Fortis (Canada) PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, social expectations, technological change, environmental mandates, and legal risks are reshaping Fortis (Canada)’s strategic landscape. Our concise PESTLE highlights near-term threats and growth levers with actionable insights for investors and strategists. Buy the full analysis to access detailed findings, data-driven scenarios, and ready-to-use recommendations.

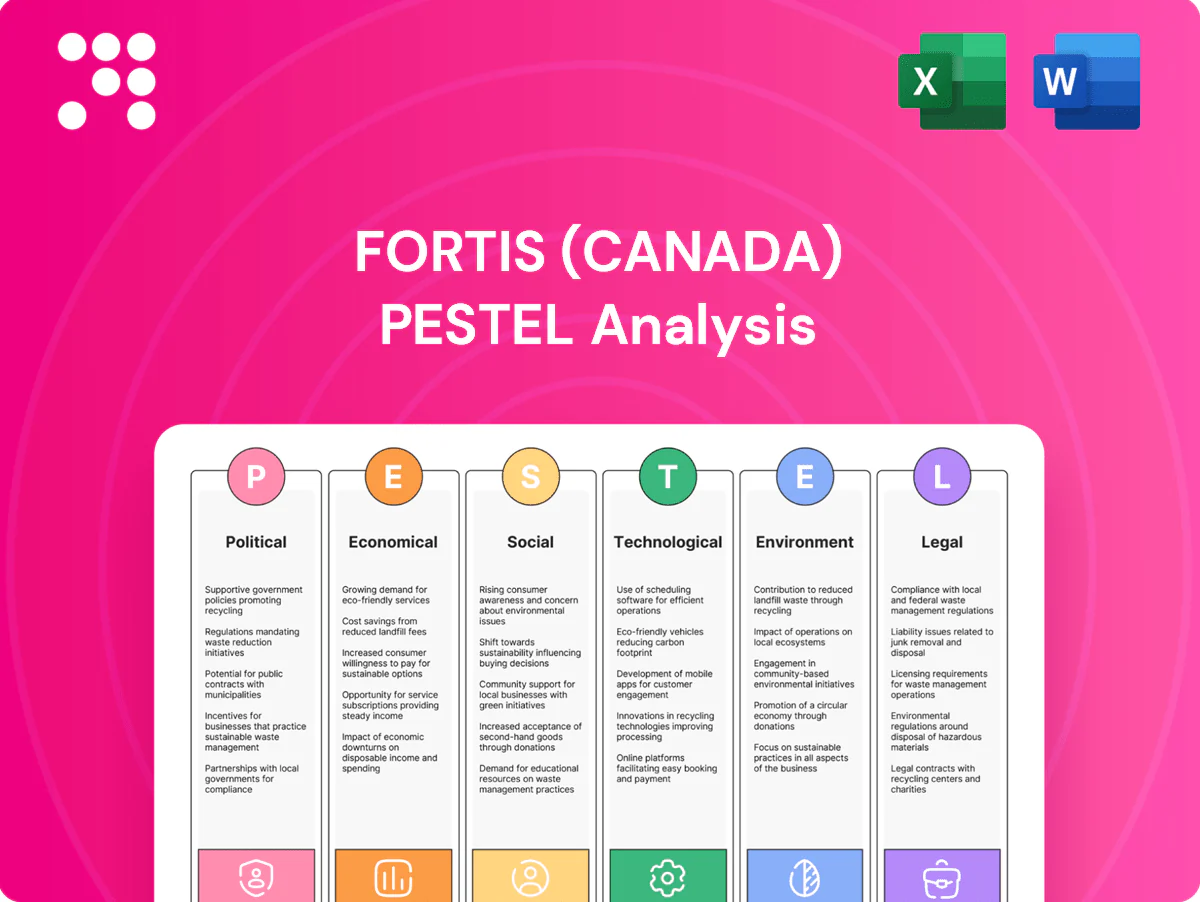

Political factors

Multi-jurisdiction regulation

Fortis operates under provincial, state, federal and Caribbean regulators with differing mandates, serving over 3 million customers and reporting total assets above CAD 40 billion in 2024.

Divergent rate-setting philosophies and policy priorities across jurisdictions can shift allowed returns and delay approvals, impacting timing of revenue recognition and capital recovery.

Coordinating multi-jurisdiction compliance raises administrative costs but diversifies political risk, while constructive regulation underpins stable, regulated earnings.

