Fox PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic cycles, social trends, and tech disruption shape Fox’s strategic options in our concise PESTLE preview. This snapshot highlights key risks and opportunities for investors and strategists. Buy the full PESTLE for the complete, actionable analysis and downloadable templates.

Political factors

Regulatory scrutiny of news media

Content-oversight and political-bias debates have prompted investigations and hearings that directly affect Fox News Media, as exemplified by the April 2023 Dominion settlement of 787.5 million dollars, underscoring legal and financial exposure.

Shifts in administration priorities can change enforcement intensity and investigative focus, raising compliance costs and operational uncertainty for Fox.

Adverse findings risk fines or mandated practice changes and political pressure has historically influenced advertiser sentiment and affiliate relations, affecting ad revenue and distribution partnerships.

FCC and broadcast policy direction

FCC leadership under Chair Jessica Rosenworcel is directing rulemakings on ownership caps (statutory national audience reach cap 39 percent), retransmission consent and public-interest obligations, all of which reshape Fox Television Stations (28 owned stations) bargaining power with MVPDs. Relaxation of limits facilitates consolidation and scale-driven retransmission revenues; tightening constrains growth and portfolio deals. Ongoing rulemakings create planning and investment uncertainty for Fox.

Sports rights and national interest

Major sports contracts sit alongside antitrust debates and league exemptions as multibillion-dollar rights (major U.S. league deals total roughly 100–120 billion USD across networks into the 2030s), shaping Fox Sports bargaining power. Political focus on sports betting (U.S. handle ~89 billion USD in 2023), NIL and athlete welfare can raise rights costs and compliance spend. International events add geopolitical risks to coverage and government stances can alter cross-border carriage and licensing across 40+ markets.

Election cycles and public funding priorities

- Ad spend: >$10B (U.S. 2024 cycle)

- Viewership spikes: 2x–3x on key nights

- Operational strain: heightened staffing/tech costs

- Compliance: stricter political ad regulations

Foreign relations and supply chains

Trade tensions, including US Section 301 tariffs covering roughly $370 billion of Chinese goods, raise capex and lead times for broadcast equipment; visa constraints (H-1B cap 85,000) strain technical staffing; sanctions on Russia and other jurisdictions since 2022 limit content partnerships and distribution; currency volatility and policy shifts complicate bidding for global sports rights in an ~$50 billion market.

- Tariffs: Section 301 ~$370B

- Visas: H-1B cap 85,000

- Sanctions: Russia/2022 impact

- Sports rights: ~ $50B market

Defamation risk $787.5M and $10B election ad volatility

Political scrutiny and defamation liabilities (Dominion settlement $787.5M) increase legal and compliance costs for Fox; regulatory rulemakings (FCC ownership cap 39%) and trade/visa limits (Section 301 ~$370B; H‑1B cap 85,000) add operational uncertainty. Election cycles (US political ad spend ~ $10B in 2024) drive volatile ad revenue and viewership spikes; sports-rights and betting policy (US handle ~$89B; rights market $100–120B) affect costs and carriage.

| Factor | Key Metric |

|---|---|

| Defamation cost | $787.5M |

| FCC cap | 39% |

| US political ads 2024 | $10B |

| Sports rights market | $100–120B |

| Sports betting 2023 | $89B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fox across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to reveal specific threats and opportunities. Designed for executives and investors, the analysis offers forward-looking insights and ready-to-use formatting for plans, decks, and reports.

Provides a concise, visually segmented PESTLE summary for Fox that can be dropped into presentations or shared across teams to speed alignment and simplify external-risk discussions.

Economic factors

Advertising market cycles

Ad revenue at Fox tracks GDP and consumer confidence closely—US ad spend reached about $390B in 2024 (eMarketer), so brand budget shifts materially affect top-line advertising. Downturns typically compress CPMs and fill rates across TV and digital, often reducing pricing 20–30% in weak quarters. Cyclical rebounds and tentpole events can rapidly restore pricing power, while growing affiliate and distribution fees cushions revenue volatility.

