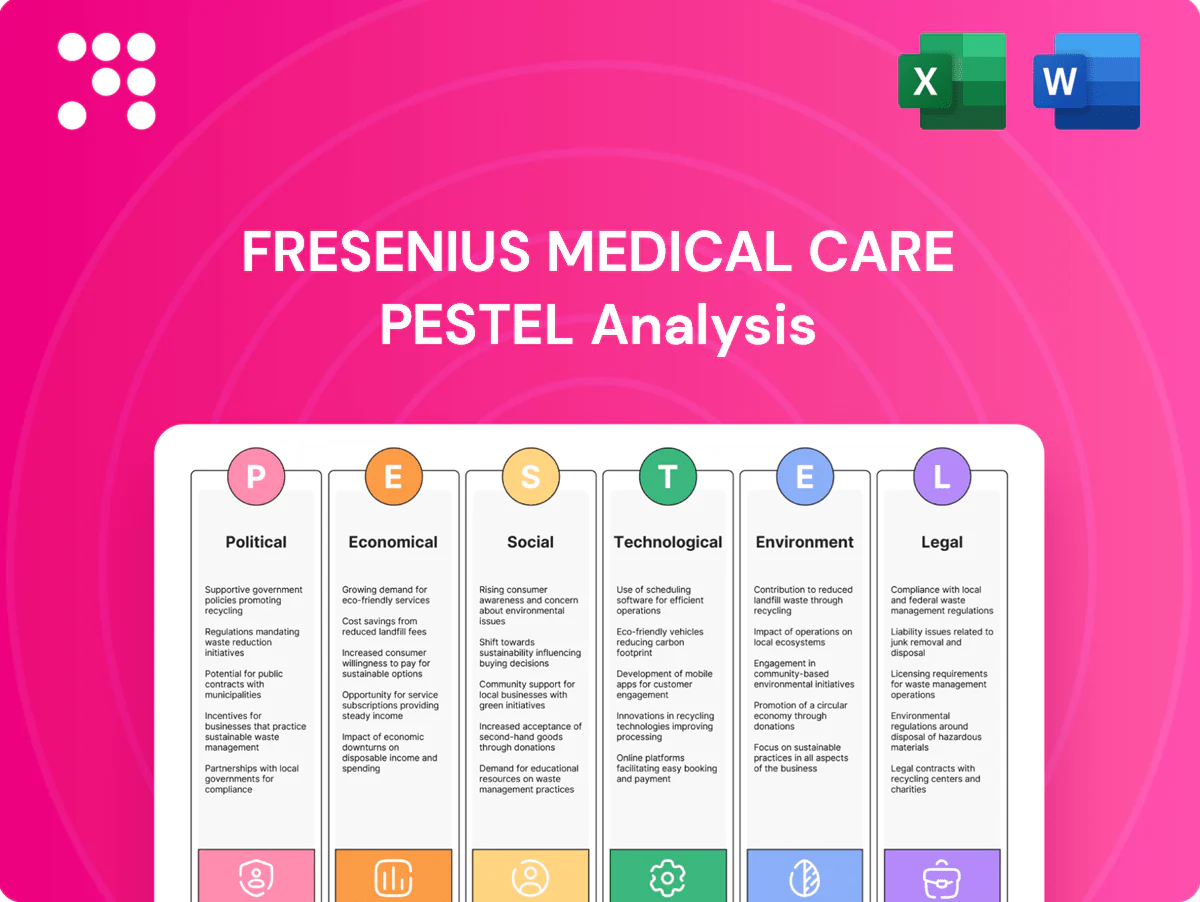

Fresenius Medical Care PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Fresenius Medical Care highlights how regulatory shifts, aging populations, reimbursement pressures, technological innovation, and sustainability trends are reshaping its competitive landscape. We translate these external forces into strategic risks and opportunities you can act on. Purchase the full PESTLE for detailed, ready-to-use insights and forecasts to inform investment or strategic decisions.

Political factors

Reimbursement policy volatility

Government reimbursement programs, especially the U.S. ESRD system, drive most dialysis revenues—Medicare accounted for roughly the majority of U.S. dialysis payments and Medicare ESRD spending was about $49.6 billion in 2022. Shifts in bundled payments, value-based incentives and CMS initiatives to expand home dialysis can compress or expand FMC margins. FMC must engage in advocacy, adjust contracting and run scenario plans for rate cuts or quality-linked bonuses.

