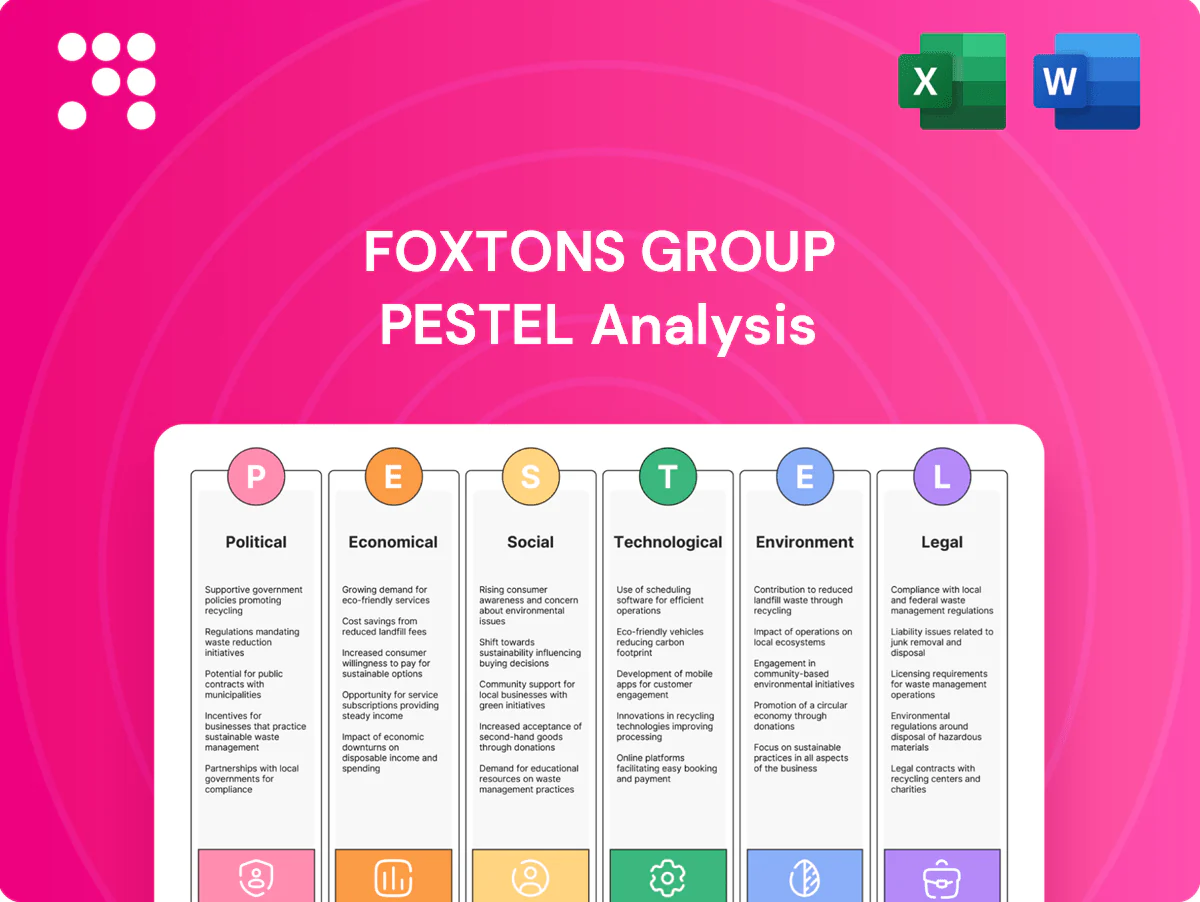

Foxtons Group PESTLE Analysis

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Foxtons Group, revealing how political, economic and regulatory shifts shape its UK real estate position. We unpack technological, social and environmental drivers that affect listings, commissions and compliance. Ideal for investors, advisors and managers seeking actionable insight. Purchase the full report for deep-dive data, charts and ready-to-use recommendations.

Political factors

UK housing policy and planning direction

National planning reforms and the 300,000 homes pa target, plus the GLA's ~66,000 homes pa London need and rising borough affordable requirements (commonly 35%+) are reshaping supply and transaction volumes. Foxtons must track policy consultations and mayoral strategies by borough, align with local plans to secure developer instructions, and use scenario planning to smooth revenue across policy cycles.

