Funai PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

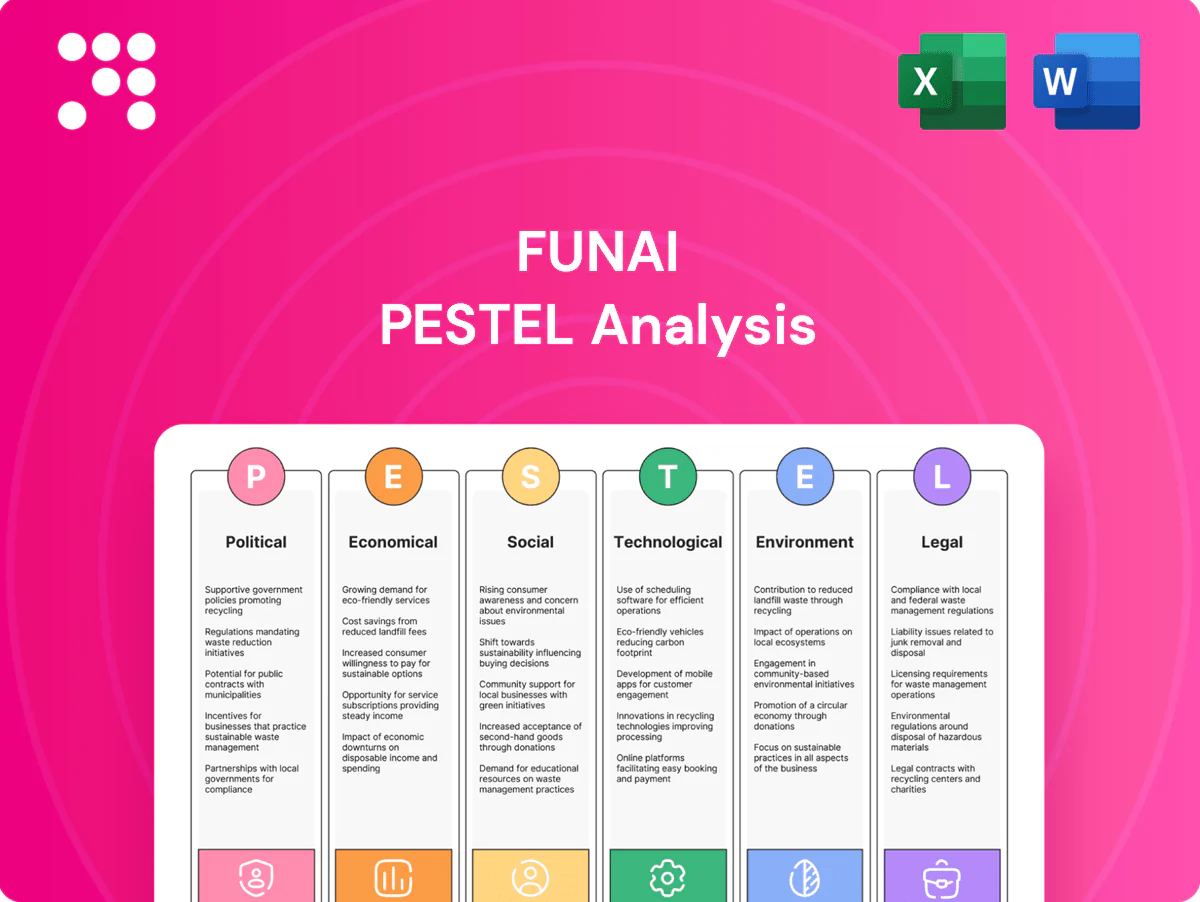

Discover how political shifts, economic trends, social dynamics, technological change, legal risks, and environmental pressures are shaping Funai’s strategic outlook. This concise PESTLE highlights key external drivers and actionable implications. Ideal for investors and strategists—purchase the full analysis for a complete, downloadable report packed with insights you can use today.

