First National Bank Business Model Canvas

Unlock a bank's strategic Business Model Canvas to benchmark, scale, and monetize services

Unlock the full strategic blueprint behind First National Bank's Business Model Canvas. This concise, section-by-section analysis reveals how the bank creates customer value, scales core activities, and monetizes services. Download the complete editable Word/Excel canvas to benchmark strategy, inform investments, and adapt proven banking tactics.

Partnerships

Core banking and fintech vendors

Strategic alliances with core system providers and cloud-enabled fintechs drive product agility and improved digital UX by enabling faster feature releases, robust API connectivity, and rapid compliance updates. Co-development with vendors reduces time-to-market and controls tech risk. Strong vendor governance enforces uptime, cybersecurity, and scalability.

Payment networks and processors

Partnerships with Visa (accepted in 200+ countries; VisaNet >65,000 messages/sec) and Mastercard (global reach 210+ countries), ACH operators (U.S. ACH moves over $70 trillion annually) and processors enable cards, treasury and real-time rails, expanding merchant acceptance and lowering transaction friction. Joint risk tools enhance fraud detection through shared screening and alerts, while volume tiers deliver improved interchange economics at scale.

Mortgage, insurance, and wealth platforms

Alliances with mortgage investors, insurers and custodians broaden First National Bank’s product breadth and distribution, linking originations to capital partners; US agency MBS outstanding was about $8.3 trillion in 2024, boosting secondary-market pricing and liquidity. Insurance carriers supply retail and commercial protection solutions—global life/health premiums totaled roughly $3.5 trillion in 2024. Custody partners enable advisory scale and specialist asset servicing, with global custodial AUC above $100 trillion in 2024.

Community, civic, and referral networks

Local chambers, nonprofits and universities strengthen First National Bank brand trust across Mid-Atlantic and Southeast markets; community banks held about 16% of U.S. banking assets in 2024 (FDIC), underscoring local influence. Referral partnerships consistently channel small-business and consumer leads. Financial literacy programs deepen community ties and co-hosted events boost acquisition and retention.

- Chambers: brand trust

- Referrals: lead flow

- Literacy: engagement

- Events: acquisition/retention

Regulatory, risk, and data partners

Regulatory advisors, regtechs and credit bureaus underpin governance and underwriting at First National Bank, enhancing KYC/AML and automated credit decisioning. Model validation firms fortify risk frameworks and independent stress testing. Industry 2024 surveys report partnerships can cut onboarding time by up to 40% and reduce credit losses by up to 20%.

- Compliance advisors

- Regtech integrations

- Credit bureau data

- Model validation

- Faster onboarding, lower losses

Partnerships and rails cut onboarding 40%, expand global reach & liquidity

Key partnerships with core system providers and fintechs accelerate releases and compliance; regtechs cut onboarding up to 40% (2024). Card and rail alliances (Visa 200+ countries; VisaNet >65,000 msgs/sec; Mastercard 210+ countries; ACH ~$70T/year) expand acceptance and lower fees. Capital partners (agency MBS $8.3T 2024), insurers (global premiums ~$3.5T 2024) and custodians (AUC >$100T 2024) scale products and liquidity.

