor-heavy demand in booms—determine how much risk buyers can realistically offload.

Ability to unbundle scopes

Owners increasingly unbundle engineering, procurement, construction and commissioning, allowing split awards that heighten competition and compress margins on each package. Unbundling can push package margins down by double digits in some projects, prompting Fluor to emphasize integrated solutions and rigorous interface management to justify bundled awards. Fluor cites framework agreements and phase-gate continuity to reduce buyer switching and protect overall margin.

Project pipeline cyclicality

Energy and mining capex cycles drive EPC utilization swings, shifting bargaining power to buyers during downcycles when backlogs thin and price competition intensifies; industry bid margins can compress several hundred basis points in soft markets (2024 industry reports note higher margin pressure vs 2022–23).

Fluor’s diversified end-market mix (energy, infrastructure, mining, and government) buffers cyclicality, yet large buyers can strategically time tenders to exploit soft periods, extracting concessions and longer payment terms from contractors.

- Downcycles: thinner backlogs → stronger buyer leverage

- Price pressure: margin compression several hundred bps (2024)

- Diversification: Fluor offsets but does not eliminate buyer timing risk

Technical specs and approved vendor lists

Buyer-defined specs and approved vendor lists constrain EPC flexibility, preserving client bargaining power and often driving higher margins and limited value-engineering; studies show early design input can cut change orders by up to 30% and lower total installed cost materially (industry 2024 front-end loading data).

- AVL constraints limit sourcing options

- Clients control acceptance/standards

- Fluor embeds constructability in FEED

- Early engagement rebalances authority

Buyers extract concessions on mega-projects >$1bn as bid margins compress

Large IOC/NOC/sovereign buyers run expert procurement on mega-projects (>$1bn) and extract concessions on price, terms and KPIs; lump-sum contracts raise buyer leverage while EPCM shifts oversight. Fluor defends via safety/track record, integrated delivery and framework agreements, yet 2024 saw bid margins compress several hundred bps vs 2022–23. Unbundling and AVL constraints sustain buyer power; early FEED reduces change orders materially.

| Metric | 2024 Data |

|---|---|

| Typical mega-project size | >$1bn |

| Margin compression | Several hundred bps (2024 vs 2022–23) |

| Buyer leverage | High (procurement teams, AVL control) |

Full Version Awaits

Fluor Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Fluor that you'll receive immediately after purchase—fully formatted, no placeholders. The document displayed is the final deliverable, ready to download and use the moment you buy. No mockups, no samples.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Fluor's Porter's Five Forces snapshot highlights supplier concentration, project-based buyer power, barriers from scale and contracts, and competitive rivalry in engineering and construction. Understanding these dynamics clarifies where margin pressure and strategic opportunity lie. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized equipment and material vendors

Critical items like reactors, turbines and large valves are sourced from a concentrated OEM pool—top gas‑turbine manufacturers (GE, Siemens Energy, Mitsubishi) held about 70% of global market share in 2024—giving suppliers pricing and delivery leverage; typical turbine lead times of 12–36 months and strict qualification raise dependence. Fluor offsets risk via early procurement, framework agreements and dual‑sourcing where feasible, but client single‑source specs can lock choices and sustain supplier power.

Process technology licensors

Proprietary process licensors in petrochemicals and refining exert high power via IP control, royalties (commonly 1–4% of production value) and mandated vendor packages; top licensors (UOP, Lummus, Axens) held roughly 60% of major process licenses in 2024, frequently limiting EPC negotiation room. Integration risks and performance guarantees tether Fluor to licensor terms, and while co‑development or alliance models can reduce costs, they rarely eliminate licensor leverage.

Skilled labor and specialty subcontractors

Scarcity of specialized trades and stringent welding qualifications—with the American Welding Society estimating a shortfall of about 400,000 welders by 2024—pushes rates and schedule risk for Fluor. Regional craft rates climbed roughly 5–12% in 2023–24, and peak-cycle demand tightens capacity, giving niche subs pricing power. Fluor offsets this through global talent pools, in-house craft training and preferred-sub networks. Local content rules in some markets still constrain choice and elevate supplier influence.

Commodity inputs and logistics

Steel, cement and bulk electricals are highly commoditized, which limits individual supplier pricing power for Fluor; however, freight, fuel and geopolitical shocks in 2024 continued to drive episodic cost swings and supply interruptions. Fluor offsets this via bulk purchasing, strategic logistics planning and index-linked contracts to pass or hedge cost exposure, though port or corridor disruptions can temporarily raise supplier leverage.

- Commoditized inputs reduce supplier margin influence

- 2024 freight/fuel/geopolitics cause episodic cost spikes

- Mitigation: bulk buys, logistics planning, index-linked contracts

- Port/corridor disruptions temporarily increase supplier power

Digital tools and data platforms

Dependence on major design software and cloud collaboration vendors (Autodesk, Bentley, AWS, Azure) creates switching costs for Fluor; licensing changes or interoperability limits in 2024 can shift bargaining power to these providers. Fluor mitigates risk with multi-tool proficiency, internal data standards, and negotiated data ownership clauses to limit vendor leverage and maintain project control.

