Fortescue Metals Group SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Fortescue Metals Group's strengths include low-cost iron ore production and ambitious green hydrogen investments, while exposure to commodity cycles, regulatory scrutiny, and capital intensity present notable risks. Opportunities lie in steel demand recovery and energy-transition services, but competition and China demand uncertainty weigh on growth. Purchase the full SWOT analysis to access a detailed, editable report and Excel toolkit for investment and strategy planning.

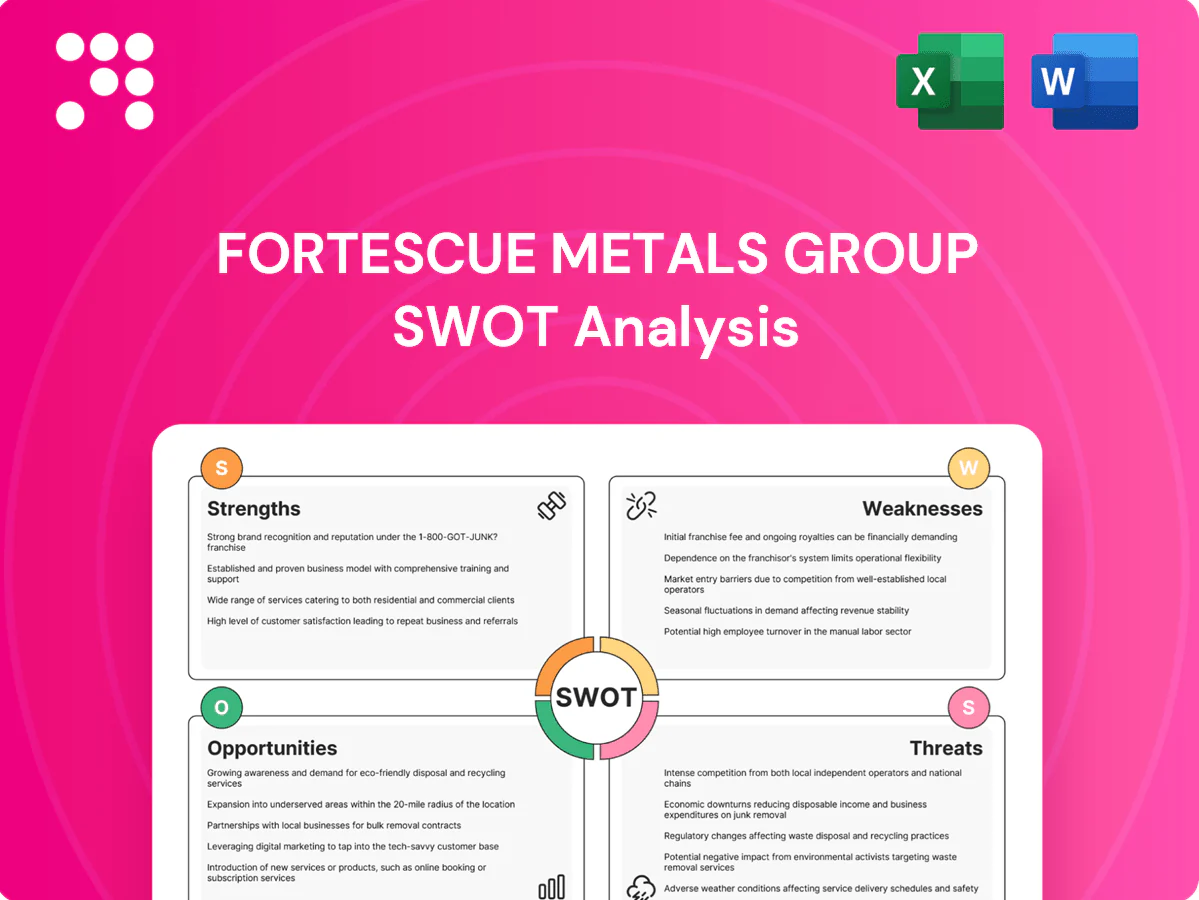

Strengths

Low-cost Pilbara producer

Fortescue is one of the lowest-cost iron ore producers in the Pilbara, leveraging scale efficiencies from >170 Mtpa shipments reported in FY2024, standardized operations and strict cost discipline. These structural advantages keep unit costs in the global lower quartile, sustaining margins through price cycles and insulating cash flow. Compared with higher-cost global peers, Fortescue’s cost position supports competitive pricing flexibility and stronger returns.

