Fortis (Canada) SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

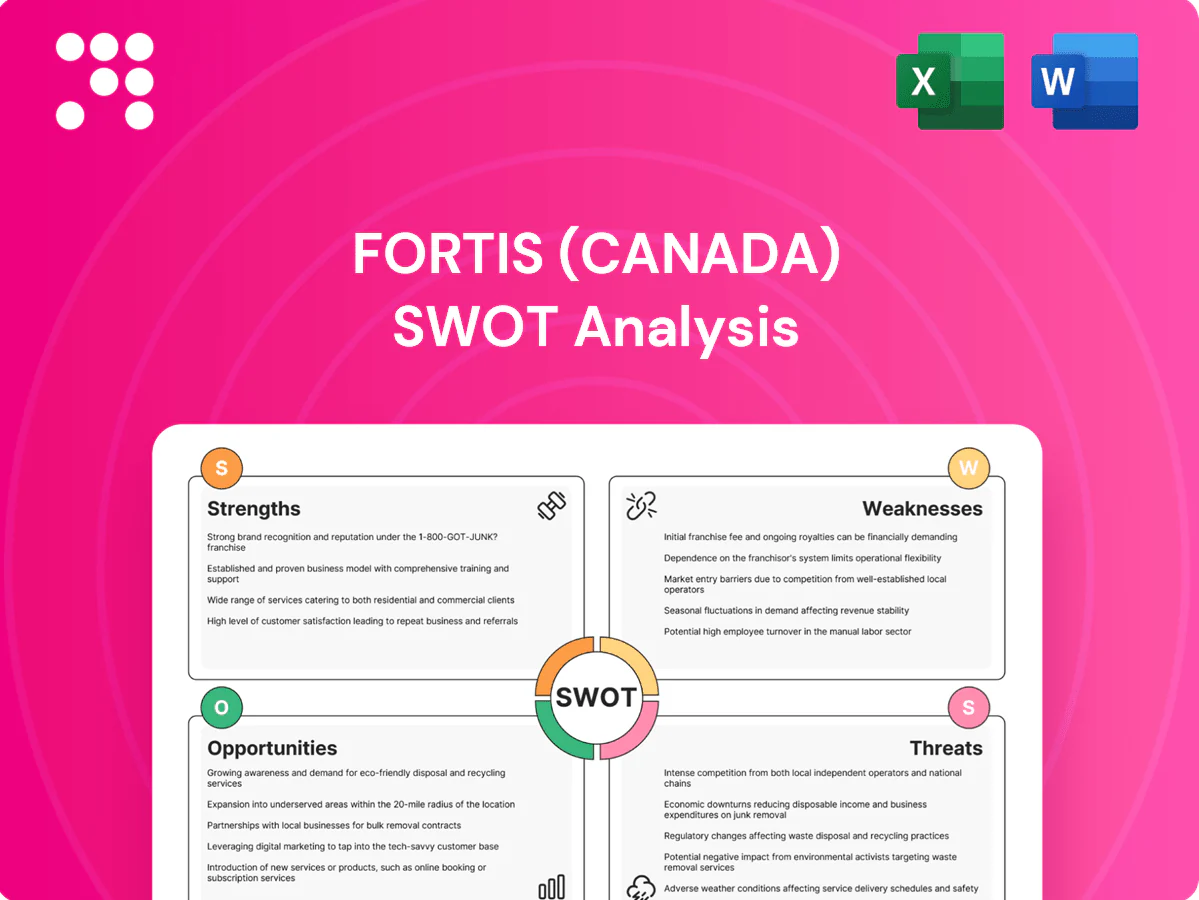

Fortis (Canada) leverages a regulated utility model and diversified North American footprint to deliver stable cash flows and predictable dividends. It faces aging infrastructure and regional concentration that can raise capex and operational risk. Growth hinges on renewable integration and grid upgrades, while regulation and extreme weather remain key threats. Discover the complete picture behind the company’s market position with our full SWOT analysis.