| Partner | 2024 Metric |

|---|---|

| Visa/Mastercard | 200+/210+ countries; VisaNet >65,000 msgs/sec |

| ACH | ~$70T annual volume |

| Agency MBS | $8.3T outstanding |

| Custody | AUC >$100T |

What is included in the product

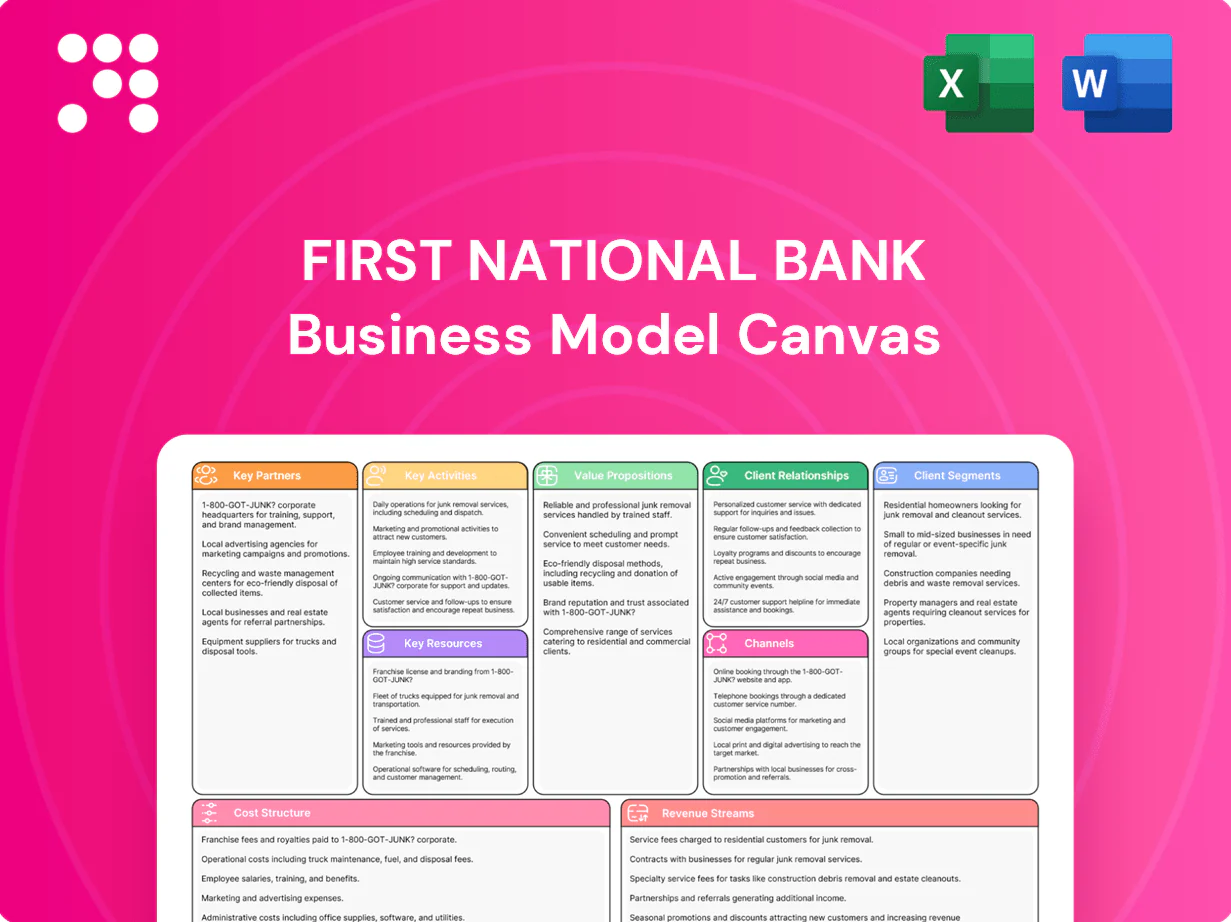

A comprehensive, pre-written BMC aligned with First National Bank’s strategy, covering customer segments, channels, value propositions, revenue streams, key activities and partnerships. Organized into 9 classic blocks with SWOT-linked analysis, competitive advantages and a polished design for presentations and funding discussions.

Condenses First National Bank’s strategy into a digestible, one-page Business Model Canvas with editable cells to quickly identify pain points, align teams, and save hours otherwise spent structuring and formatting internal analyses.

Activities

Relationship-centric lending

Origination and servicing of commercial, consumer and mortgage loans anchor FNBs revenue base, with tailored underwriting and timely servicing driving fee and interest income. Relationship pricing deepens share of wallet by aligning rates and bundles to client segments. Ongoing credit monitoring preserves asset quality through early intervention. Cross-selling maps deposits, cards and wealth solutions to client life cycles.

Treasury and payments services

Treasury and payments services — cash management, receivables, payables and merchant acquiring — create sticky commercial deposits by concentrating operating balances and transaction flows with the bank. Real-time rails such as FedNow (live since July 2023) accelerate collections and disbursements, improving daily cash conversion for clients. API-based embedding lets clients automate treasury functions inside ERP/pos systems, increasing product usage and cross-sell. Advisory on working capital and payment optimization lifts fee income and retention.

