Ford Motor PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological disruption, legal changes, and environmental pressures are converging to reshape Ford Motor’s strategy and performance. Our concise PESTLE pinpoints risks and opportunities for investors and strategists. Buy the full, fully sourced PESTLE now to get detailed, actionable insights ready for immediate use.

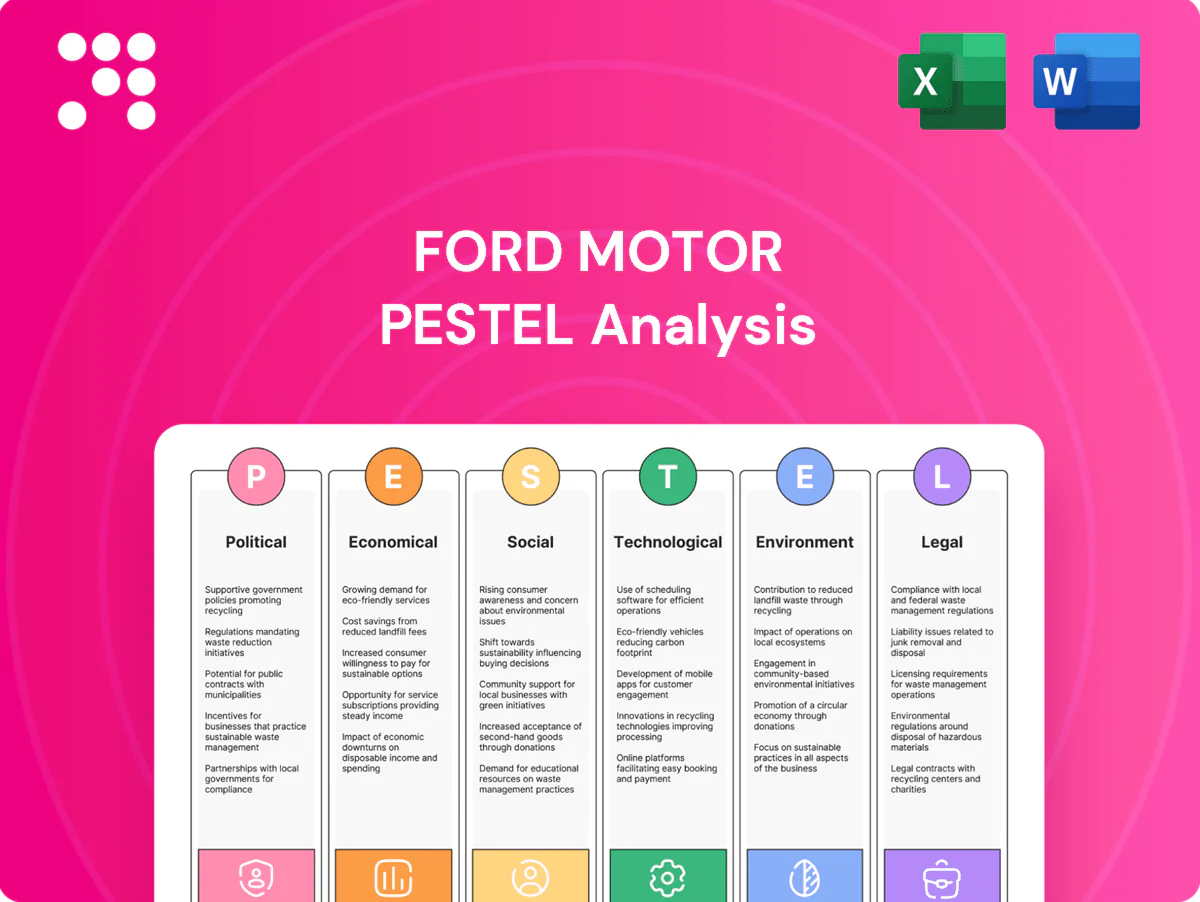

Political factors

EV incentives and industrial policy

U.S. subsidies under the $369 billion Inflation Reduction Act and EU Green Deal rules, plus the $7,500 EV tax credit, directly shape Ford’s pricing, localization and supply‑chain siting. Eligibility rules requiring domestic battery materials and final assembly push Ford’s North American investment (Ford has targeted roughly $50 billion for EVs/AVs through 2026). Policy shifts or budget cuts could compress margins and slow adoption. Ford must time product cadence to capture credits without overreliance.

