Fuchs Petrolub SE Porter's Five Forces Analysis

Don't Miss the Bigger Picture

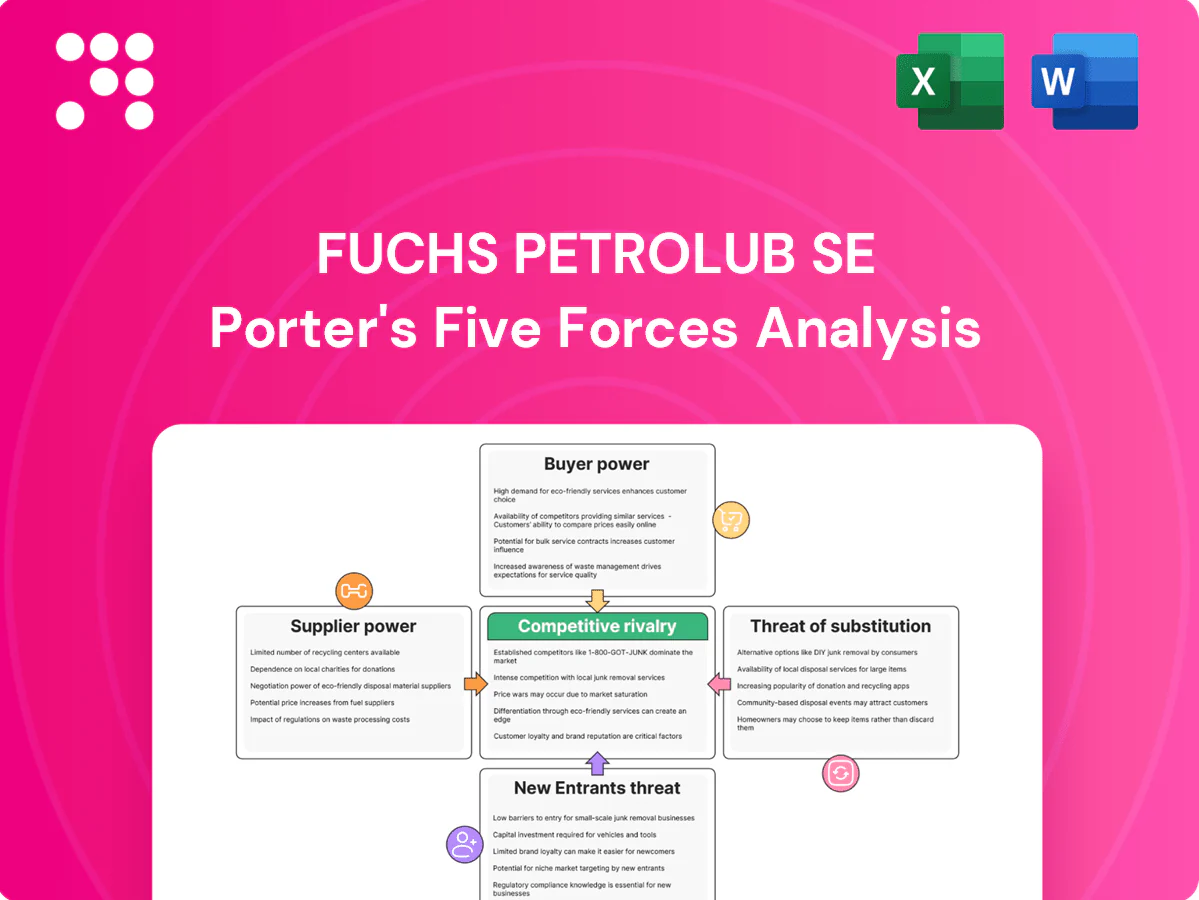

Fuchs Petrolub SE faces moderate supplier power, strong buyer expectations for quality and sustainability, and a mixed threat from substitutes as EVs and synthetics evolve. Competitive rivalry is high among global lubricant specialists, while barriers curb but don’t eliminate new entrants. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated base oil and additives sources

Large additive suppliers and regional base oil oligopolies keep bargaining power moderate-to-high, with proprietary additive packages and OEM approvals creating high switching costs. Fuchs reported roughly €2.1bn revenue in 2024, using multi-sourcing and long-term contracts to reduce input risk. Sudden supply shocks still compress margins, as seen in recent base oil price volatility. The company’s global footprint lets it rebalance volumes across regions to mitigate localized shortages.