Wealth and advisory delivery

Financial planning, investment management, and trust services at First National Bank expanded noninterest income, supporting an estimated 9% AUM growth in 2024; goals-based advice personalizes portfolios to client objectives, while integrated digital tools increased transparency and client engagement; rigorous fiduciary oversight underpins retention and long-term loyalty.

Digital product development

Digital product development delivers iterative mobile, online banking and onboarding builds that optimize customer journeys, with 2024 industry focus on rapid release cycles and personalized experiences. Data analytics drive real-time offers and alerts while embedded cybersecurity and fraud prevention reduce risk by design. Continuous testing improves accessibility, performance and regulatory compliance.

- Iterative releases

- Data-driven personalization

- Security-by-design

- Continuous accessibility & performance testing

Risk, compliance, and capital management

Credit, market, liquidity and operational risk frameworks maintain resilience through limits, early-warning metrics and loss provisioning; banks typically target CET1 near 10–12% versus the Basel III minimum CET1 4.5% (as of 2024) and LCR ≥100% to ensure funding stability.

Stress testing and ALM shape pricing and balance-sheet mix by quantifying scenario losses and interest‑rate risk; AML/KYC controls protect reputation and reduce regulatory fines; capital planning underpins sustainable growth and dividend capacity.

- Risk types: credit, market, liquidity, operational

- Regulatory facts: Basel III CET1 min 4.5% (2024), LCR ≥100%

- Targets: bank CET1 commonly 10–12%

- Controls: stress tests, ALM, AML/KYC, capital planning

Loan NII, FedNow rails and +9% AUM drive fee and deposit growth

Origination and servicing of commercial, consumer and mortgage loans drive NII and fees, with tailored underwriting and credit monitoring preserving asset quality.

Treasury, payments and FedNow-enabled real-time rails concentrate commercial deposits and boost fee income via embedded APIs.

Wealth/advisory (AUM +9% in 2024), digital product releases and strong risk/capital targets (CET1 10–12%, Basel III min 4.5% in 2024) sustain revenue diversification.

| Metric | 2024/Fact |

|---|---|

| AUM growth | +9% |

| CET1 target | 10–12% |

| Basel III CET1 min | 4.5% |

| FedNow | Live Jul 2023 |

What You See Is What You Get

Business Model Canvas

The First National Bank Business Model Canvas preview shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this exact document—complete and fully editable. Files are provided in Word and Excel formats, ready for presenting or customizing. No hidden content or surprises—what you see is what you get.

Unlock a bank's strategic Business Model Canvas to benchmark, scale, and monetize services

Unlock the full strategic blueprint behind First National Bank's Business Model Canvas. This concise, section-by-section analysis reveals how the bank creates customer value, scales core activities, and monetizes services. Download the complete editable Word/Excel canvas to benchmark strategy, inform investments, and adapt proven banking tactics.

Partnerships

Core banking and fintech vendors

Strategic alliances with core system providers and cloud-enabled fintechs drive product agility and improved digital UX by enabling faster feature releases, robust API connectivity, and rapid compliance updates. Co-development with vendors reduces time-to-market and controls tech risk. Strong vendor governance enforces uptime, cybersecurity, and scalability.

Payment networks and processors

Partnerships with Visa (accepted in 200+ countries; VisaNet >65,000 messages/sec) and Mastercard (global reach 210+ countries), ACH operators (U.S. ACH moves over $70 trillion annually) and processors enable cards, treasury and real-time rails, expanding merchant acceptance and lowering transaction friction. Joint risk tools enhance fraud detection through shared screening and alerts, while volume tiers deliver improved interchange economics at scale.

Mortgage, insurance, and wealth platforms

Alliances with mortgage investors, insurers and custodians broaden First National Bank’s product breadth and distribution, linking originations to capital partners; US agency MBS outstanding was about $8.3 trillion in 2024, boosting secondary-market pricing and liquidity. Insurance carriers supply retail and commercial protection solutions—global life/health premiums totaled roughly $3.5 trillion in 2024. Custody partners enable advisory scale and specialist asset servicing, with global custodial AUC above $100 trillion in 2024.