- Vendor concentration: Autodesk, Bentley, major cloud and cybersecurity vendors

- Fluor defenses: multi-tool skills, internal standards

- Contract levers: data ownership clauses, interoperability requirements

Supplier power, welder shortfalls and freight shocks squeeze costs and schedules

Supplier power is high for critical OEMs (top gas turbines ~70% share in 2024) and proprietary licensors (~60% of major process licenses), raising price and delivery leverage. Skilled craft scarcity (≈400,000 welder shortfall in 2024) and 5–12% regional rate rises tighten schedules. Commodities are commoditized but freight/geopolitics cause episodic spikes; Fluor mitigates via early buys, dual‑sourcing, contracts.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| OEM turbines | 70% market | High price/leadtimes | Early procurement |

| Licensors | 60% licenses | IP royalties | Alliances |

| Skilled craft | -400k welders | Rate/schedule risk | Training/networks |

What is included in the product

Condensed Porter’s Five Forces analysis tailored for Fluor, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal strategic pressures, emerging disruptors, and implications for pricing, margins, and long-term positioning.

A concise, one-sheet Fluor Porter's Five Forces summary with adjustable pressure levels and radar chart—easy to drop into decks or Excel dashboards, no macros required for quick strategic decisions.

Customers Bargaining Power

Sophisticated mega-cap clients

IOCs, NOCs, miners and sovereign clients run sophisticated procurement teams and benchmark bids on multi-billion-dollar projects (mega projects often exceed $1 billion), giving them high bargaining power. They demand competitive bidding, transparency and stringent performance and payment terms tied to KPIs and safety records. Fluor defends margins by selling track record, safety credentials and total lifecycle value, yet strategic accounts still extract concessions on price and contract terms due to deal scale.

Contracting models and risk transfer

Lump-sum turnkey contracts with liquidated damages transfer cost and schedule risk to the contractor, increasing buyer leverage while EPCM and reimbursable models balance risk but impose tighter KPIs and oversight.

Fluor prices transferred risk into bid contingencies and escalation clauses and increasingly pursues collaborative delivery and integrated project teams to recalibrate bargaining power.

Market cycles—tightening procurement windows in downturns versus vendor-heavy demand in booms—determine how much risk buyers can realistically offload.

Ability to unbundle scopes

Owners increasingly unbundle engineering, procurement, construction and commissioning, allowing split awards that heighten competition and compress margins on each package. Unbundling can push package margins down by double digits in some projects, prompting Fluor to emphasize integrated solutions and rigorous interface management to justify bundled awards. Fluor cites framework agreements and phase-gate continuity to reduce buyer switching and protect overall margin.

Project pipeline cyclicality

Energy and mining capex cycles drive EPC utilization swings, shifting bargaining power to buyers during downcycles when backlogs thin and price competition intensifies; industry bid margins can compress several hundred basis points in soft markets (2024 industry reports note higher margin pressure vs 2022–23).

Fluor’s diversified end-market mix (energy, infrastructure, mining, and government) buffers cyclicality, yet large buyers can strategically time tenders to exploit soft periods, extracting concessions and longer payment terms from contractors.

- Downcycles: thinner backlogs → stronger buyer leverage

- Price pressure: margin compression several hundred bps (2024)

- Diversification: Fluor offsets but does not eliminate buyer timing risk

Technical specs and approved vendor lists

Buyer-defined specs and approved vendor lists constrain EPC flexibility, preserving client bargaining power and often driving higher margins and limited value-engineering; studies show early design input can cut change orders by up to 30% and lower total installed cost materially (industry 2024 front-end loading data).

- AVL constraints limit sourcing options

- Clients control acceptance/standards

- Fluor embeds constructability in FEED

- Early engagement rebalances authority

Buyers extract concessions on mega-projects >$1bn as bid margins compress

Large IOC/NOC/sovereign buyers run expert procurement on mega-projects (>$1bn) and extract concessions on price, terms and KPIs; lump-sum contracts raise buyer leverage while EPCM shifts oversight. Fluor defends via safety/track record, integrated delivery and framework agreements, yet 2024 saw bid margins compress several hundred bps vs 2022–23. Unbundling and AVL constraints sustain buyer power; early FEED reduces change orders materially.

| Metric | 2024 Data |

|---|---|

| Typical mega-project size | >$1bn |

| Margin compression | Several hundred bps (2024 vs 2022–23) |

| Buyer leverage | High (procurement teams, AVL control) |

Full Version Awaits

Fluor Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Fluor that you'll receive immediately after purchase—fully formatted, no placeholders. The document displayed is the final deliverable, ready to download and use the moment you buy. No mockups, no samples.