Affiliate and distribution fees

Retransmission and carriage fees are a steady revenue stream for Fox but hinge on subscriber trends, with ongoing cord-cutting reducing volumes even as per-subscriber rates have risen. Negotiation outcomes with MVPDs and vMVPDs directly affect near-term margins and cash flow. Blackouts during disputes risk audience erosion and political scrutiny, amplifying reputational impact for Fox.

Sports rights inflation

Premium live sports rights are rising faster than ad growth, squeezing margins; Amazon reportedly pays about 1 billion per year for NFL Thursday Night Football, illustrating escalated pricing. Fox can offset cost pressure through strategic portfolio curation and sublicensing to regional and streaming partners. Monetization via dynamic ad insertion and cross-platform bundles is critical to lift yield per viewer. Competitive bids from streamers like Amazon and Apple intensify pricing pressure.

Labor and production costs

Wage inflation and new union agreements raised operating costs for Fox; US average hourly earnings grew about 3.9% YoY in 2024 (BLS), while SAG-AFTRA/WGA actions in 2023 (July–Nov) highlighted exposure to labor disputes.

Remote and cloud production reduce some fixed costs, but strikes disrupt pipelines and insurance/security around high-profile events pushed commercial insurance rates up roughly 10–15% in 2024 (Marsh).

- Wage growth: 3.9% (2024, BLS)

- Major strike period: Jul–Nov 2023

- Insurance rate rise: ~10–15% (2024, Marsh)

- Remote/cloud mitigate but don’t eliminate labor risk

Capital markets and FX

Higher global rates (US fed funds ~5.25–5.50% in 2024–25) raise Fox’s debt service and constrain share buyback capacity; S&P 500 forward P/E ~17.5 in mid‑2025 limits equity‑financed M&A flexibility. A stronger dollar (DXY ~103–105) raises costs for international rights and studio equipment, while VIX ~17–20 shifts advertiser mix toward performance and slows pacing.

- Rates: higher debt service, less buybacks

- Equity P/E: limits M&A leeway

- FX DXY ~103–105: costly rights/equipment

- VIX ~17–20: advertiser mix & pacing shift

Defamation risk $787.5M and $10B election ad volatility

Fox revenue is sensitive to US ad spend (~$390B in 2024) and GDP; downturns can cut CPMs 20–30% but tentpoles restore pricing. Retransmission fees offset cord-cutting as per‑sub rates rise; carriage disputes risk blackouts. Sports rights inflation (e.g., NFL TNF ~$1B/yr) and wage growth (3.9% 2024) squeeze margins while rates (~5.25–5.50%) raise debt costs.