Integrated rail and port

Fortescue owns and operates an integrated iron‑ore system including about 700 km of private heavy‑haul rail and significant berthing capacity at Port Hedland, enabling direct control of mine‑to‑ship flows. End‑to‑end control reduces turnaround times and unit costs—FMG reported ~185 Mt shipped in FY2024 with improved rail availability supporting lower FOB unit costs. Vertical integration enables targeted de‑bottlenecking and rail/port optimization, underpinning strong export performance to Asia, especially China and Japan.

Deep Asian customer footprint

Fortescue maintains long-term offtake relationships with Chinese, Japanese and Korean steelmakers, with over 70% of shipments destined for Asia, supported by contract structures combining multi-year take-or-pay terms and spot-linked sales. Its port and mine blending capabilities deliver consistent 62%+ Fe product quality and reliable throughput, underpinning steady supply. Proximity to Asian mills and dedicated market intelligence teams secure resilient offtake during volatility.

Robust cash generation

Robust cash generation: Fortescue delivered strong free cash flow in recent high-price cycles, reporting A$6.8bn FCF in FY2024, underpinning a net cash position ~A$4.5bn at year-end. This balance sheet flexibility has funded A$3.2bn of dividends and buybacks while enabling reinvestment in growth and decarbonization projects. Management has a disciplined capital allocation track record driving returns.

FFI platform for green growth

Fortescue Future Industries (FFI) is Fortescue Metals Groups commercial vehicle for green hydrogen, green ammonia and associated technologies, running pilot projects and first-mover partnerships across Australia, the US, UK and Chile to scale electrolysis and storage at industrial scale.

FFI offers a pathway to decarbonize Fortescues mining operations and supply chain while creating new revenue streams from hydrogen exports and tech licensing, supporting Fortescues net-zero Scope 1–2 ambition by 2030 and Scope 3 targets.

- FFI: green hydrogen, ammonia, tech platform

- First-mover pilots & cross-border partnerships

- Decarbonizes mining ops; new revenues from exports/licensing

- Strategic hedge vs tightening carbon policy

Pilbara low-cost iron-ore leader — 185 Mt, A$6.8bn FCF

Fortescue is a low‑cost Pilbara iron‑ore leader (185 Mt shipped FY2024) with integrated mine‑rail‑port control and consistent 62%+ Fe product, underpinning strong Asian offtake. FY2024 FCF A$6.8bn; net cash ~A$4.5bn; A$3.2bn returned to shareholders. FFI pilots green hydrogen/ammonia across AUS, US, UK, Chile to decarbonize operations and create new revenue.

| Metric | FY2024 |

|---|---|

| Shipments | 185 Mt |

| FCF | A$6.8bn |

| Net cash | ~A$4.5bn |

| Returns | A$3.2bn |

| Fe grade | 62%+ |

What is included in the product

Delivers a strategic overview of Fortescue Metals Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position and future risks.

Provides a concise SWOT matrix for Fortescue Metals Group to quickly surface strategic pain points and align remediation actions for faster decision-making and investor-ready summaries.

Weaknesses

Revenue concentration in iron ore

Fortescue derived over 90% of revenue from iron ore in FY2024, reflecting heavy reliance on a single commodity and a narrow product suite.

Earnings are highly sensitive to movements in the 62% Fe benchmark price, meaning EBITDA and NPAT swing materially with market volatility.

Unlike multi‑commodity peers such as BHP and Rio Tinto, Fortescue’s limited diversification concentrates downside risk in iron ore downturns.

China demand dependence

Fortescue faces outsized exposure to China’s steel sector and property cycle, with China accounting for roughly 70% of seaborne iron‑ore imports (about 1.1 billion tonnes in 2024), so swings in demand drive volumes and realised prices. Policy shifts, stimulus or environmental curbs in China can rapidly depress domestic steel output and iron‑ore imports. Trade tensions and geopolitical frictions with Australia amplify shipment and pricing risk, and customer concentration raises counterparty vulnerability.

Grade discount dynamics

Fortescue's concentrate has historically averaged around 58% Fe, below Vale's roughly 65% Fe and the 62% Fe IODEX benchmark used for pricing, and typically under Rio/BHP blends that often test 59–62% Fe. Lower Fe and higher silica/alumina attract discounts and impurity penalties versus 62% benchmark spreads, compressing realised prices. FMG has invested in blending and beneficiation (capital spend >US$5bn since 2017) but residual grade-related headwinds persist as mills tighten emissions and quality specs.

