Fresenius Medical Care Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

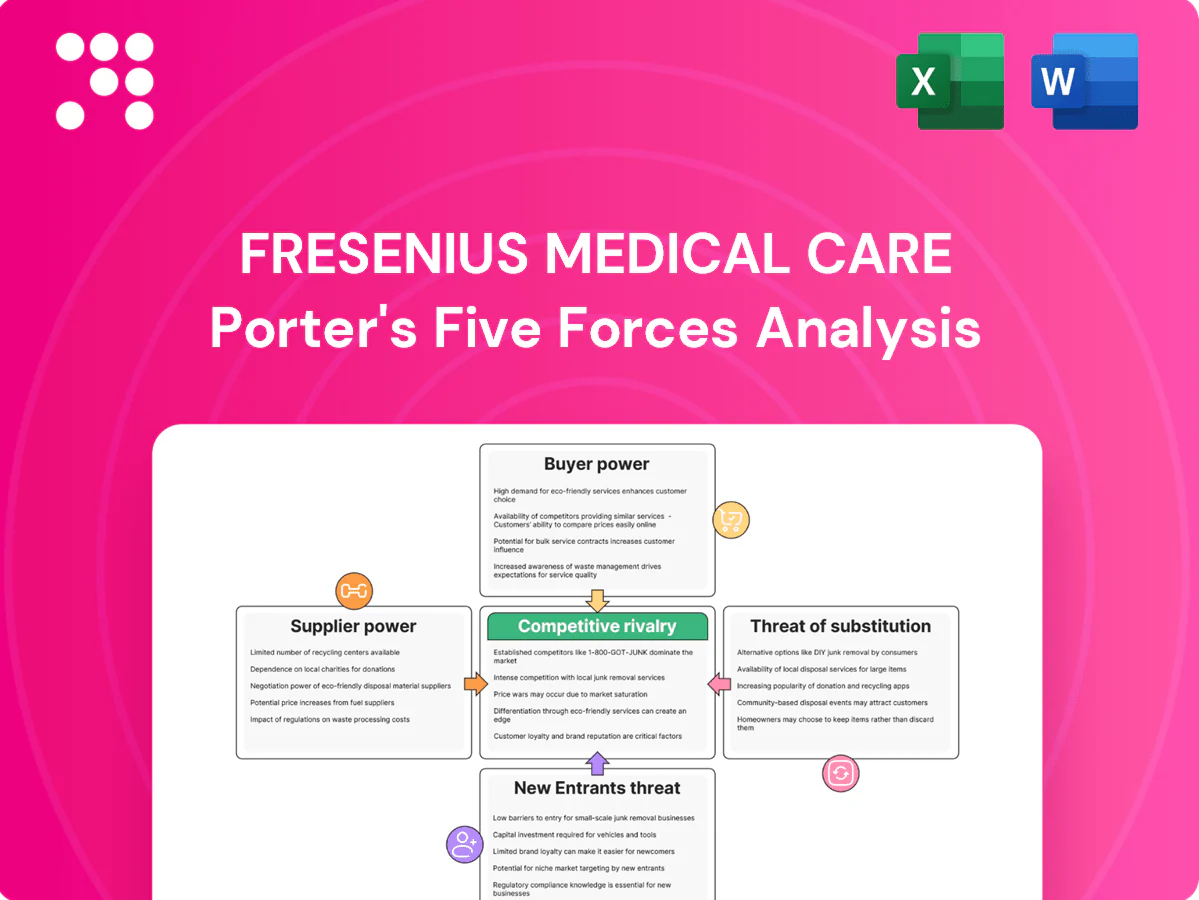

Fresenius Medical Care faces moderate supplier power, high buyer sensitivity, intense rival rivalry, limited threat of new entrants, and rising substitute and tech risks; these forces shape pricing, margin pressure, and strategic focus. This snapshot highlights where management must prioritize innovation and cost control. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fresenius Medical Care’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

High-spec membranes, medical-grade polymers and precision components come from a limited set of qualified suppliers, increasing supplier leverage due to quality and regulatory barriers. Fresenius Medical Care operates about 4,000 clinics and treats roughly 345,000 patients, giving scale that tempers pricing power via vendor qualification programs. Dual-sourcing and long-term contracts further mitigate disruption risk.