Stamp Duty and property tax changes

Adjustments to Stamp Duty Land Tax nil-rate band (currently £250,000) and surcharges (3% on additional properties, 2% non-resident surcharge) directly shift buyer sentiment, timing and price-band activity. Surcharges can push marginal buyers toward lettings, altering sales-vs-lettings demand. Foxtons should time pricing advice and targeted marketing around fiscal announcements. Flexible fee strategies can capture displaced demand and convert renters into landlords.

Private rented sector reforms

Reforms to tenancy rules, notice periods and landlord obligations (affecting about 4.5m private rented households, ~19% of UK homes) could reduce landlord ROI and increase letting churn. Abolition/amendment of no-fault evictions and stronger tenant rights raise management intensity and dispute handling. Foxtons can differentiate with compliance guidance, landlord education and expanded property management services to mitigate regulatory burden.

Local government licensing and enforcement

Local selective licensing and HMO rules reshape Foxtons operating costs and listing eligibility, with over 50 English councils running selective licensing schemes by 2024 and HMOs subject to borough-specific caps and licensing fees that can add thousands per property.

- Compliance variation: borough-level rules require granular audit trails

- Cost impact: licenses/repairs raise per-listing expense

- Scale solution: standardize processes across branches

- Speed: visibility on local timelines improves transaction velocity

Immigration and international mobility stance

Visa rules and student caps materially influence inbound buyer flows and tenant demand in Foxtons’ prime and commuter markets; UK net migration was 606,000 year to June 2023 (ONS), a driver of urban occupancy and rent pressure. Changes in migration quickly affect occupancy rates and rents, so Foxtons can launch tailored student and corporate packages and secure recurring demand via university and relocation partnerships.

- Target: students, corporates

- Partnerships: universities, relocation firms

- Risk: visa caps reduce overseas buyer/tenant inflows

300,000 homes target, higher affordable minima and SDLT surcharges shift market to lettings

Planning targets (300,000 homes pa UK, GLA ~66,000 pa) and rising borough affordable minima (commonly 35%+) alter supply and instructions. SDLT nil-rate £250,000 plus 3%/2% surcharges shift buyer timing toward lettings. Tenancy reforms (4.5m PRS households, ~19% homes), 50+ selective licensing councils and 606,000 net migration (to Jun 2023) change demand, compliance and management costs.

| Factor | Key stat | Implication |

|---|---|---|

| Housing targets | 300,000 UK / 66,000 London | Instruction mix shifts |

| Tax | NRB £250k; 3%/2% | Sales→lettings pressure |

| PRS rules | 4.5m households | Higher management costs |

What is included in the product

Explores how macro-environmental factors uniquely affect Foxtons Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed insights, forward-looking scenarios and practical implications for executives, investors and advisors operating in the UK property market.

A concise, shareable PESTLE snapshot of Foxtons Group that’s visually segmented for quick interpretation, ideal for meetings, presentations, and cross-team alignment; editable notes let users tailor external risk and market-position insights to region or business line.

Economic factors

Interest rates and mortgage availability

Rate cycles (Bank Rate around 5.25% in 2024–25) directly affect affordability, approvals and buyer urgency, hitting first-time buyers—who comprise roughly 40% of purchases—hardest and keeping purchase volumes below pre‑2019 levels.

Lender criteria swing with the cycle, raising fall‑through risk when underwriting tightens; Foxtons mitigates this by pre‑qualifying buyers and matching listings to prevailing affordability bands.

Developer part‑exchange schemes and strengthened broker alliances reduce transaction friction and conversion risk, supporting volumes even in higher‑rate environments.

Inflation, wages, and household confidence

UK inflation eased from a 2022 peak of about 11% to below 4% in 2024, yet real incomes remain squeezed as wage growth lagged core prices, directly limiting rental affordability and purchase budgets. Persistent negative GfK consumer confidence through 2024 lowered viewing-to-offer conversion and increased chain fragility. Foxtons should tie pricing guidance and marketing cadence to sentiment indicators and use flexible fee structures to preserve volume in softer periods.

London housing supply-demand imbalance

Chronic under-supply in London—GLA estimated need ~66,000 homes pa vs delivery ~40,000 pa—supports prices while constraining transaction volumes. Rapid Build-to-Rent growth (UK pipeline ~150,000 units, c.60,000 in London) and rising institutional ownership shift inventory mix. Foxtons can deepen landlord networks and secure new-build instructions from developers. Data-led targeting across 50+ micro-markets pinpoints pockets of liquidity.