Capital intensity and project risk

Fortescue faces heavy sustaining and growth capital intensity across mines, rail and port, with large ongoing investments increasing its exposure to execution risk, cost inflation and schedule slippage. Concurrent brownfield expansions add complexity and operating disruption risk, while Fortescue Future Industries scale-up—targeting 15GW of renewable projects by 2030—carries technology, permitting and financing uncertainties.

- Capital intensity: heavy sustaining and growth capex

- Execution risk: cost inflation and schedule slippage

- Complexity: concurrent brownfield expansions

- FFI: 15GW by 2030 scale-up uncertainties

ESG and social license exposure

ESG and social license exposure in the Pilbara is acute given sensitive land use, Indigenous cultural heritage sites and scarce groundwater resources requiring strict water management and monitoring.

Fortescue faces intense scope 1–3 emissions scrutiny; the company targets operational net zero by 2030 and value-chain reductions by 2040, raising capital and tech cost pressures.

Heightened governance and stakeholder engagement obligations increase risk of permitting delays, compliance costs and reputational damage if Indigenous or environmental concerns arise.

- Land use and cultural heritage sensitivity

- Water scarcity and monitoring obligations

- Scope 1–3 decarbonization targets 2030/2040

- Permitting delays, governance and reputational risk

Commodity risk: >90% iron ore revenue; linked to 62% Fe benchmark

>90% of FY2024 revenue from iron ore, concentrating commodity risk.

Earnings track the 62% Fe benchmark; China ≈70% of seaborne imports (1.1bn t, 2024) magnifies demand swings.

Avg concentrate ~58% Fe (below 62% benchmark); high capex (>US$5bn since 2017) and FFI 15GW by 2030 raise execution risk.

| Metric | Value |

|---|---|

| FY2024 iron ore rev | >90% |

| Avg Fe grade | ~58% Fe |

Preview the Actual Deliverable

Fortescue Metals Group SWOT Analysis

This Fortescue Metals Group SWOT Analysis preview is taken directly from the full report you’ll receive upon purchase—no surprises, just professional quality. The excerpt reflects the complete, editable analysis of strengths, weaknesses, opportunities, and threats. Buy now to unlock the entire, detailed document immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Fortescue Metals Group's strengths include low-cost iron ore production and ambitious green hydrogen investments, while exposure to commodity cycles, regulatory scrutiny, and capital intensity present notable risks. Opportunities lie in steel demand recovery and energy-transition services, but competition and China demand uncertainty weigh on growth. Purchase the full SWOT analysis to access a detailed, editable report and Excel toolkit for investment and strategy planning.

Strengths

Low-cost Pilbara producer

Fortescue is one of the lowest-cost iron ore producers in the Pilbara, leveraging scale efficiencies from >170 Mtpa shipments reported in FY2024, standardized operations and strict cost discipline. These structural advantages keep unit costs in the global lower quartile, sustaining margins through price cycles and insulating cash flow. Compared with higher-cost global peers, Fortescue’s cost position supports competitive pricing flexibility and stronger returns.

Integrated rail and port

Fortescue owns and operates an integrated iron‑ore system including about 700 km of private heavy‑haul rail and significant berthing capacity at Port Hedland, enabling direct control of mine‑to‑ship flows. End‑to‑end control reduces turnaround times and unit costs—FMG reported ~185 Mt shipped in FY2024 with improved rail availability supporting lower FOB unit costs. Vertical integration enables targeted de‑bottlenecking and rail/port optimization, underpinning strong export performance to Asia, especially China and Japan.

Deep Asian customer footprint

Fortescue maintains long-term offtake relationships with Chinese, Japanese and Korean steelmakers, with over 70% of shipments destined for Asia, supported by contract structures combining multi-year take-or-pay terms and spot-linked sales. Its port and mine blending capabilities deliver consistent 62%+ Fe product quality and reliable throughput, underpinning steady supply. Proximity to Asian mills and dedicated market intelligence teams secure resilient offtake during volatility.

Robust cash generation

Robust cash generation: Fortescue delivered strong free cash flow in recent high-price cycles, reporting A$6.8bn FCF in FY2024, underpinning a net cash position ~A$4.5bn at year-end. This balance sheet flexibility has funded A$3.2bn of dividends and buybacks while enabling reinvestment in growth and decarbonization projects. Management has a disciplined capital allocation track record driving returns.