| Metric | Value |

|---|---|

| US ad spend 2024 | $390B |

| Wage growth 2024 | 3.9% |

| Fed funds (2024–25) | 5.25–5.50% |

| DXY | 103–105 |

Preview the Actual Deliverable

Fox PESTLE Analysis

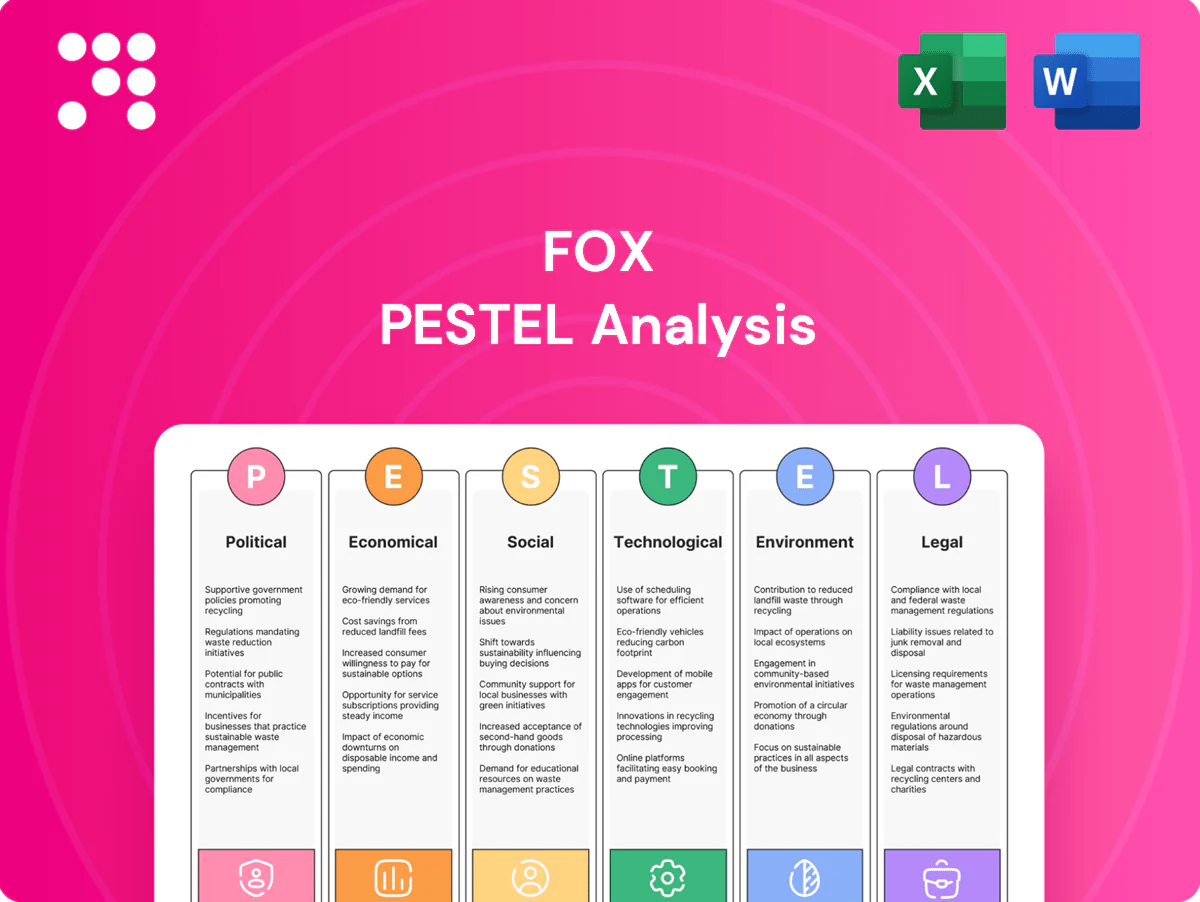

The preview shown here of the Fox PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers, delivered exactly as shown. After payment you’ll be able to download this final, professionally structured file instantly.

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic cycles, social trends, and tech disruption shape Fox’s strategic options in our concise PESTLE preview. This snapshot highlights key risks and opportunities for investors and strategists. Buy the full PESTLE for the complete, actionable analysis and downloadable templates.

Political factors

Regulatory scrutiny of news media

Content-oversight and political-bias debates have prompted investigations and hearings that directly affect Fox News Media, as exemplified by the April 2023 Dominion settlement of 787.5 million dollars, underscoring legal and financial exposure.

Shifts in administration priorities can change enforcement intensity and investigative focus, raising compliance costs and operational uncertainty for Fox.

Adverse findings risk fines or mandated practice changes and political pressure has historically influenced advertiser sentiment and affiliate relations, affecting ad revenue and distribution partnerships.

FCC and broadcast policy direction

FCC leadership under Chair Jessica Rosenworcel is directing rulemakings on ownership caps (statutory national audience reach cap 39 percent), retransmission consent and public-interest obligations, all of which reshape Fox Television Stations (28 owned stations) bargaining power with MVPDs. Relaxation of limits facilitates consolidation and scale-driven retransmission revenues; tightening constrains growth and portfolio deals. Ongoing rulemakings create planning and investment uncertainty for Fox.

Sports rights and national interest

Major sports contracts sit alongside antitrust debates and league exemptions as multibillion-dollar rights (major U.S. league deals total roughly 100–120 billion USD across networks into the 2030s), shaping Fox Sports bargaining power. Political focus on sports betting (U.S. handle ~89 billion USD in 2023), NIL and athlete welfare can raise rights costs and compliance spend. International events add geopolitical risks to coverage and government stances can alter cross-border carriage and licensing across 40+ markets.

