Ford Otosan Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

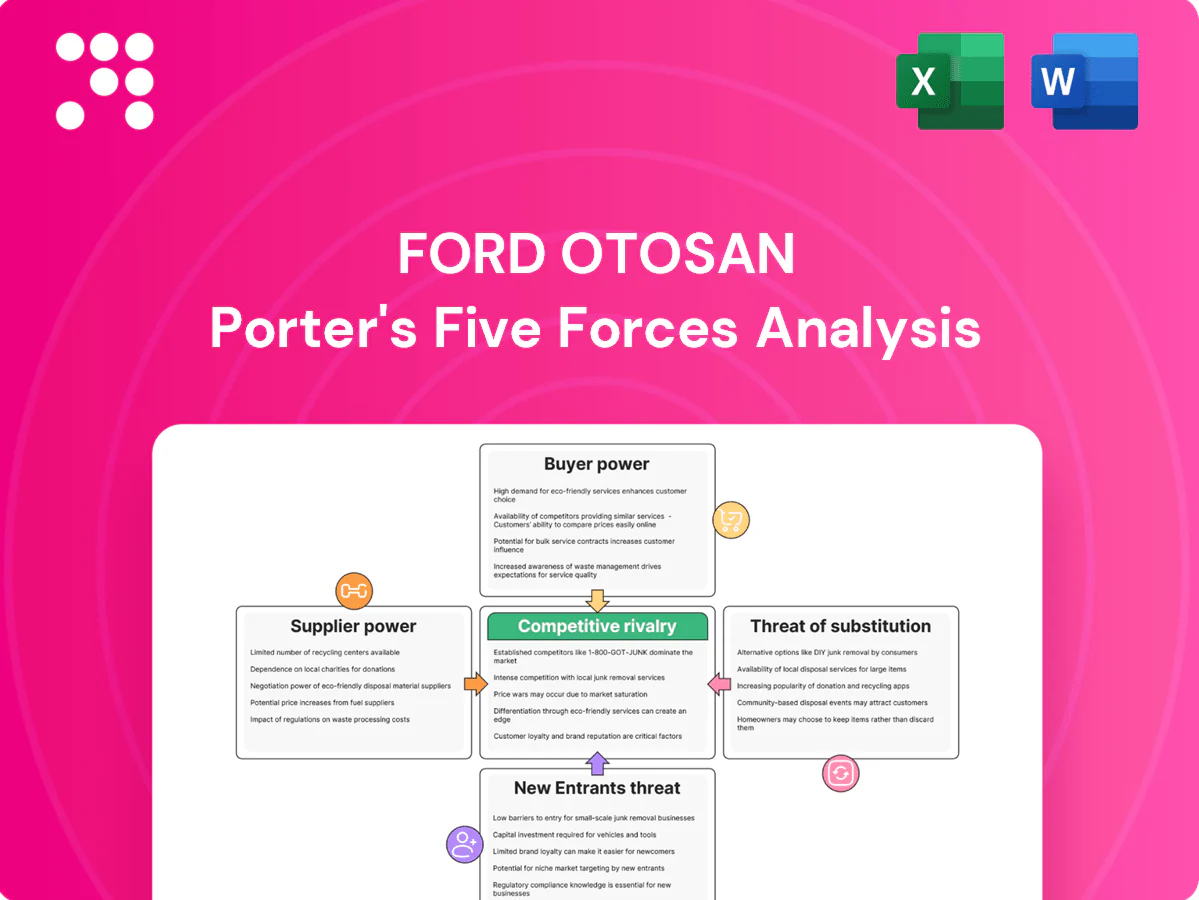

Ford Otosan navigates intense rivalry, evolving buyer preferences, and supply-chain complexity in a capital-intensive auto market. Competitive pressures from global OEMs and electrification raise new strategic risks and opportunities. This brief scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Ford Otosan.