Specification lock-in and qualification needs

Many lubricant formulations are tied to OEM-qualified chemistries, making supplier switches slow; industry requalification cycles typically run 6–18 months and can cost over €100,000 per SKU, giving incumbents leverage on critical items. Requalification complexity and cost limit buyer bargaining power. Fuchs mitigates this by expanding acceptable formulation windows through in-house R&D and global technical service teams, reducing switch barriers for customers.

Commodity volatility pass-through

Base oil and additive price swings materially influence Fuchs Petrolub SE COGS, forcing pricing pass-throughs to customers; base oil benchmarks rose roughly 18% year-on-year in H1 2024, compressing margins when contracts lag price adjustments. Time lags and fixed customer contracts can squeeze margins during spikes, and suppliers have applied surcharges or allocations in tight markets. Fuchs offsets volatility through hedging programs and inventory planning to smooth cost impacts.

Specialty chemicals scarcity

Certain anti-wear, detergent and ester components are produced by few manufacturers and face long lead times; REACH lists over 22,000 registered substances and the US TSCA inventory contains roughly 86,000 chemicals, tightening compliant sourcing. Supply disruptions hit premium and niche lubricants disproportionately, while strategic stocks and closer supplier collaboration materially reduce outage risk.

- Limited producers: concentration risk

- Regulatory scope: REACH >22,000, TSCA ~86,000

- Impact: premium/niche products most exposed

- Mitigation: strategic stocks + supplier collaboration

Packaging and logistics dependencies

Drums, totes and additives transportation remain exposed to freight and resin price cycles, with regional port or road bottlenecks raising supplier leverage during peak periods.

Fuchs’s networked plants and local sourcing reduce single-point exposure by shifting volumes across sites and suppliers.

Standardized packaging specifications increase substitutability and lower switching costs for packaging vendors.

- Packaging types: drums/totes/additives

- Risks: freight/resin volatility, regional bottlenecks

- Mitigants: networked plants, local sourcing, standardization

Base oil spike (+18%) & requal. costs (€100k+) power

Large additive suppliers and regional base oil oligopolies give suppliers moderate-high power; proprietary chemistries and OEM approvals raise switching costs. Fuchs €2.1bn 2024 revenue; base oil benchmarks +18% YoY H1 2024 compressed margins. Fuchs uses multi-sourcing, hedging, inventories and networked plants to mitigate risk.

| Metric | Value |

|---|---|

| Revenue 2024 | €2.1bn |

| Base oil Δ H1 2024 | +18% |

| Requalification | 6–18 months, >€100k/SKU |

What is included in the product

Tailored Porter's Five Forces analysis for Fuchs Petrolub SE uncovering key drivers of competition, supplier and buyer power, threat of substitutes, and barriers to entry that shape pricing and profitability; highlights disruptive forces, emerging threats, and strategic levers for protecting market share.

A concise, one-sheet Porter's Five Forces for Fuchs Petrolub SE—instantly visualizes supplier, buyer, entrant, substitute and rivalry pressures to speed strategic decisions. Clean layout and easy data swaps let non-experts customize scenarios (regulatory shifts, raw material shocks) and drop directly into decks.

Customers Bargaining Power

OEMs and industrial majors wield scale

Automotive OEMs, Tier-1s and large industrials exert strong bargaining power, negotiating aggressively through tenders where volume concentration and multi-year contracts amplify leverage. They demand rigorous technical support, sustainability compliance and pricing concessions tied to long-term supply. Fuchs counters by proving value-in-use, offering co-engineering, tailored formulations and total-cost-of-ownership reductions to retain business.

Switching costs via approvals and warranties

Once a lubricant is approved and validated for machinery or vehicles, customers incur testing, qualification time and potential production downtime to switch suppliers, creating meaningful switching costs. Warranty exposure and compliance risks, including liability for component failure, deter frequent changes and reduce propensity to chase marginal price savings. This technical and contractual stickiness tempers buyer power despite overall price sensitivity. High-quality service, on-site support and tailored formulations further deepen lock-in.