Public healthcare spending priorities

National budget allocations to chronic care and renal programs directly shape capacity and expansion: Fresenius Medical Care reported roughly €21 billion revenue in 2024 and serves about 345,000 dialysis patients, so shifts in public funding affect clinic openings and reimbursement rates. Fiscal tightening can delay new clinics, while targeted chronic-disease or home-dialysis incentives accelerate adoption. FMC must align offerings to prevention/home therapies and diversify payer exposure to reduce country-specific budget risk.

Trade and geopolitical supply risks

Tariffs, export controls and geopolitical tensions threaten access to membranes, resins and components, increasing lead times by months and raising costs for Fresenius Medical Care, which reported €20.6bn revenue in 2023; policies in China, the EU and the U.S. disproportionately affect supply chains. FMC must advance dual/multi-sourcing, localized manufacturing, strategic inventories and nearshoring to maintain resilience and reduce disruption risk.

Public–private partnerships in care delivery

Governments increasingly outsource dialysis to private operators, and Fresenius Medical Care, active in over 120 countries and serving ~345,000 patients (2024), competes on tender dynamics, local-partner and national-content rules that materially affect win rates. FMC can leverage superior clinical outcomes and cost-efficiency to secure PPPs, while transparent outcomes reporting bolsters contract bids and renewals.

- Tender dynamics: local-partner and national-content rules

- Competitive edge: clinical outcomes + cost efficiency

- Evidence: ~345,000 patients served (2024)

- Renewals: transparent outcomes reporting strengthens bids

Health policy push for home-based care

Many jurisdictions push home therapies to cut system costs and boost patient autonomy, with studies showing up to 30% lower annual dialysis costs for home modalities versus in-center care; incentives and training mandates are accelerating peritoneal and home hemodialysis uptake. Fresenius Medical Care should scale patient education, supply logistics and tele-support to capture market share, while policy-aligned pilots can unlock preferential funding.

- Reduce cost: up to 30% lower per-patient dialysis cost

- Growth driver: mandates/incentives raise home uptake

- FMC focus: education, logistics, tele-support

- Strategy: policy pilots to access preferential funding

Medicare ESRD $49.6bn and value-based pay drive shift to home dialysis (≈30% lower cost)

Government reimbursement (Medicare ESRD ~$49.6bn in 2022) and bundled/value-based payment shifts drive FMC margins; policy-driven home-dialysis expansion (≈30% lower annual cost) reshapes service mix. Public budgets and tender/local-content rules affect clinic openings and PPP wins; supply-chain controls raise component lead times. FMC: diversify payers, localize supply, scale home-care and outcomes reporting.

| Metric | Value | Political Impact |

|---|---|---|

| Revenue (2024) | ≈€21bn | Scale affects negotiation power |

| Patients (2024) | ≈345,000 | Service demand shapes policy influence |

| Medicare ESRD (2022) | $49.6bn | Reimbursement risk/benchmark |

| Home dialysis cost delta | ≈-30% | Incentive for policy shifts |

What is included in the product

Explores how macro-environmental forces uniquely affect Fresenius Medical Care across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context and forward-looking insights to help executives and investors identify risks, opportunities and actionable strategies.

A clean, summarized Fresenius Medical Care PESTLE that is visually segmented by category, letting teams quickly interpret regulatory, market and technological risks and drop concise bullets into presentations for fast alignment.

Economic factors

Inflation and input cost pressures

Rising costs for plastics, dialyzer fibers, energy and logistics have compressed Fresenius Medical Care product margins, while contract pricing lags delay pass-through to payers and clinics. FMC must deploy cost engineering, hedging and disciplined price escalators to protect margins. Lean operations and automation are critical to offset wage inflation and sustain profitability.

Foreign exchange and global revenue mix

Fresenius Medical Care reported €20.7bn revenue in 2024, with a multi-currency footprint that exposes earnings to FX volatility as revenues and costs are denominated across USD, EUR and emerging-market currencies. Dollar strength in 2024 depressed translated euro earnings while easing some dollar-priced input costs. Natural hedging from local cost bases and use of financial derivatives trimmed translation swings. Pricing strategies must embed local-currency risk and frequent adjustments.