Vertical integration offset

Fresenius Medical Care vertically integrates by manufacturing many dialyzers, machines and disposables in-house, capturing margin and reducing reliance on external suppliers; as of 2024 it serves roughly 345,000 patients and employs about 118,000 worldwide, giving scale to internal production. This backward integration strengthens negotiation leverage on remaining third-party inputs. However, suppliers of specialized subcomponents and outsourced maintenance services retain bargaining power.

Regulatory switching costs

Revalidating alternate suppliers for Class II/III devices is costly and time-consuming in a regulated environment; GMP and FDA QSR (21 CFR 820) requirements plus ISO 13485:2016 and EU MDR (effective 26 May 2021) raise qualification hurdles. These compliance frictions elevate supplier stickiness. Fresenius Medical Care employs standardized platforms and centralized change-control processes to streamline transitions but cannot eliminate regulatory requalification time and cost.

Commodity and logistics exposure

Resins, plastics and energy are key cost drivers for Fresenius Medical Care; 2024 saw renewed price volatility and periodic transport bottlenecks that can tighten sterilization and freight capacity, temporarily strengthening supplier leverage. The company uses hedging, manufacturing footprint diversification and multi-year freight contracts to limit pass-through, yet sudden geopolitical or logistic shocks in 2024 still compressed margins.

- Resins/plastics exposure: input-cost sensitivity

- Energy & freight: capacity-driven price spikes

- Mitigants: hedging, footprint & long-term freight deals

- Residual risk: 2024 shocks can transmit to margins

Technology and software dependencies

Embedded software, sensors and connectivity modules often come from specialized vendors, and strict cybersecurity and interoperability standards in 2024 narrow options; Fresenius leverages scale across ~4,000 clinics and ~345,000 patients to negotiate co‑development and volume discounts but still faces switching friction and certification delays. Lifecycle support commitments can entrench supplier influence over multi‑year device cycles.

- Vendor concentration: specialized suppliers dominate

- Scale leverage: ~4,000 clinics, ~345,000 patients (2024)

- Risk: switching friction, long support SLAs

- Mitigation: co‑development and volume negotiation

Supplier leverage persists despite ~4,000 clinics and vertical manufacturing

Supplier power is elevated by specialized membranes, polymers and software vendors with high qualification barriers; Fresenius Medical Care’s scale (~4,000 clinics, ~345,000 patients in 2024) and vertical manufacturing reduce but do not eliminate leverage. Regulatory requalification and 2024 input-price shocks sustain residual supplier influence.

| Metric | 2024 value | Impact |

|---|---|---|

| Clinics | ~4,000 | Negotiation leverage |

| Patients | ~345,000 | Volume discounts |

| Employees | ~118,000 | In-house production |

What is included in the product

Tailored Porter's Five Forces analysis for Fresenius Medical Care uncovering competitive intensity, buyer/supplier power, substitutes and entry barriers, identifying disruptive threats and strategic levers to protect market share.

One-sheet Porter's Five Forces for Fresenius Medical Care—quickly spot regulatory, supplier and competitor pressures and relieve decision-making friction; includes customizable pressure levels and an instant spider chart ready for decks or integration into Excel dashboards.

Customers Bargaining Power

Consolidated purchasers

Consolidated purchasers—GPOs, integrated health systems and large dialysis chains—run competitive tenders that leverage scale to push aggressive pricing and stricter service-level demands. In response Fresenius Medical Care bundles dialysis services, supplies and care-management and highlights outcomes data to win contracts; Fresenius reported revenue of €21.9 billion in 2024, and multi-year framework agreements partially stabilize volume and cash flow.

Payer reimbursement pressure

Public payers and insurers, led by Medicare which covers roughly 75–80% of U.S. dialysis patients, set reimbursement ceilings that cap Fresenius Medical Care’s economic surplus. Annual rate updates and modality incentives drive shifts toward home dialysis and PD, altering acquisition volumes and pricing leverage. Reimbursement pressure cascades to equipment and consumable margins, while QIP/value‑based contracts (payment adjustments up to ~2%) reward cost‑effective, high‑quality care.