Political factors

Trade policy shifts

US–China tech tensions and export controls, which helped drive a global semiconductor market of roughly $600 billion in 2024, can disrupt component flows and market access for electronics. Japan’s alignment with allied controls on advanced chips increases sourcing risk and may complicate ODM/EMS contracts. Funai must diversify suppliers and redesign BOMs to remain compliant. Ongoing monitoring of tariff regimes and country-of-origin rules, including US tariffs up to 25%, is essential.

Industrial policy incentives

Japan has rolled out trillion-yen industrial incentives (¥1.35 trillion program for chips announced 2022), the US CHIPS Act provides about $52.7 billion for semiconductor incentives, and the EU aims to mobilize up to €43 billion for advanced manufacturing. Funai can leverage local-content incentives by partnering with regional fabs or contract assemblers to qualify for subsidies. Accessing grants requires meeting localization and workforce criteria, including local sourcing and training commitments. Strategic site selection in Japan, US or EU hubs reduces geopolitical and supply-chain risk.

Public procurement dynamics

Commercial products and IT solutions can tap rising government digitalization and education budgets, with public education spending averaging about 4% of GDP globally and global government IT investment near US$500 billion in 2024, boosting addressable markets. Procurement standards now prioritize security, energy efficiency and lifecycle support, while certification readiness can lift tender win rates materially. Building distributor-government relationships expands pipeline visibility and deal flow.

Currency and central bank posture

- FX exposure: USD/JPY ~150–160

- Financing: short-term BOJ rate ~0% vs negative prior

- Hedging: align tenor with order cycles

- Pricing: add political-risk corridors

Supply-chain resilience agendas

Semiconductor friend-shoring rises amid US–China controls; subsidies ¥1.35T and $52.7bn

US–China tech tensions and export controls (global semiconductors ≈$600bn in 2024) risk component access; Japan aligns with allied chip controls. Trillion-yen Japan incentives (¥1.35T), US CHIPS $52.7bn and EU ~€43bn shift sourcing and subsidy opportunities. Weak yen (USD/JPY ~150–160) raises import costs but aids exports; hedging and friend-shoring reduce political risk.

| Factor | Data | Impact |

|---|---|---|

| Export controls | Semis $600bn (2024) | Supply risk |

| Incentives | ¥1.35T / $52.7bn / €43bn | Localize/partner |

| FX | USD/JPY 150–160 | Margin pressure |

What is included in the product

Analyzes how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Funai, with data-backed trends, detailed subpoints and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A clean, summarized version of Funai's PESTLE analysis, visually segmented by category and written in plain language to enable quick sharing, note-taking, presentation drops, and fast alignment on external risks and market positioning.

Economic factors

Electronics demand cycles

Consumer TV and printer demand remains cyclical and mature, pressuring volumes as replacement cycles lengthen and discretionary spending fluctuates. Funai’s B2B and solutions segments provide steadier margins and contract revenue that mitigate retail volatility. Product mix optimization toward higher-margin models smooths revenue swings. Tight inventory discipline reduces markdown risk and protects gross margins.

Inflation and input costs

Components, freight and labor inflation compress Funai margins as input prices and logistics costs remain volatile; Drewry World Container Index fell from a Sept 2021 peak of US$10,377 to roughly US$1,900 in 2023–24 yet volatility still raises costs. Long-term supply agreements and design-to-cost reduce exposure. Passing through costs requires differentiated features or services. Lean operations protect EBITDA in slowdowns.

FX sensitivity (JPY)

Imported components priced in USD push Funai's COGS higher when the yen weakens; USD/JPY averaged about 145 in 2024 and spiked toward 155 in early 2025, amplifying input costs. Yen weakness can boost export competitiveness outside Japan, while dynamic hedging and USD revenue natural offsets mitigate volatility; pricing ladders should include explicit FX triggers tied to USD/JPY bands.

Print and media secular decline

Consumer printing volumes continue secular decline as digitization reduces home/page demand, shifting profit pools toward niche commercial print, consumables and managed print services; supplies account for ≈60% of OEM profit contribution while lifecycle services and subscription models stabilize cash flow and recurring revenue.