Trade tariffs and geopolitics

Section 232 tariffs (25% steel, 10% aluminum) and curbs on Chinese EV components raise Ford's input costs and complicate sourcing. US export controls since 2022 on advanced chips and tightened 2023–24 measures target batteries and critical minerals, constraining suppliers. USMCA's 75% North American content rule shifts supplier choices. Sudden tariff swings can delay launches and compress margins.

Regulatory emission targets

Stricter U.S. and EU rules — including the U.S. 50% EV sales federal 2030 goal and the EU target of 55% new‑car CO2 cuts by 2030 and zero tailpipe emissions for new cars by 2035 — are accelerating Ford’s shift to EVs and hybrids. Non‑compliance exposes Ford to heavy penalties and forced fleet reshaping under EU/US regimes. Divergent regional timelines complicate global platform planning and capex. Emissions credits trading and OEM partnerships provide short‑term compliance levers.

Public procurement and infrastructure

Government fleet electrification driven by Executive Order 14057 (2021) and federal procurement expands Ford’s addressable EV market via large fleet buys; the NEVI program provides $5 billion in federal funding for charger build‑outs, while funding cycles and permitting speed directly affect charger availability for customers. Federal and state grants influence dealer investments, and DOT‑designated priority corridors concentrate geographic sales traction.

- EO 14057: federal fleet electrification increases commercial demand

- NEVI $5B: accelerates public charger rollout

- Permitting/funding cycles: key to charger uptime and customer access

- Priority corridors: drive regional sales momentum

Political stability and localization

- IRA $369B climate package

- US EV tax-credit: North American final assembly/domestic content rules

- Supplier clustering from localization mandates

- State incentives often reach hundreds of millions, affecting IRR

IRA $369B, $7,500 EV credit & NEVI $5B speed EV rollout

IRA $369B, $7,500 EV credit and NEVI $5B force localization, affect pricing and charger rollout. USMCA 75% content, Section 232 tariffs (25% steel, 10% aluminum) and export controls raise input/sourcing risk. EU/US 2030–35 EV targets accelerate Ford’s ~$50B EV/AV capex to 2026 and compress non‑compliant fleet options.

| Factor | Value | Impact |

|---|---|---|

| IRA | $369B | Subsidies, localization |

| EV credit | $7,500 | Pricing/uptake |

| NEVI | $5B | Charger buildout |

What is included in the product

Explores how macro-environmental forces uniquely affect Ford Motor across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples. Designed for executives and investors, it highlights threats, opportunities and forward-looking implications for strategy and scenario planning.

A concise, visually segmented PESTLE snapshot for Ford that can be dropped into presentations, annotated for region- or business-specific notes, and easily shared to speed alignment, support risk discussions, and streamline strategic planning across teams.

Economic factors

Interest rates and affordability

Higher policy rates—Fed funds roughly 5.25–5.50% in mid‑2025—raise monthly payments and worsen leasing math for Ford Credit, squeezing demand. Consumers shift to lower trims and used cars as Manheim values remain about 20–25% below 2021 peaks, reducing average transaction prices. Rate cuts historically revive retail finance and inventory turns quickly. Elevated credit losses and volatile residuals amplify Ford earnings swings.

Commodity and battery materials

Lithium, nickel, cobalt and graphite swings materially affect EV margins; Benchmark Mineral Intelligence showed lithium carbonate around 20,000 USD/t, nickel ~18,000 USD/t, cobalt ~35,000 USD/t and natural graphite ~2,000 USD/t in mid‑2025. Hedging and long‑term offtakes stabilize costs but add rigidity. Material substitution (LFP vs NMC) trades cost and range versus supply risk, while growing recycling capacity can dampen future input volatility.

