Fortnox Porter's Five Forces Analysis

Don't Miss the Bigger Picture

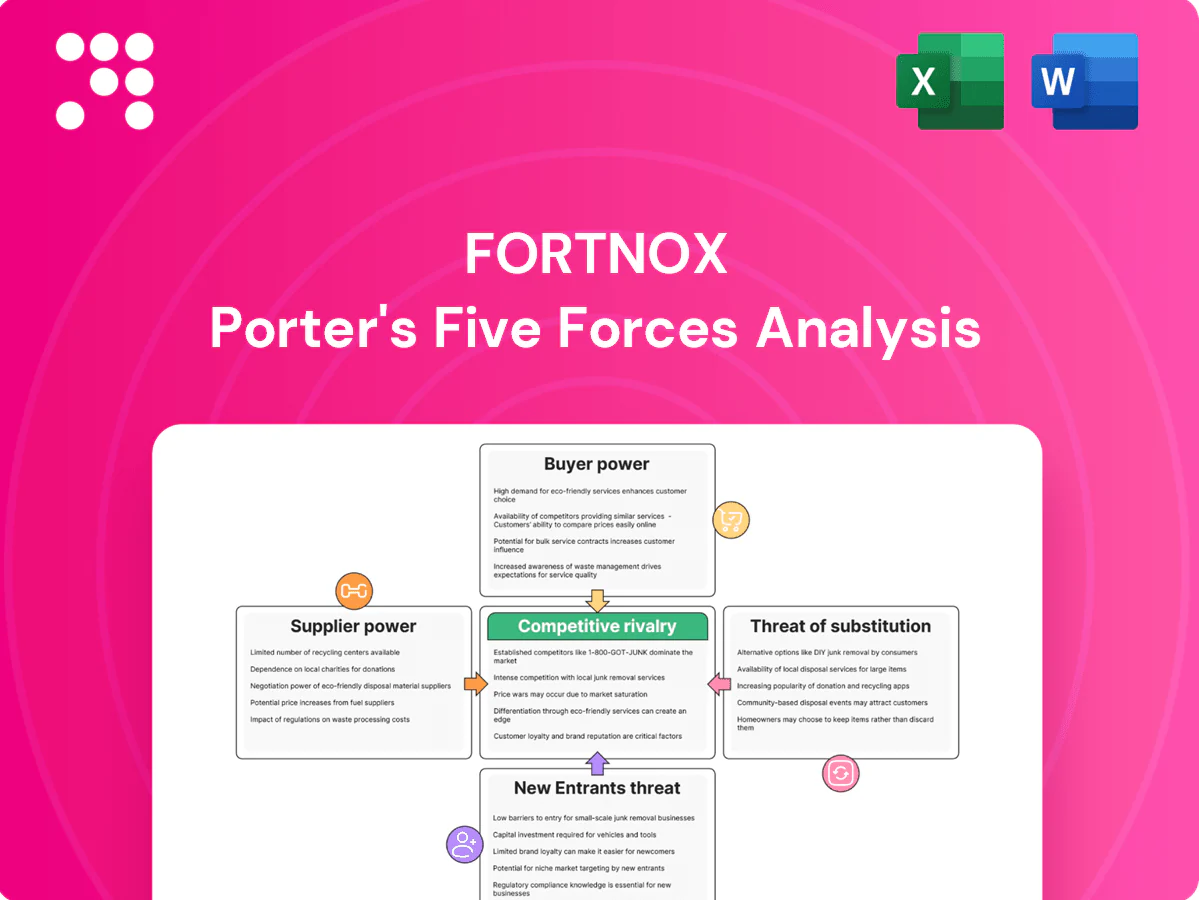

Fortnox's Porter's Five Forces snapshot highlights moderate supplier power, high buyer expectations, intense rivalry among Nordic SaaS firms, low threat of substitutes, and rising entrant pressure from vertical fintechs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fortnox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud infrastructure

Fortnox depends on hyperscale cloud providers for compute, storage and uptime SLAs, exposing it to vendor concentration risks given AWS (32%), Azure (23%) and Google Cloud (11%) together held ~66% of global cloud market in 2024. Concentration creates switching frictions and price exposure; multi-cloud deployments and reserved instances lower leverage but cannot eliminate outage or price‑hike contagion. Negotiating volume discounts and designing for architectural portability materially reduces supplier power.