FFI platform for green growth

Fortescue Future Industries (FFI) is Fortescue Metals Groups commercial vehicle for green hydrogen, green ammonia and associated technologies, running pilot projects and first-mover partnerships across Australia, the US, UK and Chile to scale electrolysis and storage at industrial scale.

FFI offers a pathway to decarbonize Fortescues mining operations and supply chain while creating new revenue streams from hydrogen exports and tech licensing, supporting Fortescues net-zero Scope 1–2 ambition by 2030 and Scope 3 targets.

- FFI: green hydrogen, ammonia, tech platform

- First-mover pilots & cross-border partnerships

- Decarbonizes mining ops; new revenues from exports/licensing

- Strategic hedge vs tightening carbon policy

Pilbara low-cost iron-ore leader — 185 Mt, A$6.8bn FCF

Fortescue is a low‑cost Pilbara iron‑ore leader (185 Mt shipped FY2024) with integrated mine‑rail‑port control and consistent 62%+ Fe product, underpinning strong Asian offtake. FY2024 FCF A$6.8bn; net cash ~A$4.5bn; A$3.2bn returned to shareholders. FFI pilots green hydrogen/ammonia across AUS, US, UK, Chile to decarbonize operations and create new revenue.

| Metric | FY2024 |

|---|---|

| Shipments | 185 Mt |

| FCF | A$6.8bn |

| Net cash | ~A$4.5bn |

| Returns | A$3.2bn |

| Fe grade | 62%+ |

What is included in the product

Delivers a strategic overview of Fortescue Metals Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position and future risks.

Provides a concise SWOT matrix for Fortescue Metals Group to quickly surface strategic pain points and align remediation actions for faster decision-making and investor-ready summaries.

Weaknesses

Revenue concentration in iron ore

Fortescue derived over 90% of revenue from iron ore in FY2024, reflecting heavy reliance on a single commodity and a narrow product suite.

Earnings are highly sensitive to movements in the 62% Fe benchmark price, meaning EBITDA and NPAT swing materially with market volatility.

Unlike multi‑commodity peers such as BHP and Rio Tinto, Fortescue’s limited diversification concentrates downside risk in iron ore downturns.

China demand dependence

Fortescue faces outsized exposure to China’s steel sector and property cycle, with China accounting for roughly 70% of seaborne iron‑ore imports (about 1.1 billion tonnes in 2024), so swings in demand drive volumes and realised prices. Policy shifts, stimulus or environmental curbs in China can rapidly depress domestic steel output and iron‑ore imports. Trade tensions and geopolitical frictions with Australia amplify shipment and pricing risk, and customer concentration raises counterparty vulnerability.

Grade discount dynamics

Fortescue's concentrate has historically averaged around 58% Fe, below Vale's roughly 65% Fe and the 62% Fe IODEX benchmark used for pricing, and typically under Rio/BHP blends that often test 59–62% Fe. Lower Fe and higher silica/alumina attract discounts and impurity penalties versus 62% benchmark spreads, compressing realised prices. FMG has invested in blending and beneficiation (capital spend >US$5bn since 2017) but residual grade-related headwinds persist as mills tighten emissions and quality specs.

Capital intensity and project risk

Fortescue faces heavy sustaining and growth capital intensity across mines, rail and port, with large ongoing investments increasing its exposure to execution risk, cost inflation and schedule slippage. Concurrent brownfield expansions add complexity and operating disruption risk, while Fortescue Future Industries scale-up—targeting 15GW of renewable projects by 2030—carries technology, permitting and financing uncertainties.

- Capital intensity: heavy sustaining and growth capex

- Execution risk: cost inflation and schedule slippage

- Complexity: concurrent brownfield expansions

- FFI: 15GW by 2030 scale-up uncertainties

ESG and social license exposure

ESG and social license exposure in the Pilbara is acute given sensitive land use, Indigenous cultural heritage sites and scarce groundwater resources requiring strict water management and monitoring.

Fortescue faces intense scope 1–3 emissions scrutiny; the company targets operational net zero by 2030 and value-chain reductions by 2040, raising capital and tech cost pressures.

Heightened governance and stakeholder engagement obligations increase risk of permitting delays, compliance costs and reputational damage if Indigenous or environmental concerns arise.