Supply chain resilience

Semiconductor and logistics constraints continue to cause intermittent production risk for Ford, as the 2021–22 chip shock cost the auto industry roughly 7.7 million lost vehicles and ~USD 110 billion in forgone revenue. Ford has shifted from pure just-in-time toward just-in-case via dual-sourcing, buffer inventories and nearshoring, raising resilience but increasing supply costs. Supplier financial health and long tooling lead times still materially affect launch reliability.

FX and regional mix

Dollar strength in 2024–25 compressed Ford’s overseas earnings translation and made US exports less price-competitive, while stronger U.S. demand for trucks versus Europe’s van/commercial demand shifted Ford’s margin mix toward higher-margin trucks in North America and lower-margin vans in the EU.

- FX: USD appreciation reduced reported foreign revenue.

- Regional mix: US trucks lift margins; EU vans weigh them down.

- Sourcing: local content cuts translation risk but component exposure remains.

- Hedging: smooths EPS volatility, does not change underlying cash economics.

Cyclical demand and fleet cycles

Macro slowdowns typically depress retail sales first while commercial and government fleet purchases lag by several quarters, with fleet replacement cycles often cushioning volumes during recovery; pent‑up replacement can lift post‑recession demand. Incentive discipline is critical to protect residual values and used‑vehicle pricing, and inventory normalization materially improves operating leverage by reducing holding costs and discounting.

- Retail hits first; fleets lag

- Pent‑up replacements can boost volumes

- Incentive discipline protects residuals and margins

- US fleet share roughly 13–15% of new volume

IRA $369B, $7,500 EV credit & NEVI $5B speed EV rollout

Higher policy rates (Fed funds 5.25–5.50% mid‑2025) squeeze Ford Credit, lowering retail demand and lease activity. Used values remain about 20–25% below 2021 peaks, reducing transaction prices and margins. EV material costs (lithium ~20,000 USD/t; nickel ~18,000 USD/t) and semiconductor/logistics shocks (2021–22 ~7.7M lost vehicles, ~110B USD revenue) heighten earnings volatility.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| Manheim vs 2021 | -20–25% |

| Lithium | ~20,000 USD/t |

| Chip shock impact | 7.7M vehicles; ~110B USD |

| US fleet share | 13–15% |

Same Document Delivered

Ford Motor PESTLE Analysis

The preview shown here is the exact Ford Motor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real snapshot of the product, delivered exactly as shown with no placeholders or teasers. After payment you’ll instantly download this same final document to support your strategic and investment decisions.

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological disruption, legal changes, and environmental pressures are converging to reshape Ford Motor’s strategy and performance. Our concise PESTLE pinpoints risks and opportunities for investors and strategists. Buy the full, fully sourced PESTLE now to get detailed, actionable insights ready for immediate use.

Political factors

EV incentives and industrial policy

U.S. subsidies under the $369 billion Inflation Reduction Act and EU Green Deal rules, plus the $7,500 EV tax credit, directly shape Ford’s pricing, localization and supply‑chain siting. Eligibility rules requiring domestic battery materials and final assembly push Ford’s North American investment (Ford has targeted roughly $50 billion for EVs/AVs through 2026). Policy shifts or budget cuts could compress margins and slow adoption. Ford must time product cadence to capture credits without overreliance.

Trade tariffs and geopolitics

Section 232 tariffs (25% steel, 10% aluminum) and curbs on Chinese EV components raise Ford's input costs and complicate sourcing. US export controls since 2022 on advanced chips and tightened 2023–24 measures target batteries and critical minerals, constraining suppliers. USMCA's 75% North American content rule shifts supplier choices. Sudden tariff swings can delay launches and compress margins.

Regulatory emission targets

Stricter U.S. and EU rules — including the U.S. 50% EV sales federal 2030 goal and the EU target of 55% new‑car CO2 cuts by 2030 and zero tailpipe emissions for new cars by 2035 — are accelerating Ford’s shift to EVs and hybrids. Non‑compliance exposes Ford to heavy penalties and forced fleet reshaping under EU/US regimes. Divergent regional timelines complicate global platform planning and capex. Emissions credits trading and OEM partnerships provide short‑term compliance levers.