Switching and compatibility costs

Installed bases—Fresenius Medical Care's >4,000 clinics serving ~345,000 patients in 2024—lock buyers into proprietary cartridges, disposables and software ecosystems, raising tangible switching and compatibility costs. Clinical training, validation and workflow integration further elevate costs and reduce buyer leverage even when tenders occur. Incremental interoperability advances can modestly lower friction over time.

Global tenders and price transparency

Global tenders and reference pricing increase product comparability and pressure margins; in 2024 cross-border benchmarks are central to procurement decisions. Buyers leverage these benchmarks to extract concessions while Fresenius, treating roughly 345,000 dialysis patients worldwide in 2024, uses scale to negotiate. Fresenius defends prices through uptime, service reliability, clinical support and total cost-of-care arguments that downplay unit price.

- Comparability: tenders + reference pricing

- Bargaining: cross-market benchmarks used

- Differentiation: uptime, clinical support, TCO

Home therapy and patient voice

Growth in home hemodialysis and peritoneal dialysis (home therapies penetration ~10–15% in many developed markets by 2023) elevates patient preference; education, training and remote monitoring increasingly drive modality choice. Payers still set reimbursement, but patient satisfaction shapes adoption and referral patterns. Superior user experience lowers buyer price pressure by increasing retention.

- Home penetration ~10–15% (2023)

- Education/training & remote monitoring = key decision factors

- High patient satisfaction reduces price sensitivity

Payer consolidation pressures prices; Medicare 75-80% dominance shifts dialysis care

Consolidated purchasers and payers (Medicare covers ~75–80% of US dialysis) exert strong price leverage; Fresenius counters with bundled services and outcomes selling (revenue €21.9bn, ~345,000 patients, >4,000 clinics in 2024). Installed base and training raise switching costs, while global tenders and rising home therapy (10–15% penetration 2023) shift modality and reimbursement pressure.

| Metric | 2023/24 |

|---|---|

| Revenue | €21.9bn (2024) |

| Patients | ~345,000 (2024) |

| Clinics | >4,000 (2024) |

| US Medicare | 75–80% of dialysis pts |

| Home penetration | 10–15% (2023) |

Preview the Actual Deliverable

Fresenius Medical Care Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Fresenius Medical Care you’ll receive after purchase—no placeholders or mockups. The full document is professionally written, fully formatted and ready to download instantly. You’ll get this identical file immediately after payment for immediate use in analysis or presentation.

Go Beyond the Preview—Access the Full Strategic Report

Fresenius Medical Care faces moderate supplier power, high buyer sensitivity, intense rival rivalry, limited threat of new entrants, and rising substitute and tech risks; these forces shape pricing, margin pressure, and strategic focus. This snapshot highlights where management must prioritize innovation and cost control. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fresenius Medical Care’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

High-spec membranes, medical-grade polymers and precision components come from a limited set of qualified suppliers, increasing supplier leverage due to quality and regulatory barriers. Fresenius Medical Care operates about 4,000 clinics and treats roughly 345,000 patients, giving scale that tempers pricing power via vendor qualification programs. Dual-sourcing and long-term contracts further mitigate disruption risk.

Vertical integration offset

Fresenius Medical Care vertically integrates by manufacturing many dialyzers, machines and disposables in-house, capturing margin and reducing reliance on external suppliers; as of 2024 it serves roughly 345,000 patients and employs about 118,000 worldwide, giving scale to internal production. This backward integration strengthens negotiation leverage on remaining third-party inputs. However, suppliers of specialized subcomponents and outsourced maintenance services retain bargaining power.

Regulatory switching costs

Revalidating alternate suppliers for Class II/III devices is costly and time-consuming in a regulated environment; GMP and FDA QSR (21 CFR 820) requirements plus ISO 13485:2016 and EU MDR (effective 26 May 2021) raise qualification hurdles. These compliance frictions elevate supplier stickiness. Fresenius Medical Care employs standardized platforms and centralized change-control processes to streamline transitions but cannot eliminate regulatory requalification time and cost.

Commodity and logistics exposure

Resins, plastics and energy are key cost drivers for Fresenius Medical Care; 2024 saw renewed price volatility and periodic transport bottlenecks that can tighten sterilization and freight capacity, temporarily strengthening supplier leverage. The company uses hedging, manufacturing footprint diversification and multi-year freight contracts to limit pass-through, yet sudden geopolitical or logistic shocks in 2024 still compressed margins.