Election cycles and public funding priorities

- Ad spend: >$10B (U.S. 2024 cycle)

- Viewership spikes: 2x–3x on key nights

- Operational strain: heightened staffing/tech costs

- Compliance: stricter political ad regulations

Foreign relations and supply chains

Trade tensions, including US Section 301 tariffs covering roughly $370 billion of Chinese goods, raise capex and lead times for broadcast equipment; visa constraints (H-1B cap 85,000) strain technical staffing; sanctions on Russia and other jurisdictions since 2022 limit content partnerships and distribution; currency volatility and policy shifts complicate bidding for global sports rights in an ~$50 billion market.

- Tariffs: Section 301 ~$370B

- Visas: H-1B cap 85,000

- Sanctions: Russia/2022 impact

- Sports rights: ~ $50B market

Defamation risk $787.5M and $10B election ad volatility

Political scrutiny and defamation liabilities (Dominion settlement $787.5M) increase legal and compliance costs for Fox; regulatory rulemakings (FCC ownership cap 39%) and trade/visa limits (Section 301 ~$370B; H‑1B cap 85,000) add operational uncertainty. Election cycles (US political ad spend ~ $10B in 2024) drive volatile ad revenue and viewership spikes; sports-rights and betting policy (US handle ~$89B; rights market $100–120B) affect costs and carriage.

| Factor | Key Metric |

|---|---|

| Defamation cost | $787.5M |

| FCC cap | 39% |

| US political ads 2024 | $10B |

| Sports rights market | $100–120B |

| Sports betting 2023 | $89B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fox across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to reveal specific threats and opportunities. Designed for executives and investors, the analysis offers forward-looking insights and ready-to-use formatting for plans, decks, and reports.

Provides a concise, visually segmented PESTLE summary for Fox that can be dropped into presentations or shared across teams to speed alignment and simplify external-risk discussions.

Economic factors

Advertising market cycles

Ad revenue at Fox tracks GDP and consumer confidence closely—US ad spend reached about $390B in 2024 (eMarketer), so brand budget shifts materially affect top-line advertising. Downturns typically compress CPMs and fill rates across TV and digital, often reducing pricing 20–30% in weak quarters. Cyclical rebounds and tentpole events can rapidly restore pricing power, while growing affiliate and distribution fees cushions revenue volatility.

Affiliate and distribution fees

Retransmission and carriage fees are a steady revenue stream for Fox but hinge on subscriber trends, with ongoing cord-cutting reducing volumes even as per-subscriber rates have risen. Negotiation outcomes with MVPDs and vMVPDs directly affect near-term margins and cash flow. Blackouts during disputes risk audience erosion and political scrutiny, amplifying reputational impact for Fox.

Sports rights inflation

Premium live sports rights are rising faster than ad growth, squeezing margins; Amazon reportedly pays about 1 billion per year for NFL Thursday Night Football, illustrating escalated pricing. Fox can offset cost pressure through strategic portfolio curation and sublicensing to regional and streaming partners. Monetization via dynamic ad insertion and cross-platform bundles is critical to lift yield per viewer. Competitive bids from streamers like Amazon and Apple intensify pricing pressure.

Labor and production costs

Wage inflation and new union agreements raised operating costs for Fox; US average hourly earnings grew about 3.9% YoY in 2024 (BLS), while SAG-AFTRA/WGA actions in 2023 (July–Nov) highlighted exposure to labor disputes.

Remote and cloud production reduce some fixed costs, but strikes disrupt pipelines and insurance/security around high-profile events pushed commercial insurance rates up roughly 10–15% in 2024 (Marsh).

- Wage growth: 3.9% (2024, BLS)

- Major strike period: Jul–Nov 2023

- Insurance rate rise: ~10–15% (2024, Marsh)

- Remote/cloud mitigate but don’t eliminate labor risk

Capital markets and FX

Higher global rates (US fed funds ~5.25–5.50% in 2024–25) raise Fox’s debt service and constrain share buyback capacity; S&P 500 forward P/E ~17.5 in mid‑2025 limits equity‑financed M&A flexibility. A stronger dollar (DXY ~103–105) raises costs for international rights and studio equipment, while VIX ~17–20 shifts advertiser mix toward performance and slows pacing.

