Cullen/Frost Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cullen/Frost Bank operates in a competitive regional banking market shaped by tight margins, regulatory pressure, and evolving fintech threats. Our Porter’s Five Forces snapshot highlights buyer leverage, rivalry intensity, supplier influence, and substitution risk. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated tech vendors

Core banking, payments and cybersecurity vendors are concentrated—FIS, Fiserv, Jack Henry and Temenos held roughly 70% of US core/payment footprints by 2024—giving suppliers significant pricing and contract leverage.

High switching costs from integrations and regulatory scrutiny lock Cullen/Frost in, so it relies on multi-year contracts and vendor diversification to mitigate risk, though mandatory upgrades and compliance-driven changes still tilt power toward suppliers.

Funding mix dependence

Depositors, wholesale lenders and capital markets supply funding for Cullen/Frost; as of 2024 core deposits accounted for roughly 80% of total funding, muting supplier leverage. Dependence on brokered or wholesale funds would raise supplier power, and rate-cycle-driven deposit outflows can quickly shift bargaining advantage to funding providers. Frost’s Texas relationship banking anchors sticky core funding and limits volatility.

Talent and compliance expertise

Tight 2024 labor markets (US unemployment averaged 3.7% per BLS) increase supplier power for Cullen/Frost as specialized bankers, risk managers and compliance staff command premium compensation. Strong retention and culture reduce that leverage, while training pipelines and internal mobility lower dependence on costly external hires.

Regulatory infrastructure

Access to Federal Reserve services and government backstops is essential for Cullen/Frost but conditional; Basel III minimum CET1 is 4.5% and Tier 1 6.0%, which regulators enforce and which shape funding cost and capital strategy. Regulators act like suppliers by imposing operating constraints; compliance failures increase effective supplier power via remediation, fines and mandated capital actions, while strong governance mitigates those risks.

- Regulatory access: Fed backstops conditional

- Capital floors: CET1 4.5%, Tier1 6.0%

- Noncompliance: raises remediation costs

- Governance: lowers regulator-induced risk

Data and credit bureaus

Data and credit bureaus (Equifax, Experian, TransUnion) supply core credit files and analytics that underwrite and monitor risk, with the big three accounting for roughly 85–90% of U.S. credit reporting volume in 2024; vendor concentration and bundled services elevate switching costs and integration timelines.

Banks offset costs via enterprise agreements that can trim per-report pricing 15–25%, while growing adoption of alternative data (≈25% y/y gain in 2024) increases options but adds integration complexity and validation burden.

- Vendor concentration: ~85–90% market share

- Enterprise deals: -15–25% unit cost

- Alt-data growth: ~25% y/y (2024)

Core tech, credit bureaus and deposits give suppliers strong leverage

Core tech/payments concentrated (FIS/Fiserv/Jack Henry/Temenos ~70% US, 2024) and credit bureaus ~85–90% give suppliers pricing/leverage. High integration/switching costs, compliance-driven upgrades and multiyear contracts lock Cullen/Frost in; enterprise deals cut unit costs 15–25%. Core deposits ~80% of funding (2024) and Texas relationship banking limit funder power, but tight labor (U.S. unemployment 3.7% 2024) and capital floors (CET1 4.5%, Tier1 6.0%) sustain supplier influence.