Suppliers Bargaining Power

Global OEM-backed sourcing leverage

As a Ford JV, Ford Otosan leverages Ford’s global procurement scale—Ford reported roughly $145 billion in global purchasing in 2024—to negotiate favorable supplier terms. Pooled volumes and standardized platforms cut per-unit input costs and dilute individual supplier bargaining power. This scale enables dual-sourcing strategies and accelerated cost take-outs, supporting margin resilience and supply continuity.

Dependence on specialized components

Dependence on specialized components—power electronics, semiconductors, e-axles and battery packs—concentrates suppliers and raises switching costs due to limited substitutes and lengthy qualification cycles. CATL retained roughly 34% share of global EV cell supply in 2023, underscoring battery supplier concentration that affects Ford Otosan's EV sourcing. Supplier power is elevated in EV and ADAS domains, with semiconductor lead times in 2024 reported at roughly 20–30 weeks, amplifying disruption risk.

Local Turkish supplier ecosystem

A mature tier-1/2 supplier base in Turkey, with over 1,000 automotive suppliers, delivers proximity and cost advantages that constrain supplier power. Intense local competition further moderates pricing leverage, though sustained lira volatility and double-digit inflation in 2023–24 have tightened margins and forced repricing. Ongoing localization demands continuous capability and quality upgrades to meet Ford’s global standards.

Long-term contracts and co-development

Logistics and commodity exposure

Steel, aluminum, energy and freight swings materially affect Ford Otosan’s total cost of ownership, with material costs roughly half of vehicle BOM and steel/aluminum about 20% of materials; suppliers frequently pass surcharges during volatility, squeezing margins. Ford Otosan uses hedging and design-for-cost measures to mitigate exposure but cannot fully offset acute price shocks. Port congestion and rerouted geopolitical lanes add bargaining friction and lead times.

- Material share: ~50% of BOM

- Steel/aluminium: ~20% of materials

- Freight/energy surcharges: passed through in volatility

- Hedge + design reduce but don’t eliminate shocks

Scale $145bn cuts supplier power; EV cells ~34%

Ford Otosan benefits from Ford’s $145bn global purchasing (2024) to dilute supplier power, enabling dual-sourcing and cost take-outs. Concentration in EV cells (CATL ~34% global share 2023) and semiconductors (lead times ~20–30 weeks in 2024) elevates supplier leverage for EV/ADAS modules. Local Turkish base of >1,000 suppliers and ~50% BOM material share tempers but does not eliminate pricing risk amid 2023–24 double-digit inflation.

| Metric | Value |

|---|---|

| Ford global purchasing (2024) | $145bn |

| CATL global EV cell share (2023) | ~34% |

| Semiconductor lead times (2024) | 20–30 weeks |

| Turkish auto suppliers | >1,000 |

| Materials share of BOM | ~50% |

What is included in the product

Tailored Porter's Five Forces analysis for Ford Otosan that assesses competitive rivalry, supplier and buyer power, entry barriers and substitutes to reveal strategic risks and opportunities.

A concise Ford Otosan Porter's Five Forces one-sheet that visualizes competitive pressure with an editable spider chart for instant strategic clarity. Customizable inputs and a clean layout make it slide-ready, easy to update for new data, and usable by non-finance teams.

Customers Bargaining Power

Fleet and export-driven demand

Large fleets and international distributors buy in volume and negotiate aggressively, using tender-based procurement that prioritizes total cost of ownership and uptime. Buyers leverage competing LCV models to extract price discounts and demand service contracts, uptime guarantees and penalty clauses. Service-level concessions—spare parts logistics, uptime SLAs and extended warranties—become decisive in winning large fleet tenders.

Moderate switching costs

Platform compatibility, standardized body-builder interfaces and aftersales tie-ins create lock-in for Ford Otosan buyers, limiting willingness to switch. Fleets typically rotate models every 3-5 years with limited retraining, enabling periodic churn. In tight markets lead times of up to 6 months can outweigh brand loyalty, elevating buyer power during cyclical troughs.