Interest rates and capital intensity

Clinic networks, equipment fleets and inventories require significant capital for Fresenius Medical Care, which reported group sales of about €20.9 billion in 2023; higher interest rates—US Fed funds around 5.25–5.50% in 2024–2025—raise financing costs and hurdle rates for new centers. FMC should prioritize ROI-positive refurbishments and asset-light models where feasible. Sale–leaseback transactions or partnerships can optimize capital structure and preserve liquidity.

Payer mix and pricing pressure

Shifts from commercial to public payers compress margins in mature markets, with Medicare covering roughly 80% of US dialysis patients, increasing reimbursement pressure. Managed care and group purchasing organizations intensify price negotiations, forcing Fresenius Medical Care to demonstrate total cost-of-care reductions and better outcomes to defend pricing. Value-based contracts offer a path to align incentives and stabilize revenue.

- Payer shift: Medicare ~80% of US dialysis patients

- Pricing pressure: stronger managed care/GPO leverage

- Defense: show lower total cost-of-care + outcomes

- Solution: expand value-based contracts to stabilize revenue

Emerging market demand growth

Rising CKD—estimated at about 850 million people globally—plus expanding insurance and primary care in emerging markets is driving dialysis volume growth, with EMs representing a key growth vector for Fresenius Medical Care. Affordability constraints push tiered product lines and pay‑as‑you‑go service models; local manufacturing and distribution lower unit costs and improve success in public tenders, while clinician training programs increase utilization and patient retention.

- CKD burden ~850 million globally

- Tiered products + pay‑per‑use for affordability

- Local manufacturing reduces tender unit costs

- Training builds clinician capacity and stickiness

Medicare ESRD $49.6bn and value-based pay drive shift to home dialysis (≈30% lower cost)

Rising input, energy and logistics costs compress margins; cost engineering, hedging and price escalators are essential. FMC reported €20.7bn revenue in 2024 with material FX exposure as USD/EUR moves affect translated earnings. Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise financing costs for clinics; Medicare covers ~80% of US dialysis patients, pressuring pricing. CKD ~850m drives EM volume growth but affordability limits.

| Metric | Value |

|---|---|

| 2024 Revenue | €20.7bn |

| Global CKD | ~850m |

| US Medicare share | ~80% |

| Fed funds (2024–25) | 5.25–5.50% |

Preview the Actual Deliverable

Fresenius Medical Care PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Fresenius Medical Care you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the final, professionally structured document.

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Fresenius Medical Care highlights how regulatory shifts, aging populations, reimbursement pressures, technological innovation, and sustainability trends are reshaping its competitive landscape. We translate these external forces into strategic risks and opportunities you can act on. Purchase the full PESTLE for detailed, ready-to-use insights and forecasts to inform investment or strategic decisions.

Political factors

Reimbursement policy volatility

Government reimbursement programs, especially the U.S. ESRD system, drive most dialysis revenues—Medicare accounted for roughly the majority of U.S. dialysis payments and Medicare ESRD spending was about $49.6 billion in 2022. Shifts in bundled payments, value-based incentives and CMS initiatives to expand home dialysis can compress or expand FMC margins. FMC must engage in advocacy, adjust contracting and run scenario plans for rate cuts or quality-linked bonuses.

Public healthcare spending priorities

National budget allocations to chronic care and renal programs directly shape capacity and expansion: Fresenius Medical Care reported roughly €21 billion revenue in 2024 and serves about 345,000 dialysis patients, so shifts in public funding affect clinic openings and reimbursement rates. Fiscal tightening can delay new clinics, while targeted chronic-disease or home-dialysis incentives accelerate adoption. FMC must align offerings to prevention/home therapies and diversify payer exposure to reduce country-specific budget risk.

Trade and geopolitical supply risks

Tariffs, export controls and geopolitical tensions threaten access to membranes, resins and components, increasing lead times by months and raising costs for Fresenius Medical Care, which reported €20.6bn revenue in 2023; policies in China, the EU and the U.S. disproportionately affect supply chains. FMC must advance dual/multi-sourcing, localized manufacturing, strategic inventories and nearshoring to maintain resilience and reduce disruption risk.

Public–private partnerships in care delivery

Governments increasingly outsource dialysis to private operators, and Fresenius Medical Care, active in over 120 countries and serving ~345,000 patients (2024), competes on tender dynamics, local-partner and national-content rules that materially affect win rates. FMC can leverage superior clinical outcomes and cost-efficiency to secure PPPs, while transparent outcomes reporting bolsters contract bids and renewals.