Community, civic, and referral networks

Local chambers, nonprofits and universities strengthen First National Bank brand trust across Mid-Atlantic and Southeast markets; community banks held about 16% of U.S. banking assets in 2024 (FDIC), underscoring local influence. Referral partnerships consistently channel small-business and consumer leads. Financial literacy programs deepen community ties and co-hosted events boost acquisition and retention.

- Chambers: brand trust

- Referrals: lead flow

- Literacy: engagement

- Events: acquisition/retention

Regulatory, risk, and data partners

Regulatory advisors, regtechs and credit bureaus underpin governance and underwriting at First National Bank, enhancing KYC/AML and automated credit decisioning. Model validation firms fortify risk frameworks and independent stress testing. Industry 2024 surveys report partnerships can cut onboarding time by up to 40% and reduce credit losses by up to 20%.

- Compliance advisors

- Regtech integrations

- Credit bureau data

- Model validation

- Faster onboarding, lower losses

Partnerships and rails cut onboarding 40%, expand global reach & liquidity

Key partnerships with core system providers and fintechs accelerate releases and compliance; regtechs cut onboarding up to 40% (2024). Card and rail alliances (Visa 200+ countries; VisaNet >65,000 msgs/sec; Mastercard 210+ countries; ACH ~$70T/year) expand acceptance and lower fees. Capital partners (agency MBS $8.3T 2024), insurers (global premiums ~$3.5T 2024) and custodians (AUC >$100T 2024) scale products and liquidity.

| Partner | 2024 Metric |

|---|---|

| Visa/Mastercard | 200+/210+ countries; VisaNet >65,000 msgs/sec |

| ACH | ~$70T annual volume |

| Agency MBS | $8.3T outstanding |

| Custody | AUC >$100T |

What is included in the product

A comprehensive, pre-written BMC aligned with First National Bank’s strategy, covering customer segments, channels, value propositions, revenue streams, key activities and partnerships. Organized into 9 classic blocks with SWOT-linked analysis, competitive advantages and a polished design for presentations and funding discussions.

Condenses First National Bank’s strategy into a digestible, one-page Business Model Canvas with editable cells to quickly identify pain points, align teams, and save hours otherwise spent structuring and formatting internal analyses.

Activities

Relationship-centric lending

Origination and servicing of commercial, consumer and mortgage loans anchor FNBs revenue base, with tailored underwriting and timely servicing driving fee and interest income. Relationship pricing deepens share of wallet by aligning rates and bundles to client segments. Ongoing credit monitoring preserves asset quality through early intervention. Cross-selling maps deposits, cards and wealth solutions to client life cycles.

Treasury and payments services

Treasury and payments services — cash management, receivables, payables and merchant acquiring — create sticky commercial deposits by concentrating operating balances and transaction flows with the bank. Real-time rails such as FedNow (live since July 2023) accelerate collections and disbursements, improving daily cash conversion for clients. API-based embedding lets clients automate treasury functions inside ERP/pos systems, increasing product usage and cross-sell. Advisory on working capital and payment optimization lifts fee income and retention.

Wealth and advisory delivery

Financial planning, investment management, and trust services at First National Bank expanded noninterest income, supporting an estimated 9% AUM growth in 2024; goals-based advice personalizes portfolios to client objectives, while integrated digital tools increased transparency and client engagement; rigorous fiduciary oversight underpins retention and long-term loyalty.

Digital product development

Digital product development delivers iterative mobile, online banking and onboarding builds that optimize customer journeys, with 2024 industry focus on rapid release cycles and personalized experiences. Data analytics drive real-time offers and alerts while embedded cybersecurity and fraud prevention reduce risk by design. Continuous testing improves accessibility, performance and regulatory compliance.

- Iterative releases

- Data-driven personalization

- Security-by-design

- Continuous accessibility & performance testing

Risk, compliance, and capital management

Credit, market, liquidity and operational risk frameworks maintain resilience through limits, early-warning metrics and loss provisioning; banks typically target CET1 near 10–12% versus the Basel III minimum CET1 4.5% (as of 2024) and LCR ≥100% to ensure funding stability.

Stress testing and ALM shape pricing and balance-sheet mix by quantifying scenario losses and interest‑rate risk; AML/KYC controls protect reputation and reduce regulatory fines; capital planning underpins sustainable growth and dividend capacity.