- Resins/plastics exposure: input-cost sensitivity

- Energy & freight: capacity-driven price spikes

- Mitigants: hedging, footprint & long-term freight deals

- Residual risk: 2024 shocks can transmit to margins

Technology and software dependencies

Embedded software, sensors and connectivity modules often come from specialized vendors, and strict cybersecurity and interoperability standards in 2024 narrow options; Fresenius leverages scale across ~4,000 clinics and ~345,000 patients to negotiate co‑development and volume discounts but still faces switching friction and certification delays. Lifecycle support commitments can entrench supplier influence over multi‑year device cycles.

- Vendor concentration: specialized suppliers dominate

- Scale leverage: ~4,000 clinics, ~345,000 patients (2024)

- Risk: switching friction, long support SLAs

- Mitigation: co‑development and volume negotiation

Supplier leverage persists despite ~4,000 clinics and vertical manufacturing

Supplier power is elevated by specialized membranes, polymers and software vendors with high qualification barriers; Fresenius Medical Care’s scale (~4,000 clinics, ~345,000 patients in 2024) and vertical manufacturing reduce but do not eliminate leverage. Regulatory requalification and 2024 input-price shocks sustain residual supplier influence.

| Metric | 2024 value | Impact |

|---|---|---|

| Clinics | ~4,000 | Negotiation leverage |

| Patients | ~345,000 | Volume discounts |

| Employees | ~118,000 | In-house production |

What is included in the product

Tailored Porter's Five Forces analysis for Fresenius Medical Care uncovering competitive intensity, buyer/supplier power, substitutes and entry barriers, identifying disruptive threats and strategic levers to protect market share.

One-sheet Porter's Five Forces for Fresenius Medical Care—quickly spot regulatory, supplier and competitor pressures and relieve decision-making friction; includes customizable pressure levels and an instant spider chart ready for decks or integration into Excel dashboards.

Customers Bargaining Power

Consolidated purchasers

Consolidated purchasers—GPOs, integrated health systems and large dialysis chains—run competitive tenders that leverage scale to push aggressive pricing and stricter service-level demands. In response Fresenius Medical Care bundles dialysis services, supplies and care-management and highlights outcomes data to win contracts; Fresenius reported revenue of €21.9 billion in 2024, and multi-year framework agreements partially stabilize volume and cash flow.

Payer reimbursement pressure

Public payers and insurers, led by Medicare which covers roughly 75–80% of U.S. dialysis patients, set reimbursement ceilings that cap Fresenius Medical Care’s economic surplus. Annual rate updates and modality incentives drive shifts toward home dialysis and PD, altering acquisition volumes and pricing leverage. Reimbursement pressure cascades to equipment and consumable margins, while QIP/value‑based contracts (payment adjustments up to ~2%) reward cost‑effective, high‑quality care.

Switching and compatibility costs

Installed bases—Fresenius Medical Care's >4,000 clinics serving ~345,000 patients in 2024—lock buyers into proprietary cartridges, disposables and software ecosystems, raising tangible switching and compatibility costs. Clinical training, validation and workflow integration further elevate costs and reduce buyer leverage even when tenders occur. Incremental interoperability advances can modestly lower friction over time.

Global tenders and price transparency

Global tenders and reference pricing increase product comparability and pressure margins; in 2024 cross-border benchmarks are central to procurement decisions. Buyers leverage these benchmarks to extract concessions while Fresenius, treating roughly 345,000 dialysis patients worldwide in 2024, uses scale to negotiate. Fresenius defends prices through uptime, service reliability, clinical support and total cost-of-care arguments that downplay unit price.

- Comparability: tenders + reference pricing

- Bargaining: cross-market benchmarks used

- Differentiation: uptime, clinical support, TCO

Home therapy and patient voice

Growth in home hemodialysis and peritoneal dialysis (home therapies penetration ~10–15% in many developed markets by 2023) elevates patient preference; education, training and remote monitoring increasingly drive modality choice. Payers still set reimbursement, but patient satisfaction shapes adoption and referral patterns. Superior user experience lowers buyer price pressure by increasing retention.