| Metric | 2024/Value |

|---|---|

| Core tech share | ~70% |

| Credit bureaus share | 85–90% |

| Core deposits | ~80% |

| Unemployment (US) | 3.7% |

| Enterprise deal saving | -15–25% |

| Alt-data growth | ~25% y/y |

What is included in the product

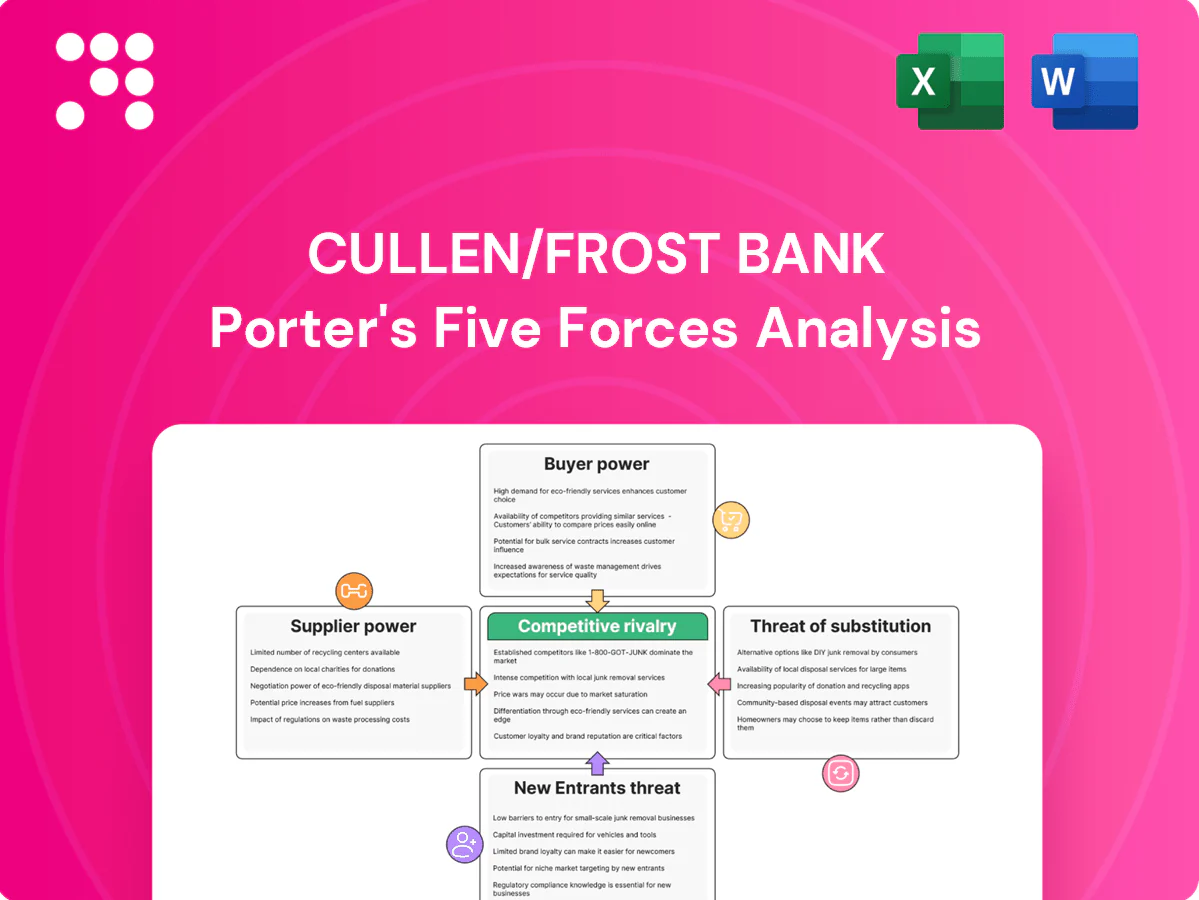

Concise Porter’s Five Forces assessment of Cullen/Frost Bank highlighting competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and regulatory barriers—identifying strategic risks and defensive advantages.

Concise Porter's Five Forces for Cullen/Frost—one-sheet with a spider chart and customizable pressure levels, no macros, easy Excel integration and deck-ready layout to quickly identify competitive pain points and strategic levers.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can instantly compare yields across banks and money funds—with Fed funds near 5.25–5.50% and online money-market yields around 4.5–5% in 2024—raising customer bargaining power. Rising rates amplify churn risk unless Cullen/Frost adjusts pricing. The bank offsets this with high-touch service and deep commercial relationships. Segmentation enables targeted pricing to retain higher-value accounts.