- Risk types: credit, market, liquidity, operational

- Regulatory facts: Basel III CET1 min 4.5% (2024), LCR ≥100%

- Targets: bank CET1 commonly 10–12%

- Controls: stress tests, ALM, AML/KYC, capital planning

Loan NII, FedNow rails and +9% AUM drive fee and deposit growth

Origination and servicing of commercial, consumer and mortgage loans drive NII and fees, with tailored underwriting and credit monitoring preserving asset quality.

Treasury, payments and FedNow-enabled real-time rails concentrate commercial deposits and boost fee income via embedded APIs.

Wealth/advisory (AUM +9% in 2024), digital product releases and strong risk/capital targets (CET1 10–12%, Basel III min 4.5% in 2024) sustain revenue diversification.

| Metric | 2024/Fact |

|---|---|

| AUM growth | +9% |

| CET1 target | 10–12% |

| Basel III CET1 min | 4.5% |

| FedNow | Live Jul 2023 |

What You See Is What You Get

Business Model Canvas

The First National Bank Business Model Canvas preview shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this exact document—complete and fully editable. Files are provided in Word and Excel formats, ready for presenting or customizing. No hidden content or surprises—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a bank's strategic Business Model Canvas to benchmark, scale, and monetize services

Unlock the full strategic blueprint behind First National Bank's Business Model Canvas. This concise, section-by-section analysis reveals how the bank creates customer value, scales core activities, and monetizes services. Download the complete editable Word/Excel canvas to benchmark strategy, inform investments, and adapt proven banking tactics.

Partnerships

Core banking and fintech vendors

Strategic alliances with core system providers and cloud-enabled fintechs drive product agility and improved digital UX by enabling faster feature releases, robust API connectivity, and rapid compliance updates. Co-development with vendors reduces time-to-market and controls tech risk. Strong vendor governance enforces uptime, cybersecurity, and scalability.

Payment networks and processors

Partnerships with Visa (accepted in 200+ countries; VisaNet >65,000 messages/sec) and Mastercard (global reach 210+ countries), ACH operators (U.S. ACH moves over $70 trillion annually) and processors enable cards, treasury and real-time rails, expanding merchant acceptance and lowering transaction friction. Joint risk tools enhance fraud detection through shared screening and alerts, while volume tiers deliver improved interchange economics at scale.

Mortgage, insurance, and wealth platforms

Alliances with mortgage investors, insurers and custodians broaden First National Bank’s product breadth and distribution, linking originations to capital partners; US agency MBS outstanding was about $8.3 trillion in 2024, boosting secondary-market pricing and liquidity. Insurance carriers supply retail and commercial protection solutions—global life/health premiums totaled roughly $3.5 trillion in 2024. Custody partners enable advisory scale and specialist asset servicing, with global custodial AUC above $100 trillion in 2024.

Community, civic, and referral networks

Local chambers, nonprofits and universities strengthen First National Bank brand trust across Mid-Atlantic and Southeast markets; community banks held about 16% of U.S. banking assets in 2024 (FDIC), underscoring local influence. Referral partnerships consistently channel small-business and consumer leads. Financial literacy programs deepen community ties and co-hosted events boost acquisition and retention.

- Chambers: brand trust

- Referrals: lead flow

- Literacy: engagement

- Events: acquisition/retention

Regulatory, risk, and data partners

Regulatory advisors, regtechs and credit bureaus underpin governance and underwriting at First National Bank, enhancing KYC/AML and automated credit decisioning. Model validation firms fortify risk frameworks and independent stress testing. Industry 2024 surveys report partnerships can cut onboarding time by up to 40% and reduce credit losses by up to 20%.