- Tender dynamics: local-partner and national-content rules

- Competitive edge: clinical outcomes + cost efficiency

- Evidence: ~345,000 patients served (2024)

- Renewals: transparent outcomes reporting strengthens bids

Health policy push for home-based care

Many jurisdictions push home therapies to cut system costs and boost patient autonomy, with studies showing up to 30% lower annual dialysis costs for home modalities versus in-center care; incentives and training mandates are accelerating peritoneal and home hemodialysis uptake. Fresenius Medical Care should scale patient education, supply logistics and tele-support to capture market share, while policy-aligned pilots can unlock preferential funding.

- Reduce cost: up to 30% lower per-patient dialysis cost

- Growth driver: mandates/incentives raise home uptake

- FMC focus: education, logistics, tele-support

- Strategy: policy pilots to access preferential funding

Medicare ESRD $49.6bn and value-based pay drive shift to home dialysis (≈30% lower cost)

Government reimbursement (Medicare ESRD ~$49.6bn in 2022) and bundled/value-based payment shifts drive FMC margins; policy-driven home-dialysis expansion (≈30% lower annual cost) reshapes service mix. Public budgets and tender/local-content rules affect clinic openings and PPP wins; supply-chain controls raise component lead times. FMC: diversify payers, localize supply, scale home-care and outcomes reporting.

| Metric | Value | Political Impact |

|---|---|---|

| Revenue (2024) | ≈€21bn | Scale affects negotiation power |

| Patients (2024) | ≈345,000 | Service demand shapes policy influence |

| Medicare ESRD (2022) | $49.6bn | Reimbursement risk/benchmark |

| Home dialysis cost delta | ≈-30% | Incentive for policy shifts |

What is included in the product

Explores how macro-environmental forces uniquely affect Fresenius Medical Care across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context and forward-looking insights to help executives and investors identify risks, opportunities and actionable strategies.

A clean, summarized Fresenius Medical Care PESTLE that is visually segmented by category, letting teams quickly interpret regulatory, market and technological risks and drop concise bullets into presentations for fast alignment.

Economic factors

Inflation and input cost pressures

Rising costs for plastics, dialyzer fibers, energy and logistics have compressed Fresenius Medical Care product margins, while contract pricing lags delay pass-through to payers and clinics. FMC must deploy cost engineering, hedging and disciplined price escalators to protect margins. Lean operations and automation are critical to offset wage inflation and sustain profitability.

Foreign exchange and global revenue mix

Fresenius Medical Care reported €20.7bn revenue in 2024, with a multi-currency footprint that exposes earnings to FX volatility as revenues and costs are denominated across USD, EUR and emerging-market currencies. Dollar strength in 2024 depressed translated euro earnings while easing some dollar-priced input costs. Natural hedging from local cost bases and use of financial derivatives trimmed translation swings. Pricing strategies must embed local-currency risk and frequent adjustments.

Interest rates and capital intensity

Clinic networks, equipment fleets and inventories require significant capital for Fresenius Medical Care, which reported group sales of about €20.9 billion in 2023; higher interest rates—US Fed funds around 5.25–5.50% in 2024–2025—raise financing costs and hurdle rates for new centers. FMC should prioritize ROI-positive refurbishments and asset-light models where feasible. Sale–leaseback transactions or partnerships can optimize capital structure and preserve liquidity.

Payer mix and pricing pressure

Shifts from commercial to public payers compress margins in mature markets, with Medicare covering roughly 80% of US dialysis patients, increasing reimbursement pressure. Managed care and group purchasing organizations intensify price negotiations, forcing Fresenius Medical Care to demonstrate total cost-of-care reductions and better outcomes to defend pricing. Value-based contracts offer a path to align incentives and stabilize revenue.

- Payer shift: Medicare ~80% of US dialysis patients

- Pricing pressure: stronger managed care/GPO leverage

- Defense: show lower total cost-of-care + outcomes

- Solution: expand value-based contracts to stabilize revenue

Emerging market demand growth

Rising CKD—estimated at about 850 million people globally—plus expanding insurance and primary care in emerging markets is driving dialysis volume growth, with EMs representing a key growth vector for Fresenius Medical Care. Affordability constraints push tiered product lines and pay‑as‑you‑go service models; local manufacturing and distribution lower unit costs and improve success in public tenders, while clinician training programs increase utilization and patient retention.