Strengths

Stable regulated earnings

Fortis derives over 90% of revenue from regulated utilities, delivering predictable cash flows and lower earnings volatility. Multi-year rate frameworks and allowed returns across its jurisdictions provide strong earnings visibility. This regulated stability underpins dividend continuity—49 consecutive years of increases as of 2024—and supports investment-grade credit metrics, cushioning cyclical economic swings.

Diversified geographic footprint

Fortis operates regulated electric and gas utilities across Canada, the U.S. and the Caribbean, serving over 4 million customers with assets exceeding CAD 60 billion. Geographic and regulatory diversification lowers concentration risk by spreading exposure across jurisdictions. Weather, policy and demand shocks are partially offset across regions, enhancing resilience and capital allocation flexibility.

Large, long-lived asset base

Fortis’s large, long‑lived transmission and distribution asset base creates high entry barriers and locks in capital as networks (typical lives 30–70 years) require ongoing replacement; Fortis Inc. reported roughly CAD 66.7 billion in total assets and serves about 3.6 million customer connections (Dec 31, 2024), a scale that delivers operating efficiencies, procurement leverage and stronger positioning in regulatory rate cases.

Visible capex growth pipeline

Planned infrastructure investments drive regulated rate base expansion, with Fortis outlining a CAD 13.1 billion capital program for 2024–2028 that prioritizes grid modernization, resiliency and interconnections. The multi-year pipeline supports visible line-of-sight to earnings CAGR through regulated returns and aligns directly with electrification and energy-transition needs.

- Rate base expansion: CAD 13.1B (2024–2028)

- Focus: grid modernization, resiliency, interconnections

- Outcome: visible earnings CAGR via regulated returns

- Alignment: supports electrification and energy transition

Strong dividend track record

Fortis maintains a strong dividend track record supported by stable regulated cash flows and a prudent payout policy, delivering a current dividend yield around 3.8% (2024) that appeals to income-focused investors. An investment-grade balance sheet (S&P/DBRS BBB+/BBB, 2024) underpins sustainability and helps lower the companys equity cost of capital, enhancing investor confidence and valuation stability.

- Dividend yield ~3.8% (2024)

- Investment-grade ratings: S&P/DBRS BBB+/BBB (2024)

- Prudent payout policy reduces capital cost

- Attracts income-oriented investors

Regulated utility: >90% regulated rev, ~3.8% yield

Fortis earns over 90% of revenue from regulated utilities, giving predictable cash flows and low volatility. Assets ~CAD 66.7B and ~3.6M customer connections (Dec 31, 2024) create scale and high entry barriers. CAD 13.1B 2024–2028 capex expands rate base; 49 years of dividend increases (2024) and ~3.8% yield support investor appeal.

| Metric | Value |

|---|---|

| Regulated Rev | >90% |

| Total Assets | CAD 66.7B |

| Customers | ~3.6M |

| Capex (2024–28) | CAD 13.1B |

| Dividend streak | 49 yrs (2024) |

| Yield | ~3.8% (2024) |

| Ratings | S&P/DBRS BBB+/BBB (2024) |

What is included in the product

Provides a concise SWOT overview of Fortis (Canada), highlighting strong regulated utility cash flows, diversified infrastructure and predictable dividends; weaknesses including capital intensity and regulatory dependence; opportunities in electrification, renewables and grid modernization; and threats from regulatory shifts, rising interest rates and climate-related risks.

Provides a concise Fortis (Canada) SWOT matrix for fast, visual strategy alignment across regulated utilities, highlighting strengths, risks, opportunities and weaknesses for quick stakeholder decisions.

Weaknesses

Interest rate sensitivity

Fortis operates a capital-intensive, acquisition-driven model that depends on continual financing; rising interest rates have increased its debt service and pressured valuations, while regulatory allowed ROEs often lag market rate moves, narrowing spreads and compressing free cash flow available after dividends.

Regulatory dependence

Earnings hinge on rate case outcomes and allowed returns, which in North American utilities typically run about 7–10% and directly affect Fortis cash flow; adverse rulings or multi-year delays (often 12–36 months) can defer cost recovery and compress margins. Jurisdictional variability across provinces, U.S. states and Caribbean territories adds legal complexity, while mounting compliance requirements elevate operating overhead and capital costs.