Dealer and distributor networks

Multi-brand dealers benchmark Ford Otosan offers and promotions against 5–10 competing brands in Turkey in 2024, raising price and incentive transparency. Inventory financing and manufacturer incentives materially influence channel behavior, with dealers prioritizing units carrying stronger floor-plan support. Transparent pricing across markets increases comparability and lets networks push for better rebates and sell-through terms to protect margins.

Evolving TCO in electrification

EV van TCO now centers on energy cost, residuals and charging uptime, with fleets targeting >95% availability. Buyers demand price protection, 8-year/160,000 km battery warranties and regular OTA software updates. Data-driven fleet management (telemetry can lift utilization 10–15%) and subsidy shifts increase buyer leverage and prompt re-pricing requests.

- Energy cost emphasis

- Battery warranty: 8y/160k km

- Charging uptime >95%

- Telemetry boosts negotiation (10–15%)

Brand, reliability, and service as mitigants

Ford Pro’s ecosystem—over 1 million connected commercial vehicles by 2024—plus telematics and a wide service footprint reduce buyer price sensitivity by shifting value to uptime and lifecycle costs. High uptime and parts availability (service-level targets above 90% in key markets) create value beyond sticker price, while stronger residuals temper discount demands. Customization and integration options embed Ford Otosan deeper into fleet operations, raising switching costs.

- Ford Pro connected vehicles: 1,000,000+ (2024)

- Service uptime/availability: >90% targets

- Residual value strength: reduces discount pressure

- Customization: increases operational stickiness

Scale and uptime beat price: 1,000,000+ connected, >95%

Large fleets and distributors exert strong price and SLA pressure via tenders, leveraging 3–5 year replacement cycles and lead times up to 6 months to negotiate discounts and uptime clauses. EV buyers focus on TCO: energy, residuals, charging uptime (>95%) and 8y/160k km battery warranties. Ford Pro scale (1,000,000+ connected vehicles in 2024) and >90% service targets reduce pure price sensitivity by shifting value to uptime.

| Metric | 2024 Value |

|---|---|

| Connected vehicles | 1,000,000+ |

| Service uptime target | >90% |

| Charging uptime | >95% |

| Battery warranty | 8y / 160,000 km |

| Fleet rotation | 3–5 yrs |

Same Document Delivered

Ford Otosan Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Ford Otosan you’ll receive—comprehensive, professionally formatted, and ready to use. It covers threat of new entrants, supplier and buyer power, substitutes, and competitive rivalry with data-driven insights. No placeholders or samples. Instant download after purchase.

A Must-Have Tool for Decision-Makers

Ford Otosan navigates intense rivalry, evolving buyer preferences, and supply-chain complexity in a capital-intensive auto market. Competitive pressures from global OEMs and electrification raise new strategic risks and opportunities. This brief scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Ford Otosan.

Suppliers Bargaining Power

Global OEM-backed sourcing leverage

As a Ford JV, Ford Otosan leverages Ford’s global procurement scale—Ford reported roughly $145 billion in global purchasing in 2024—to negotiate favorable supplier terms. Pooled volumes and standardized platforms cut per-unit input costs and dilute individual supplier bargaining power. This scale enables dual-sourcing strategies and accelerated cost take-outs, supporting margin resilience and supply continuity.

Dependence on specialized components

Dependence on specialized components—power electronics, semiconductors, e-axles and battery packs—concentrates suppliers and raises switching costs due to limited substitutes and lengthy qualification cycles. CATL retained roughly 34% share of global EV cell supply in 2023, underscoring battery supplier concentration that affects Ford Otosan's EV sourcing. Supplier power is elevated in EV and ADAS domains, with semiconductor lead times in 2024 reported at roughly 20–30 weeks, amplifying disruption risk.

Local Turkish supplier ecosystem

A mature tier-1/2 supplier base in Turkey, with over 1,000 automotive suppliers, delivers proximity and cost advantages that constrain supplier power. Intense local competition further moderates pricing leverage, though sustained lira volatility and double-digit inflation in 2023–24 have tightened margins and forced repricing. Ongoing localization demands continuous capability and quality upgrades to meet Ford’s global standards.