Commercial client leverage

Middle-market and corporate clients often multi-bank and leverage competitive bids to negotiate fees and covenants, with treasury management and credit lines routinely rebid; Cullen/Frost reported over $70 billion in assets in 2024, underscoring its scale in those contests. Bundled solutions raise switching costs and dilute buyer power, while relationship managers and local credit decisioning strengthen retention and reduce churn.

Digital service expectations

Customers now expect seamless mobile, API, and real-time payments: 2024 surveys show about 82% of U.S. consumers use mobile banking and real-time payments volumes rose over 30% YoY in 2023, pressuring Frost as feature gaps drive migration—roughly 40% of users say they'd switch for better digital services. Continuous UX upgrades reduce buyer leverage while service-level reliability becomes a competitive differentiator beyond price.

Information transparency

Rate tables, fee disclosures and online reviews make Cullen/Frost services easily comparable, increasing buyer leverage in commoditized deposit and lending products; advisory-led, customized solutions reduce price sensitivity by emphasizing tailored outcomes over headline rates.

Wealth and insurance cross-sell

Affluent clients can readily shop investment and insurance products, increasing their bargaining power as open architecture platforms widen provider choice. Integrated wealth and fiduciary advice at Cullen/Frost strengthens retention and supports premium pricing. Detailed performance reporting and trust services deepen relationships and lower churn, counterbalancing buyer leverage.

- Buyer choice: open architecture raises switching

- Retention: integrated fiduciary advice improves pricing power

- Loyalty: performance reporting and trust services reduce churn

Depositors chase yields; scale and relationship banking curb churn as digital demand rises

Customers have high bargaining power as rate-sensitive depositors chase yields (Fed funds 5.25–5.50%; online MM ~4.5–5% in 2024), while Frost's scale ($70B assets in 2024) and relationship banking mitigate churn. Digital expectations (82% mobile use; RTP volumes +30% YoY) and 40% switch intent for better digital services amplify nonprice competition.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| Online MM yield | 4.5–5% |

| Frost assets | $70B |

| Mobile use | 82% |

| RTP growth | +30% YoY |

| Switch intent | ~40% |

Full Version Awaits

Cullen/Frost Bank Porter's Five Forces Analysis

This preview shows the full Cullen/Frost Bank Porter’s Five Forces Analysis and is the exact document you'll receive upon purchase. It contains the complete, professionally formatted competitive assessment—no placeholders or samples. Buy and download instantly to access this same ready-to-use file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cullen/Frost Bank operates in a competitive regional banking market shaped by tight margins, regulatory pressure, and evolving fintech threats. Our Porter’s Five Forces snapshot highlights buyer leverage, rivalry intensity, supplier influence, and substitution risk. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated tech vendors

Core banking, payments and cybersecurity vendors are concentrated—FIS, Fiserv, Jack Henry and Temenos held roughly 70% of US core/payment footprints by 2024—giving suppliers significant pricing and contract leverage.

High switching costs from integrations and regulatory scrutiny lock Cullen/Frost in, so it relies on multi-year contracts and vendor diversification to mitigate risk, though mandatory upgrades and compliance-driven changes still tilt power toward suppliers.

Funding mix dependence

Depositors, wholesale lenders and capital markets supply funding for Cullen/Frost; as of 2024 core deposits accounted for roughly 80% of total funding, muting supplier leverage. Dependence on brokered or wholesale funds would raise supplier power, and rate-cycle-driven deposit outflows can quickly shift bargaining advantage to funding providers. Frost’s Texas relationship banking anchors sticky core funding and limits volatility.

Talent and compliance expertise

Tight 2024 labor markets (US unemployment averaged 3.7% per BLS) increase supplier power for Cullen/Frost as specialized bankers, risk managers and compliance staff command premium compensation. Strong retention and culture reduce that leverage, while training pipelines and internal mobility lower dependence on costly external hires.