Currency movements and foreign capital

Sterling volatility — GBP/USD around 1.27 in mid‑2025 — can both attract price‑sensitive international buyers to prime central London and deter others; Foxtons can time marketing to currency windows while advising clients on hedging and cross‑border payment options that speed settlements. Multilingual agents and international referral partners expand reach into key markets.

- FX exposure: price windows matter

- Hedging/payment fintech: smoother timelines

- Campaigns timed to GBP strength/weakness

- Multilingual agents + referral network

Corporate relocations and employment hubs

Changes in City, tech and media clusters shift Foxtons rental hotspots and sales turnover as London office vacancy hovered near 10% in 2024 while central footfall recovered to roughly 70% of 2019 levels, concentrating demand in South Bank, Canary Wharf and tech corridors.

Hybrid work raised suburban and Zone 3-5 demand; Foxtons can realign branches to transport-linked corridors and new office hubs, using corporate lettings—which accounted for a growing share of agency pipelines in 2024—to stabilise occupancy.

- Vacancy ~10% (2024)

- Central footfall ~70% of 2019 (2024)

- Growth in Zone 3-5 rental demand

- Corporate lettings stabilise occupancy

300,000 homes target, higher affordable minima and SDLT surcharges shift market to lettings

Higher Bank Rate (~5.25% in 2024–25) and tighter lending cut affordability (first‑time buyers ~40% of purchases), damping volumes; chronic London under‑supply (need ~66k pa vs delivery ~40k) supports prices but limits transactions. Build‑to‑Rent pipeline (~150k UK, ~60k London) and sterling swings (GBP/USD ~1.27 mid‑2025) shift buyer mix toward institutions and price‑sensitive internationals.

| Indicator | 2024–25 | Impact |

|---|---|---|

| Bank Rate | ~5.25% | Lower affordability |

| First‑time buyers | ~40% | Volume sensitivity |

| London supply gap | 66k need vs 40k delivery | Price support |

| BTR pipeline | ~150k UK / ~60k London | More institutional stock |

| GBP/USD | ~1.27 | Shifts intl demand |

Full Version Awaits

Foxtons Group PESTLE Analysis

This Foxtons Group PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the business. The content and structure shown in the preview is the same document you’ll download after payment, fully formatted and ready to use. It’s the exact, finished file you’ll own immediately after checkout.

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Foxtons Group, revealing how political, economic and regulatory shifts shape its UK real estate position. We unpack technological, social and environmental drivers that affect listings, commissions and compliance. Ideal for investors, advisors and managers seeking actionable insight. Purchase the full report for deep-dive data, charts and ready-to-use recommendations.

Political factors

UK housing policy and planning direction

National planning reforms and the 300,000 homes pa target, plus the GLA's ~66,000 homes pa London need and rising borough affordable requirements (commonly 35%+) are reshaping supply and transaction volumes. Foxtons must track policy consultations and mayoral strategies by borough, align with local plans to secure developer instructions, and use scenario planning to smooth revenue across policy cycles.

Stamp Duty and property tax changes

Adjustments to Stamp Duty Land Tax nil-rate band (currently £250,000) and surcharges (3% on additional properties, 2% non-resident surcharge) directly shift buyer sentiment, timing and price-band activity. Surcharges can push marginal buyers toward lettings, altering sales-vs-lettings demand. Foxtons should time pricing advice and targeted marketing around fiscal announcements. Flexible fee strategies can capture displaced demand and convert renters into landlords.

Private rented sector reforms

Reforms to tenancy rules, notice periods and landlord obligations (affecting about 4.5m private rented households, ~19% of UK homes) could reduce landlord ROI and increase letting churn. Abolition/amendment of no-fault evictions and stronger tenant rights raise management intensity and dispute handling. Foxtons can differentiate with compliance guidance, landlord education and expanded property management services to mitigate regulatory burden.

Local government licensing and enforcement

Local selective licensing and HMO rules reshape Foxtons operating costs and listing eligibility, with over 50 English councils running selective licensing schemes by 2024 and HMOs subject to borough-specific caps and licensing fees that can add thousands per property.

