Fresenius Medical Care SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Fresenius Medical Care's SWOT highlights resilient dialysis market leadership, global scale and clinical innovation, alongside regulatory, reimbursement and supply-chain pressures that could affect margins. Our full SWOT unpacks competitive advantages, operational risks and growth levers with financial context and actionable recommendations. Purchase the complete, editable Word + Excel report to plan, pitch, and invest with confidence.

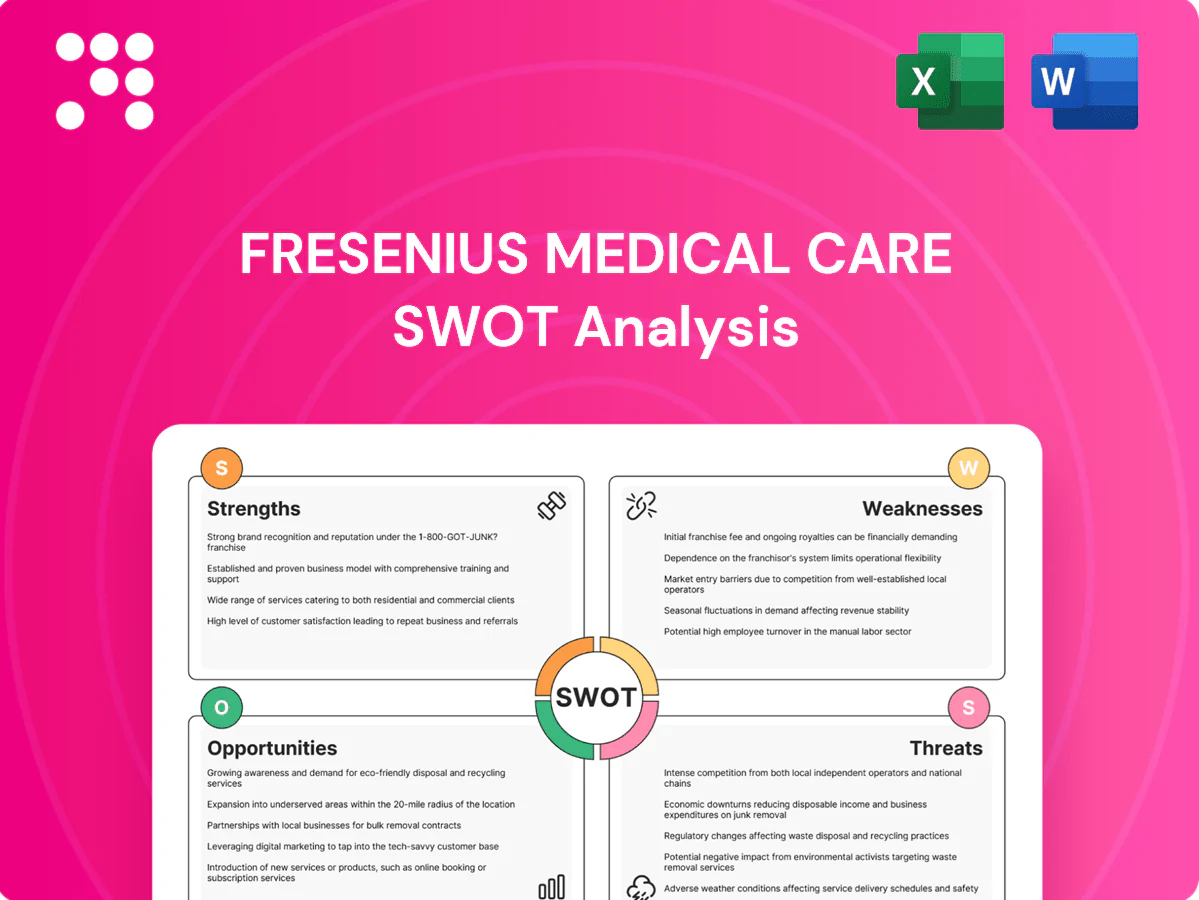

Strengths

Global dialysis leader

Fresenius Medical Care operates about 4,200 dialysis clinics serving roughly 345,000 patients and reported approximately €20.9bn revenue in 2024, making it a global dialysis leader. Its scale drives cost efficiencies, standardized protocols and data-driven care improvements. A broad geographic footprint diversifies revenue and patient mix, while strong brand recognition supports payer negotiations and patient referrals.

Integrated products + services

Owning both dialysis equipment and treatment delivery creates a closed-loop ecosystem, serving about 345,000 patients across roughly 4,000 clinics (2024). Clinic feedback accelerates product innovation and reliability, shortening development cycles and improving uptime. Bundled device-plus-care solutions help optimize clinical outcomes and total cost of care through coordinated protocols. Vertical integration secures supply chains and enables greater margin capture across the value chain.

Comprehensive portfolio

Fresenius Medical Care offers in-center, home hemodialysis and peritoneal dialysis across about 4,000 clinics, treating roughly 350,000 patients globally, backed by a broad range of machines, dialyzers and disposables. This portfolio breadth drives cross-selling and recurring consumables revenue, strengthening long-term customer lock-in. It also enables tailored care pathways across acuity levels, improving retention and lifetime patient value.

Clinical expertise & data

Fresenius Medical Care leverages extensive clinical expertise and real-world data from approximately 345,000 dialysis patients (2023–24) to refine treatment protocols and standardize care across its network. Clinical teams and registries enable robust outcomes tracking and quality metrics, while integrated data assets support risk management and strengthen payer value propositions. Continuous improvement loops drive higher consistency in standard-of-care delivery.

- Real-world evidence: ~345,000 patients (2023–24)

- Registries: outcomes & quality tracking

- Data: supports payer value & risk management

- Continuous improvement: standardization

Resilient demand

End-stage renal disease care is non-discretionary and recurring, supporting Fresenius Medical Care’s defensive cash flows; about 10% of the global population has CKD and roughly 3 million patients receive dialysis worldwide, underpinning steady volume growth as populations age.

- CKD prevalence ~10%

- ~3 million dialysis patients

- US Medicare ESRD coverage since 1972

Dialysis platform: ~4,200 clinics and €20.9bn revenue

Fresenius Medical Care operates ~4,200 clinics serving ~345,000 patients with ~€20.9bn revenue in 2024, securing scale-driven cost and negotiating advantages. Vertical integration of devices and care creates a closed-loop ecosystem that boosts margins and innovation. Large real-world data and non-discretionary recurring dialysis demand underpin defensive, predictable cash flows.

| Metric | Value |

|---|---|

| Clinics | ~4,200 (2024) |

| Patients served | ~345,000 (2024) |

| Revenue | €20.9bn (2024) |

| Global dialysis pts | ~3m |

| CKD prevalence | ~10% |

What is included in the product

Delivers a strategic overview of Fresenius Medical Care’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to its competitive position and future growth.

Provides a concise SWOT matrix highlighting Fresenius Medical Care's strengths, weaknesses, opportunities, and threats to quickly pinpoint strategic pain points and prioritize remediation actions for management and investors.

Weaknesses

Reimbursement dependence

Revenue is highly tied to government and insurer rates—Medicare covers roughly 80% of U.S. dialysis patients, exposing Fresenius to public-rate shifts that can quickly compress margins. Negotiating power and reimbursement levels vary widely across the 50+ countries where it operates, creating uneven revenue risk. Complex prior-authorizations and billing rules add administrative cost and operational drag.

High operating intensity

Clinic operations are labor- and compliance-heavy for Fresenius Medical Care, which operates roughly 4,000 dialysis clinics and serves about 345,000 patients worldwide (2024). Staffing shortages and wage inflation have compressed margins as labor is the largest operating cost; ongoing facility upkeep and equipment capex add capital intensity, while high fixed-cost leverage hurts lower-volume regions.

Litigation and compliance risk

Healthcare regulations are stringent and evolving, and Fresenius Medical Care's 2023 revenue of €21.7bn means any compliance breach risks large-scale financial exposure. Quality lapses or billing errors can trigger penalties running into millions, while legal disputes incur high defense costs and distract management. Reputation damage can reduce referrals and jeopardize hospital contracts, directly threatening revenue streams.

Product concentration

Core revenues remain heavily tied to dialysis modalities and disposables, with roughly 75% of group sales generated from renal care, concentrating earnings and margin exposure. Limited presence beyond renal therapy increases sector risk if reimbursement or regulations shift. Rapid technology shifts in renal replacement therapy could materially disrupt demand while diversification into adjacencies has progressed only measuredly.

- Revenue concentration: ~75% renal care

- Sector risk: high exposure to dialysis trends

- Tech risk: innovations could reduce disposables demand

- Diversification: gradual, limited scale

US market exposure

Fresenius Medical Care derives about two-thirds of revenue and roughly 70% of operating profit from the US; Medicare ESRD payment bundles and evolving value‑based programs can materially swing margins. Intense provider competition in major metros pressures volumes, while structural pricing scrutiny from payers and regulators caps rate flexibility.

- US ≈ two-thirds of revenue; ≈70% operating profit

- Medicare bundle/value‑based rule changes drive volatility

- High competition in major metropolitan markets

- Persistent pricing and regulatory scrutiny

Renal-focused: ~75% sales, ~66% US rev; Medicare risk

Revenue concentrated in renal care (~75% of sales) and the US (≈66% revenue, ≈70% operating profit) exposes Fresenius to Medicare policy shifts (Medicare covers ~80% of U.S. dialysis patients). Large footprint (~4,000 clinics; ~345,000 patients in 2024) creates labor, capex and compliance cost pressures; regulatory breaches risk material penalties against €21.7bn 2023 revenue.

| Metric | Value |

|---|---|

| 2023 revenue | €21.7bn |

| Renal care share | ~75% |

| US revenue share | ≈66% |

| Patients (2024) | ~345,000 |

| Clinics | ~4,000 |

Preview the Actual Deliverable

Fresenius Medical Care SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buying unlocks the complete, editable version.

You’re viewing a live excerpt of the real file—purchase to download the entire, ready-to-use report immediately.

Make Insightful Decisions Backed by Expert Research

Fresenius Medical Care's SWOT highlights resilient dialysis market leadership, global scale and clinical innovation, alongside regulatory, reimbursement and supply-chain pressures that could affect margins. Our full SWOT unpacks competitive advantages, operational risks and growth levers with financial context and actionable recommendations. Purchase the complete, editable Word + Excel report to plan, pitch, and invest with confidence.

Strengths

Global dialysis leader

Fresenius Medical Care operates about 4,200 dialysis clinics serving roughly 345,000 patients and reported approximately €20.9bn revenue in 2024, making it a global dialysis leader. Its scale drives cost efficiencies, standardized protocols and data-driven care improvements. A broad geographic footprint diversifies revenue and patient mix, while strong brand recognition supports payer negotiations and patient referrals.

Integrated products + services

Owning both dialysis equipment and treatment delivery creates a closed-loop ecosystem, serving about 345,000 patients across roughly 4,000 clinics (2024). Clinic feedback accelerates product innovation and reliability, shortening development cycles and improving uptime. Bundled device-plus-care solutions help optimize clinical outcomes and total cost of care through coordinated protocols. Vertical integration secures supply chains and enables greater margin capture across the value chain.

Comprehensive portfolio

Fresenius Medical Care offers in-center, home hemodialysis and peritoneal dialysis across about 4,000 clinics, treating roughly 350,000 patients globally, backed by a broad range of machines, dialyzers and disposables. This portfolio breadth drives cross-selling and recurring consumables revenue, strengthening long-term customer lock-in. It also enables tailored care pathways across acuity levels, improving retention and lifetime patient value.

Clinical expertise & data

Fresenius Medical Care leverages extensive clinical expertise and real-world data from approximately 345,000 dialysis patients (2023–24) to refine treatment protocols and standardize care across its network. Clinical teams and registries enable robust outcomes tracking and quality metrics, while integrated data assets support risk management and strengthen payer value propositions. Continuous improvement loops drive higher consistency in standard-of-care delivery.

- Real-world evidence: ~345,000 patients (2023–24)

- Registries: outcomes & quality tracking

- Data: supports payer value & risk management

- Continuous improvement: standardization

Resilient demand

End-stage renal disease care is non-discretionary and recurring, supporting Fresenius Medical Care’s defensive cash flows; about 10% of the global population has CKD and roughly 3 million patients receive dialysis worldwide, underpinning steady volume growth as populations age.

- CKD prevalence ~10%

- ~3 million dialysis patients

- US Medicare ESRD coverage since 1972

Dialysis platform: ~4,200 clinics and €20.9bn revenue

Fresenius Medical Care operates ~4,200 clinics serving ~345,000 patients with ~€20.9bn revenue in 2024, securing scale-driven cost and negotiating advantages. Vertical integration of devices and care creates a closed-loop ecosystem that boosts margins and innovation. Large real-world data and non-discretionary recurring dialysis demand underpin defensive, predictable cash flows.

| Metric | Value |

|---|---|

| Clinics | ~4,200 (2024) |

| Patients served | ~345,000 (2024) |

| Revenue | €20.9bn (2024) |

| Global dialysis pts | ~3m |

| CKD prevalence | ~10% |

What is included in the product

Delivers a strategic overview of Fresenius Medical Care’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to its competitive position and future growth.

Provides a concise SWOT matrix highlighting Fresenius Medical Care's strengths, weaknesses, opportunities, and threats to quickly pinpoint strategic pain points and prioritize remediation actions for management and investors.

Weaknesses

Reimbursement dependence

Revenue is highly tied to government and insurer rates—Medicare covers roughly 80% of U.S. dialysis patients, exposing Fresenius to public-rate shifts that can quickly compress margins. Negotiating power and reimbursement levels vary widely across the 50+ countries where it operates, creating uneven revenue risk. Complex prior-authorizations and billing rules add administrative cost and operational drag.

High operating intensity

Clinic operations are labor- and compliance-heavy for Fresenius Medical Care, which operates roughly 4,000 dialysis clinics and serves about 345,000 patients worldwide (2024). Staffing shortages and wage inflation have compressed margins as labor is the largest operating cost; ongoing facility upkeep and equipment capex add capital intensity, while high fixed-cost leverage hurts lower-volume regions.

Litigation and compliance risk

Healthcare regulations are stringent and evolving, and Fresenius Medical Care's 2023 revenue of €21.7bn means any compliance breach risks large-scale financial exposure. Quality lapses or billing errors can trigger penalties running into millions, while legal disputes incur high defense costs and distract management. Reputation damage can reduce referrals and jeopardize hospital contracts, directly threatening revenue streams.

Product concentration

Core revenues remain heavily tied to dialysis modalities and disposables, with roughly 75% of group sales generated from renal care, concentrating earnings and margin exposure. Limited presence beyond renal therapy increases sector risk if reimbursement or regulations shift. Rapid technology shifts in renal replacement therapy could materially disrupt demand while diversification into adjacencies has progressed only measuredly.

- Revenue concentration: ~75% renal care

- Sector risk: high exposure to dialysis trends

- Tech risk: innovations could reduce disposables demand

- Diversification: gradual, limited scale

US market exposure

Fresenius Medical Care derives about two-thirds of revenue and roughly 70% of operating profit from the US; Medicare ESRD payment bundles and evolving value‑based programs can materially swing margins. Intense provider competition in major metros pressures volumes, while structural pricing scrutiny from payers and regulators caps rate flexibility.

- US ≈ two-thirds of revenue; ≈70% operating profit

- Medicare bundle/value‑based rule changes drive volatility

- High competition in major metropolitan markets

- Persistent pricing and regulatory scrutiny

Renal-focused: ~75% sales, ~66% US rev; Medicare risk

Revenue concentrated in renal care (~75% of sales) and the US (≈66% revenue, ≈70% operating profit) exposes Fresenius to Medicare policy shifts (Medicare covers ~80% of U.S. dialysis patients). Large footprint (~4,000 clinics; ~345,000 patients in 2024) creates labor, capex and compliance cost pressures; regulatory breaches risk material penalties against €21.7bn 2023 revenue.

| Metric | Value |

|---|---|

| 2023 revenue | €21.7bn |

| Renal care share | ~75% |

| US revenue share | ≈66% |

| Patients (2024) | ~345,000 |

| Clinics | ~4,000 |

Preview the Actual Deliverable

Fresenius Medical Care SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buying unlocks the complete, editable version.

You’re viewing a live excerpt of the real file—purchase to download the entire, ready-to-use report immediately.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Fresenius Medical Care's SWOT highlights resilient dialysis market leadership, global scale and clinical innovation, alongside regulatory, reimbursement and supply-chain pressures that could affect margins. Our full SWOT unpacks competitive advantages, operational risks and growth levers with financial context and actionable recommendations. Purchase the complete, editable Word + Excel report to plan, pitch, and invest with confidence.

Strengths

Global dialysis leader

Fresenius Medical Care operates about 4,200 dialysis clinics serving roughly 345,000 patients and reported approximately €20.9bn revenue in 2024, making it a global dialysis leader. Its scale drives cost efficiencies, standardized protocols and data-driven care improvements. A broad geographic footprint diversifies revenue and patient mix, while strong brand recognition supports payer negotiations and patient referrals.

Integrated products + services

Owning both dialysis equipment and treatment delivery creates a closed-loop ecosystem, serving about 345,000 patients across roughly 4,000 clinics (2024). Clinic feedback accelerates product innovation and reliability, shortening development cycles and improving uptime. Bundled device-plus-care solutions help optimize clinical outcomes and total cost of care through coordinated protocols. Vertical integration secures supply chains and enables greater margin capture across the value chain.

Comprehensive portfolio

Fresenius Medical Care offers in-center, home hemodialysis and peritoneal dialysis across about 4,000 clinics, treating roughly 350,000 patients globally, backed by a broad range of machines, dialyzers and disposables. This portfolio breadth drives cross-selling and recurring consumables revenue, strengthening long-term customer lock-in. It also enables tailored care pathways across acuity levels, improving retention and lifetime patient value.

Clinical expertise & data

Fresenius Medical Care leverages extensive clinical expertise and real-world data from approximately 345,000 dialysis patients (2023–24) to refine treatment protocols and standardize care across its network. Clinical teams and registries enable robust outcomes tracking and quality metrics, while integrated data assets support risk management and strengthen payer value propositions. Continuous improvement loops drive higher consistency in standard-of-care delivery.

- Real-world evidence: ~345,000 patients (2023–24)

- Registries: outcomes & quality tracking

- Data: supports payer value & risk management

- Continuous improvement: standardization

Resilient demand

End-stage renal disease care is non-discretionary and recurring, supporting Fresenius Medical Care’s defensive cash flows; about 10% of the global population has CKD and roughly 3 million patients receive dialysis worldwide, underpinning steady volume growth as populations age.

- CKD prevalence ~10%

- ~3 million dialysis patients

- US Medicare ESRD coverage since 1972

Dialysis platform: ~4,200 clinics and €20.9bn revenue

Fresenius Medical Care operates ~4,200 clinics serving ~345,000 patients with ~€20.9bn revenue in 2024, securing scale-driven cost and negotiating advantages. Vertical integration of devices and care creates a closed-loop ecosystem that boosts margins and innovation. Large real-world data and non-discretionary recurring dialysis demand underpin defensive, predictable cash flows.

| Metric | Value |

|---|---|

| Clinics | ~4,200 (2024) |

| Patients served | ~345,000 (2024) |

| Revenue | €20.9bn (2024) |

| Global dialysis pts | ~3m |

| CKD prevalence | ~10% |

What is included in the product

Delivers a strategic overview of Fresenius Medical Care’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to its competitive position and future growth.

Provides a concise SWOT matrix highlighting Fresenius Medical Care's strengths, weaknesses, opportunities, and threats to quickly pinpoint strategic pain points and prioritize remediation actions for management and investors.

Weaknesses

Reimbursement dependence

Revenue is highly tied to government and insurer rates—Medicare covers roughly 80% of U.S. dialysis patients, exposing Fresenius to public-rate shifts that can quickly compress margins. Negotiating power and reimbursement levels vary widely across the 50+ countries where it operates, creating uneven revenue risk. Complex prior-authorizations and billing rules add administrative cost and operational drag.

High operating intensity

Clinic operations are labor- and compliance-heavy for Fresenius Medical Care, which operates roughly 4,000 dialysis clinics and serves about 345,000 patients worldwide (2024). Staffing shortages and wage inflation have compressed margins as labor is the largest operating cost; ongoing facility upkeep and equipment capex add capital intensity, while high fixed-cost leverage hurts lower-volume regions.

Litigation and compliance risk

Healthcare regulations are stringent and evolving, and Fresenius Medical Care's 2023 revenue of €21.7bn means any compliance breach risks large-scale financial exposure. Quality lapses or billing errors can trigger penalties running into millions, while legal disputes incur high defense costs and distract management. Reputation damage can reduce referrals and jeopardize hospital contracts, directly threatening revenue streams.

Product concentration

Core revenues remain heavily tied to dialysis modalities and disposables, with roughly 75% of group sales generated from renal care, concentrating earnings and margin exposure. Limited presence beyond renal therapy increases sector risk if reimbursement or regulations shift. Rapid technology shifts in renal replacement therapy could materially disrupt demand while diversification into adjacencies has progressed only measuredly.

- Revenue concentration: ~75% renal care

- Sector risk: high exposure to dialysis trends

- Tech risk: innovations could reduce disposables demand

- Diversification: gradual, limited scale

US market exposure

Fresenius Medical Care derives about two-thirds of revenue and roughly 70% of operating profit from the US; Medicare ESRD payment bundles and evolving value‑based programs can materially swing margins. Intense provider competition in major metros pressures volumes, while structural pricing scrutiny from payers and regulators caps rate flexibility.

- US ≈ two-thirds of revenue; ≈70% operating profit

- Medicare bundle/value‑based rule changes drive volatility

- High competition in major metropolitan markets

- Persistent pricing and regulatory scrutiny

Renal-focused: ~75% sales, ~66% US rev; Medicare risk

Revenue concentrated in renal care (~75% of sales) and the US (≈66% revenue, ≈70% operating profit) exposes Fresenius to Medicare policy shifts (Medicare covers ~80% of U.S. dialysis patients). Large footprint (~4,000 clinics; ~345,000 patients in 2024) creates labor, capex and compliance cost pressures; regulatory breaches risk material penalties against €21.7bn 2023 revenue.

| Metric | Value |

|---|---|

| 2023 revenue | €21.7bn |

| Renal care share | ~75% |

| US revenue share | ≈66% |

| Patients (2024) | ~345,000 |

| Clinics | ~4,000 |

Preview the Actual Deliverable

Fresenius Medical Care SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buying unlocks the complete, editable version.

You’re viewing a live excerpt of the real file—purchase to download the entire, ready-to-use report immediately.