Banking and payments integrations

Fortnox’s core value hinges on secure, compliant bank feeds and payment gateways; in 2024 major EU banks and PSPs advertise API access with SLAs commonly at or near 99.9%, while banks control pricing, access terms and maintenance windows that constrain feature delivery.

PSD2/Open Banking improved baseline access—major banks have APIs by 2024—but practical quality and third-party success rates vary widely across institutions, impacting reliability.

Diversifying direct integrations and using aggregation partners (TTPs) materially reduces single-supplier risk and preserves Fortnox’s roadmap flexibility.

Regulatory and tax content providers

Accurate, timely tax tables, e-invoicing formats and compliance schemas (eg EN 16931, adopted 2017) are essential inputs suppliers provide and governments/standards bodies indirectly supply. EU public procurement has required e-invoicing since 2019, forcing Fortnox to embed schemas on fixed timelines. Implementation timelines and poor documentation raise developer costs; strong compliance teams and automated update pipelines limit disruption.

Third‑party app ecosystem partners

Third‑party app partners extend Fortnox value via add‑ons for vertical workflows, payroll and CRM adjacencies; popular niche apps can leverage co‑marketing and revenue shares to negotiate favorable splits. In 2024 Fortnox’s platform reach — serving hundreds of thousands of Swedish SMBs — provides distribution that balances supplier leverage. Clear APIs, certification and tiered marketplaces keep commercial terms favorable.

- Vertical add‑ons boost stickiness

- Niche apps gain co‑marketing leverage

- Platform scale (2024) offsets supplier power

- APIs & certification standardize terms

Skilled software talent

Engineering, security and product specialists are scarce and exert strong bargaining power as talent markets function like critical input suppliers, driving wage pressure and risk to product roadmaps. Remote hiring expands candidate pools but intensifies global competition and retention challenges. Fortnox must invest in culture, modern tooling and clear career paths to retain key skills and protect delivery.

- Talent scarcity — high bargaining power

- Remote hiring — wider pool, more competition

- Wage inflation risk — impacts margins

- Retention levers — culture, tooling, career paths

SMB platform exposed to cloud concentration: AWS 32%, Azure 23%, GCP 11%

Fortnox faces supplier concentration in cloud providers (AWS 32%, Azure 23%, GCP 11% global share in 2024), raising switching and price risks. Banks/PSPs control payment APIs despite PSD2; SLAs commonly ~99.9% in 2024. Diversification (TTPs, multi‑cloud, vertical apps) and platform scale (hundreds of thousands Swedish SMBs 2024) reduce supplier power; talent scarcity increases wage pressure.

| Metric | 2024 |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Bank API SLA | ~99.9% |

| E‑invoicing mandate | EU since 2019 |

| Customer reach | Hundreds of thousands SMBs |

What is included in the product

Tailored exclusively for Fortnox, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to its cloud accounting and SMB software niche. It identifies disruptive substitutes and emerging threats while evaluating dynamics that protect Fortnox’s incumbency and affect pricing and profitability.

A clear, one-sheet summary of Fortnox's Five Forces—instantly reveals competitive pain points and strategic levers for quick decision-making, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Price‑sensitive SME customer base

Price‑sensitive SME customer base—with SMEs accounting for 99% of EU firms (Eurostat 2023) —means monthly SaaS fees are scrutinized; Fortnoxs transparent pricing and modular add‑ons make churn tangible if perceived value falls. Limited seat counts constrain volume discounts, while proven automation ROI (time savings, fewer errors) weakens buyer leverage.