- CKD burden ~850 million globally

- Tiered products + pay‑per‑use for affordability

- Local manufacturing reduces tender unit costs

- Training builds clinician capacity and stickiness

Medicare ESRD $49.6bn and value-based pay drive shift to home dialysis (≈30% lower cost)

Rising input, energy and logistics costs compress margins; cost engineering, hedging and price escalators are essential. FMC reported €20.7bn revenue in 2024 with material FX exposure as USD/EUR moves affect translated earnings. Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise financing costs for clinics; Medicare covers ~80% of US dialysis patients, pressuring pricing. CKD ~850m drives EM volume growth but affordability limits.

| Metric | Value |

|---|---|

| 2024 Revenue | €20.7bn |

| Global CKD | ~850m |

| US Medicare share | ~80% |

| Fed funds (2024–25) | 5.25–5.50% |

Preview the Actual Deliverable

Fresenius Medical Care PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Fresenius Medical Care you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the final, professionally structured document.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Our PESTLE analysis of Fresenius Medical Care highlights how regulatory shifts, aging populations, reimbursement pressures, technological innovation, and sustainability trends are reshaping its competitive landscape. We translate these external forces into strategic risks and opportunities you can act on. Purchase the full PESTLE for detailed, ready-to-use insights and forecasts to inform investment or strategic decisions.

Political factors

Reimbursement policy volatility

Government reimbursement programs, especially the U.S. ESRD system, drive most dialysis revenues—Medicare accounted for roughly the majority of U.S. dialysis payments and Medicare ESRD spending was about $49.6 billion in 2022. Shifts in bundled payments, value-based incentives and CMS initiatives to expand home dialysis can compress or expand FMC margins. FMC must engage in advocacy, adjust contracting and run scenario plans for rate cuts or quality-linked bonuses.

Public healthcare spending priorities

National budget allocations to chronic care and renal programs directly shape capacity and expansion: Fresenius Medical Care reported roughly €21 billion revenue in 2024 and serves about 345,000 dialysis patients, so shifts in public funding affect clinic openings and reimbursement rates. Fiscal tightening can delay new clinics, while targeted chronic-disease or home-dialysis incentives accelerate adoption. FMC must align offerings to prevention/home therapies and diversify payer exposure to reduce country-specific budget risk.

Trade and geopolitical supply risks

Tariffs, export controls and geopolitical tensions threaten access to membranes, resins and components, increasing lead times by months and raising costs for Fresenius Medical Care, which reported €20.6bn revenue in 2023; policies in China, the EU and the U.S. disproportionately affect supply chains. FMC must advance dual/multi-sourcing, localized manufacturing, strategic inventories and nearshoring to maintain resilience and reduce disruption risk.

Public–private partnerships in care delivery

Governments increasingly outsource dialysis to private operators, and Fresenius Medical Care, active in over 120 countries and serving ~345,000 patients (2024), competes on tender dynamics, local-partner and national-content rules that materially affect win rates. FMC can leverage superior clinical outcomes and cost-efficiency to secure PPPs, while transparent outcomes reporting bolsters contract bids and renewals.

- Tender dynamics: local-partner and national-content rules

- Competitive edge: clinical outcomes + cost efficiency

- Evidence: ~345,000 patients served (2024)

- Renewals: transparent outcomes reporting strengthens bids

Health policy push for home-based care

Many jurisdictions push home therapies to cut system costs and boost patient autonomy, with studies showing up to 30% lower annual dialysis costs for home modalities versus in-center care; incentives and training mandates are accelerating peritoneal and home hemodialysis uptake. Fresenius Medical Care should scale patient education, supply logistics and tele-support to capture market share, while policy-aligned pilots can unlock preferential funding.