- Trend: consumer print down, commercial niche up

- Profit: consumables ≈60%

- Model: MPS/subscriptions stabilize cash flow

- R&D: prioritize high-margin specialty media

Capex and working capital

Long lead times in electronics, which peaked during 2020–22, still strain cash during demand swings; median semiconductor lead time eased to about 12 weeks in 2024, keeping inventory buffers high. Funai uses vendor-managed inventory and S&OP to improve turns, asset-light EMS partnerships to reduce fixed-capex exposure, and a strict ROIC target to guide portfolio pruning.

- Lead time ~12 weeks (2024)

- VMI + S&OP improve turns

- EMS partnerships lower fixed capex

- ROIC-driven portfolio cuts

Semiconductor friend-shoring rises amid US–China controls; subsidies ¥1.35T and $52.7bn

Consumer TV/printer demand is cyclical and mature, pressuring volumes while B2B/solutions yield steadier margins. Input inflation and logistics volatility squeeze gross margins; Drewry WCI fell from US$10,377 (Sep 2021) to ~US$1,900 (2023–24). USD/JPY ~145 (2024) raised COGS; consumables ≈60% of OEM profit. Semiconductor lead time ~12 weeks (2024).

| Metric | Value |

|---|---|

| USD/JPY (2024) | ~145 |

| Drewry WCI (2023–24) | ~US$1,900 |

| Consumables profit | ≈60% |

| Semiconductor lead time (2024) | ~12 wks |

Preview Before You Purchase

Funai PESTLE Analysis

The preview shown here is the exact Funai PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises. After checkout you’ll instantly receive this finished, professionally structured document to apply directly to your research or strategy work.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, social dynamics, technological change, legal risks, and environmental pressures are shaping Funai’s strategic outlook. This concise PESTLE highlights key external drivers and actionable implications. Ideal for investors and strategists—purchase the full analysis for a complete, downloadable report packed with insights you can use today.

Political factors

Trade policy shifts

US–China tech tensions and export controls, which helped drive a global semiconductor market of roughly $600 billion in 2024, can disrupt component flows and market access for electronics. Japan’s alignment with allied controls on advanced chips increases sourcing risk and may complicate ODM/EMS contracts. Funai must diversify suppliers and redesign BOMs to remain compliant. Ongoing monitoring of tariff regimes and country-of-origin rules, including US tariffs up to 25%, is essential.

Industrial policy incentives

Japan has rolled out trillion-yen industrial incentives (¥1.35 trillion program for chips announced 2022), the US CHIPS Act provides about $52.7 billion for semiconductor incentives, and the EU aims to mobilize up to €43 billion for advanced manufacturing. Funai can leverage local-content incentives by partnering with regional fabs or contract assemblers to qualify for subsidies. Accessing grants requires meeting localization and workforce criteria, including local sourcing and training commitments. Strategic site selection in Japan, US or EU hubs reduces geopolitical and supply-chain risk.

Public procurement dynamics

Commercial products and IT solutions can tap rising government digitalization and education budgets, with public education spending averaging about 4% of GDP globally and global government IT investment near US$500 billion in 2024, boosting addressable markets. Procurement standards now prioritize security, energy efficiency and lifecycle support, while certification readiness can lift tender win rates materially. Building distributor-government relationships expands pipeline visibility and deal flow.

Currency and central bank posture

- FX exposure: USD/JPY ~150–160

- Financing: short-term BOJ rate ~0% vs negative prior

- Hedging: align tenor with order cycles

- Pricing: add political-risk corridors

Supply-chain resilience agendas

Semiconductor friend-shoring rises amid US–China controls; subsidies ¥1.35T and $52.7bn

US–China tech tensions and export controls (global semiconductors ≈$600bn in 2024) risk component access; Japan aligns with allied chip controls. Trillion-yen Japan incentives (¥1.35T), US CHIPS $52.7bn and EU ~€43bn shift sourcing and subsidy opportunities. Weak yen (USD/JPY ~150–160) raises import costs but aids exports; hedging and friend-shoring reduce political risk.

| Factor | Data | Impact |

|---|---|---|

| Export controls | Semis $600bn (2024) | Supply risk |

| Incentives | ¥1.35T / $52.7bn / €43bn | Localize/partner |

| FX | USD/JPY 150–160 | Margin pressure |

What is included in the product

Analyzes how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Funai, with data-backed trends, detailed subpoints and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A clean, summarized version of Funai's PESTLE analysis, visually segmented by category and written in plain language to enable quick sharing, note-taking, presentation drops, and fast alignment on external risks and market positioning.