- Land use and cultural heritage sensitivity

- Water scarcity and monitoring obligations

- Scope 1–3 decarbonization targets 2030/2040

- Permitting delays, governance and reputational risk

Commodity risk: >90% iron ore revenue; linked to 62% Fe benchmark

>90% of FY2024 revenue from iron ore, concentrating commodity risk.

Earnings track the 62% Fe benchmark; China ≈70% of seaborne imports (1.1bn t, 2024) magnifies demand swings.

Avg concentrate ~58% Fe (below 62% benchmark); high capex (>US$5bn since 2017) and FFI 15GW by 2030 raise execution risk.

| Metric | Value |

|---|---|

| FY2024 iron ore rev | >90% |

| Avg Fe grade | ~58% Fe |

Preview the Actual Deliverable

Fortescue Metals Group SWOT Analysis

This Fortescue Metals Group SWOT Analysis preview is taken directly from the full report you’ll receive upon purchase—no surprises, just professional quality. The excerpt reflects the complete, editable analysis of strengths, weaknesses, opportunities, and threats. Buy now to unlock the entire, detailed document immediately after checkout.

Description

Make Insightful Decisions Backed by Expert Research

Fortescue Metals Group's strengths include low-cost iron ore production and ambitious green hydrogen investments, while exposure to commodity cycles, regulatory scrutiny, and capital intensity present notable risks. Opportunities lie in steel demand recovery and energy-transition services, but competition and China demand uncertainty weigh on growth. Purchase the full SWOT analysis to access a detailed, editable report and Excel toolkit for investment and strategy planning.

Strengths

Low-cost Pilbara producer

Fortescue is one of the lowest-cost iron ore producers in the Pilbara, leveraging scale efficiencies from >170 Mtpa shipments reported in FY2024, standardized operations and strict cost discipline. These structural advantages keep unit costs in the global lower quartile, sustaining margins through price cycles and insulating cash flow. Compared with higher-cost global peers, Fortescue’s cost position supports competitive pricing flexibility and stronger returns.

Integrated rail and port

Fortescue owns and operates an integrated iron‑ore system including about 700 km of private heavy‑haul rail and significant berthing capacity at Port Hedland, enabling direct control of mine‑to‑ship flows. End‑to‑end control reduces turnaround times and unit costs—FMG reported ~185 Mt shipped in FY2024 with improved rail availability supporting lower FOB unit costs. Vertical integration enables targeted de‑bottlenecking and rail/port optimization, underpinning strong export performance to Asia, especially China and Japan.

Deep Asian customer footprint

Fortescue maintains long-term offtake relationships with Chinese, Japanese and Korean steelmakers, with over 70% of shipments destined for Asia, supported by contract structures combining multi-year take-or-pay terms and spot-linked sales. Its port and mine blending capabilities deliver consistent 62%+ Fe product quality and reliable throughput, underpinning steady supply. Proximity to Asian mills and dedicated market intelligence teams secure resilient offtake during volatility.

Robust cash generation

Robust cash generation: Fortescue delivered strong free cash flow in recent high-price cycles, reporting A$6.8bn FCF in FY2024, underpinning a net cash position ~A$4.5bn at year-end. This balance sheet flexibility has funded A$3.2bn of dividends and buybacks while enabling reinvestment in growth and decarbonization projects. Management has a disciplined capital allocation track record driving returns.

FFI platform for green growth

Fortescue Future Industries (FFI) is Fortescue Metals Groups commercial vehicle for green hydrogen, green ammonia and associated technologies, running pilot projects and first-mover partnerships across Australia, the US, UK and Chile to scale electrolysis and storage at industrial scale.

FFI offers a pathway to decarbonize Fortescues mining operations and supply chain while creating new revenue streams from hydrogen exports and tech licensing, supporting Fortescues net-zero Scope 1–2 ambition by 2030 and Scope 3 targets.