Limited unregulated upside

Fortis’s business remains overwhelmingly regulated, with over 90% of earnings tied to rate-regulated assets, which caps upside from market-driven returns. Merchant generation and ancillary services contribute only modestly to consolidated EBITDA, limiting benefit from commodity price rallies. This structure constrains upside in strong market conditions compared with peers with larger merchant exposure. Growth is paced by approved ratebase capex under multi-year plans (~CAD 17 billion range).

Exposure to extreme weather

Storms, wildfires and hurricanes across Fortis service territories drive frequent outages that elevate O&M and restoration costs, straining operational budgets. Regulatory cost recovery is possible but timing gaps between incurred expenses and reimbursements compress cash flow and increase short-term liquidity risk. Asset hardening and resilience programs demand incremental capital expenditure, pressuring near-term investment plans and rate cases.

- Storms/wildfires/hurricanes: widespread outage risk

- Higher O&M/restoration costs; partial regulatory recovery

- Timing gaps hurt cash flow and liquidity

- Incremental capex needed for asset hardening

Foreign exchange and policy mix

U.S. and Caribbean earnings expose Fortis to foreign-exchange translation risk, amplifying reported volatility when CAD strengthens or weakens; cross-border tax and regulatory shifts in jurisdictions like the Caribbean can materially alter effective returns. Hedging programs reduce but do not eliminate currency-driven earnings swings, and multi-jurisdictional corporate structures add administrative and compliance drag.

- FX translation risk from U.S. and Caribbean operations

- Exposure to cross-border tax and regulatory changes

- Hedging limits but does not remove currency volatility

- Complex structures raise administrative costs and compliance burden

Regulated earnings >90%; CAD 17B capex; ROE 7-10%; rate-case lag 12-36m

Highly regulated earnings (>90%); acquisition/capex-driven model (~CAD 17B multiyear capex); allowed ROEs ~7–10% vs rising market rates; rate-case delays 12–36 months; weather-driven O&M spikes and restoration costs; FX translation from U.S./Caribbean operations.

| Metric | Value |

|---|---|

| Regulated EBITDA share | >90% |

| Multiyear capex | ~CAD 17B |

| Allowed ROE range | 7–10% |

What You See Is What You Get

Fortis (Canada) SWOT Analysis

This is the actual Fortis (Canada) SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; purchase unlocks the entire in-depth, editable version. You’re viewing the real analysis file ready for immediate download after checkout.

Dive Deeper Into the Company’s Strategic Blueprint

Fortis (Canada) leverages a regulated utility model and diversified North American footprint to deliver stable cash flows and predictable dividends. It faces aging infrastructure and regional concentration that can raise capex and operational risk. Growth hinges on renewable integration and grid upgrades, while regulation and extreme weather remain key threats. Discover the complete picture behind the company’s market position with our full SWOT analysis.

Strengths

Stable regulated earnings

Fortis derives over 90% of revenue from regulated utilities, delivering predictable cash flows and lower earnings volatility. Multi-year rate frameworks and allowed returns across its jurisdictions provide strong earnings visibility. This regulated stability underpins dividend continuity—49 consecutive years of increases as of 2024—and supports investment-grade credit metrics, cushioning cyclical economic swings.

Diversified geographic footprint

Fortis operates regulated electric and gas utilities across Canada, the U.S. and the Caribbean, serving over 4 million customers with assets exceeding CAD 60 billion. Geographic and regulatory diversification lowers concentration risk by spreading exposure across jurisdictions. Weather, policy and demand shocks are partially offset across regions, enhancing resilience and capital allocation flexibility.

Large, long-lived asset base

Fortis’s large, long‑lived transmission and distribution asset base creates high entry barriers and locks in capital as networks (typical lives 30–70 years) require ongoing replacement; Fortis Inc. reported roughly CAD 66.7 billion in total assets and serves about 3.6 million customer connections (Dec 31, 2024), a scale that delivers operating efficiencies, procurement leverage and stronger positioning in regulatory rate cases.