Aftermarket fragmentation softens leverage

SMB industrial users and retail/independent workshops are highly fragmented, which reduces their individual bargaining clout versus large OEMs. Brand trust and rapid local service often trump price for these buyers. Fuchs’s distributor network, present in over 50 countries, captures this segment by emphasizing availability and technical support. Fragmentation therefore softens customer leverage.

Transparency and price benchmarking

Platts and Argus base-oil indices and public specs make price benchmarking straightforward, enabling rapid comparisons. The global lubricants market was around 40 billion USD in 2024, letting large buyers cross-bid global brands and private labels and increasing price pressure on standard commodity grades. Differentiated specialty fluids face less direct benchmarking and preserve higher margins.

- Index-driven pricing: easier cross-supplier comparison

- Market size 2024: ~40 billion USD

- Standard grades: intensified price pressure

- Specialties: lower direct benchmarking, higher margin resilience

Demand shifts from electrification

EV adoption is cutting engine-oil volumes as new EVs and hybrids grew to over 14% of global light‑vehicle sales in 2023, driving buyers to demand longer drain intervals and lower total cost of ownership. Fleet electrification centralizes purchasing, increasing buyer leverage and forcing suppliers to offer integrated e‑fluids and thermal management. Fuchs must defend share with e‑fluids, heat‑transfer solutions and technical partnerships to retain pricing power.

- Impact: lower lubricant volumes; higher TCO focus

- Fleet effect: consolidated procurement amplifies bargaining power

- Defense: e‑fluids, thermal management, tech partnerships

OEM tenders squeeze margins; co-engineering shields pricing; EVs 14% cut oil

Large OEMs/Tier‑1s and fleets exert strong price leverage via tenders and consolidated procurement; Fuchs offsets with co‑engineering, validated specs and service to protect margins. High switching costs and warranty risks reduce churn despite index price transparency; specialties remain less exposed. EVs (14% LV sales 2023) lower engine‑oil volumes, raising buyer focus on TCO.

| Metric | Value |

|---|---|

| Global market 2024 | ~40bn USD |

| EV share 2023 | 14% |

| Distributor footprint | 50+ countries |

Preview Before You Purchase

Fuchs Petrolub SE Porter's Five Forces Analysis

This Fuchs Petrolub SE Porter's Five Forces analysis is the exact, professionally formatted document you see in preview. It covers competitive rivalry, supplier and buyer power, threat of entry and substitutes. No mockups or placeholders—download the same file instantly after purchase.

Don't Miss the Bigger Picture

Fuchs Petrolub SE faces moderate supplier power, strong buyer expectations for quality and sustainability, and a mixed threat from substitutes as EVs and synthetics evolve. Competitive rivalry is high among global lubricant specialists, while barriers curb but don’t eliminate new entrants. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated base oil and additives sources

Large additive suppliers and regional base oil oligopolies keep bargaining power moderate-to-high, with proprietary additive packages and OEM approvals creating high switching costs. Fuchs reported roughly €2.1bn revenue in 2024, using multi-sourcing and long-term contracts to reduce input risk. Sudden supply shocks still compress margins, as seen in recent base oil price volatility. The company’s global footprint lets it rebalance volumes across regions to mitigate localized shortages.

Specification lock-in and qualification needs

Many lubricant formulations are tied to OEM-qualified chemistries, making supplier switches slow; industry requalification cycles typically run 6–18 months and can cost over €100,000 per SKU, giving incumbents leverage on critical items. Requalification complexity and cost limit buyer bargaining power. Fuchs mitigates this by expanding acceptable formulation windows through in-house R&D and global technical service teams, reducing switch barriers for customers.

Commodity volatility pass-through

Base oil and additive price swings materially influence Fuchs Petrolub SE COGS, forcing pricing pass-throughs to customers; base oil benchmarks rose roughly 18% year-on-year in H1 2024, compressing margins when contracts lag price adjustments. Time lags and fixed customer contracts can squeeze margins during spikes, and suppliers have applied surcharges or allocations in tight markets. Fuchs offsets volatility through hedging programs and inventory planning to smooth cost impacts.