Energy transition policy

Federal and provincial decarbonization commitments—Canada net-zero by 2050 and 100% clean electricity by 2035—drive electrification and higher grid investment, benefiting utilities like Fortis, which serves roughly 3 million customers across North America. Incentives and mandates for renewables, storage and EVs can expand Fortis’s rate base and justify elevated capital deployment. Post-election policy shifts may change cost-recovery timelines and mechanisms. Fortis must align capex plans with evolving targets to protect returns.

Indigenous and community relations

Projects in Canada increasingly require engagement, benefit agreements and meaningful consent with Indigenous peoples after federal Bill C-15 (2021) to implement UNDRIP; Canada has about 1.8 million Indigenous people (2021 census) and 634 First Nations communities. Strong partnerships and co-development models can accelerate approvals and reduce opposition, while missteps risk delays, legal challenges and reputational damage.

Cross-border and Caribbean exposure

Fortis operations in the U.S. and Caribbean introduce foreign policy and geopolitical variables that affect permitting, tariffs, and cross-border contracts; the company served roughly 3.1 million customers as of 2024, concentrating regulatory exposure outside Canada.

Trade, currency volatility and disaster recovery policies in the Caribbean materially influence costs and cash flows, with emergency rebuilding and fuel-import rules driving short-term capex variations.

Federal infrastructure programs in the U.S. can unlock grants and tax incentives, while instability in some local governments raises execution and permitting risk for grid upgrades.

- Geopolitical exposure: regulatory/tariff risk

- Financial drivers: currency, disaster-rebuild capex

- Opportunities: U.S. federal infrastructure funding

- Risks: local government stability impacts execution

Infrastructure and resilience funding

Public programs such as the federal Disaster Mitigation and Adaptation Fund (DMAF, launched at C$2 billion) and provincial grid-hardening grants can de-risk Fortis Canada projects and support its ~C$2.1 billion 2024 capital program by lowering upfront utility financing needs. Eligibility and policy design determine access; cost-sharing models shift costs between taxpayers, ratepayers and regulators, affecting customer bills and allowed returns. Active, timely advocacy by Fortis influences allocation and project timelines.

- DMAF initial funding: C$2 billion

- Fortis Canada 2024 capital program: ~C$2.1 billion

- Cost-sharing alters rate impacts and regulatory outcomes

- Policy/eligibility drive project access and timing

Utility facing multi-jurisdictional regulation, decarbonization mandates and geopolitical risks

Fortis faces multi-jurisdictional regulation across provinces, U.S. states and the Caribbean that shapes allowed returns and approval timing. Federal decarbonization targets (Canada net-zero 2050; 100% clean electricity by 2035) and grants (DMAF C$2bn) drive higher grid investment and capital recovery needs. Indigenous consent rules (Bill C-15) and Caribbean geopolitical, currency and disaster risks add approval, cost and execution uncertainty.

| Metric | Value |

|---|---|

| Customers (2024) | ~3.1M |

| Total assets (2024) | ~C$40B+ |

| Fortis 2024 capex | ~C$2.1B |

| DMAF initial funding | C$2B |

| Canada targets | Net-zero 2050; 100% clean electricity 2035 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fortis (Canada) across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, investors and advisors, it highlights forward-looking risks, opportunities and strategic implications ready for business plans, pitch decks and scenario planning.

A clean, summarized Fortis (Canada) PESTLE that’s visually segmented by category for quick interpretation and easy insertion into presentations, helping teams align on external risks and market positioning during planning sessions.

Economic factors

Interest rates and WACC

Rising rates—Bank of Canada policy at 5.00% (mid-2024)—elevate Fortis’ financing costs and push up WACC, compressing allowed ROEs where regulatory returns lag market funding. Regulatory lag can narrow spreads versus cost of capital, squeezing utility economics. Fortis’ investment-grade profile aids access to long-term debt at competitive spreads, while active treasury management is critical to execute multi-year capex.

Inflation and cost pass-through

Material, labor and contractor inflation have pushed Fortis project budgets higher, with Canada’s CPI easing to about 2.9% in 2024 but input-cost volatility persisting into 2025. Recovery of escalation hinges on provincial rate mechanisms, riders and deferral trackers in Fortis’ regulated utilities. Persistent inflation raises bill-pressure and affordability concerns for customers; efficient procurement and productivity gains are key to mitigating margin and rate impacts.