Visible capex growth pipeline

Planned infrastructure investments drive regulated rate base expansion, with Fortis outlining a CAD 13.1 billion capital program for 2024–2028 that prioritizes grid modernization, resiliency and interconnections. The multi-year pipeline supports visible line-of-sight to earnings CAGR through regulated returns and aligns directly with electrification and energy-transition needs.

- Rate base expansion: CAD 13.1B (2024–2028)

- Focus: grid modernization, resiliency, interconnections

- Outcome: visible earnings CAGR via regulated returns

- Alignment: supports electrification and energy transition

Strong dividend track record

Fortis maintains a strong dividend track record supported by stable regulated cash flows and a prudent payout policy, delivering a current dividend yield around 3.8% (2024) that appeals to income-focused investors. An investment-grade balance sheet (S&P/DBRS BBB+/BBB, 2024) underpins sustainability and helps lower the companys equity cost of capital, enhancing investor confidence and valuation stability.

- Dividend yield ~3.8% (2024)

- Investment-grade ratings: S&P/DBRS BBB+/BBB (2024)

- Prudent payout policy reduces capital cost

- Attracts income-oriented investors

Regulated utility: >90% regulated rev, ~3.8% yield

Fortis earns over 90% of revenue from regulated utilities, giving predictable cash flows and low volatility. Assets ~CAD 66.7B and ~3.6M customer connections (Dec 31, 2024) create scale and high entry barriers. CAD 13.1B 2024–2028 capex expands rate base; 49 years of dividend increases (2024) and ~3.8% yield support investor appeal.

| Metric | Value |

|---|---|

| Regulated Rev | >90% |

| Total Assets | CAD 66.7B |

| Customers | ~3.6M |

| Capex (2024–28) | CAD 13.1B |

| Dividend streak | 49 yrs (2024) |

| Yield | ~3.8% (2024) |

| Ratings | S&P/DBRS BBB+/BBB (2024) |

What is included in the product

Provides a concise SWOT overview of Fortis (Canada), highlighting strong regulated utility cash flows, diversified infrastructure and predictable dividends; weaknesses including capital intensity and regulatory dependence; opportunities in electrification, renewables and grid modernization; and threats from regulatory shifts, rising interest rates and climate-related risks.

Provides a concise Fortis (Canada) SWOT matrix for fast, visual strategy alignment across regulated utilities, highlighting strengths, risks, opportunities and weaknesses for quick stakeholder decisions.

Weaknesses

Interest rate sensitivity

Fortis operates a capital-intensive, acquisition-driven model that depends on continual financing; rising interest rates have increased its debt service and pressured valuations, while regulatory allowed ROEs often lag market rate moves, narrowing spreads and compressing free cash flow available after dividends.

Regulatory dependence

Earnings hinge on rate case outcomes and allowed returns, which in North American utilities typically run about 7–10% and directly affect Fortis cash flow; adverse rulings or multi-year delays (often 12–36 months) can defer cost recovery and compress margins. Jurisdictional variability across provinces, U.S. states and Caribbean territories adds legal complexity, while mounting compliance requirements elevate operating overhead and capital costs.

Limited unregulated upside

Fortis’s business remains overwhelmingly regulated, with over 90% of earnings tied to rate-regulated assets, which caps upside from market-driven returns. Merchant generation and ancillary services contribute only modestly to consolidated EBITDA, limiting benefit from commodity price rallies. This structure constrains upside in strong market conditions compared with peers with larger merchant exposure. Growth is paced by approved ratebase capex under multi-year plans (~CAD 17 billion range).

Exposure to extreme weather

Storms, wildfires and hurricanes across Fortis service territories drive frequent outages that elevate O&M and restoration costs, straining operational budgets. Regulatory cost recovery is possible but timing gaps between incurred expenses and reimbursements compress cash flow and increase short-term liquidity risk. Asset hardening and resilience programs demand incremental capital expenditure, pressuring near-term investment plans and rate cases.

- Storms/wildfires/hurricanes: widespread outage risk

- Higher O&M/restoration costs; partial regulatory recovery

- Timing gaps hurt cash flow and liquidity

- Incremental capex needed for asset hardening

Foreign exchange and policy mix

U.S. and Caribbean earnings expose Fortis to foreign-exchange translation risk, amplifying reported volatility when CAD strengthens or weakens; cross-border tax and regulatory shifts in jurisdictions like the Caribbean can materially alter effective returns. Hedging programs reduce but do not eliminate currency-driven earnings swings, and multi-jurisdictional corporate structures add administrative and compliance drag.