Switching costs via data and workflows

Data migration of historical ledgers and bespoke accountant workflows creates practical lock-in for Fortnox users, with over 400,000 Swedish SMEs on the platform in 2024 making full migrations costly and time-consuming. API exports and standard formats reduce barriers but still require days to weeks of reconfiguration and reconciliation. Embedded payments and bank rule automation further intensify stickiness, moderating buyer power despite many alternatives.

Accountant and advisor influence

Bookkeepers and accounting bureaus heavily shape platform selection for Fortnox; as of 2024 Fortnox reports serving over 500,000 company subscriptions, so bureau recommendations can aggregate substantial demand and secure volume-based terms. Targeted training and partner programs convert these influencers into advocates and can raise switching costs. Losing a few key bureaus could rapidly amplify buyer power and trigger churn.

Multi‑homing across point tools

- multi‑homing: ~6 SaaS apps (2024)

- pressure: higher price/feature comparisons

- defenses: native integrations, bundles

- retention: unified support, SSO

Demand for reliability and compliance

Customers face real penalties from financial errors and downtime; GDPR fines can reach €20 million or 4% of global turnover. High expectations for uptime (commonly 99.9%+), strict support SLAs and fast compliance responsiveness boost buyer leverage. Clear incident communication and audit readiness (eg ISO/IEC 27001) reduce risk, while superior trust allows Fortnox to justify premium pricing and curb buyer power.

- Uptime: 99.9%+

- Compliance: GDPR fines €20M/4% turnover

- Standards: ISO/IEC 27001 readiness

- Benefit: Trust → premium pricing

SME multihoming raises price pressure Swedish accounting locks in 400,000+

SME price sensitivity and multi‑homing (~6 SaaS apps in 2024) increase comparison pressure, but Fortnox’s modular pricing, integrations and automation (ROI) reduce buyer leverage. Data migration and embedded banking create lock‑in—>400,000+ Swedish SMEs, >500,000 subscriptions (2024). Compliance (GDPR €20M/4%) and 99.9%+ uptime support premium pricing.

| Metric | Value (2024) |

|---|---|

| Swedish customers | 400,000+ |

| Subscriptions | 500,000+ |

| Apps per SME | ~6 |

| GDPR fine | €20M/4% |

| Uptime | 99.9%+ |

Full Version Awaits

Fortnox Porter's Five Forces Analysis

This preview shows the exact Fortnox Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use upon payment. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and clear strategic implications for decision makers.

Don't Miss the Bigger Picture

Fortnox's Porter's Five Forces snapshot highlights moderate supplier power, high buyer expectations, intense rivalry among Nordic SaaS firms, low threat of substitutes, and rising entrant pressure from vertical fintechs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fortnox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud infrastructure

Fortnox depends on hyperscale cloud providers for compute, storage and uptime SLAs, exposing it to vendor concentration risks given AWS (32%), Azure (23%) and Google Cloud (11%) together held ~66% of global cloud market in 2024. Concentration creates switching frictions and price exposure; multi-cloud deployments and reserved instances lower leverage but cannot eliminate outage or price‑hike contagion. Negotiating volume discounts and designing for architectural portability materially reduces supplier power.

Banking and payments integrations

Fortnox’s core value hinges on secure, compliant bank feeds and payment gateways; in 2024 major EU banks and PSPs advertise API access with SLAs commonly at or near 99.9%, while banks control pricing, access terms and maintenance windows that constrain feature delivery.

PSD2/Open Banking improved baseline access—major banks have APIs by 2024—but practical quality and third-party success rates vary widely across institutions, impacting reliability.

Diversifying direct integrations and using aggregation partners (TTPs) materially reduces single-supplier risk and preserves Fortnox’s roadmap flexibility.

Regulatory and tax content providers

Accurate, timely tax tables, e-invoicing formats and compliance schemas (eg EN 16931, adopted 2017) are essential inputs suppliers provide and governments/standards bodies indirectly supply. EU public procurement has required e-invoicing since 2019, forcing Fortnox to embed schemas on fixed timelines. Implementation timelines and poor documentation raise developer costs; strong compliance teams and automated update pipelines limit disruption.