Economic factors

Electronics demand cycles

Consumer TV and printer demand remains cyclical and mature, pressuring volumes as replacement cycles lengthen and discretionary spending fluctuates. Funai’s B2B and solutions segments provide steadier margins and contract revenue that mitigate retail volatility. Product mix optimization toward higher-margin models smooths revenue swings. Tight inventory discipline reduces markdown risk and protects gross margins.

Inflation and input costs

Components, freight and labor inflation compress Funai margins as input prices and logistics costs remain volatile; Drewry World Container Index fell from a Sept 2021 peak of US$10,377 to roughly US$1,900 in 2023–24 yet volatility still raises costs. Long-term supply agreements and design-to-cost reduce exposure. Passing through costs requires differentiated features or services. Lean operations protect EBITDA in slowdowns.

FX sensitivity (JPY)

Imported components priced in USD push Funai's COGS higher when the yen weakens; USD/JPY averaged about 145 in 2024 and spiked toward 155 in early 2025, amplifying input costs. Yen weakness can boost export competitiveness outside Japan, while dynamic hedging and USD revenue natural offsets mitigate volatility; pricing ladders should include explicit FX triggers tied to USD/JPY bands.

Print and media secular decline

Consumer printing volumes continue secular decline as digitization reduces home/page demand, shifting profit pools toward niche commercial print, consumables and managed print services; supplies account for ≈60% of OEM profit contribution while lifecycle services and subscription models stabilize cash flow and recurring revenue.

- Trend: consumer print down, commercial niche up

- Profit: consumables ≈60%

- Model: MPS/subscriptions stabilize cash flow

- R&D: prioritize high-margin specialty media

Capex and working capital

Long lead times in electronics, which peaked during 2020–22, still strain cash during demand swings; median semiconductor lead time eased to about 12 weeks in 2024, keeping inventory buffers high. Funai uses vendor-managed inventory and S&OP to improve turns, asset-light EMS partnerships to reduce fixed-capex exposure, and a strict ROIC target to guide portfolio pruning.

- Lead time ~12 weeks (2024)

- VMI + S&OP improve turns

- EMS partnerships lower fixed capex

- ROIC-driven portfolio cuts

Semiconductor friend-shoring rises amid US–China controls; subsidies ¥1.35T and $52.7bn

Consumer TV/printer demand is cyclical and mature, pressuring volumes while B2B/solutions yield steadier margins. Input inflation and logistics volatility squeeze gross margins; Drewry WCI fell from US$10,377 (Sep 2021) to ~US$1,900 (2023–24). USD/JPY ~145 (2024) raised COGS; consumables ≈60% of OEM profit. Semiconductor lead time ~12 weeks (2024).

| Metric | Value |

|---|---|

| USD/JPY (2024) | ~145 |

| Drewry WCI (2023–24) | ~US$1,900 |

| Consumables profit | ≈60% |

| Semiconductor lead time (2024) | ~12 wks |

Preview Before You Purchase

Funai PESTLE Analysis

The preview shown here is the exact Funai PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises. After checkout you’ll instantly receive this finished, professionally structured document to apply directly to your research or strategy work.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, social dynamics, technological change, legal risks, and environmental pressures are shaping Funai’s strategic outlook. This concise PESTLE highlights key external drivers and actionable implications. Ideal for investors and strategists—purchase the full analysis for a complete, downloadable report packed with insights you can use today.

Political factors

Trade policy shifts

US–China tech tensions and export controls, which helped drive a global semiconductor market of roughly $600 billion in 2024, can disrupt component flows and market access for electronics. Japan’s alignment with allied controls on advanced chips increases sourcing risk and may complicate ODM/EMS contracts. Funai must diversify suppliers and redesign BOMs to remain compliant. Ongoing monitoring of tariff regimes and country-of-origin rules, including US tariffs up to 25%, is essential.