- Rates: higher debt service, less buybacks

- Equity P/E: limits M&A leeway

- FX DXY ~103–105: costly rights/equipment

- VIX ~17–20: advertiser mix & pacing shift

Defamation risk $787.5M and $10B election ad volatility

Fox revenue is sensitive to US ad spend (~$390B in 2024) and GDP; downturns can cut CPMs 20–30% but tentpoles restore pricing. Retransmission fees offset cord-cutting as per‑sub rates rise; carriage disputes risk blackouts. Sports rights inflation (e.g., NFL TNF ~$1B/yr) and wage growth (3.9% 2024) squeeze margins while rates (~5.25–5.50%) raise debt costs.

| Metric | Value |

|---|---|

| US ad spend 2024 | $390B |

| Wage growth 2024 | 3.9% |

| Fed funds (2024–25) | 5.25–5.50% |

| DXY | 103–105 |

Preview the Actual Deliverable

Fox PESTLE Analysis

The preview shown here of the Fox PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers, delivered exactly as shown. After payment you’ll be able to download this final, professionally structured file instantly.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Uncover how political shifts, economic cycles, social trends, and tech disruption shape Fox’s strategic options in our concise PESTLE preview. This snapshot highlights key risks and opportunities for investors and strategists. Buy the full PESTLE for the complete, actionable analysis and downloadable templates.

Political factors

Regulatory scrutiny of news media

Content-oversight and political-bias debates have prompted investigations and hearings that directly affect Fox News Media, as exemplified by the April 2023 Dominion settlement of 787.5 million dollars, underscoring legal and financial exposure.

Shifts in administration priorities can change enforcement intensity and investigative focus, raising compliance costs and operational uncertainty for Fox.

Adverse findings risk fines or mandated practice changes and political pressure has historically influenced advertiser sentiment and affiliate relations, affecting ad revenue and distribution partnerships.

FCC and broadcast policy direction

FCC leadership under Chair Jessica Rosenworcel is directing rulemakings on ownership caps (statutory national audience reach cap 39 percent), retransmission consent and public-interest obligations, all of which reshape Fox Television Stations (28 owned stations) bargaining power with MVPDs. Relaxation of limits facilitates consolidation and scale-driven retransmission revenues; tightening constrains growth and portfolio deals. Ongoing rulemakings create planning and investment uncertainty for Fox.

Sports rights and national interest

Major sports contracts sit alongside antitrust debates and league exemptions as multibillion-dollar rights (major U.S. league deals total roughly 100–120 billion USD across networks into the 2030s), shaping Fox Sports bargaining power. Political focus on sports betting (U.S. handle ~89 billion USD in 2023), NIL and athlete welfare can raise rights costs and compliance spend. International events add geopolitical risks to coverage and government stances can alter cross-border carriage and licensing across 40+ markets.

Election cycles and public funding priorities

- Ad spend: >$10B (U.S. 2024 cycle)

- Viewership spikes: 2x–3x on key nights

- Operational strain: heightened staffing/tech costs

- Compliance: stricter political ad regulations

Foreign relations and supply chains

Trade tensions, including US Section 301 tariffs covering roughly $370 billion of Chinese goods, raise capex and lead times for broadcast equipment; visa constraints (H-1B cap 85,000) strain technical staffing; sanctions on Russia and other jurisdictions since 2022 limit content partnerships and distribution; currency volatility and policy shifts complicate bidding for global sports rights in an ~$50 billion market.

- Tariffs: Section 301 ~$370B

- Visas: H-1B cap 85,000

- Sanctions: Russia/2022 impact

- Sports rights: ~ $50B market

Defamation risk $787.5M and $10B election ad volatility

Political scrutiny and defamation liabilities (Dominion settlement $787.5M) increase legal and compliance costs for Fox; regulatory rulemakings (FCC ownership cap 39%) and trade/visa limits (Section 301 ~$370B; H‑1B cap 85,000) add operational uncertainty. Election cycles (US political ad spend ~ $10B in 2024) drive volatile ad revenue and viewership spikes; sports-rights and betting policy (US handle ~$89B; rights market $100–120B) affect costs and carriage.

| Factor | Key Metric |

|---|---|

| Defamation cost | $787.5M |

| FCC cap | 39% |

| US political ads 2024 | $10B |

| Sports rights market | $100–120B |

| Sports betting 2023 | $89B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fox across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and current trends to reveal specific threats and opportunities. Designed for executives and investors, the analysis offers forward-looking insights and ready-to-use formatting for plans, decks, and reports.