Third‑party app ecosystem partners

Third‑party app partners extend Fortnox value via add‑ons for vertical workflows, payroll and CRM adjacencies; popular niche apps can leverage co‑marketing and revenue shares to negotiate favorable splits. In 2024 Fortnox’s platform reach — serving hundreds of thousands of Swedish SMBs — provides distribution that balances supplier leverage. Clear APIs, certification and tiered marketplaces keep commercial terms favorable.

- Vertical add‑ons boost stickiness

- Niche apps gain co‑marketing leverage

- Platform scale (2024) offsets supplier power

- APIs & certification standardize terms

Skilled software talent

Engineering, security and product specialists are scarce and exert strong bargaining power as talent markets function like critical input suppliers, driving wage pressure and risk to product roadmaps. Remote hiring expands candidate pools but intensifies global competition and retention challenges. Fortnox must invest in culture, modern tooling and clear career paths to retain key skills and protect delivery.

- Talent scarcity — high bargaining power

- Remote hiring — wider pool, more competition

- Wage inflation risk — impacts margins

- Retention levers — culture, tooling, career paths

SMB platform exposed to cloud concentration: AWS 32%, Azure 23%, GCP 11%

Fortnox faces supplier concentration in cloud providers (AWS 32%, Azure 23%, GCP 11% global share in 2024), raising switching and price risks. Banks/PSPs control payment APIs despite PSD2; SLAs commonly ~99.9% in 2024. Diversification (TTPs, multi‑cloud, vertical apps) and platform scale (hundreds of thousands Swedish SMBs 2024) reduce supplier power; talent scarcity increases wage pressure.

| Metric | 2024 |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Bank API SLA | ~99.9% |

| E‑invoicing mandate | EU since 2019 |

| Customer reach | Hundreds of thousands SMBs |

What is included in the product

Tailored exclusively for Fortnox, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to its cloud accounting and SMB software niche. It identifies disruptive substitutes and emerging threats while evaluating dynamics that protect Fortnox’s incumbency and affect pricing and profitability.

A clear, one-sheet summary of Fortnox's Five Forces—instantly reveals competitive pain points and strategic levers for quick decision-making, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Price‑sensitive SME customer base

Price‑sensitive SME customer base—with SMEs accounting for 99% of EU firms (Eurostat 2023) —means monthly SaaS fees are scrutinized; Fortnoxs transparent pricing and modular add‑ons make churn tangible if perceived value falls. Limited seat counts constrain volume discounts, while proven automation ROI (time savings, fewer errors) weakens buyer leverage.

Switching costs via data and workflows

Data migration of historical ledgers and bespoke accountant workflows creates practical lock-in for Fortnox users, with over 400,000 Swedish SMEs on the platform in 2024 making full migrations costly and time-consuming. API exports and standard formats reduce barriers but still require days to weeks of reconfiguration and reconciliation. Embedded payments and bank rule automation further intensify stickiness, moderating buyer power despite many alternatives.

Accountant and advisor influence

Bookkeepers and accounting bureaus heavily shape platform selection for Fortnox; as of 2024 Fortnox reports serving over 500,000 company subscriptions, so bureau recommendations can aggregate substantial demand and secure volume-based terms. Targeted training and partner programs convert these influencers into advocates and can raise switching costs. Losing a few key bureaus could rapidly amplify buyer power and trigger churn.

Multi‑homing across point tools

- multi‑homing: ~6 SaaS apps (2024)

- pressure: higher price/feature comparisons

- defenses: native integrations, bundles

- retention: unified support, SSO

Demand for reliability and compliance

Customers face real penalties from financial errors and downtime; GDPR fines can reach €20 million or 4% of global turnover. High expectations for uptime (commonly 99.9%+), strict support SLAs and fast compliance responsiveness boost buyer leverage. Clear incident communication and audit readiness (eg ISO/IEC 27001) reduce risk, while superior trust allows Fortnox to justify premium pricing and curb buyer power.