Specialty chemicals scarcity

Certain anti-wear, detergent and ester components are produced by few manufacturers and face long lead times; REACH lists over 22,000 registered substances and the US TSCA inventory contains roughly 86,000 chemicals, tightening compliant sourcing. Supply disruptions hit premium and niche lubricants disproportionately, while strategic stocks and closer supplier collaboration materially reduce outage risk.

- Limited producers: concentration risk

- Regulatory scope: REACH >22,000, TSCA ~86,000

- Impact: premium/niche products most exposed

- Mitigation: strategic stocks + supplier collaboration

Packaging and logistics dependencies

Drums, totes and additives transportation remain exposed to freight and resin price cycles, with regional port or road bottlenecks raising supplier leverage during peak periods.

Fuchs’s networked plants and local sourcing reduce single-point exposure by shifting volumes across sites and suppliers.

Standardized packaging specifications increase substitutability and lower switching costs for packaging vendors.

- Packaging types: drums/totes/additives

- Risks: freight/resin volatility, regional bottlenecks

- Mitigants: networked plants, local sourcing, standardization

Base oil spike (+18%) & requal. costs (€100k+) power

Large additive suppliers and regional base oil oligopolies give suppliers moderate-high power; proprietary chemistries and OEM approvals raise switching costs. Fuchs €2.1bn 2024 revenue; base oil benchmarks +18% YoY H1 2024 compressed margins. Fuchs uses multi-sourcing, hedging, inventories and networked plants to mitigate risk.

| Metric | Value |

|---|---|

| Revenue 2024 | €2.1bn |

| Base oil Δ H1 2024 | +18% |

| Requalification | 6–18 months, >€100k/SKU |

What is included in the product

Tailored Porter's Five Forces analysis for Fuchs Petrolub SE uncovering key drivers of competition, supplier and buyer power, threat of substitutes, and barriers to entry that shape pricing and profitability; highlights disruptive forces, emerging threats, and strategic levers for protecting market share.

A concise, one-sheet Porter's Five Forces for Fuchs Petrolub SE—instantly visualizes supplier, buyer, entrant, substitute and rivalry pressures to speed strategic decisions. Clean layout and easy data swaps let non-experts customize scenarios (regulatory shifts, raw material shocks) and drop directly into decks.

Customers Bargaining Power

OEMs and industrial majors wield scale

Automotive OEMs, Tier-1s and large industrials exert strong bargaining power, negotiating aggressively through tenders where volume concentration and multi-year contracts amplify leverage. They demand rigorous technical support, sustainability compliance and pricing concessions tied to long-term supply. Fuchs counters by proving value-in-use, offering co-engineering, tailored formulations and total-cost-of-ownership reductions to retain business.

Switching costs via approvals and warranties

Once a lubricant is approved and validated for machinery or vehicles, customers incur testing, qualification time and potential production downtime to switch suppliers, creating meaningful switching costs. Warranty exposure and compliance risks, including liability for component failure, deter frequent changes and reduce propensity to chase marginal price savings. This technical and contractual stickiness tempers buyer power despite overall price sensitivity. High-quality service, on-site support and tailored formulations further deepen lock-in.

Aftermarket fragmentation softens leverage

SMB industrial users and retail/independent workshops are highly fragmented, which reduces their individual bargaining clout versus large OEMs. Brand trust and rapid local service often trump price for these buyers. Fuchs’s distributor network, present in over 50 countries, captures this segment by emphasizing availability and technical support. Fragmentation therefore softens customer leverage.

Transparency and price benchmarking

Platts and Argus base-oil indices and public specs make price benchmarking straightforward, enabling rapid comparisons. The global lubricants market was around 40 billion USD in 2024, letting large buyers cross-bid global brands and private labels and increasing price pressure on standard commodity grades. Differentiated specialty fluids face less direct benchmarking and preserve higher margins.

- Index-driven pricing: easier cross-supplier comparison

- Market size 2024: ~40 billion USD

- Standard grades: intensified price pressure

- Specialties: lower direct benchmarking, higher margin resilience

Demand shifts from electrification

EV adoption is cutting engine-oil volumes as new EVs and hybrids grew to over 14% of global light‑vehicle sales in 2023, driving buyers to demand longer drain intervals and lower total cost of ownership. Fleet electrification centralizes purchasing, increasing buyer leverage and forcing suppliers to offer integrated e‑fluids and thermal management. Fuchs must defend share with e‑fluids, heat‑transfer solutions and technical partnerships to retain pricing power.