Public procurement and infrastructure

Government fleet electrification driven by Executive Order 14057 (2021) and federal procurement expands Ford’s addressable EV market via large fleet buys; the NEVI program provides $5 billion in federal funding for charger build‑outs, while funding cycles and permitting speed directly affect charger availability for customers. Federal and state grants influence dealer investments, and DOT‑designated priority corridors concentrate geographic sales traction.

- EO 14057: federal fleet electrification increases commercial demand

- NEVI $5B: accelerates public charger rollout

- Permitting/funding cycles: key to charger uptime and customer access

- Priority corridors: drive regional sales momentum

Political stability and localization

- IRA $369B climate package

- US EV tax-credit: North American final assembly/domestic content rules

- Supplier clustering from localization mandates

- State incentives often reach hundreds of millions, affecting IRR

IRA $369B, $7,500 EV credit & NEVI $5B speed EV rollout

IRA $369B, $7,500 EV credit and NEVI $5B force localization, affect pricing and charger rollout. USMCA 75% content, Section 232 tariffs (25% steel, 10% aluminum) and export controls raise input/sourcing risk. EU/US 2030–35 EV targets accelerate Ford’s ~$50B EV/AV capex to 2026 and compress non‑compliant fleet options.

| Factor | Value | Impact |

|---|---|---|

| IRA | $369B | Subsidies, localization |

| EV credit | $7,500 | Pricing/uptake |

| NEVI | $5B | Charger buildout |

What is included in the product

Explores how macro-environmental forces uniquely affect Ford Motor across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples. Designed for executives and investors, it highlights threats, opportunities and forward-looking implications for strategy and scenario planning.

A concise, visually segmented PESTLE snapshot for Ford that can be dropped into presentations, annotated for region- or business-specific notes, and easily shared to speed alignment, support risk discussions, and streamline strategic planning across teams.

Economic factors

Interest rates and affordability

Higher policy rates—Fed funds roughly 5.25–5.50% in mid‑2025—raise monthly payments and worsen leasing math for Ford Credit, squeezing demand. Consumers shift to lower trims and used cars as Manheim values remain about 20–25% below 2021 peaks, reducing average transaction prices. Rate cuts historically revive retail finance and inventory turns quickly. Elevated credit losses and volatile residuals amplify Ford earnings swings.

Commodity and battery materials

Lithium, nickel, cobalt and graphite swings materially affect EV margins; Benchmark Mineral Intelligence showed lithium carbonate around 20,000 USD/t, nickel ~18,000 USD/t, cobalt ~35,000 USD/t and natural graphite ~2,000 USD/t in mid‑2025. Hedging and long‑term offtakes stabilize costs but add rigidity. Material substitution (LFP vs NMC) trades cost and range versus supply risk, while growing recycling capacity can dampen future input volatility.

Supply chain resilience

Semiconductor and logistics constraints continue to cause intermittent production risk for Ford, as the 2021–22 chip shock cost the auto industry roughly 7.7 million lost vehicles and ~USD 110 billion in forgone revenue. Ford has shifted from pure just-in-time toward just-in-case via dual-sourcing, buffer inventories and nearshoring, raising resilience but increasing supply costs. Supplier financial health and long tooling lead times still materially affect launch reliability.

FX and regional mix

Dollar strength in 2024–25 compressed Ford’s overseas earnings translation and made US exports less price-competitive, while stronger U.S. demand for trucks versus Europe’s van/commercial demand shifted Ford’s margin mix toward higher-margin trucks in North America and lower-margin vans in the EU.

- FX: USD appreciation reduced reported foreign revenue.

- Regional mix: US trucks lift margins; EU vans weigh them down.

- Sourcing: local content cuts translation risk but component exposure remains.

- Hedging: smooths EPS volatility, does not change underlying cash economics.

Cyclical demand and fleet cycles

Macro slowdowns typically depress retail sales first while commercial and government fleet purchases lag by several quarters, with fleet replacement cycles often cushioning volumes during recovery; pent‑up replacement can lift post‑recession demand. Incentive discipline is critical to protect residual values and used‑vehicle pricing, and inventory normalization materially improves operating leverage by reducing holding costs and discounting.