- Uptime: 99.9%+

- Compliance: GDPR fines €20M/4% turnover

- Standards: ISO/IEC 27001 readiness

- Benefit: Trust → premium pricing

SME multihoming raises price pressure Swedish accounting locks in 400,000+

SME price sensitivity and multi‑homing (~6 SaaS apps in 2024) increase comparison pressure, but Fortnox’s modular pricing, integrations and automation (ROI) reduce buyer leverage. Data migration and embedded banking create lock‑in—>400,000+ Swedish SMEs, >500,000 subscriptions (2024). Compliance (GDPR €20M/4%) and 99.9%+ uptime support premium pricing.

| Metric | Value (2024) |

|---|---|

| Swedish customers | 400,000+ |

| Subscriptions | 500,000+ |

| Apps per SME | ~6 |

| GDPR fine | €20M/4% |

| Uptime | 99.9%+ |

Full Version Awaits

Fortnox Porter's Five Forces Analysis

This preview shows the exact Fortnox Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use upon payment. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and clear strategic implications for decision makers.

Description

Don't Miss the Bigger Picture

Fortnox's Porter's Five Forces snapshot highlights moderate supplier power, high buyer expectations, intense rivalry among Nordic SaaS firms, low threat of substitutes, and rising entrant pressure from vertical fintechs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fortnox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud infrastructure

Fortnox depends on hyperscale cloud providers for compute, storage and uptime SLAs, exposing it to vendor concentration risks given AWS (32%), Azure (23%) and Google Cloud (11%) together held ~66% of global cloud market in 2024. Concentration creates switching frictions and price exposure; multi-cloud deployments and reserved instances lower leverage but cannot eliminate outage or price‑hike contagion. Negotiating volume discounts and designing for architectural portability materially reduces supplier power.

Banking and payments integrations

Fortnox’s core value hinges on secure, compliant bank feeds and payment gateways; in 2024 major EU banks and PSPs advertise API access with SLAs commonly at or near 99.9%, while banks control pricing, access terms and maintenance windows that constrain feature delivery.

PSD2/Open Banking improved baseline access—major banks have APIs by 2024—but practical quality and third-party success rates vary widely across institutions, impacting reliability.

Diversifying direct integrations and using aggregation partners (TTPs) materially reduces single-supplier risk and preserves Fortnox’s roadmap flexibility.

Regulatory and tax content providers

Accurate, timely tax tables, e-invoicing formats and compliance schemas (eg EN 16931, adopted 2017) are essential inputs suppliers provide and governments/standards bodies indirectly supply. EU public procurement has required e-invoicing since 2019, forcing Fortnox to embed schemas on fixed timelines. Implementation timelines and poor documentation raise developer costs; strong compliance teams and automated update pipelines limit disruption.

Third‑party app ecosystem partners

Third‑party app partners extend Fortnox value via add‑ons for vertical workflows, payroll and CRM adjacencies; popular niche apps can leverage co‑marketing and revenue shares to negotiate favorable splits. In 2024 Fortnox’s platform reach — serving hundreds of thousands of Swedish SMBs — provides distribution that balances supplier leverage. Clear APIs, certification and tiered marketplaces keep commercial terms favorable.

- Vertical add‑ons boost stickiness

- Niche apps gain co‑marketing leverage

- Platform scale (2024) offsets supplier power

- APIs & certification standardize terms

Skilled software talent

Engineering, security and product specialists are scarce and exert strong bargaining power as talent markets function like critical input suppliers, driving wage pressure and risk to product roadmaps. Remote hiring expands candidate pools but intensifies global competition and retention challenges. Fortnox must invest in culture, modern tooling and clear career paths to retain key skills and protect delivery.