- Impact: lower lubricant volumes; higher TCO focus

- Fleet effect: consolidated procurement amplifies bargaining power

- Defense: e‑fluids, thermal management, tech partnerships

OEM tenders squeeze margins; co-engineering shields pricing; EVs 14% cut oil

Large OEMs/Tier‑1s and fleets exert strong price leverage via tenders and consolidated procurement; Fuchs offsets with co‑engineering, validated specs and service to protect margins. High switching costs and warranty risks reduce churn despite index price transparency; specialties remain less exposed. EVs (14% LV sales 2023) lower engine‑oil volumes, raising buyer focus on TCO.

| Metric | Value |

|---|---|

| Global market 2024 | ~40bn USD |

| EV share 2023 | 14% |

| Distributor footprint | 50+ countries |

Preview Before You Purchase

Fuchs Petrolub SE Porter's Five Forces Analysis

This Fuchs Petrolub SE Porter's Five Forces analysis is the exact, professionally formatted document you see in preview. It covers competitive rivalry, supplier and buyer power, threat of entry and substitutes. No mockups or placeholders—download the same file instantly after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Fuchs Petrolub SE faces moderate supplier power, strong buyer expectations for quality and sustainability, and a mixed threat from substitutes as EVs and synthetics evolve. Competitive rivalry is high among global lubricant specialists, while barriers curb but don’t eliminate new entrants. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated base oil and additives sources

Large additive suppliers and regional base oil oligopolies keep bargaining power moderate-to-high, with proprietary additive packages and OEM approvals creating high switching costs. Fuchs reported roughly €2.1bn revenue in 2024, using multi-sourcing and long-term contracts to reduce input risk. Sudden supply shocks still compress margins, as seen in recent base oil price volatility. The company’s global footprint lets it rebalance volumes across regions to mitigate localized shortages.

Specification lock-in and qualification needs

Many lubricant formulations are tied to OEM-qualified chemistries, making supplier switches slow; industry requalification cycles typically run 6–18 months and can cost over €100,000 per SKU, giving incumbents leverage on critical items. Requalification complexity and cost limit buyer bargaining power. Fuchs mitigates this by expanding acceptable formulation windows through in-house R&D and global technical service teams, reducing switch barriers for customers.

Commodity volatility pass-through

Base oil and additive price swings materially influence Fuchs Petrolub SE COGS, forcing pricing pass-throughs to customers; base oil benchmarks rose roughly 18% year-on-year in H1 2024, compressing margins when contracts lag price adjustments. Time lags and fixed customer contracts can squeeze margins during spikes, and suppliers have applied surcharges or allocations in tight markets. Fuchs offsets volatility through hedging programs and inventory planning to smooth cost impacts.

Specialty chemicals scarcity

Certain anti-wear, detergent and ester components are produced by few manufacturers and face long lead times; REACH lists over 22,000 registered substances and the US TSCA inventory contains roughly 86,000 chemicals, tightening compliant sourcing. Supply disruptions hit premium and niche lubricants disproportionately, while strategic stocks and closer supplier collaboration materially reduce outage risk.

- Limited producers: concentration risk

- Regulatory scope: REACH >22,000, TSCA ~86,000

- Impact: premium/niche products most exposed

- Mitigation: strategic stocks + supplier collaboration

Packaging and logistics dependencies

Drums, totes and additives transportation remain exposed to freight and resin price cycles, with regional port or road bottlenecks raising supplier leverage during peak periods.

Fuchs’s networked plants and local sourcing reduce single-point exposure by shifting volumes across sites and suppliers.

Standardized packaging specifications increase substitutability and lower switching costs for packaging vendors.