- Compliance variation: borough-level rules require granular audit trails

- Cost impact: licenses/repairs raise per-listing expense

- Scale solution: standardize processes across branches

- Speed: visibility on local timelines improves transaction velocity

Immigration and international mobility stance

Visa rules and student caps materially influence inbound buyer flows and tenant demand in Foxtons’ prime and commuter markets; UK net migration was 606,000 year to June 2023 (ONS), a driver of urban occupancy and rent pressure. Changes in migration quickly affect occupancy rates and rents, so Foxtons can launch tailored student and corporate packages and secure recurring demand via university and relocation partnerships.

- Target: students, corporates

- Partnerships: universities, relocation firms

- Risk: visa caps reduce overseas buyer/tenant inflows

300,000 homes target, higher affordable minima and SDLT surcharges shift market to lettings

Planning targets (300,000 homes pa UK, GLA ~66,000 pa) and rising borough affordable minima (commonly 35%+) alter supply and instructions. SDLT nil-rate £250,000 plus 3%/2% surcharges shift buyer timing toward lettings. Tenancy reforms (4.5m PRS households, ~19% homes), 50+ selective licensing councils and 606,000 net migration (to Jun 2023) change demand, compliance and management costs.

| Factor | Key stat | Implication |

|---|---|---|

| Housing targets | 300,000 UK / 66,000 London | Instruction mix shifts |

| Tax | NRB £250k; 3%/2% | Sales→lettings pressure |

| PRS rules | 4.5m households | Higher management costs |

What is included in the product

Explores how macro-environmental factors uniquely affect Foxtons Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed insights, forward-looking scenarios and practical implications for executives, investors and advisors operating in the UK property market.

A concise, shareable PESTLE snapshot of Foxtons Group that’s visually segmented for quick interpretation, ideal for meetings, presentations, and cross-team alignment; editable notes let users tailor external risk and market-position insights to region or business line.

Economic factors

Interest rates and mortgage availability

Rate cycles (Bank Rate around 5.25% in 2024–25) directly affect affordability, approvals and buyer urgency, hitting first-time buyers—who comprise roughly 40% of purchases—hardest and keeping purchase volumes below pre‑2019 levels.

Lender criteria swing with the cycle, raising fall‑through risk when underwriting tightens; Foxtons mitigates this by pre‑qualifying buyers and matching listings to prevailing affordability bands.

Developer part‑exchange schemes and strengthened broker alliances reduce transaction friction and conversion risk, supporting volumes even in higher‑rate environments.

Inflation, wages, and household confidence

UK inflation eased from a 2022 peak of about 11% to below 4% in 2024, yet real incomes remain squeezed as wage growth lagged core prices, directly limiting rental affordability and purchase budgets. Persistent negative GfK consumer confidence through 2024 lowered viewing-to-offer conversion and increased chain fragility. Foxtons should tie pricing guidance and marketing cadence to sentiment indicators and use flexible fee structures to preserve volume in softer periods.

London housing supply-demand imbalance

Chronic under-supply in London—GLA estimated need ~66,000 homes pa vs delivery ~40,000 pa—supports prices while constraining transaction volumes. Rapid Build-to-Rent growth (UK pipeline ~150,000 units, c.60,000 in London) and rising institutional ownership shift inventory mix. Foxtons can deepen landlord networks and secure new-build instructions from developers. Data-led targeting across 50+ micro-markets pinpoints pockets of liquidity.

Currency movements and foreign capital

Sterling volatility — GBP/USD around 1.27 in mid‑2025 — can both attract price‑sensitive international buyers to prime central London and deter others; Foxtons can time marketing to currency windows while advising clients on hedging and cross‑border payment options that speed settlements. Multilingual agents and international referral partners expand reach into key markets.

- FX exposure: price windows matter

- Hedging/payment fintech: smoother timelines

- Campaigns timed to GBP strength/weakness

- Multilingual agents + referral network

Corporate relocations and employment hubs

Changes in City, tech and media clusters shift Foxtons rental hotspots and sales turnover as London office vacancy hovered near 10% in 2024 while central footfall recovered to roughly 70% of 2019 levels, concentrating demand in South Bank, Canary Wharf and tech corridors.

Hybrid work raised suburban and Zone 3-5 demand; Foxtons can realign branches to transport-linked corridors and new office hubs, using corporate lettings—which accounted for a growing share of agency pipelines in 2024—to stabilise occupancy.