Load growth and electrification

Rising EV adoption (~12% of new light-duty sales in Canada in 2024), heat pump retrofits, expanding data center load growth and industrial decarbonization projects are driving incremental demand for Fortis Canada’s networks. Regional uptake and demand-side management programs shape net load profiles and peak timing. Strong load growth supports rate base expansion—Fortis targets multi-year rate base increases—while recessions or efficiency gains can temper volumes.

Capital expenditure pipeline

Fortis Canada’s multiyear capital programs in transmission, distribution and clean energy through 2024–25 underpin rate base growth and system resilience. Strong execution discipline and tight scheduling aim to limit cost and timeline overruns. Ongoing supply‑chain constraints can push in‑service dates, so projects are paced to balance customer affordability and regulatory approval.

- Multiyear focus: transmission, distribution, clean energy (2024–25)

- Execution: scheduling discipline to limit overruns

- Risks: supply‑chain delays may shift in‑service dates

- Pacing: aligns costs with customer affordability and regulators

FX and Caribbean macro

Fortis exposure to USD and Caribbean currencies creates currency- and GDP-linked earnings sensitivity, with Caribbean revenues tied to tourism-driven domestic demand and commodity-price swings affecting collections and arrears.

Active hedging programs and regulated rate mechanisms mitigate FX-driven earnings volatility, while regional diversification across Canadian, U.S. and Caribbean utilities stabilizes consolidated cash flows.

Tourism cyclicality and commodity price movements materially influence Caribbean load growth and receivables, making localized macro monitoring and liquidity provisioning critical.

- FX exposure: USD/CAD and Caribbean currency sensitivity

- Hedging: reduces earnings volatility

- Tourism & commodities: drive demand and collections

- Diversification: stabilizes cash flows across regions

Utility facing multi-jurisdictional regulation, decarbonization mandates and geopolitical risks

Rising BoC policy at 5.00% (mid‑2024) raises Fortis’ funding costs and compresses ROE spreads versus allowed returns. CPI ~2.9% in 2024 and input inflation persist, pressuring capex and customer bills. EVs ~12% of new Canadian sales (2024) and multiyear capex expand rate base while supply‑chain and USD/Caribbean FX risks add volatility.

| Metric | Value |

|---|---|

| BoC policy rate | 5.00% |

| CPI (Canada) 2024 | 2.9% |

| EV share (new sales) 2024 | ~12% |

Full Version Awaits

Fortis (Canada) PESTLE Analysis

The Fortis (Canada) PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The content and layout shown in the preview is the exact document you’ll download after purchase—fully formatted and ready to use. No placeholders or surprises.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, social expectations, technological change, environmental mandates, and legal risks are reshaping Fortis (Canada)’s strategic landscape. Our concise PESTLE highlights near-term threats and growth levers with actionable insights for investors and strategists. Buy the full analysis to access detailed findings, data-driven scenarios, and ready-to-use recommendations.

Political factors

Multi-jurisdiction regulation

Fortis operates under provincial, state, federal and Caribbean regulators with differing mandates, serving over 3 million customers and reporting total assets above CAD 40 billion in 2024.

Divergent rate-setting philosophies and policy priorities across jurisdictions can shift allowed returns and delay approvals, impacting timing of revenue recognition and capital recovery.

Coordinating multi-jurisdiction compliance raises administrative costs but diversifies political risk, while constructive regulation underpins stable, regulated earnings.

Energy transition policy

Federal and provincial decarbonization commitments—Canada net-zero by 2050 and 100% clean electricity by 2035—drive electrification and higher grid investment, benefiting utilities like Fortis, which serves roughly 3 million customers across North America. Incentives and mandates for renewables, storage and EVs can expand Fortis’s rate base and justify elevated capital deployment. Post-election policy shifts may change cost-recovery timelines and mechanisms. Fortis must align capex plans with evolving targets to protect returns.

Indigenous and community relations

Projects in Canada increasingly require engagement, benefit agreements and meaningful consent with Indigenous peoples after federal Bill C-15 (2021) to implement UNDRIP; Canada has about 1.8 million Indigenous people (2021 census) and 634 First Nations communities. Strong partnerships and co-development models can accelerate approvals and reduce opposition, while missteps risk delays, legal challenges and reputational damage.

Cross-border and Caribbean exposure

Fortis operations in the U.S. and Caribbean introduce foreign policy and geopolitical variables that affect permitting, tariffs, and cross-border contracts; the company served roughly 3.1 million customers as of 2024, concentrating regulatory exposure outside Canada.

Trade, currency volatility and disaster recovery policies in the Caribbean materially influence costs and cash flows, with emergency rebuilding and fuel-import rules driving short-term capex variations.