- Packaging types: drums/totes/additives

- Risks: freight/resin volatility, regional bottlenecks

- Mitigants: networked plants, local sourcing, standardization

Base oil spike (+18%) & requal. costs (€100k+) power

Large additive suppliers and regional base oil oligopolies give suppliers moderate-high power; proprietary chemistries and OEM approvals raise switching costs. Fuchs €2.1bn 2024 revenue; base oil benchmarks +18% YoY H1 2024 compressed margins. Fuchs uses multi-sourcing, hedging, inventories and networked plants to mitigate risk.

| Metric | Value |

|---|---|

| Revenue 2024 | €2.1bn |

| Base oil Δ H1 2024 | +18% |

| Requalification | 6–18 months, >€100k/SKU |

What is included in the product

Tailored Porter's Five Forces analysis for Fuchs Petrolub SE uncovering key drivers of competition, supplier and buyer power, threat of substitutes, and barriers to entry that shape pricing and profitability; highlights disruptive forces, emerging threats, and strategic levers for protecting market share.

A concise, one-sheet Porter's Five Forces for Fuchs Petrolub SE—instantly visualizes supplier, buyer, entrant, substitute and rivalry pressures to speed strategic decisions. Clean layout and easy data swaps let non-experts customize scenarios (regulatory shifts, raw material shocks) and drop directly into decks.

Customers Bargaining Power

OEMs and industrial majors wield scale

Automotive OEMs, Tier-1s and large industrials exert strong bargaining power, negotiating aggressively through tenders where volume concentration and multi-year contracts amplify leverage. They demand rigorous technical support, sustainability compliance and pricing concessions tied to long-term supply. Fuchs counters by proving value-in-use, offering co-engineering, tailored formulations and total-cost-of-ownership reductions to retain business.

Switching costs via approvals and warranties

Once a lubricant is approved and validated for machinery or vehicles, customers incur testing, qualification time and potential production downtime to switch suppliers, creating meaningful switching costs. Warranty exposure and compliance risks, including liability for component failure, deter frequent changes and reduce propensity to chase marginal price savings. This technical and contractual stickiness tempers buyer power despite overall price sensitivity. High-quality service, on-site support and tailored formulations further deepen lock-in.

Aftermarket fragmentation softens leverage

SMB industrial users and retail/independent workshops are highly fragmented, which reduces their individual bargaining clout versus large OEMs. Brand trust and rapid local service often trump price for these buyers. Fuchs’s distributor network, present in over 50 countries, captures this segment by emphasizing availability and technical support. Fragmentation therefore softens customer leverage.

Transparency and price benchmarking

Platts and Argus base-oil indices and public specs make price benchmarking straightforward, enabling rapid comparisons. The global lubricants market was around 40 billion USD in 2024, letting large buyers cross-bid global brands and private labels and increasing price pressure on standard commodity grades. Differentiated specialty fluids face less direct benchmarking and preserve higher margins.

- Index-driven pricing: easier cross-supplier comparison

- Market size 2024: ~40 billion USD

- Standard grades: intensified price pressure

- Specialties: lower direct benchmarking, higher margin resilience

Demand shifts from electrification

EV adoption is cutting engine-oil volumes as new EVs and hybrids grew to over 14% of global light‑vehicle sales in 2023, driving buyers to demand longer drain intervals and lower total cost of ownership. Fleet electrification centralizes purchasing, increasing buyer leverage and forcing suppliers to offer integrated e‑fluids and thermal management. Fuchs must defend share with e‑fluids, heat‑transfer solutions and technical partnerships to retain pricing power.

- Impact: lower lubricant volumes; higher TCO focus

- Fleet effect: consolidated procurement amplifies bargaining power

- Defense: e‑fluids, thermal management, tech partnerships

OEM tenders squeeze margins; co-engineering shields pricing; EVs 14% cut oil

Large OEMs/Tier‑1s and fleets exert strong price leverage via tenders and consolidated procurement; Fuchs offsets with co‑engineering, validated specs and service to protect margins. High switching costs and warranty risks reduce churn despite index price transparency; specialties remain less exposed. EVs (14% LV sales 2023) lower engine‑oil volumes, raising buyer focus on TCO.

| Metric | Value |

|---|---|

| Global market 2024 | ~40bn USD |

| EV share 2023 | 14% |

| Distributor footprint | 50+ countries |

Preview Before You Purchase

Fuchs Petrolub SE Porter's Five Forces Analysis

This Fuchs Petrolub SE Porter's Five Forces analysis is the exact, professionally formatted document you see in preview. It covers competitive rivalry, supplier and buyer power, threat of entry and substitutes. No mockups or placeholders—download the same file instantly after purchase.