- Home penetration ~10–15% (2023)

- Education/training & remote monitoring = key decision factors

- High patient satisfaction reduces price sensitivity

Payer consolidation pressures prices; Medicare 75-80% dominance shifts dialysis care

Consolidated purchasers and payers (Medicare covers ~75–80% of US dialysis) exert strong price leverage; Fresenius counters with bundled services and outcomes selling (revenue €21.9bn, ~345,000 patients, >4,000 clinics in 2024). Installed base and training raise switching costs, while global tenders and rising home therapy (10–15% penetration 2023) shift modality and reimbursement pressure.

| Metric | 2023/24 |

|---|---|

| Revenue | €21.9bn (2024) |

| Patients | ~345,000 (2024) |

| Clinics | >4,000 (2024) |

| US Medicare | 75–80% of dialysis pts |

| Home penetration | 10–15% (2023) |

Preview the Actual Deliverable

Fresenius Medical Care Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Fresenius Medical Care you’ll receive after purchase—no placeholders or mockups. The full document is professionally written, fully formatted and ready to download instantly. You’ll get this identical file immediately after payment for immediate use in analysis or presentation.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Fresenius Medical Care faces moderate supplier power, high buyer sensitivity, intense rival rivalry, limited threat of new entrants, and rising substitute and tech risks; these forces shape pricing, margin pressure, and strategic focus. This snapshot highlights where management must prioritize innovation and cost control. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Fresenius Medical Care’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs

High-spec membranes, medical-grade polymers and precision components come from a limited set of qualified suppliers, increasing supplier leverage due to quality and regulatory barriers. Fresenius Medical Care operates about 4,000 clinics and treats roughly 345,000 patients, giving scale that tempers pricing power via vendor qualification programs. Dual-sourcing and long-term contracts further mitigate disruption risk.

Vertical integration offset

Fresenius Medical Care vertically integrates by manufacturing many dialyzers, machines and disposables in-house, capturing margin and reducing reliance on external suppliers; as of 2024 it serves roughly 345,000 patients and employs about 118,000 worldwide, giving scale to internal production. This backward integration strengthens negotiation leverage on remaining third-party inputs. However, suppliers of specialized subcomponents and outsourced maintenance services retain bargaining power.

Regulatory switching costs

Revalidating alternate suppliers for Class II/III devices is costly and time-consuming in a regulated environment; GMP and FDA QSR (21 CFR 820) requirements plus ISO 13485:2016 and EU MDR (effective 26 May 2021) raise qualification hurdles. These compliance frictions elevate supplier stickiness. Fresenius Medical Care employs standardized platforms and centralized change-control processes to streamline transitions but cannot eliminate regulatory requalification time and cost.

Commodity and logistics exposure

Resins, plastics and energy are key cost drivers for Fresenius Medical Care; 2024 saw renewed price volatility and periodic transport bottlenecks that can tighten sterilization and freight capacity, temporarily strengthening supplier leverage. The company uses hedging, manufacturing footprint diversification and multi-year freight contracts to limit pass-through, yet sudden geopolitical or logistic shocks in 2024 still compressed margins.

- Resins/plastics exposure: input-cost sensitivity

- Energy & freight: capacity-driven price spikes

- Mitigants: hedging, footprint & long-term freight deals

- Residual risk: 2024 shocks can transmit to margins

Technology and software dependencies

Embedded software, sensors and connectivity modules often come from specialized vendors, and strict cybersecurity and interoperability standards in 2024 narrow options; Fresenius leverages scale across ~4,000 clinics and ~345,000 patients to negotiate co‑development and volume discounts but still faces switching friction and certification delays. Lifecycle support commitments can entrench supplier influence over multi‑year device cycles.