Federal infrastructure programs in the U.S. can unlock grants and tax incentives, while instability in some local governments raises execution and permitting risk for grid upgrades.

- Geopolitical exposure: regulatory/tariff risk

- Financial drivers: currency, disaster-rebuild capex

- Opportunities: U.S. federal infrastructure funding

- Risks: local government stability impacts execution

Infrastructure and resilience funding

Public programs such as the federal Disaster Mitigation and Adaptation Fund (DMAF, launched at C$2 billion) and provincial grid-hardening grants can de-risk Fortis Canada projects and support its ~C$2.1 billion 2024 capital program by lowering upfront utility financing needs. Eligibility and policy design determine access; cost-sharing models shift costs between taxpayers, ratepayers and regulators, affecting customer bills and allowed returns. Active, timely advocacy by Fortis influences allocation and project timelines.

- DMAF initial funding: C$2 billion

- Fortis Canada 2024 capital program: ~C$2.1 billion

- Cost-sharing alters rate impacts and regulatory outcomes

- Policy/eligibility drive project access and timing

Utility facing multi-jurisdictional regulation, decarbonization mandates and geopolitical risks

Fortis faces multi-jurisdictional regulation across provinces, U.S. states and the Caribbean that shapes allowed returns and approval timing. Federal decarbonization targets (Canada net-zero 2050; 100% clean electricity by 2035) and grants (DMAF C$2bn) drive higher grid investment and capital recovery needs. Indigenous consent rules (Bill C-15) and Caribbean geopolitical, currency and disaster risks add approval, cost and execution uncertainty.

| Metric | Value |

|---|---|

| Customers (2024) | ~3.1M |

| Total assets (2024) | ~C$40B+ |

| Fortis 2024 capex | ~C$2.1B |

| DMAF initial funding | C$2B |

| Canada targets | Net-zero 2050; 100% clean electricity 2035 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fortis (Canada) across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, investors and advisors, it highlights forward-looking risks, opportunities and strategic implications ready for business plans, pitch decks and scenario planning.

A clean, summarized Fortis (Canada) PESTLE that’s visually segmented by category for quick interpretation and easy insertion into presentations, helping teams align on external risks and market positioning during planning sessions.

Economic factors

Interest rates and WACC

Rising rates—Bank of Canada policy at 5.00% (mid-2024)—elevate Fortis’ financing costs and push up WACC, compressing allowed ROEs where regulatory returns lag market funding. Regulatory lag can narrow spreads versus cost of capital, squeezing utility economics. Fortis’ investment-grade profile aids access to long-term debt at competitive spreads, while active treasury management is critical to execute multi-year capex.

Inflation and cost pass-through

Material, labor and contractor inflation have pushed Fortis project budgets higher, with Canada’s CPI easing to about 2.9% in 2024 but input-cost volatility persisting into 2025. Recovery of escalation hinges on provincial rate mechanisms, riders and deferral trackers in Fortis’ regulated utilities. Persistent inflation raises bill-pressure and affordability concerns for customers; efficient procurement and productivity gains are key to mitigating margin and rate impacts.

Load growth and electrification

Rising EV adoption (~12% of new light-duty sales in Canada in 2024), heat pump retrofits, expanding data center load growth and industrial decarbonization projects are driving incremental demand for Fortis Canada’s networks. Regional uptake and demand-side management programs shape net load profiles and peak timing. Strong load growth supports rate base expansion—Fortis targets multi-year rate base increases—while recessions or efficiency gains can temper volumes.

Capital expenditure pipeline

Fortis Canada’s multiyear capital programs in transmission, distribution and clean energy through 2024–25 underpin rate base growth and system resilience. Strong execution discipline and tight scheduling aim to limit cost and timeline overruns. Ongoing supply‑chain constraints can push in‑service dates, so projects are paced to balance customer affordability and regulatory approval.

- Multiyear focus: transmission, distribution, clean energy (2024–25)

- Execution: scheduling discipline to limit overruns

- Risks: supply‑chain delays may shift in‑service dates

- Pacing: aligns costs with customer affordability and regulators

FX and Caribbean macro

Fortis exposure to USD and Caribbean currencies creates currency- and GDP-linked earnings sensitivity, with Caribbean revenues tied to tourism-driven domestic demand and commodity-price swings affecting collections and arrears.

Active hedging programs and regulated rate mechanisms mitigate FX-driven earnings volatility, while regional diversification across Canadian, U.S. and Caribbean utilities stabilizes consolidated cash flows.