Long-term contracts and co-development

Logistics and commodity exposure

Steel, aluminum, energy and freight swings materially affect Ford Otosan’s total cost of ownership, with material costs roughly half of vehicle BOM and steel/aluminum about 20% of materials; suppliers frequently pass surcharges during volatility, squeezing margins. Ford Otosan uses hedging and design-for-cost measures to mitigate exposure but cannot fully offset acute price shocks. Port congestion and rerouted geopolitical lanes add bargaining friction and lead times.

- Material share: ~50% of BOM

- Steel/aluminium: ~20% of materials

- Freight/energy surcharges: passed through in volatility

- Hedge + design reduce but don’t eliminate shocks

Scale $145bn cuts supplier power; EV cells ~34%

Ford Otosan benefits from Ford’s $145bn global purchasing (2024) to dilute supplier power, enabling dual-sourcing and cost take-outs. Concentration in EV cells (CATL ~34% global share 2023) and semiconductors (lead times ~20–30 weeks in 2024) elevates supplier leverage for EV/ADAS modules. Local Turkish base of >1,000 suppliers and ~50% BOM material share tempers but does not eliminate pricing risk amid 2023–24 double-digit inflation.

| Metric | Value |

|---|---|

| Ford global purchasing (2024) | $145bn |

| CATL global EV cell share (2023) | ~34% |

| Semiconductor lead times (2024) | 20–30 weeks |

| Turkish auto suppliers | >1,000 |

| Materials share of BOM | ~50% |

What is included in the product

Tailored Porter's Five Forces analysis for Ford Otosan that assesses competitive rivalry, supplier and buyer power, entry barriers and substitutes to reveal strategic risks and opportunities.

A concise Ford Otosan Porter's Five Forces one-sheet that visualizes competitive pressure with an editable spider chart for instant strategic clarity. Customizable inputs and a clean layout make it slide-ready, easy to update for new data, and usable by non-finance teams.

Customers Bargaining Power

Fleet and export-driven demand

Large fleets and international distributors buy in volume and negotiate aggressively, using tender-based procurement that prioritizes total cost of ownership and uptime. Buyers leverage competing LCV models to extract price discounts and demand service contracts, uptime guarantees and penalty clauses. Service-level concessions—spare parts logistics, uptime SLAs and extended warranties—become decisive in winning large fleet tenders.

Moderate switching costs

Platform compatibility, standardized body-builder interfaces and aftersales tie-ins create lock-in for Ford Otosan buyers, limiting willingness to switch. Fleets typically rotate models every 3-5 years with limited retraining, enabling periodic churn. In tight markets lead times of up to 6 months can outweigh brand loyalty, elevating buyer power during cyclical troughs.

Dealer and distributor networks

Multi-brand dealers benchmark Ford Otosan offers and promotions against 5–10 competing brands in Turkey in 2024, raising price and incentive transparency. Inventory financing and manufacturer incentives materially influence channel behavior, with dealers prioritizing units carrying stronger floor-plan support. Transparent pricing across markets increases comparability and lets networks push for better rebates and sell-through terms to protect margins.

Evolving TCO in electrification

EV van TCO now centers on energy cost, residuals and charging uptime, with fleets targeting >95% availability. Buyers demand price protection, 8-year/160,000 km battery warranties and regular OTA software updates. Data-driven fleet management (telemetry can lift utilization 10–15%) and subsidy shifts increase buyer leverage and prompt re-pricing requests.

- Energy cost emphasis

- Battery warranty: 8y/160k km

- Charging uptime >95%

- Telemetry boosts negotiation (10–15%)

Brand, reliability, and service as mitigants

Ford Pro’s ecosystem—over 1 million connected commercial vehicles by 2024—plus telematics and a wide service footprint reduce buyer price sensitivity by shifting value to uptime and lifecycle costs. High uptime and parts availability (service-level targets above 90% in key markets) create value beyond sticker price, while stronger residuals temper discount demands. Customization and integration options embed Ford Otosan deeper into fleet operations, raising switching costs.