- Vendor concentration: specialized suppliers dominate

- Scale leverage: ~4,000 clinics, ~345,000 patients (2024)

- Risk: switching friction, long support SLAs

- Mitigation: co‑development and volume negotiation

Supplier leverage persists despite ~4,000 clinics and vertical manufacturing

Supplier power is elevated by specialized membranes, polymers and software vendors with high qualification barriers; Fresenius Medical Care’s scale (~4,000 clinics, ~345,000 patients in 2024) and vertical manufacturing reduce but do not eliminate leverage. Regulatory requalification and 2024 input-price shocks sustain residual supplier influence.

| Metric | 2024 value | Impact |

|---|---|---|

| Clinics | ~4,000 | Negotiation leverage |

| Patients | ~345,000 | Volume discounts |

| Employees | ~118,000 | In-house production |

What is included in the product

Tailored Porter's Five Forces analysis for Fresenius Medical Care uncovering competitive intensity, buyer/supplier power, substitutes and entry barriers, identifying disruptive threats and strategic levers to protect market share.

One-sheet Porter's Five Forces for Fresenius Medical Care—quickly spot regulatory, supplier and competitor pressures and relieve decision-making friction; includes customizable pressure levels and an instant spider chart ready for decks or integration into Excel dashboards.

Customers Bargaining Power

Consolidated purchasers

Consolidated purchasers—GPOs, integrated health systems and large dialysis chains—run competitive tenders that leverage scale to push aggressive pricing and stricter service-level demands. In response Fresenius Medical Care bundles dialysis services, supplies and care-management and highlights outcomes data to win contracts; Fresenius reported revenue of €21.9 billion in 2024, and multi-year framework agreements partially stabilize volume and cash flow.

Payer reimbursement pressure

Public payers and insurers, led by Medicare which covers roughly 75–80% of U.S. dialysis patients, set reimbursement ceilings that cap Fresenius Medical Care’s economic surplus. Annual rate updates and modality incentives drive shifts toward home dialysis and PD, altering acquisition volumes and pricing leverage. Reimbursement pressure cascades to equipment and consumable margins, while QIP/value‑based contracts (payment adjustments up to ~2%) reward cost‑effective, high‑quality care.

Switching and compatibility costs

Installed bases—Fresenius Medical Care's >4,000 clinics serving ~345,000 patients in 2024—lock buyers into proprietary cartridges, disposables and software ecosystems, raising tangible switching and compatibility costs. Clinical training, validation and workflow integration further elevate costs and reduce buyer leverage even when tenders occur. Incremental interoperability advances can modestly lower friction over time.

Global tenders and price transparency

Global tenders and reference pricing increase product comparability and pressure margins; in 2024 cross-border benchmarks are central to procurement decisions. Buyers leverage these benchmarks to extract concessions while Fresenius, treating roughly 345,000 dialysis patients worldwide in 2024, uses scale to negotiate. Fresenius defends prices through uptime, service reliability, clinical support and total cost-of-care arguments that downplay unit price.

- Comparability: tenders + reference pricing

- Bargaining: cross-market benchmarks used

- Differentiation: uptime, clinical support, TCO

Home therapy and patient voice

Growth in home hemodialysis and peritoneal dialysis (home therapies penetration ~10–15% in many developed markets by 2023) elevates patient preference; education, training and remote monitoring increasingly drive modality choice. Payers still set reimbursement, but patient satisfaction shapes adoption and referral patterns. Superior user experience lowers buyer price pressure by increasing retention.

- Home penetration ~10–15% (2023)

- Education/training & remote monitoring = key decision factors

- High patient satisfaction reduces price sensitivity

Payer consolidation pressures prices; Medicare 75-80% dominance shifts dialysis care

Consolidated purchasers and payers (Medicare covers ~75–80% of US dialysis) exert strong price leverage; Fresenius counters with bundled services and outcomes selling (revenue €21.9bn, ~345,000 patients, >4,000 clinics in 2024). Installed base and training raise switching costs, while global tenders and rising home therapy (10–15% penetration 2023) shift modality and reimbursement pressure.

| Metric | 2023/24 |

|---|---|

| Revenue | €21.9bn (2024) |

| Patients | ~345,000 (2024) |

| Clinics | >4,000 (2024) |

| US Medicare | 75–80% of dialysis pts |

| Home penetration | 10–15% (2023) |

Preview the Actual Deliverable

Fresenius Medical Care Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Fresenius Medical Care you’ll receive after purchase—no placeholders or mockups. The full document is professionally written, fully formatted and ready to download instantly. You’ll get this identical file immediately after payment for immediate use in analysis or presentation.