Tourism cyclicality and commodity price movements materially influence Caribbean load growth and receivables, making localized macro monitoring and liquidity provisioning critical.

- FX exposure: USD/CAD and Caribbean currency sensitivity

- Hedging: reduces earnings volatility

- Tourism & commodities: drive demand and collections

- Diversification: stabilizes cash flows across regions

Utility facing multi-jurisdictional regulation, decarbonization mandates and geopolitical risks

Rising BoC policy at 5.00% (mid‑2024) raises Fortis’ funding costs and compresses ROE spreads versus allowed returns. CPI ~2.9% in 2024 and input inflation persist, pressuring capex and customer bills. EVs ~12% of new Canadian sales (2024) and multiyear capex expand rate base while supply‑chain and USD/Caribbean FX risks add volatility.

| Metric | Value |

|---|---|

| BoC policy rate | 5.00% |

| CPI (Canada) 2024 | 2.9% |

| EV share (new sales) 2024 | ~12% |

Full Version Awaits

Fortis (Canada) PESTLE Analysis

The Fortis (Canada) PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The content and layout shown in the preview is the exact document you’ll download after purchase—fully formatted and ready to use. No placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic pressures, social expectations, technological change, environmental mandates, and legal risks are reshaping Fortis (Canada)’s strategic landscape. Our concise PESTLE highlights near-term threats and growth levers with actionable insights for investors and strategists. Buy the full analysis to access detailed findings, data-driven scenarios, and ready-to-use recommendations.

Political factors

Multi-jurisdiction regulation

Fortis operates under provincial, state, federal and Caribbean regulators with differing mandates, serving over 3 million customers and reporting total assets above CAD 40 billion in 2024.

Divergent rate-setting philosophies and policy priorities across jurisdictions can shift allowed returns and delay approvals, impacting timing of revenue recognition and capital recovery.

Coordinating multi-jurisdiction compliance raises administrative costs but diversifies political risk, while constructive regulation underpins stable, regulated earnings.

Energy transition policy

Federal and provincial decarbonization commitments—Canada net-zero by 2050 and 100% clean electricity by 2035—drive electrification and higher grid investment, benefiting utilities like Fortis, which serves roughly 3 million customers across North America. Incentives and mandates for renewables, storage and EVs can expand Fortis’s rate base and justify elevated capital deployment. Post-election policy shifts may change cost-recovery timelines and mechanisms. Fortis must align capex plans with evolving targets to protect returns.

Indigenous and community relations

Projects in Canada increasingly require engagement, benefit agreements and meaningful consent with Indigenous peoples after federal Bill C-15 (2021) to implement UNDRIP; Canada has about 1.8 million Indigenous people (2021 census) and 634 First Nations communities. Strong partnerships and co-development models can accelerate approvals and reduce opposition, while missteps risk delays, legal challenges and reputational damage.

Cross-border and Caribbean exposure

Fortis operations in the U.S. and Caribbean introduce foreign policy and geopolitical variables that affect permitting, tariffs, and cross-border contracts; the company served roughly 3.1 million customers as of 2024, concentrating regulatory exposure outside Canada.

Trade, currency volatility and disaster recovery policies in the Caribbean materially influence costs and cash flows, with emergency rebuilding and fuel-import rules driving short-term capex variations.

Federal infrastructure programs in the U.S. can unlock grants and tax incentives, while instability in some local governments raises execution and permitting risk for grid upgrades.

- Geopolitical exposure: regulatory/tariff risk

- Financial drivers: currency, disaster-rebuild capex

- Opportunities: U.S. federal infrastructure funding

- Risks: local government stability impacts execution

Infrastructure and resilience funding

Public programs such as the federal Disaster Mitigation and Adaptation Fund (DMAF, launched at C$2 billion) and provincial grid-hardening grants can de-risk Fortis Canada projects and support its ~C$2.1 billion 2024 capital program by lowering upfront utility financing needs. Eligibility and policy design determine access; cost-sharing models shift costs between taxpayers, ratepayers and regulators, affecting customer bills and allowed returns. Active, timely advocacy by Fortis influences allocation and project timelines.