- Reduce cost: up to 30% lower per-patient dialysis cost

- Growth driver: mandates/incentives raise home uptake

- FMC focus: education, logistics, tele-support

- Strategy: policy pilots to access preferential funding

Medicare ESRD $49.6bn and value-based pay drive shift to home dialysis (≈30% lower cost)

Government reimbursement (Medicare ESRD ~$49.6bn in 2022) and bundled/value-based payment shifts drive FMC margins; policy-driven home-dialysis expansion (≈30% lower annual cost) reshapes service mix. Public budgets and tender/local-content rules affect clinic openings and PPP wins; supply-chain controls raise component lead times. FMC: diversify payers, localize supply, scale home-care and outcomes reporting.

| Metric | Value | Political Impact |

|---|---|---|

| Revenue (2024) | ≈€21bn | Scale affects negotiation power |

| Patients (2024) | ≈345,000 | Service demand shapes policy influence |

| Medicare ESRD (2022) | $49.6bn | Reimbursement risk/benchmark |

| Home dialysis cost delta | ≈-30% | Incentive for policy shifts |

What is included in the product

Explores how macro-environmental forces uniquely affect Fresenius Medical Care across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context and forward-looking insights to help executives and investors identify risks, opportunities and actionable strategies.

A clean, summarized Fresenius Medical Care PESTLE that is visually segmented by category, letting teams quickly interpret regulatory, market and technological risks and drop concise bullets into presentations for fast alignment.

Economic factors

Inflation and input cost pressures

Rising costs for plastics, dialyzer fibers, energy and logistics have compressed Fresenius Medical Care product margins, while contract pricing lags delay pass-through to payers and clinics. FMC must deploy cost engineering, hedging and disciplined price escalators to protect margins. Lean operations and automation are critical to offset wage inflation and sustain profitability.

Foreign exchange and global revenue mix

Fresenius Medical Care reported €20.7bn revenue in 2024, with a multi-currency footprint that exposes earnings to FX volatility as revenues and costs are denominated across USD, EUR and emerging-market currencies. Dollar strength in 2024 depressed translated euro earnings while easing some dollar-priced input costs. Natural hedging from local cost bases and use of financial derivatives trimmed translation swings. Pricing strategies must embed local-currency risk and frequent adjustments.

Interest rates and capital intensity

Clinic networks, equipment fleets and inventories require significant capital for Fresenius Medical Care, which reported group sales of about €20.9 billion in 2023; higher interest rates—US Fed funds around 5.25–5.50% in 2024–2025—raise financing costs and hurdle rates for new centers. FMC should prioritize ROI-positive refurbishments and asset-light models where feasible. Sale–leaseback transactions or partnerships can optimize capital structure and preserve liquidity.

Payer mix and pricing pressure

Shifts from commercial to public payers compress margins in mature markets, with Medicare covering roughly 80% of US dialysis patients, increasing reimbursement pressure. Managed care and group purchasing organizations intensify price negotiations, forcing Fresenius Medical Care to demonstrate total cost-of-care reductions and better outcomes to defend pricing. Value-based contracts offer a path to align incentives and stabilize revenue.

- Payer shift: Medicare ~80% of US dialysis patients

- Pricing pressure: stronger managed care/GPO leverage

- Defense: show lower total cost-of-care + outcomes

- Solution: expand value-based contracts to stabilize revenue

Emerging market demand growth

Rising CKD—estimated at about 850 million people globally—plus expanding insurance and primary care in emerging markets is driving dialysis volume growth, with EMs representing a key growth vector for Fresenius Medical Care. Affordability constraints push tiered product lines and pay‑as‑you‑go service models; local manufacturing and distribution lower unit costs and improve success in public tenders, while clinician training programs increase utilization and patient retention.

- CKD burden ~850 million globally

- Tiered products + pay‑per‑use for affordability

- Local manufacturing reduces tender unit costs

- Training builds clinician capacity and stickiness

Medicare ESRD $49.6bn and value-based pay drive shift to home dialysis (≈30% lower cost)

Rising input, energy and logistics costs compress margins; cost engineering, hedging and price escalators are essential. FMC reported €20.7bn revenue in 2024 with material FX exposure as USD/EUR moves affect translated earnings. Higher rates (Fed funds ~5.25–5.50% in 2024–25) raise financing costs for clinics; Medicare covers ~80% of US dialysis patients, pressuring pricing. CKD ~850m drives EM volume growth but affordability limits.

| Metric | Value |

|---|---|

| 2024 Revenue | €20.7bn |

| Global CKD | ~850m |

| US Medicare share | ~80% |

| Fed funds (2024–25) | 5.25–5.50% |

Preview the Actual Deliverable

Fresenius Medical Care PESTLE Analysis

The preview shown here is the exact PESTLE analysis of Fresenius Medical Care you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the final, professionally structured document.