- Talent scarcity — high bargaining power

- Remote hiring — wider pool, more competition

- Wage inflation risk — impacts margins

- Retention levers — culture, tooling, career paths

SMB platform exposed to cloud concentration: AWS 32%, Azure 23%, GCP 11%

Fortnox faces supplier concentration in cloud providers (AWS 32%, Azure 23%, GCP 11% global share in 2024), raising switching and price risks. Banks/PSPs control payment APIs despite PSD2; SLAs commonly ~99.9% in 2024. Diversification (TTPs, multi‑cloud, vertical apps) and platform scale (hundreds of thousands Swedish SMBs 2024) reduce supplier power; talent scarcity increases wage pressure.

| Metric | 2024 |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Bank API SLA | ~99.9% |

| E‑invoicing mandate | EU since 2019 |

| Customer reach | Hundreds of thousands SMBs |

What is included in the product

Tailored exclusively for Fortnox, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to its cloud accounting and SMB software niche. It identifies disruptive substitutes and emerging threats while evaluating dynamics that protect Fortnox’s incumbency and affect pricing and profitability.

A clear, one-sheet summary of Fortnox's Five Forces—instantly reveals competitive pain points and strategic levers for quick decision-making, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Price‑sensitive SME customer base

Price‑sensitive SME customer base—with SMEs accounting for 99% of EU firms (Eurostat 2023) —means monthly SaaS fees are scrutinized; Fortnoxs transparent pricing and modular add‑ons make churn tangible if perceived value falls. Limited seat counts constrain volume discounts, while proven automation ROI (time savings, fewer errors) weakens buyer leverage.

Switching costs via data and workflows

Data migration of historical ledgers and bespoke accountant workflows creates practical lock-in for Fortnox users, with over 400,000 Swedish SMEs on the platform in 2024 making full migrations costly and time-consuming. API exports and standard formats reduce barriers but still require days to weeks of reconfiguration and reconciliation. Embedded payments and bank rule automation further intensify stickiness, moderating buyer power despite many alternatives.

Accountant and advisor influence

Bookkeepers and accounting bureaus heavily shape platform selection for Fortnox; as of 2024 Fortnox reports serving over 500,000 company subscriptions, so bureau recommendations can aggregate substantial demand and secure volume-based terms. Targeted training and partner programs convert these influencers into advocates and can raise switching costs. Losing a few key bureaus could rapidly amplify buyer power and trigger churn.

Multi‑homing across point tools

- multi‑homing: ~6 SaaS apps (2024)

- pressure: higher price/feature comparisons

- defenses: native integrations, bundles

- retention: unified support, SSO

Demand for reliability and compliance

Customers face real penalties from financial errors and downtime; GDPR fines can reach €20 million or 4% of global turnover. High expectations for uptime (commonly 99.9%+), strict support SLAs and fast compliance responsiveness boost buyer leverage. Clear incident communication and audit readiness (eg ISO/IEC 27001) reduce risk, while superior trust allows Fortnox to justify premium pricing and curb buyer power.

- Uptime: 99.9%+

- Compliance: GDPR fines €20M/4% turnover

- Standards: ISO/IEC 27001 readiness

- Benefit: Trust → premium pricing

SME multihoming raises price pressure Swedish accounting locks in 400,000+

SME price sensitivity and multi‑homing (~6 SaaS apps in 2024) increase comparison pressure, but Fortnox’s modular pricing, integrations and automation (ROI) reduce buyer leverage. Data migration and embedded banking create lock‑in—>400,000+ Swedish SMEs, >500,000 subscriptions (2024). Compliance (GDPR €20M/4%) and 99.9%+ uptime support premium pricing.

| Metric | Value (2024) |

|---|---|

| Swedish customers | 400,000+ |

| Subscriptions | 500,000+ |

| Apps per SME | ~6 |

| GDPR fine | €20M/4% |

| Uptime | 99.9%+ |

Full Version Awaits

Fortnox Porter's Five Forces Analysis

This preview shows the exact Fortnox Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professional, and ready for download and use upon payment. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and clear strategic implications for decision makers.