- FX translation risk from U.S. and Caribbean operations

- Exposure to cross-border tax and regulatory changes

- Hedging limits but does not remove currency volatility

- Complex structures raise administrative costs and compliance burden

Regulated earnings >90%; CAD 17B capex; ROE 7-10%; rate-case lag 12-36m

Highly regulated earnings (>90%); acquisition/capex-driven model (~CAD 17B multiyear capex); allowed ROEs ~7–10% vs rising market rates; rate-case delays 12–36 months; weather-driven O&M spikes and restoration costs; FX translation from U.S./Caribbean operations.

| Metric | Value |

|---|---|

| Regulated EBITDA share | >90% |

| Multiyear capex | ~CAD 17B |

| Allowed ROE range | 7–10% |

What You See Is What You Get

Fortis (Canada) SWOT Analysis

This is the actual Fortis (Canada) SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; purchase unlocks the entire in-depth, editable version. You’re viewing the real analysis file ready for immediate download after checkout.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Fortis (Canada) leverages a regulated utility model and diversified North American footprint to deliver stable cash flows and predictable dividends. It faces aging infrastructure and regional concentration that can raise capex and operational risk. Growth hinges on renewable integration and grid upgrades, while regulation and extreme weather remain key threats. Discover the complete picture behind the company’s market position with our full SWOT analysis.

Strengths

Stable regulated earnings

Fortis derives over 90% of revenue from regulated utilities, delivering predictable cash flows and lower earnings volatility. Multi-year rate frameworks and allowed returns across its jurisdictions provide strong earnings visibility. This regulated stability underpins dividend continuity—49 consecutive years of increases as of 2024—and supports investment-grade credit metrics, cushioning cyclical economic swings.

Diversified geographic footprint

Fortis operates regulated electric and gas utilities across Canada, the U.S. and the Caribbean, serving over 4 million customers with assets exceeding CAD 60 billion. Geographic and regulatory diversification lowers concentration risk by spreading exposure across jurisdictions. Weather, policy and demand shocks are partially offset across regions, enhancing resilience and capital allocation flexibility.

Large, long-lived asset base

Fortis’s large, long‑lived transmission and distribution asset base creates high entry barriers and locks in capital as networks (typical lives 30–70 years) require ongoing replacement; Fortis Inc. reported roughly CAD 66.7 billion in total assets and serves about 3.6 million customer connections (Dec 31, 2024), a scale that delivers operating efficiencies, procurement leverage and stronger positioning in regulatory rate cases.

Visible capex growth pipeline

Planned infrastructure investments drive regulated rate base expansion, with Fortis outlining a CAD 13.1 billion capital program for 2024–2028 that prioritizes grid modernization, resiliency and interconnections. The multi-year pipeline supports visible line-of-sight to earnings CAGR through regulated returns and aligns directly with electrification and energy-transition needs.

- Rate base expansion: CAD 13.1B (2024–2028)

- Focus: grid modernization, resiliency, interconnections

- Outcome: visible earnings CAGR via regulated returns

- Alignment: supports electrification and energy transition

Strong dividend track record

Fortis maintains a strong dividend track record supported by stable regulated cash flows and a prudent payout policy, delivering a current dividend yield around 3.8% (2024) that appeals to income-focused investors. An investment-grade balance sheet (S&P/DBRS BBB+/BBB, 2024) underpins sustainability and helps lower the companys equity cost of capital, enhancing investor confidence and valuation stability.