- DMAF initial funding: C$2 billion

- Fortis Canada 2024 capital program: ~C$2.1 billion

- Cost-sharing alters rate impacts and regulatory outcomes

- Policy/eligibility drive project access and timing

Utility facing multi-jurisdictional regulation, decarbonization mandates and geopolitical risks

Fortis faces multi-jurisdictional regulation across provinces, U.S. states and the Caribbean that shapes allowed returns and approval timing. Federal decarbonization targets (Canada net-zero 2050; 100% clean electricity by 2035) and grants (DMAF C$2bn) drive higher grid investment and capital recovery needs. Indigenous consent rules (Bill C-15) and Caribbean geopolitical, currency and disaster risks add approval, cost and execution uncertainty.

| Metric | Value |

|---|---|

| Customers (2024) | ~3.1M |

| Total assets (2024) | ~C$40B+ |

| Fortis 2024 capex | ~C$2.1B |

| DMAF initial funding | C$2B |

| Canada targets | Net-zero 2050; 100% clean electricity 2035 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fortis (Canada) across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives, investors and advisors, it highlights forward-looking risks, opportunities and strategic implications ready for business plans, pitch decks and scenario planning.

A clean, summarized Fortis (Canada) PESTLE that’s visually segmented by category for quick interpretation and easy insertion into presentations, helping teams align on external risks and market positioning during planning sessions.

Economic factors

Interest rates and WACC

Rising rates—Bank of Canada policy at 5.00% (mid-2024)—elevate Fortis’ financing costs and push up WACC, compressing allowed ROEs where regulatory returns lag market funding. Regulatory lag can narrow spreads versus cost of capital, squeezing utility economics. Fortis’ investment-grade profile aids access to long-term debt at competitive spreads, while active treasury management is critical to execute multi-year capex.

Inflation and cost pass-through

Material, labor and contractor inflation have pushed Fortis project budgets higher, with Canada’s CPI easing to about 2.9% in 2024 but input-cost volatility persisting into 2025. Recovery of escalation hinges on provincial rate mechanisms, riders and deferral trackers in Fortis’ regulated utilities. Persistent inflation raises bill-pressure and affordability concerns for customers; efficient procurement and productivity gains are key to mitigating margin and rate impacts.

Load growth and electrification

Rising EV adoption (~12% of new light-duty sales in Canada in 2024), heat pump retrofits, expanding data center load growth and industrial decarbonization projects are driving incremental demand for Fortis Canada’s networks. Regional uptake and demand-side management programs shape net load profiles and peak timing. Strong load growth supports rate base expansion—Fortis targets multi-year rate base increases—while recessions or efficiency gains can temper volumes.

Capital expenditure pipeline

Fortis Canada’s multiyear capital programs in transmission, distribution and clean energy through 2024–25 underpin rate base growth and system resilience. Strong execution discipline and tight scheduling aim to limit cost and timeline overruns. Ongoing supply‑chain constraints can push in‑service dates, so projects are paced to balance customer affordability and regulatory approval.

- Multiyear focus: transmission, distribution, clean energy (2024–25)

- Execution: scheduling discipline to limit overruns

- Risks: supply‑chain delays may shift in‑service dates

- Pacing: aligns costs with customer affordability and regulators

FX and Caribbean macro

Fortis exposure to USD and Caribbean currencies creates currency- and GDP-linked earnings sensitivity, with Caribbean revenues tied to tourism-driven domestic demand and commodity-price swings affecting collections and arrears.

Active hedging programs and regulated rate mechanisms mitigate FX-driven earnings volatility, while regional diversification across Canadian, U.S. and Caribbean utilities stabilizes consolidated cash flows.

Tourism cyclicality and commodity price movements materially influence Caribbean load growth and receivables, making localized macro monitoring and liquidity provisioning critical.

- FX exposure: USD/CAD and Caribbean currency sensitivity

- Hedging: reduces earnings volatility

- Tourism & commodities: drive demand and collections

- Diversification: stabilizes cash flows across regions

Utility facing multi-jurisdictional regulation, decarbonization mandates and geopolitical risks

Rising BoC policy at 5.00% (mid‑2024) raises Fortis’ funding costs and compresses ROE spreads versus allowed returns. CPI ~2.9% in 2024 and input inflation persist, pressuring capex and customer bills. EVs ~12% of new Canadian sales (2024) and multiyear capex expand rate base while supply‑chain and USD/Caribbean FX risks add volatility.

| Metric | Value |

|---|---|

| BoC policy rate | 5.00% |

| CPI (Canada) 2024 | 2.9% |

| EV share (new sales) 2024 | ~12% |

Full Version Awaits

Fortis (Canada) PESTLE Analysis

The Fortis (Canada) PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The content and layout shown in the preview is the exact document you’ll download after purchase—fully formatted and ready to use. No placeholders or surprises.