Regulatory infrastructure

Access to Federal Reserve services and government backstops is essential for Cullen/Frost but conditional; Basel III minimum CET1 is 4.5% and Tier 1 6.0%, which regulators enforce and which shape funding cost and capital strategy. Regulators act like suppliers by imposing operating constraints; compliance failures increase effective supplier power via remediation, fines and mandated capital actions, while strong governance mitigates those risks.

- Regulatory access: Fed backstops conditional

- Capital floors: CET1 4.5%, Tier1 6.0%

- Noncompliance: raises remediation costs

- Governance: lowers regulator-induced risk

Data and credit bureaus

Data and credit bureaus (Equifax, Experian, TransUnion) supply core credit files and analytics that underwrite and monitor risk, with the big three accounting for roughly 85–90% of U.S. credit reporting volume in 2024; vendor concentration and bundled services elevate switching costs and integration timelines.

Banks offset costs via enterprise agreements that can trim per-report pricing 15–25%, while growing adoption of alternative data (≈25% y/y gain in 2024) increases options but adds integration complexity and validation burden.

- Vendor concentration: ~85–90% market share

- Enterprise deals: -15–25% unit cost

- Alt-data growth: ~25% y/y (2024)

Core tech, credit bureaus and deposits give suppliers strong leverage

Core tech/payments concentrated (FIS/Fiserv/Jack Henry/Temenos ~70% US, 2024) and credit bureaus ~85–90% give suppliers pricing/leverage. High integration/switching costs, compliance-driven upgrades and multiyear contracts lock Cullen/Frost in; enterprise deals cut unit costs 15–25%. Core deposits ~80% of funding (2024) and Texas relationship banking limit funder power, but tight labor (U.S. unemployment 3.7% 2024) and capital floors (CET1 4.5%, Tier1 6.0%) sustain supplier influence.

| Metric | 2024/Value |

|---|---|

| Core tech share | ~70% |

| Credit bureaus share | 85–90% |

| Core deposits | ~80% |

| Unemployment (US) | 3.7% |

| Enterprise deal saving | -15–25% |

| Alt-data growth | ~25% y/y |

What is included in the product

Concise Porter’s Five Forces assessment of Cullen/Frost Bank highlighting competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and regulatory barriers—identifying strategic risks and defensive advantages.

Concise Porter's Five Forces for Cullen/Frost—one-sheet with a spider chart and customizable pressure levels, no macros, easy Excel integration and deck-ready layout to quickly identify competitive pain points and strategic levers.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can instantly compare yields across banks and money funds—with Fed funds near 5.25–5.50% and online money-market yields around 4.5–5% in 2024—raising customer bargaining power. Rising rates amplify churn risk unless Cullen/Frost adjusts pricing. The bank offsets this with high-touch service and deep commercial relationships. Segmentation enables targeted pricing to retain higher-value accounts.

Commercial client leverage

Middle-market and corporate clients often multi-bank and leverage competitive bids to negotiate fees and covenants, with treasury management and credit lines routinely rebid; Cullen/Frost reported over $70 billion in assets in 2024, underscoring its scale in those contests. Bundled solutions raise switching costs and dilute buyer power, while relationship managers and local credit decisioning strengthen retention and reduce churn.

Digital service expectations

Customers now expect seamless mobile, API, and real-time payments: 2024 surveys show about 82% of U.S. consumers use mobile banking and real-time payments volumes rose over 30% YoY in 2023, pressuring Frost as feature gaps drive migration—roughly 40% of users say they'd switch for better digital services. Continuous UX upgrades reduce buyer leverage while service-level reliability becomes a competitive differentiator beyond price.

Information transparency

Rate tables, fee disclosures and online reviews make Cullen/Frost services easily comparable, increasing buyer leverage in commoditized deposit and lending products; advisory-led, customized solutions reduce price sensitivity by emphasizing tailored outcomes over headline rates.

Wealth and insurance cross-sell

Affluent clients can readily shop investment and insurance products, increasing their bargaining power as open architecture platforms widen provider choice. Integrated wealth and fiduciary advice at Cullen/Frost strengthens retention and supports premium pricing. Detailed performance reporting and trust services deepen relationships and lower churn, counterbalancing buyer leverage.