- FFI: green hydrogen, ammonia, tech platform

- First-mover pilots & cross-border partnerships

- Decarbonizes mining ops; new revenues from exports/licensing

- Strategic hedge vs tightening carbon policy

Pilbara low-cost iron-ore leader — 185 Mt, A$6.8bn FCF

Fortescue is a low‑cost Pilbara iron‑ore leader (185 Mt shipped FY2024) with integrated mine‑rail‑port control and consistent 62%+ Fe product, underpinning strong Asian offtake. FY2024 FCF A$6.8bn; net cash ~A$4.5bn; A$3.2bn returned to shareholders. FFI pilots green hydrogen/ammonia across AUS, US, UK, Chile to decarbonize operations and create new revenue.

| Metric | FY2024 |

|---|---|

| Shipments | 185 Mt |

| FCF | A$6.8bn |

| Net cash | ~A$4.5bn |

| Returns | A$3.2bn |

| Fe grade | 62%+ |

What is included in the product

Delivers a strategic overview of Fortescue Metals Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position and future risks.

Provides a concise SWOT matrix for Fortescue Metals Group to quickly surface strategic pain points and align remediation actions for faster decision-making and investor-ready summaries.

Weaknesses

Revenue concentration in iron ore

Fortescue derived over 90% of revenue from iron ore in FY2024, reflecting heavy reliance on a single commodity and a narrow product suite.

Earnings are highly sensitive to movements in the 62% Fe benchmark price, meaning EBITDA and NPAT swing materially with market volatility.

Unlike multi‑commodity peers such as BHP and Rio Tinto, Fortescue’s limited diversification concentrates downside risk in iron ore downturns.

China demand dependence

Fortescue faces outsized exposure to China’s steel sector and property cycle, with China accounting for roughly 70% of seaborne iron‑ore imports (about 1.1 billion tonnes in 2024), so swings in demand drive volumes and realised prices. Policy shifts, stimulus or environmental curbs in China can rapidly depress domestic steel output and iron‑ore imports. Trade tensions and geopolitical frictions with Australia amplify shipment and pricing risk, and customer concentration raises counterparty vulnerability.

Grade discount dynamics

Fortescue's concentrate has historically averaged around 58% Fe, below Vale's roughly 65% Fe and the 62% Fe IODEX benchmark used for pricing, and typically under Rio/BHP blends that often test 59–62% Fe. Lower Fe and higher silica/alumina attract discounts and impurity penalties versus 62% benchmark spreads, compressing realised prices. FMG has invested in blending and beneficiation (capital spend >US$5bn since 2017) but residual grade-related headwinds persist as mills tighten emissions and quality specs.

Capital intensity and project risk

Fortescue faces heavy sustaining and growth capital intensity across mines, rail and port, with large ongoing investments increasing its exposure to execution risk, cost inflation and schedule slippage. Concurrent brownfield expansions add complexity and operating disruption risk, while Fortescue Future Industries scale-up—targeting 15GW of renewable projects by 2030—carries technology, permitting and financing uncertainties.

- Capital intensity: heavy sustaining and growth capex

- Execution risk: cost inflation and schedule slippage

- Complexity: concurrent brownfield expansions

- FFI: 15GW by 2030 scale-up uncertainties

ESG and social license exposure

ESG and social license exposure in the Pilbara is acute given sensitive land use, Indigenous cultural heritage sites and scarce groundwater resources requiring strict water management and monitoring.

Fortescue faces intense scope 1–3 emissions scrutiny; the company targets operational net zero by 2030 and value-chain reductions by 2040, raising capital and tech cost pressures.

Heightened governance and stakeholder engagement obligations increase risk of permitting delays, compliance costs and reputational damage if Indigenous or environmental concerns arise.

- Land use and cultural heritage sensitivity

- Water scarcity and monitoring obligations

- Scope 1–3 decarbonization targets 2030/2040

- Permitting delays, governance and reputational risk

Commodity risk: >90% iron ore revenue; linked to 62% Fe benchmark

>90% of FY2024 revenue from iron ore, concentrating commodity risk.

Earnings track the 62% Fe benchmark; China ≈70% of seaborne imports (1.1bn t, 2024) magnifies demand swings.

Avg concentrate ~58% Fe (below 62% benchmark); high capex (>US$5bn since 2017) and FFI 15GW by 2030 raise execution risk.

| Metric | Value |

|---|---|

| FY2024 iron ore rev | >90% |

| Avg Fe grade | ~58% Fe |

Preview the Actual Deliverable

Fortescue Metals Group SWOT Analysis

This Fortescue Metals Group SWOT Analysis preview is taken directly from the full report you’ll receive upon purchase—no surprises, just professional quality. The excerpt reflects the complete, editable analysis of strengths, weaknesses, opportunities, and threats. Buy now to unlock the entire, detailed document immediately after checkout.