- Vacancy ~10% (2024)

- Central footfall ~70% of 2019 (2024)

- Growth in Zone 3-5 rental demand

- Corporate lettings stabilise occupancy

300,000 homes target, higher affordable minima and SDLT surcharges shift market to lettings

Higher Bank Rate (~5.25% in 2024–25) and tighter lending cut affordability (first‑time buyers ~40% of purchases), damping volumes; chronic London under‑supply (need ~66k pa vs delivery ~40k) supports prices but limits transactions. Build‑to‑Rent pipeline (~150k UK, ~60k London) and sterling swings (GBP/USD ~1.27 mid‑2025) shift buyer mix toward institutions and price‑sensitive internationals.

| Indicator | 2024–25 | Impact |

|---|---|---|

| Bank Rate | ~5.25% | Lower affordability |

| First‑time buyers | ~40% | Volume sensitivity |

| London supply gap | 66k need vs 40k delivery | Price support |

| BTR pipeline | ~150k UK / ~60k London | More institutional stock |

| GBP/USD | ~1.27 | Shifts intl demand |

Full Version Awaits

Foxtons Group PESTLE Analysis

This Foxtons Group PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the business. The content and structure shown in the preview is the same document you’ll download after payment, fully formatted and ready to use. It’s the exact, finished file you’ll own immediately after checkout.

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Foxtons Group, revealing how political, economic and regulatory shifts shape its UK real estate position. We unpack technological, social and environmental drivers that affect listings, commissions and compliance. Ideal for investors, advisors and managers seeking actionable insight. Purchase the full report for deep-dive data, charts and ready-to-use recommendations.

Political factors

UK housing policy and planning direction

National planning reforms and the 300,000 homes pa target, plus the GLA's ~66,000 homes pa London need and rising borough affordable requirements (commonly 35%+) are reshaping supply and transaction volumes. Foxtons must track policy consultations and mayoral strategies by borough, align with local plans to secure developer instructions, and use scenario planning to smooth revenue across policy cycles.

Stamp Duty and property tax changes

Adjustments to Stamp Duty Land Tax nil-rate band (currently £250,000) and surcharges (3% on additional properties, 2% non-resident surcharge) directly shift buyer sentiment, timing and price-band activity. Surcharges can push marginal buyers toward lettings, altering sales-vs-lettings demand. Foxtons should time pricing advice and targeted marketing around fiscal announcements. Flexible fee strategies can capture displaced demand and convert renters into landlords.

Private rented sector reforms

Reforms to tenancy rules, notice periods and landlord obligations (affecting about 4.5m private rented households, ~19% of UK homes) could reduce landlord ROI and increase letting churn. Abolition/amendment of no-fault evictions and stronger tenant rights raise management intensity and dispute handling. Foxtons can differentiate with compliance guidance, landlord education and expanded property management services to mitigate regulatory burden.

Local government licensing and enforcement

Local selective licensing and HMO rules reshape Foxtons operating costs and listing eligibility, with over 50 English councils running selective licensing schemes by 2024 and HMOs subject to borough-specific caps and licensing fees that can add thousands per property.

- Compliance variation: borough-level rules require granular audit trails

- Cost impact: licenses/repairs raise per-listing expense

- Scale solution: standardize processes across branches

- Speed: visibility on local timelines improves transaction velocity

Immigration and international mobility stance

Visa rules and student caps materially influence inbound buyer flows and tenant demand in Foxtons’ prime and commuter markets; UK net migration was 606,000 year to June 2023 (ONS), a driver of urban occupancy and rent pressure. Changes in migration quickly affect occupancy rates and rents, so Foxtons can launch tailored student and corporate packages and secure recurring demand via university and relocation partnerships.

- Target: students, corporates

- Partnerships: universities, relocation firms

- Risk: visa caps reduce overseas buyer/tenant inflows

300,000 homes target, higher affordable minima and SDLT surcharges shift market to lettings

Planning targets (300,000 homes pa UK, GLA ~66,000 pa) and rising borough affordable minima (commonly 35%+) alter supply and instructions. SDLT nil-rate £250,000 plus 3%/2% surcharges shift buyer timing toward lettings. Tenancy reforms (4.5m PRS households, ~19% homes), 50+ selective licensing councils and 606,000 net migration (to Jun 2023) change demand, compliance and management costs.

| Factor | Key stat | Implication |

|---|---|---|

| Housing targets | 300,000 UK / 66,000 London | Instruction mix shifts |

| Tax | NRB £250k; 3%/2% | Sales→lettings pressure |

| PRS rules | 4.5m households | Higher management costs |

What is included in the product

Explores how macro-environmental factors uniquely affect Foxtons Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed insights, forward-looking scenarios and practical implications for executives, investors and advisors operating in the UK property market.