- Buyer choice: open architecture raises switching

- Retention: integrated fiduciary advice improves pricing power

- Loyalty: performance reporting and trust services reduce churn

Depositors chase yields; scale and relationship banking curb churn as digital demand rises

Customers have high bargaining power as rate-sensitive depositors chase yields (Fed funds 5.25–5.50%; online MM ~4.5–5% in 2024), while Frost's scale ($70B assets in 2024) and relationship banking mitigate churn. Digital expectations (82% mobile use; RTP volumes +30% YoY) and 40% switch intent for better digital services amplify nonprice competition.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| Online MM yield | 4.5–5% |

| Frost assets | $70B |

| Mobile use | 82% |

| RTP growth | +30% YoY |

| Switch intent | ~40% |

Full Version Awaits

Cullen/Frost Bank Porter's Five Forces Analysis

This preview shows the full Cullen/Frost Bank Porter’s Five Forces Analysis and is the exact document you'll receive upon purchase. It contains the complete, professionally formatted competitive assessment—no placeholders or samples. Buy and download instantly to access this same ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cullen/Frost Bank operates in a competitive regional banking market shaped by tight margins, regulatory pressure, and evolving fintech threats. Our Porter’s Five Forces snapshot highlights buyer leverage, rivalry intensity, supplier influence, and substitution risk. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated tech vendors

Core banking, payments and cybersecurity vendors are concentrated—FIS, Fiserv, Jack Henry and Temenos held roughly 70% of US core/payment footprints by 2024—giving suppliers significant pricing and contract leverage.

High switching costs from integrations and regulatory scrutiny lock Cullen/Frost in, so it relies on multi-year contracts and vendor diversification to mitigate risk, though mandatory upgrades and compliance-driven changes still tilt power toward suppliers.

Funding mix dependence

Depositors, wholesale lenders and capital markets supply funding for Cullen/Frost; as of 2024 core deposits accounted for roughly 80% of total funding, muting supplier leverage. Dependence on brokered or wholesale funds would raise supplier power, and rate-cycle-driven deposit outflows can quickly shift bargaining advantage to funding providers. Frost’s Texas relationship banking anchors sticky core funding and limits volatility.

Talent and compliance expertise

Tight 2024 labor markets (US unemployment averaged 3.7% per BLS) increase supplier power for Cullen/Frost as specialized bankers, risk managers and compliance staff command premium compensation. Strong retention and culture reduce that leverage, while training pipelines and internal mobility lower dependence on costly external hires.

Regulatory infrastructure

Access to Federal Reserve services and government backstops is essential for Cullen/Frost but conditional; Basel III minimum CET1 is 4.5% and Tier 1 6.0%, which regulators enforce and which shape funding cost and capital strategy. Regulators act like suppliers by imposing operating constraints; compliance failures increase effective supplier power via remediation, fines and mandated capital actions, while strong governance mitigates those risks.

- Regulatory access: Fed backstops conditional

- Capital floors: CET1 4.5%, Tier1 6.0%

- Noncompliance: raises remediation costs

- Governance: lowers regulator-induced risk

Data and credit bureaus

Data and credit bureaus (Equifax, Experian, TransUnion) supply core credit files and analytics that underwrite and monitor risk, with the big three accounting for roughly 85–90% of U.S. credit reporting volume in 2024; vendor concentration and bundled services elevate switching costs and integration timelines.

Banks offset costs via enterprise agreements that can trim per-report pricing 15–25%, while growing adoption of alternative data (≈25% y/y gain in 2024) increases options but adds integration complexity and validation burden.