- Retail hits first; fleets lag

- Pent‑up replacements can boost volumes

- Incentive discipline protects residuals and margins

- US fleet share roughly 13–15% of new volume

IRA $369B, $7,500 EV credit & NEVI $5B speed EV rollout

Higher policy rates (Fed funds 5.25–5.50% mid‑2025) squeeze Ford Credit, lowering retail demand and lease activity. Used values remain about 20–25% below 2021 peaks, reducing transaction prices and margins. EV material costs (lithium ~20,000 USD/t; nickel ~18,000 USD/t) and semiconductor/logistics shocks (2021–22 ~7.7M lost vehicles, ~110B USD revenue) heighten earnings volatility.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| Manheim vs 2021 | -20–25% |

| Lithium | ~20,000 USD/t |

| Chip shock impact | 7.7M vehicles; ~110B USD |

| US fleet share | 13–15% |

Same Document Delivered

Ford Motor PESTLE Analysis

The preview shown here is the exact Ford Motor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real snapshot of the product, delivered exactly as shown with no placeholders or teasers. After payment you’ll instantly download this same final document to support your strategic and investment decisions.

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological disruption, legal changes, and environmental pressures are converging to reshape Ford Motor’s strategy and performance. Our concise PESTLE pinpoints risks and opportunities for investors and strategists. Buy the full, fully sourced PESTLE now to get detailed, actionable insights ready for immediate use.

Political factors

EV incentives and industrial policy

U.S. subsidies under the $369 billion Inflation Reduction Act and EU Green Deal rules, plus the $7,500 EV tax credit, directly shape Ford’s pricing, localization and supply‑chain siting. Eligibility rules requiring domestic battery materials and final assembly push Ford’s North American investment (Ford has targeted roughly $50 billion for EVs/AVs through 2026). Policy shifts or budget cuts could compress margins and slow adoption. Ford must time product cadence to capture credits without overreliance.

Trade tariffs and geopolitics

Section 232 tariffs (25% steel, 10% aluminum) and curbs on Chinese EV components raise Ford's input costs and complicate sourcing. US export controls since 2022 on advanced chips and tightened 2023–24 measures target batteries and critical minerals, constraining suppliers. USMCA's 75% North American content rule shifts supplier choices. Sudden tariff swings can delay launches and compress margins.

Regulatory emission targets

Stricter U.S. and EU rules — including the U.S. 50% EV sales federal 2030 goal and the EU target of 55% new‑car CO2 cuts by 2030 and zero tailpipe emissions for new cars by 2035 — are accelerating Ford’s shift to EVs and hybrids. Non‑compliance exposes Ford to heavy penalties and forced fleet reshaping under EU/US regimes. Divergent regional timelines complicate global platform planning and capex. Emissions credits trading and OEM partnerships provide short‑term compliance levers.

Public procurement and infrastructure

Government fleet electrification driven by Executive Order 14057 (2021) and federal procurement expands Ford’s addressable EV market via large fleet buys; the NEVI program provides $5 billion in federal funding for charger build‑outs, while funding cycles and permitting speed directly affect charger availability for customers. Federal and state grants influence dealer investments, and DOT‑designated priority corridors concentrate geographic sales traction.

- EO 14057: federal fleet electrification increases commercial demand

- NEVI $5B: accelerates public charger rollout

- Permitting/funding cycles: key to charger uptime and customer access

- Priority corridors: drive regional sales momentum

Political stability and localization

- IRA $369B climate package

- US EV tax-credit: North American final assembly/domestic content rules

- Supplier clustering from localization mandates

- State incentives often reach hundreds of millions, affecting IRR

IRA $369B, $7,500 EV credit & NEVI $5B speed EV rollout

IRA $369B, $7,500 EV credit and NEVI $5B force localization, affect pricing and charger rollout. USMCA 75% content, Section 232 tariffs (25% steel, 10% aluminum) and export controls raise input/sourcing risk. EU/US 2030–35 EV targets accelerate Ford’s ~$50B EV/AV capex to 2026 and compress non‑compliant fleet options.

| Factor | Value | Impact |

|---|---|---|

| IRA | $369B | Subsidies, localization |

| EV credit | $7,500 | Pricing/uptake |

| NEVI | $5B | Charger buildout |

What is included in the product

Explores how macro-environmental forces uniquely affect Ford Motor across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples. Designed for executives and investors, it highlights threats, opportunities and forward-looking implications for strategy and scenario planning.