- Ford Pro connected vehicles: 1,000,000+ (2024)

- Service uptime/availability: >90% targets

- Residual value strength: reduces discount pressure

- Customization: increases operational stickiness

Scale and uptime beat price: 1,000,000+ connected, >95%

Large fleets and distributors exert strong price and SLA pressure via tenders, leveraging 3–5 year replacement cycles and lead times up to 6 months to negotiate discounts and uptime clauses. EV buyers focus on TCO: energy, residuals, charging uptime (>95%) and 8y/160k km battery warranties. Ford Pro scale (1,000,000+ connected vehicles in 2024) and >90% service targets reduce pure price sensitivity by shifting value to uptime.

| Metric | 2024 Value |

|---|---|

| Connected vehicles | 1,000,000+ |

| Service uptime target | >90% |

| Charging uptime | >95% |

| Battery warranty | 8y / 160,000 km |

| Fleet rotation | 3–5 yrs |

Same Document Delivered

Ford Otosan Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Ford Otosan you’ll receive—comprehensive, professionally formatted, and ready to use. It covers threat of new entrants, supplier and buyer power, substitutes, and competitive rivalry with data-driven insights. No placeholders or samples. Instant download after purchase.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Ford Otosan navigates intense rivalry, evolving buyer preferences, and supply-chain complexity in a capital-intensive auto market. Competitive pressures from global OEMs and electrification raise new strategic risks and opportunities. This brief scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Ford Otosan.

Suppliers Bargaining Power

Global OEM-backed sourcing leverage

As a Ford JV, Ford Otosan leverages Ford’s global procurement scale—Ford reported roughly $145 billion in global purchasing in 2024—to negotiate favorable supplier terms. Pooled volumes and standardized platforms cut per-unit input costs and dilute individual supplier bargaining power. This scale enables dual-sourcing strategies and accelerated cost take-outs, supporting margin resilience and supply continuity.

Dependence on specialized components

Dependence on specialized components—power electronics, semiconductors, e-axles and battery packs—concentrates suppliers and raises switching costs due to limited substitutes and lengthy qualification cycles. CATL retained roughly 34% share of global EV cell supply in 2023, underscoring battery supplier concentration that affects Ford Otosan's EV sourcing. Supplier power is elevated in EV and ADAS domains, with semiconductor lead times in 2024 reported at roughly 20–30 weeks, amplifying disruption risk.

Local Turkish supplier ecosystem

A mature tier-1/2 supplier base in Turkey, with over 1,000 automotive suppliers, delivers proximity and cost advantages that constrain supplier power. Intense local competition further moderates pricing leverage, though sustained lira volatility and double-digit inflation in 2023–24 have tightened margins and forced repricing. Ongoing localization demands continuous capability and quality upgrades to meet Ford’s global standards.

Long-term contracts and co-development

Logistics and commodity exposure

Steel, aluminum, energy and freight swings materially affect Ford Otosan’s total cost of ownership, with material costs roughly half of vehicle BOM and steel/aluminum about 20% of materials; suppliers frequently pass surcharges during volatility, squeezing margins. Ford Otosan uses hedging and design-for-cost measures to mitigate exposure but cannot fully offset acute price shocks. Port congestion and rerouted geopolitical lanes add bargaining friction and lead times.

- Material share: ~50% of BOM

- Steel/aluminium: ~20% of materials

- Freight/energy surcharges: passed through in volatility

- Hedge + design reduce but don’t eliminate shocks

Scale $145bn cuts supplier power; EV cells ~34%

Ford Otosan benefits from Ford’s $145bn global purchasing (2024) to dilute supplier power, enabling dual-sourcing and cost take-outs. Concentration in EV cells (CATL ~34% global share 2023) and semiconductors (lead times ~20–30 weeks in 2024) elevates supplier leverage for EV/ADAS modules. Local Turkish base of >1,000 suppliers and ~50% BOM material share tempers but does not eliminate pricing risk amid 2023–24 double-digit inflation.

| Metric | Value |

|---|---|

| Ford global purchasing (2024) | $145bn |

| CATL global EV cell share (2023) | ~34% |

| Semiconductor lead times (2024) | 20–30 weeks |

| Turkish auto suppliers | >1,000 |

| Materials share of BOM | ~50% |

What is included in the product

Tailored Porter's Five Forces analysis for Ford Otosan that assesses competitive rivalry, supplier and buyer power, entry barriers and substitutes to reveal strategic risks and opportunities.