Industrial policy incentives

Japan has rolled out trillion-yen industrial incentives (¥1.35 trillion program for chips announced 2022), the US CHIPS Act provides about $52.7 billion for semiconductor incentives, and the EU aims to mobilize up to €43 billion for advanced manufacturing. Funai can leverage local-content incentives by partnering with regional fabs or contract assemblers to qualify for subsidies. Accessing grants requires meeting localization and workforce criteria, including local sourcing and training commitments. Strategic site selection in Japan, US or EU hubs reduces geopolitical and supply-chain risk.

Public procurement dynamics

Commercial products and IT solutions can tap rising government digitalization and education budgets, with public education spending averaging about 4% of GDP globally and global government IT investment near US$500 billion in 2024, boosting addressable markets. Procurement standards now prioritize security, energy efficiency and lifecycle support, while certification readiness can lift tender win rates materially. Building distributor-government relationships expands pipeline visibility and deal flow.

Currency and central bank posture

- FX exposure: USD/JPY ~150–160

- Financing: short-term BOJ rate ~0% vs negative prior

- Hedging: align tenor with order cycles

- Pricing: add political-risk corridors

Supply-chain resilience agendas

Semiconductor friend-shoring rises amid US–China controls; subsidies ¥1.35T and $52.7bn

US–China tech tensions and export controls (global semiconductors ≈$600bn in 2024) risk component access; Japan aligns with allied chip controls. Trillion-yen Japan incentives (¥1.35T), US CHIPS $52.7bn and EU ~€43bn shift sourcing and subsidy opportunities. Weak yen (USD/JPY ~150–160) raises import costs but aids exports; hedging and friend-shoring reduce political risk.

| Factor | Data | Impact |

|---|---|---|

| Export controls | Semis $600bn (2024) | Supply risk |

| Incentives | ¥1.35T / $52.7bn / €43bn | Localize/partner |

| FX | USD/JPY 150–160 | Margin pressure |

What is included in the product

Analyzes how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Funai, with data-backed trends, detailed subpoints and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A clean, summarized version of Funai's PESTLE analysis, visually segmented by category and written in plain language to enable quick sharing, note-taking, presentation drops, and fast alignment on external risks and market positioning.

Economic factors

Electronics demand cycles

Consumer TV and printer demand remains cyclical and mature, pressuring volumes as replacement cycles lengthen and discretionary spending fluctuates. Funai’s B2B and solutions segments provide steadier margins and contract revenue that mitigate retail volatility. Product mix optimization toward higher-margin models smooths revenue swings. Tight inventory discipline reduces markdown risk and protects gross margins.

Inflation and input costs

Components, freight and labor inflation compress Funai margins as input prices and logistics costs remain volatile; Drewry World Container Index fell from a Sept 2021 peak of US$10,377 to roughly US$1,900 in 2023–24 yet volatility still raises costs. Long-term supply agreements and design-to-cost reduce exposure. Passing through costs requires differentiated features or services. Lean operations protect EBITDA in slowdowns.

FX sensitivity (JPY)

Imported components priced in USD push Funai's COGS higher when the yen weakens; USD/JPY averaged about 145 in 2024 and spiked toward 155 in early 2025, amplifying input costs. Yen weakness can boost export competitiveness outside Japan, while dynamic hedging and USD revenue natural offsets mitigate volatility; pricing ladders should include explicit FX triggers tied to USD/JPY bands.

Print and media secular decline

Consumer printing volumes continue secular decline as digitization reduces home/page demand, shifting profit pools toward niche commercial print, consumables and managed print services; supplies account for ≈60% of OEM profit contribution while lifecycle services and subscription models stabilize cash flow and recurring revenue.

- Trend: consumer print down, commercial niche up

- Profit: consumables ≈60%

- Model: MPS/subscriptions stabilize cash flow

- R&D: prioritize high-margin specialty media

Capex and working capital

Long lead times in electronics, which peaked during 2020–22, still strain cash during demand swings; median semiconductor lead time eased to about 12 weeks in 2024, keeping inventory buffers high. