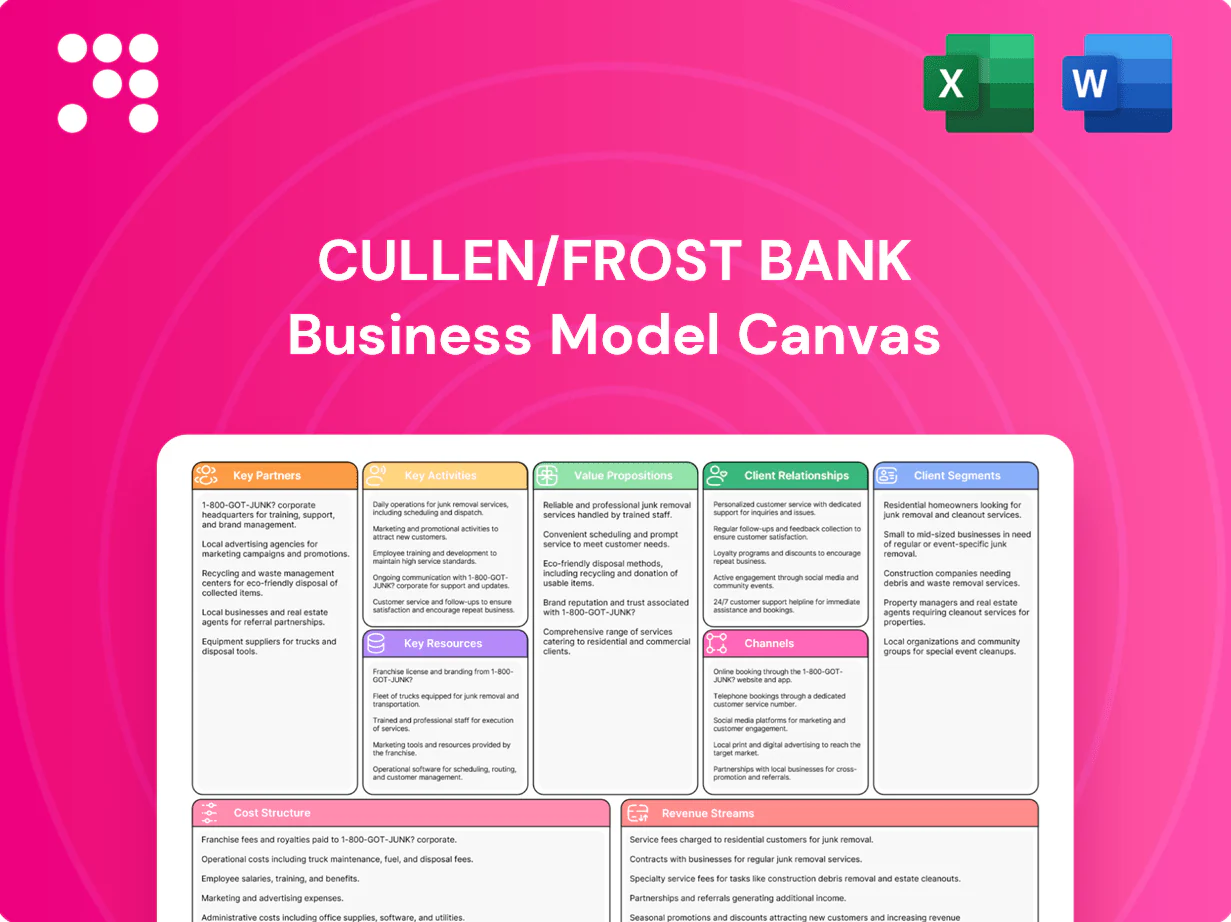

Cullen/Frost Bank Business Model Canvas

Unlock a regional bank's strategic blueprint with our Business Model Canvas

Unlock Cullen/Frost Bank’s strategic blueprint with our Business Model Canvas. This concise, section-by-section canvas reveals value propositions, revenue streams, partnerships and cost drivers to inform investors, consultants, and founders. Purchase the full Word/Excel package for actionable analysis and ready-to-use templates.

Partnerships

Payment networks

Partnerships with Visa, Mastercard, ACH, and Fedwire give Cullen/Frost seamless card issuance and payments across Texas and nationally, leveraging networks that process over $3 trillion daily on Fedwire and more than 30 billion ACH transactions annually. These partners provide scale, advanced fraud tools, and interchange connectivity, enabling Frost to deliver fast, reliable consumer and business transactions. Strong ties bolster treasury, merchant, and debit/credit services.

Core & fintech vendors

Alliances with core banking platforms, cloud providers, and fintechs accelerate digital features and operational resilience, with McKinsey 2024 finding cloud migration can cut IT costs 20–30%. Vendors enable mobile apps, APIs, data analytics, and cybersecurity to expand services and fraud defense. Co-development shortens time-to-market for customer-facing innovations, while integration partners modernize legacy stacks with minimal service disruption.

Broker-dealers & custodians

Broker-dealers and custodians provide Cullen/Frost investment services with trade execution, safekeeping, and access to products, leveraging custodian platforms that together hold trillions of dollars in client assets as of 2024. These partnerships expand offerings to mutual funds, ETFs, fixed income and alternatives, enabling scalable, compliant wealth-management operations. Clients gain diversified choices and operational efficiency through integrated custody and execution services.

Insurance carriers

Insurance carriers supply property-casualty, life, and specialty coverage distributed through Frost, broadening risk solutions for businesses and individuals; Cullen/Frost reported total assets of $46.9 billion in 2024, supporting expanded product distribution. Joint marketing and underwriting expertise improve product fit and pricing while cross-sell drives fee income and deeper client relationships.

- Carriers: broaden risk portfolio

- Joint underwriting: better pricing

- Cross-sell: fee income growth

Community & commercial partners

Local chambers, economic development groups, and industry associations connect Frost to Texas businesses, generating qualified leads and community trust and supporting SBA lending and CRA initiatives. These collaborations drove regional growth in 2024 and reinforce Frost’s brand as a relationship-first Texas bank with 160+ branches across the state (2024).

- Local chambers

- Economic development groups

- Industry associations

- 160+ branches (2024)

Nationwide payment rails, cloud agility and custodial alliances power treasury and wealth services

Partnerships with Visa, Mastercard, ACH and Fedwire enable nationwide payments (Fedwire $3T/day; ACH >30B txns/yr) and support treasury, merchant and card services. Alliances with core platforms, cloud and fintechs speed digital features and resilience (cloud can cut IT costs 20–30% per McKinsey 2024). Custodians/broker-dealers and insurers expand wealth and risk offerings; Frost reported $46.9B assets and 160+ branches (2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Payments (Visa/Mastercard/Fedwire/ACH) | Payments/settlement | Fedwire $3T/day; ACH >30B/yr |

| Cloud/Fintech | Digital/ops | IT costs -20–30% |

| Custodians/Brokers | Wealth services | Supports diversified products |

| Insurers/Local partners | Risk distribution & leads | $46.9B assets; 160+ branches |

What is included in the product

A comprehensive, pre-written Cullen/Frost Bank Business Model Canvas outlining customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations and competitive advantages, with linked SWOT analysis for investor presentations and strategic decision-making.

High-level view of Cullen/Frost Bank's business model with editable cells, saving hours of structuring and formatting while enabling shareable, collaborative snapshots for quick executive summaries and board-ready presentations.

Activities

Lending & credit

Underwriting and portfolio management for commercial, real estate, and consumer loans drive Cullen/Frost’s interest income across a $33.5B loan book (12/31/2024), while risk models and relationship insights shape pricing and exposure limits. Continuous monitoring and stress-testing kept the nonperforming loan ratio near 0.42% in 2024, protecting asset quality through cycles. Credit policy is tailored to Texas market dynamics and regulatory standards.

Deposit gathering

Acquiring low-cost, sticky deposits sustains margin and liquidity for Cullen/Frost, which held over $40 billion in deposits in 2024; this stable base cushions net interest margin and funding volatility. Branch teams, digital onboarding, and targeted campaigns attract households and businesses, while cash management solutions retain operating balances. Pricing, service, and trust support multi-decade relationships.

Treasury & payments

Treasury and payments deliver faster, secure payment and receivables solutions—ACH, wires, RDC, merchant services and lockbox—streamlining cash conversion cycles and supporting over 30 billion ACH payments annually by 2024. Robust fraud prevention and layered controls reduce losses and exposure across business portfolios. Deep ERP integrations and open APIs boost client stickiness and recurring fee income for Cullen/Frost.

Wealth & advisory

Wealth & advisory integrates investment management, trust, brokerage, and planning to deepen wallet share, with research-driven asset allocation and fiduciary oversight directing client outcomes. Advisors coordinate banking, lending, and insurance strategies, while discretionary mandates and advisory fees create recurring revenue streams in 2024.

- Investment management

- Fiduciary oversight

- Banking-lending-insurance coordination

- Discretionary mandates & advisory fees

Risk & compliance

Cullen/Frost maintains strong credit, market, liquidity, operational, and cyber risk frameworks that protect the franchise and align with 2024 regulatory expectations; AML/BSA, KYC, and consumer compliance programs drive ongoing regulatory alignment. Stress testing and capital planning in 2024 prepare the bank for downturn scenarios. Robust vendor and model risk management fortify enterprise resilience.

- 2024: ongoing stress tests & capital planning

- AML/BSA, KYC, consumer compliance

- Credit, market, liquidity, operational, cyber controls

- Vendor & model risk management

UW-led: $33.5B loans, >$40B deposits, 0.42% NPL

Underwriting and portfolio management drive interest income across a $33.5B loan book (12/31/2024) with NPL ratio ~0.42% in 2024, supported by stress testing and Texas-tailored credit policy. Stable funding from >$40B deposits sustains margin and liquidity. Payments, treasury, wealth, and risk controls generate fee income and protect the franchise.

| Metric | 2024 |

|---|---|

| Loan book | $33.5B |

| Deposits | >$40B |

| NPL ratio | 0.42% |

| ACH volume | ~30B |

Full Document Unlocks After Purchase

Business Model Canvas

The Cullen/Frost Bank Business Model Canvas you’re previewing is the exact deliverable—not a mockup—and includes the same content you’ll receive after purchase. When you complete your order you’ll get this full, ready-to-edit document in Word and Excel formats, formatted and structured exactly as shown.

Unlock a regional bank's strategic blueprint with our Business Model Canvas

Unlock Cullen/Frost Bank’s strategic blueprint with our Business Model Canvas. This concise, section-by-section canvas reveals value propositions, revenue streams, partnerships and cost drivers to inform investors, consultants, and founders. Purchase the full Word/Excel package for actionable analysis and ready-to-use templates.

Partnerships

Payment networks

Partnerships with Visa, Mastercard, ACH, and Fedwire give Cullen/Frost seamless card issuance and payments across Texas and nationally, leveraging networks that process over $3 trillion daily on Fedwire and more than 30 billion ACH transactions annually. These partners provide scale, advanced fraud tools, and interchange connectivity, enabling Frost to deliver fast, reliable consumer and business transactions. Strong ties bolster treasury, merchant, and debit/credit services.

Core & fintech vendors

Alliances with core banking platforms, cloud providers, and fintechs accelerate digital features and operational resilience, with McKinsey 2024 finding cloud migration can cut IT costs 20–30%. Vendors enable mobile apps, APIs, data analytics, and cybersecurity to expand services and fraud defense. Co-development shortens time-to-market for customer-facing innovations, while integration partners modernize legacy stacks with minimal service disruption.

Broker-dealers & custodians

Broker-dealers and custodians provide Cullen/Frost investment services with trade execution, safekeeping, and access to products, leveraging custodian platforms that together hold trillions of dollars in client assets as of 2024. These partnerships expand offerings to mutual funds, ETFs, fixed income and alternatives, enabling scalable, compliant wealth-management operations. Clients gain diversified choices and operational efficiency through integrated custody and execution services.

Insurance carriers

Insurance carriers supply property-casualty, life, and specialty coverage distributed through Frost, broadening risk solutions for businesses and individuals; Cullen/Frost reported total assets of $46.9 billion in 2024, supporting expanded product distribution. Joint marketing and underwriting expertise improve product fit and pricing while cross-sell drives fee income and deeper client relationships.

- Carriers: broaden risk portfolio

- Joint underwriting: better pricing

- Cross-sell: fee income growth

Community & commercial partners

Local chambers, economic development groups, and industry associations connect Frost to Texas businesses, generating qualified leads and community trust and supporting SBA lending and CRA initiatives. These collaborations drove regional growth in 2024 and reinforce Frost’s brand as a relationship-first Texas bank with 160+ branches across the state (2024).

- Local chambers

- Economic development groups

- Industry associations

- 160+ branches (2024)

Nationwide payment rails, cloud agility and custodial alliances power treasury and wealth services

Partnerships with Visa, Mastercard, ACH and Fedwire enable nationwide payments (Fedwire $3T/day; ACH >30B txns/yr) and support treasury, merchant and card services. Alliances with core platforms, cloud and fintechs speed digital features and resilience (cloud can cut IT costs 20–30% per McKinsey 2024). Custodians/broker-dealers and insurers expand wealth and risk offerings; Frost reported $46.9B assets and 160+ branches (2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Payments (Visa/Mastercard/Fedwire/ACH) | Payments/settlement | Fedwire $3T/day; ACH >30B/yr |

| Cloud/Fintech | Digital/ops | IT costs -20–30% |

| Custodians/Brokers | Wealth services | Supports diversified products |

| Insurers/Local partners | Risk distribution & leads | $46.9B assets; 160+ branches |

What is included in the product

A comprehensive, pre-written Cullen/Frost Bank Business Model Canvas outlining customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations and competitive advantages, with linked SWOT analysis for investor presentations and strategic decision-making.

High-level view of Cullen/Frost Bank's business model with editable cells, saving hours of structuring and formatting while enabling shareable, collaborative snapshots for quick executive summaries and board-ready presentations.

Activities

Lending & credit

Underwriting and portfolio management for commercial, real estate, and consumer loans drive Cullen/Frost’s interest income across a $33.5B loan book (12/31/2024), while risk models and relationship insights shape pricing and exposure limits. Continuous monitoring and stress-testing kept the nonperforming loan ratio near 0.42% in 2024, protecting asset quality through cycles. Credit policy is tailored to Texas market dynamics and regulatory standards.

Deposit gathering

Acquiring low-cost, sticky deposits sustains margin and liquidity for Cullen/Frost, which held over $40 billion in deposits in 2024; this stable base cushions net interest margin and funding volatility. Branch teams, digital onboarding, and targeted campaigns attract households and businesses, while cash management solutions retain operating balances. Pricing, service, and trust support multi-decade relationships.

Treasury & payments

Treasury and payments deliver faster, secure payment and receivables solutions—ACH, wires, RDC, merchant services and lockbox—streamlining cash conversion cycles and supporting over 30 billion ACH payments annually by 2024. Robust fraud prevention and layered controls reduce losses and exposure across business portfolios. Deep ERP integrations and open APIs boost client stickiness and recurring fee income for Cullen/Frost.

Wealth & advisory

Wealth & advisory integrates investment management, trust, brokerage, and planning to deepen wallet share, with research-driven asset allocation and fiduciary oversight directing client outcomes. Advisors coordinate banking, lending, and insurance strategies, while discretionary mandates and advisory fees create recurring revenue streams in 2024.

- Investment management

- Fiduciary oversight

- Banking-lending-insurance coordination

- Discretionary mandates & advisory fees

Risk & compliance

Cullen/Frost maintains strong credit, market, liquidity, operational, and cyber risk frameworks that protect the franchise and align with 2024 regulatory expectations; AML/BSA, KYC, and consumer compliance programs drive ongoing regulatory alignment. Stress testing and capital planning in 2024 prepare the bank for downturn scenarios. Robust vendor and model risk management fortify enterprise resilience.

- 2024: ongoing stress tests & capital planning

- AML/BSA, KYC, consumer compliance

- Credit, market, liquidity, operational, cyber controls

- Vendor & model risk management

UW-led: $33.5B loans, >$40B deposits, 0.42% NPL

Underwriting and portfolio management drive interest income across a $33.5B loan book (12/31/2024) with NPL ratio ~0.42% in 2024, supported by stress testing and Texas-tailored credit policy. Stable funding from >$40B deposits sustains margin and liquidity. Payments, treasury, wealth, and risk controls generate fee income and protect the franchise.

| Metric | 2024 |

|---|---|

| Loan book | $33.5B |

| Deposits | >$40B |

| NPL ratio | 0.42% |

| ACH volume | ~30B |

Full Document Unlocks After Purchase

Business Model Canvas

The Cullen/Frost Bank Business Model Canvas you’re previewing is the exact deliverable—not a mockup—and includes the same content you’ll receive after purchase. When you complete your order you’ll get this full, ready-to-edit document in Word and Excel formats, formatted and structured exactly as shown.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a regional bank's strategic blueprint with our Business Model Canvas

Unlock Cullen/Frost Bank’s strategic blueprint with our Business Model Canvas. This concise, section-by-section canvas reveals value propositions, revenue streams, partnerships and cost drivers to inform investors, consultants, and founders. Purchase the full Word/Excel package for actionable analysis and ready-to-use templates.

Partnerships

Payment networks

Partnerships with Visa, Mastercard, ACH, and Fedwire give Cullen/Frost seamless card issuance and payments across Texas and nationally, leveraging networks that process over $3 trillion daily on Fedwire and more than 30 billion ACH transactions annually. These partners provide scale, advanced fraud tools, and interchange connectivity, enabling Frost to deliver fast, reliable consumer and business transactions. Strong ties bolster treasury, merchant, and debit/credit services.

Core & fintech vendors

Alliances with core banking platforms, cloud providers, and fintechs accelerate digital features and operational resilience, with McKinsey 2024 finding cloud migration can cut IT costs 20–30%. Vendors enable mobile apps, APIs, data analytics, and cybersecurity to expand services and fraud defense. Co-development shortens time-to-market for customer-facing innovations, while integration partners modernize legacy stacks with minimal service disruption.

Broker-dealers & custodians

Broker-dealers and custodians provide Cullen/Frost investment services with trade execution, safekeeping, and access to products, leveraging custodian platforms that together hold trillions of dollars in client assets as of 2024. These partnerships expand offerings to mutual funds, ETFs, fixed income and alternatives, enabling scalable, compliant wealth-management operations. Clients gain diversified choices and operational efficiency through integrated custody and execution services.

Insurance carriers

Insurance carriers supply property-casualty, life, and specialty coverage distributed through Frost, broadening risk solutions for businesses and individuals; Cullen/Frost reported total assets of $46.9 billion in 2024, supporting expanded product distribution. Joint marketing and underwriting expertise improve product fit and pricing while cross-sell drives fee income and deeper client relationships.

- Carriers: broaden risk portfolio

- Joint underwriting: better pricing

- Cross-sell: fee income growth

Community & commercial partners

Local chambers, economic development groups, and industry associations connect Frost to Texas businesses, generating qualified leads and community trust and supporting SBA lending and CRA initiatives. These collaborations drove regional growth in 2024 and reinforce Frost’s brand as a relationship-first Texas bank with 160+ branches across the state (2024).

- Local chambers

- Economic development groups

- Industry associations

- 160+ branches (2024)

Nationwide payment rails, cloud agility and custodial alliances power treasury and wealth services

Partnerships with Visa, Mastercard, ACH and Fedwire enable nationwide payments (Fedwire $3T/day; ACH >30B txns/yr) and support treasury, merchant and card services. Alliances with core platforms, cloud and fintechs speed digital features and resilience (cloud can cut IT costs 20–30% per McKinsey 2024). Custodians/broker-dealers and insurers expand wealth and risk offerings; Frost reported $46.9B assets and 160+ branches (2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Payments (Visa/Mastercard/Fedwire/ACH) | Payments/settlement | Fedwire $3T/day; ACH >30B/yr |

| Cloud/Fintech | Digital/ops | IT costs -20–30% |

| Custodians/Brokers | Wealth services | Supports diversified products |

| Insurers/Local partners | Risk distribution & leads | $46.9B assets; 160+ branches |

What is included in the product

A comprehensive, pre-written Cullen/Frost Bank Business Model Canvas outlining customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations and competitive advantages, with linked SWOT analysis for investor presentations and strategic decision-making.

High-level view of Cullen/Frost Bank's business model with editable cells, saving hours of structuring and formatting while enabling shareable, collaborative snapshots for quick executive summaries and board-ready presentations.

Activities

Lending & credit

Underwriting and portfolio management for commercial, real estate, and consumer loans drive Cullen/Frost’s interest income across a $33.5B loan book (12/31/2024), while risk models and relationship insights shape pricing and exposure limits. Continuous monitoring and stress-testing kept the nonperforming loan ratio near 0.42% in 2024, protecting asset quality through cycles. Credit policy is tailored to Texas market dynamics and regulatory standards.

Deposit gathering

Acquiring low-cost, sticky deposits sustains margin and liquidity for Cullen/Frost, which held over $40 billion in deposits in 2024; this stable base cushions net interest margin and funding volatility. Branch teams, digital onboarding, and targeted campaigns attract households and businesses, while cash management solutions retain operating balances. Pricing, service, and trust support multi-decade relationships.

Treasury & payments

Treasury and payments deliver faster, secure payment and receivables solutions—ACH, wires, RDC, merchant services and lockbox—streamlining cash conversion cycles and supporting over 30 billion ACH payments annually by 2024. Robust fraud prevention and layered controls reduce losses and exposure across business portfolios. Deep ERP integrations and open APIs boost client stickiness and recurring fee income for Cullen/Frost.

Wealth & advisory

Wealth & advisory integrates investment management, trust, brokerage, and planning to deepen wallet share, with research-driven asset allocation and fiduciary oversight directing client outcomes. Advisors coordinate banking, lending, and insurance strategies, while discretionary mandates and advisory fees create recurring revenue streams in 2024.

- Investment management

- Fiduciary oversight

- Banking-lending-insurance coordination

- Discretionary mandates & advisory fees

Risk & compliance

Cullen/Frost maintains strong credit, market, liquidity, operational, and cyber risk frameworks that protect the franchise and align with 2024 regulatory expectations; AML/BSA, KYC, and consumer compliance programs drive ongoing regulatory alignment. Stress testing and capital planning in 2024 prepare the bank for downturn scenarios. Robust vendor and model risk management fortify enterprise resilience.

- 2024: ongoing stress tests & capital planning

- AML/BSA, KYC, consumer compliance

- Credit, market, liquidity, operational, cyber controls

- Vendor & model risk management

UW-led: $33.5B loans, >$40B deposits, 0.42% NPL

Underwriting and portfolio management drive interest income across a $33.5B loan book (12/31/2024) with NPL ratio ~0.42% in 2024, supported by stress testing and Texas-tailored credit policy. Stable funding from >$40B deposits sustains margin and liquidity. Payments, treasury, wealth, and risk controls generate fee income and protect the franchise.

| Metric | 2024 |

|---|---|

| Loan book | $33.5B |

| Deposits | >$40B |

| NPL ratio | 0.42% |

| ACH volume | ~30B |

Full Document Unlocks After Purchase

Business Model Canvas

The Cullen/Frost Bank Business Model Canvas you’re previewing is the exact deliverable—not a mockup—and includes the same content you’ll receive after purchase. When you complete your order you’ll get this full, ready-to-edit document in Word and Excel formats, formatted and structured exactly as shown.