- Vendor concentration: ~85–90% market share

- Enterprise deals: -15–25% unit cost

- Alt-data growth: ~25% y/y (2024)

Core tech, credit bureaus and deposits give suppliers strong leverage

Core tech/payments concentrated (FIS/Fiserv/Jack Henry/Temenos ~70% US, 2024) and credit bureaus ~85–90% give suppliers pricing/leverage. High integration/switching costs, compliance-driven upgrades and multiyear contracts lock Cullen/Frost in; enterprise deals cut unit costs 15–25%. Core deposits ~80% of funding (2024) and Texas relationship banking limit funder power, but tight labor (U.S. unemployment 3.7% 2024) and capital floors (CET1 4.5%, Tier1 6.0%) sustain supplier influence.

| Metric | 2024/Value |

|---|---|

| Core tech share | ~70% |

| Credit bureaus share | 85–90% |

| Core deposits | ~80% |

| Unemployment (US) | 3.7% |

| Enterprise deal saving | -15–25% |

| Alt-data growth | ~25% y/y |

What is included in the product

Concise Porter’s Five Forces assessment of Cullen/Frost Bank highlighting competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and regulatory barriers—identifying strategic risks and defensive advantages.

Concise Porter's Five Forces for Cullen/Frost—one-sheet with a spider chart and customizable pressure levels, no macros, easy Excel integration and deck-ready layout to quickly identify competitive pain points and strategic levers.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors can instantly compare yields across banks and money funds—with Fed funds near 5.25–5.50% and online money-market yields around 4.5–5% in 2024—raising customer bargaining power. Rising rates amplify churn risk unless Cullen/Frost adjusts pricing. The bank offsets this with high-touch service and deep commercial relationships. Segmentation enables targeted pricing to retain higher-value accounts.

Commercial client leverage

Middle-market and corporate clients often multi-bank and leverage competitive bids to negotiate fees and covenants, with treasury management and credit lines routinely rebid; Cullen/Frost reported over $70 billion in assets in 2024, underscoring its scale in those contests. Bundled solutions raise switching costs and dilute buyer power, while relationship managers and local credit decisioning strengthen retention and reduce churn.

Digital service expectations

Customers now expect seamless mobile, API, and real-time payments: 2024 surveys show about 82% of U.S. consumers use mobile banking and real-time payments volumes rose over 30% YoY in 2023, pressuring Frost as feature gaps drive migration—roughly 40% of users say they'd switch for better digital services. Continuous UX upgrades reduce buyer leverage while service-level reliability becomes a competitive differentiator beyond price.

Information transparency

Rate tables, fee disclosures and online reviews make Cullen/Frost services easily comparable, increasing buyer leverage in commoditized deposit and lending products; advisory-led, customized solutions reduce price sensitivity by emphasizing tailored outcomes over headline rates.

Wealth and insurance cross-sell

Affluent clients can readily shop investment and insurance products, increasing their bargaining power as open architecture platforms widen provider choice. Integrated wealth and fiduciary advice at Cullen/Frost strengthens retention and supports premium pricing. Detailed performance reporting and trust services deepen relationships and lower churn, counterbalancing buyer leverage.

- Buyer choice: open architecture raises switching

- Retention: integrated fiduciary advice improves pricing power

- Loyalty: performance reporting and trust services reduce churn

Depositors chase yields; scale and relationship banking curb churn as digital demand rises

Customers have high bargaining power as rate-sensitive depositors chase yields (Fed funds 5.25–5.50%; online MM ~4.5–5% in 2024), while Frost's scale ($70B assets in 2024) and relationship banking mitigate churn. Digital expectations (82% mobile use; RTP volumes +30% YoY) and 40% switch intent for better digital services amplify nonprice competition.

| Metric | 2024 |

|---|---|

| Fed funds | 5.25–5.50% |

| Online MM yield | 4.5–5% |

| Frost assets | $70B |

| Mobile use | 82% |

| RTP growth | +30% YoY |

| Switch intent | ~40% |

Full Version Awaits

Cullen/Frost Bank Porter's Five Forces Analysis

This preview shows the full Cullen/Frost Bank Porter’s Five Forces Analysis and is the exact document you'll receive upon purchase. It contains the complete, professionally formatted competitive assessment—no placeholders or samples. Buy and download instantly to access this same ready-to-use file.