- Compliance advisors

- Regtech integrations

- Credit bureau data

- Model validation

- Faster onboarding, lower losses

Partnerships and rails cut onboarding 40%, expand global reach & liquidity

Key partnerships with core system providers and fintechs accelerate releases and compliance; regtechs cut onboarding up to 40% (2024). Card and rail alliances (Visa 200+ countries; VisaNet >65,000 msgs/sec; Mastercard 210+ countries; ACH ~$70T/year) expand acceptance and lower fees. Capital partners (agency MBS $8.3T 2024), insurers (global premiums ~$3.5T 2024) and custodians (AUC >$100T 2024) scale products and liquidity.

| Partner | 2024 Metric |

|---|---|

| Visa/Mastercard | 200+/210+ countries; VisaNet >65,000 msgs/sec |

| ACH | ~$70T annual volume |

| Agency MBS | $8.3T outstanding |

| Custody | AUC >$100T |

What is included in the product

A comprehensive, pre-written BMC aligned with First National Bank’s strategy, covering customer segments, channels, value propositions, revenue streams, key activities and partnerships. Organized into 9 classic blocks with SWOT-linked analysis, competitive advantages and a polished design for presentations and funding discussions.

Condenses First National Bank’s strategy into a digestible, one-page Business Model Canvas with editable cells to quickly identify pain points, align teams, and save hours otherwise spent structuring and formatting internal analyses.

Activities

Relationship-centric lending

Origination and servicing of commercial, consumer and mortgage loans anchor FNBs revenue base, with tailored underwriting and timely servicing driving fee and interest income. Relationship pricing deepens share of wallet by aligning rates and bundles to client segments. Ongoing credit monitoring preserves asset quality through early intervention. Cross-selling maps deposits, cards and wealth solutions to client life cycles.

Treasury and payments services

Treasury and payments services — cash management, receivables, payables and merchant acquiring — create sticky commercial deposits by concentrating operating balances and transaction flows with the bank. Real-time rails such as FedNow (live since July 2023) accelerate collections and disbursements, improving daily cash conversion for clients. API-based embedding lets clients automate treasury functions inside ERP/pos systems, increasing product usage and cross-sell. Advisory on working capital and payment optimization lifts fee income and retention.

Wealth and advisory delivery

Financial planning, investment management, and trust services at First National Bank expanded noninterest income, supporting an estimated 9% AUM growth in 2024; goals-based advice personalizes portfolios to client objectives, while integrated digital tools increased transparency and client engagement; rigorous fiduciary oversight underpins retention and long-term loyalty.

Digital product development

Digital product development delivers iterative mobile, online banking and onboarding builds that optimize customer journeys, with 2024 industry focus on rapid release cycles and personalized experiences. Data analytics drive real-time offers and alerts while embedded cybersecurity and fraud prevention reduce risk by design. Continuous testing improves accessibility, performance and regulatory compliance.

- Iterative releases

- Data-driven personalization

- Security-by-design

- Continuous accessibility & performance testing

Risk, compliance, and capital management

Credit, market, liquidity and operational risk frameworks maintain resilience through limits, early-warning metrics and loss provisioning; banks typically target CET1 near 10–12% versus the Basel III minimum CET1 4.5% (as of 2024) and LCR ≥100% to ensure funding stability.

Stress testing and ALM shape pricing and balance-sheet mix by quantifying scenario losses and interest‑rate risk; AML/KYC controls protect reputation and reduce regulatory fines; capital planning underpins sustainable growth and dividend capacity.

- Risk types: credit, market, liquidity, operational

- Regulatory facts: Basel III CET1 min 4.5% (2024), LCR ≥100%

- Targets: bank CET1 commonly 10–12%

- Controls: stress tests, ALM, AML/KYC, capital planning

Loan NII, FedNow rails and +9% AUM drive fee and deposit growth

Origination and servicing of commercial, consumer and mortgage loans drive NII and fees, with tailored underwriting and credit monitoring preserving asset quality.

Treasury, payments and FedNow-enabled real-time rails concentrate commercial deposits and boost fee income via embedded APIs.

Wealth/advisory (AUM +9% in 2024), digital product releases and strong risk/capital targets (CET1 10–12%, Basel III min 4.5% in 2024) sustain revenue diversification.

| Metric | 2024/Fact |

|---|---|

| AUM growth | +9% |

| CET1 target | 10–12% |

| Basel III CET1 min | 4.5% |

| FedNow | Live Jul 2023 |

What You See Is What You Get

Business Model Canvas

The First National Bank Business Model Canvas preview shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this exact document—complete and fully editable. Files are provided in Word and Excel formats, ready for presenting or customizing. No hidden content or surprises—what you see is what you get.