- Dividend yield ~3.8% (2024)

- Investment-grade ratings: S&P/DBRS BBB+/BBB (2024)

- Prudent payout policy reduces capital cost

- Attracts income-oriented investors

Regulated utility: >90% regulated rev, ~3.8% yield

Fortis earns over 90% of revenue from regulated utilities, giving predictable cash flows and low volatility. Assets ~CAD 66.7B and ~3.6M customer connections (Dec 31, 2024) create scale and high entry barriers. CAD 13.1B 2024–2028 capex expands rate base; 49 years of dividend increases (2024) and ~3.8% yield support investor appeal.

| Metric | Value |

|---|---|

| Regulated Rev | >90% |

| Total Assets | CAD 66.7B |

| Customers | ~3.6M |

| Capex (2024–28) | CAD 13.1B |

| Dividend streak | 49 yrs (2024) |

| Yield | ~3.8% (2024) |

| Ratings | S&P/DBRS BBB+/BBB (2024) |

What is included in the product

Provides a concise SWOT overview of Fortis (Canada), highlighting strong regulated utility cash flows, diversified infrastructure and predictable dividends; weaknesses including capital intensity and regulatory dependence; opportunities in electrification, renewables and grid modernization; and threats from regulatory shifts, rising interest rates and climate-related risks.

Provides a concise Fortis (Canada) SWOT matrix for fast, visual strategy alignment across regulated utilities, highlighting strengths, risks, opportunities and weaknesses for quick stakeholder decisions.

Weaknesses

Interest rate sensitivity

Fortis operates a capital-intensive, acquisition-driven model that depends on continual financing; rising interest rates have increased its debt service and pressured valuations, while regulatory allowed ROEs often lag market rate moves, narrowing spreads and compressing free cash flow available after dividends.

Regulatory dependence

Earnings hinge on rate case outcomes and allowed returns, which in North American utilities typically run about 7–10% and directly affect Fortis cash flow; adverse rulings or multi-year delays (often 12–36 months) can defer cost recovery and compress margins. Jurisdictional variability across provinces, U.S. states and Caribbean territories adds legal complexity, while mounting compliance requirements elevate operating overhead and capital costs.

Limited unregulated upside

Fortis’s business remains overwhelmingly regulated, with over 90% of earnings tied to rate-regulated assets, which caps upside from market-driven returns. Merchant generation and ancillary services contribute only modestly to consolidated EBITDA, limiting benefit from commodity price rallies. This structure constrains upside in strong market conditions compared with peers with larger merchant exposure. Growth is paced by approved ratebase capex under multi-year plans (~CAD 17 billion range).

Exposure to extreme weather

Storms, wildfires and hurricanes across Fortis service territories drive frequent outages that elevate O&M and restoration costs, straining operational budgets. Regulatory cost recovery is possible but timing gaps between incurred expenses and reimbursements compress cash flow and increase short-term liquidity risk. Asset hardening and resilience programs demand incremental capital expenditure, pressuring near-term investment plans and rate cases.

- Storms/wildfires/hurricanes: widespread outage risk

- Higher O&M/restoration costs; partial regulatory recovery

- Timing gaps hurt cash flow and liquidity

- Incremental capex needed for asset hardening

Foreign exchange and policy mix

U.S. and Caribbean earnings expose Fortis to foreign-exchange translation risk, amplifying reported volatility when CAD strengthens or weakens; cross-border tax and regulatory shifts in jurisdictions like the Caribbean can materially alter effective returns. Hedging programs reduce but do not eliminate currency-driven earnings swings, and multi-jurisdictional corporate structures add administrative and compliance drag.

- FX translation risk from U.S. and Caribbean operations

- Exposure to cross-border tax and regulatory changes

- Hedging limits but does not remove currency volatility

- Complex structures raise administrative costs and compliance burden

Regulated earnings >90%; CAD 17B capex; ROE 7-10%; rate-case lag 12-36m

Highly regulated earnings (>90%); acquisition/capex-driven model (~CAD 17B multiyear capex); allowed ROEs ~7–10% vs rising market rates; rate-case delays 12–36 months; weather-driven O&M spikes and restoration costs; FX translation from U.S./Caribbean operations.

| Metric | Value |

|---|---|

| Regulated EBITDA share | >90% |

| Multiyear capex | ~CAD 17B |

| Allowed ROE range | 7–10% |

What You See Is What You Get

Fortis (Canada) SWOT Analysis

This is the actual Fortis (Canada) SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; purchase unlocks the entire in-depth, editable version. You’re viewing the real analysis file ready for immediate download after checkout.