A concise Ford Otosan Porter's Five Forces one-sheet that visualizes competitive pressure with an editable spider chart for instant strategic clarity. Customizable inputs and a clean layout make it slide-ready, easy to update for new data, and usable by non-finance teams.

Customers Bargaining Power

Fleet and export-driven demand

Large fleets and international distributors buy in volume and negotiate aggressively, using tender-based procurement that prioritizes total cost of ownership and uptime. Buyers leverage competing LCV models to extract price discounts and demand service contracts, uptime guarantees and penalty clauses. Service-level concessions—spare parts logistics, uptime SLAs and extended warranties—become decisive in winning large fleet tenders.

Moderate switching costs

Platform compatibility, standardized body-builder interfaces and aftersales tie-ins create lock-in for Ford Otosan buyers, limiting willingness to switch. Fleets typically rotate models every 3-5 years with limited retraining, enabling periodic churn. In tight markets lead times of up to 6 months can outweigh brand loyalty, elevating buyer power during cyclical troughs.

Dealer and distributor networks

Multi-brand dealers benchmark Ford Otosan offers and promotions against 5–10 competing brands in Turkey in 2024, raising price and incentive transparency. Inventory financing and manufacturer incentives materially influence channel behavior, with dealers prioritizing units carrying stronger floor-plan support. Transparent pricing across markets increases comparability and lets networks push for better rebates and sell-through terms to protect margins.

Evolving TCO in electrification

EV van TCO now centers on energy cost, residuals and charging uptime, with fleets targeting >95% availability. Buyers demand price protection, 8-year/160,000 km battery warranties and regular OTA software updates. Data-driven fleet management (telemetry can lift utilization 10–15%) and subsidy shifts increase buyer leverage and prompt re-pricing requests.

- Energy cost emphasis

- Battery warranty: 8y/160k km

- Charging uptime >95%

- Telemetry boosts negotiation (10–15%)

Brand, reliability, and service as mitigants

Ford Pro’s ecosystem—over 1 million connected commercial vehicles by 2024—plus telematics and a wide service footprint reduce buyer price sensitivity by shifting value to uptime and lifecycle costs. High uptime and parts availability (service-level targets above 90% in key markets) create value beyond sticker price, while stronger residuals temper discount demands. Customization and integration options embed Ford Otosan deeper into fleet operations, raising switching costs.

- Ford Pro connected vehicles: 1,000,000+ (2024)

- Service uptime/availability: >90% targets

- Residual value strength: reduces discount pressure

- Customization: increases operational stickiness

Scale and uptime beat price: 1,000,000+ connected, >95%

Large fleets and distributors exert strong price and SLA pressure via tenders, leveraging 3–5 year replacement cycles and lead times up to 6 months to negotiate discounts and uptime clauses. EV buyers focus on TCO: energy, residuals, charging uptime (>95%) and 8y/160k km battery warranties. Ford Pro scale (1,000,000+ connected vehicles in 2024) and >90% service targets reduce pure price sensitivity by shifting value to uptime.

| Metric | 2024 Value |

|---|---|

| Connected vehicles | 1,000,000+ |

| Service uptime target | >90% |

| Charging uptime | >95% |

| Battery warranty | 8y / 160,000 km |

| Fleet rotation | 3–5 yrs |

Same Document Delivered

Ford Otosan Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Ford Otosan you’ll receive—comprehensive, professionally formatted, and ready to use. It covers threat of new entrants, supplier and buyer power, substitutes, and competitive rivalry with data-driven insights. No placeholders or samples. Instant download after purchase.