A concise, shareable PESTLE snapshot of Foxtons Group that’s visually segmented for quick interpretation, ideal for meetings, presentations, and cross-team alignment; editable notes let users tailor external risk and market-position insights to region or business line.

Economic factors

Interest rates and mortgage availability

Rate cycles (Bank Rate around 5.25% in 2024–25) directly affect affordability, approvals and buyer urgency, hitting first-time buyers—who comprise roughly 40% of purchases—hardest and keeping purchase volumes below pre‑2019 levels.

Lender criteria swing with the cycle, raising fall‑through risk when underwriting tightens; Foxtons mitigates this by pre‑qualifying buyers and matching listings to prevailing affordability bands.

Developer part‑exchange schemes and strengthened broker alliances reduce transaction friction and conversion risk, supporting volumes even in higher‑rate environments.

Inflation, wages, and household confidence

UK inflation eased from a 2022 peak of about 11% to below 4% in 2024, yet real incomes remain squeezed as wage growth lagged core prices, directly limiting rental affordability and purchase budgets. Persistent negative GfK consumer confidence through 2024 lowered viewing-to-offer conversion and increased chain fragility. Foxtons should tie pricing guidance and marketing cadence to sentiment indicators and use flexible fee structures to preserve volume in softer periods.

London housing supply-demand imbalance

Chronic under-supply in London—GLA estimated need ~66,000 homes pa vs delivery ~40,000 pa—supports prices while constraining transaction volumes. Rapid Build-to-Rent growth (UK pipeline ~150,000 units, c.60,000 in London) and rising institutional ownership shift inventory mix. Foxtons can deepen landlord networks and secure new-build instructions from developers. Data-led targeting across 50+ micro-markets pinpoints pockets of liquidity.

Currency movements and foreign capital

Sterling volatility — GBP/USD around 1.27 in mid‑2025 — can both attract price‑sensitive international buyers to prime central London and deter others; Foxtons can time marketing to currency windows while advising clients on hedging and cross‑border payment options that speed settlements. Multilingual agents and international referral partners expand reach into key markets.

- FX exposure: price windows matter

- Hedging/payment fintech: smoother timelines

- Campaigns timed to GBP strength/weakness

- Multilingual agents + referral network

Corporate relocations and employment hubs

Changes in City, tech and media clusters shift Foxtons rental hotspots and sales turnover as London office vacancy hovered near 10% in 2024 while central footfall recovered to roughly 70% of 2019 levels, concentrating demand in South Bank, Canary Wharf and tech corridors.

Hybrid work raised suburban and Zone 3-5 demand; Foxtons can realign branches to transport-linked corridors and new office hubs, using corporate lettings—which accounted for a growing share of agency pipelines in 2024—to stabilise occupancy.

- Vacancy ~10% (2024)

- Central footfall ~70% of 2019 (2024)

- Growth in Zone 3-5 rental demand

- Corporate lettings stabilise occupancy

300,000 homes target, higher affordable minima and SDLT surcharges shift market to lettings

Higher Bank Rate (~5.25% in 2024–25) and tighter lending cut affordability (first‑time buyers ~40% of purchases), damping volumes; chronic London under‑supply (need ~66k pa vs delivery ~40k) supports prices but limits transactions. Build‑to‑Rent pipeline (~150k UK, ~60k London) and sterling swings (GBP/USD ~1.27 mid‑2025) shift buyer mix toward institutions and price‑sensitive internationals.

| Indicator | 2024–25 | Impact |

|---|---|---|

| Bank Rate | ~5.25% | Lower affordability |

| First‑time buyers | ~40% | Volume sensitivity |

| London supply gap | 66k need vs 40k delivery | Price support |

| BTR pipeline | ~150k UK / ~60k London | More institutional stock |

| GBP/USD | ~1.27 | Shifts intl demand |

Full Version Awaits

Foxtons Group PESTLE Analysis

This Foxtons Group PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the business. The content and structure shown in the preview is the same document you’ll download after payment, fully formatted and ready to use. It’s the exact, finished file you’ll own immediately after checkout.