Provides a concise, visually segmented PESTLE summary for Fox that can be dropped into presentations or shared across teams to speed alignment and simplify external-risk discussions.

Economic factors

Advertising market cycles

Ad revenue at Fox tracks GDP and consumer confidence closely—US ad spend reached about $390B in 2024 (eMarketer), so brand budget shifts materially affect top-line advertising. Downturns typically compress CPMs and fill rates across TV and digital, often reducing pricing 20–30% in weak quarters. Cyclical rebounds and tentpole events can rapidly restore pricing power, while growing affiliate and distribution fees cushions revenue volatility.

Affiliate and distribution fees

Retransmission and carriage fees are a steady revenue stream for Fox but hinge on subscriber trends, with ongoing cord-cutting reducing volumes even as per-subscriber rates have risen. Negotiation outcomes with MVPDs and vMVPDs directly affect near-term margins and cash flow. Blackouts during disputes risk audience erosion and political scrutiny, amplifying reputational impact for Fox.

Sports rights inflation

Premium live sports rights are rising faster than ad growth, squeezing margins; Amazon reportedly pays about 1 billion per year for NFL Thursday Night Football, illustrating escalated pricing. Fox can offset cost pressure through strategic portfolio curation and sublicensing to regional and streaming partners. Monetization via dynamic ad insertion and cross-platform bundles is critical to lift yield per viewer. Competitive bids from streamers like Amazon and Apple intensify pricing pressure.

Labor and production costs

Wage inflation and new union agreements raised operating costs for Fox; US average hourly earnings grew about 3.9% YoY in 2024 (BLS), while SAG-AFTRA/WGA actions in 2023 (July–Nov) highlighted exposure to labor disputes.

Remote and cloud production reduce some fixed costs, but strikes disrupt pipelines and insurance/security around high-profile events pushed commercial insurance rates up roughly 10–15% in 2024 (Marsh).

- Wage growth: 3.9% (2024, BLS)

- Major strike period: Jul–Nov 2023

- Insurance rate rise: ~10–15% (2024, Marsh)

- Remote/cloud mitigate but don’t eliminate labor risk

Capital markets and FX

Higher global rates (US fed funds ~5.25–5.50% in 2024–25) raise Fox’s debt service and constrain share buyback capacity; S&P 500 forward P/E ~17.5 in mid‑2025 limits equity‑financed M&A flexibility. A stronger dollar (DXY ~103–105) raises costs for international rights and studio equipment, while VIX ~17–20 shifts advertiser mix toward performance and slows pacing.

- Rates: higher debt service, less buybacks

- Equity P/E: limits M&A leeway

- FX DXY ~103–105: costly rights/equipment

- VIX ~17–20: advertiser mix & pacing shift

Defamation risk $787.5M and $10B election ad volatility

Fox revenue is sensitive to US ad spend (~$390B in 2024) and GDP; downturns can cut CPMs 20–30% but tentpoles restore pricing. Retransmission fees offset cord-cutting as per‑sub rates rise; carriage disputes risk blackouts. Sports rights inflation (e.g., NFL TNF ~$1B/yr) and wage growth (3.9% 2024) squeeze margins while rates (~5.25–5.50%) raise debt costs.

| Metric | Value |

|---|---|

| US ad spend 2024 | $390B |

| Wage growth 2024 | 3.9% |

| Fed funds (2024–25) | 5.25–5.50% |

| DXY | 103–105 |

Preview the Actual Deliverable

Fox PESTLE Analysis

The preview shown here of the Fox PESTLE Analysis is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers, delivered exactly as shown. After payment you’ll be able to download this final, professionally structured file instantly.