A concise, visually segmented PESTLE snapshot for Ford that can be dropped into presentations, annotated for region- or business-specific notes, and easily shared to speed alignment, support risk discussions, and streamline strategic planning across teams.

Economic factors

Interest rates and affordability

Higher policy rates—Fed funds roughly 5.25–5.50% in mid‑2025—raise monthly payments and worsen leasing math for Ford Credit, squeezing demand. Consumers shift to lower trims and used cars as Manheim values remain about 20–25% below 2021 peaks, reducing average transaction prices. Rate cuts historically revive retail finance and inventory turns quickly. Elevated credit losses and volatile residuals amplify Ford earnings swings.

Commodity and battery materials

Lithium, nickel, cobalt and graphite swings materially affect EV margins; Benchmark Mineral Intelligence showed lithium carbonate around 20,000 USD/t, nickel ~18,000 USD/t, cobalt ~35,000 USD/t and natural graphite ~2,000 USD/t in mid‑2025. Hedging and long‑term offtakes stabilize costs but add rigidity. Material substitution (LFP vs NMC) trades cost and range versus supply risk, while growing recycling capacity can dampen future input volatility.

Supply chain resilience

Semiconductor and logistics constraints continue to cause intermittent production risk for Ford, as the 2021–22 chip shock cost the auto industry roughly 7.7 million lost vehicles and ~USD 110 billion in forgone revenue. Ford has shifted from pure just-in-time toward just-in-case via dual-sourcing, buffer inventories and nearshoring, raising resilience but increasing supply costs. Supplier financial health and long tooling lead times still materially affect launch reliability.

FX and regional mix

Dollar strength in 2024–25 compressed Ford’s overseas earnings translation and made US exports less price-competitive, while stronger U.S. demand for trucks versus Europe’s van/commercial demand shifted Ford’s margin mix toward higher-margin trucks in North America and lower-margin vans in the EU.

- FX: USD appreciation reduced reported foreign revenue.

- Regional mix: US trucks lift margins; EU vans weigh them down.

- Sourcing: local content cuts translation risk but component exposure remains.

- Hedging: smooths EPS volatility, does not change underlying cash economics.

Cyclical demand and fleet cycles

Macro slowdowns typically depress retail sales first while commercial and government fleet purchases lag by several quarters, with fleet replacement cycles often cushioning volumes during recovery; pent‑up replacement can lift post‑recession demand. Incentive discipline is critical to protect residual values and used‑vehicle pricing, and inventory normalization materially improves operating leverage by reducing holding costs and discounting.

- Retail hits first; fleets lag

- Pent‑up replacements can boost volumes

- Incentive discipline protects residuals and margins

- US fleet share roughly 13–15% of new volume

IRA $369B, $7,500 EV credit & NEVI $5B speed EV rollout

Higher policy rates (Fed funds 5.25–5.50% mid‑2025) squeeze Ford Credit, lowering retail demand and lease activity. Used values remain about 20–25% below 2021 peaks, reducing transaction prices and margins. EV material costs (lithium ~20,000 USD/t; nickel ~18,000 USD/t) and semiconductor/logistics shocks (2021–22 ~7.7M lost vehicles, ~110B USD revenue) heighten earnings volatility.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| Manheim vs 2021 | -20–25% |

| Lithium | ~20,000 USD/t |

| Chip shock impact | 7.7M vehicles; ~110B USD |

| US fleet share | 13–15% |

Same Document Delivered

Ford Motor PESTLE Analysis

The preview shown here is the exact Ford Motor PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real snapshot of the product, delivered exactly as shown with no placeholders or teasers. After payment you’ll instantly download this same final document to support your strategic and investment decisions.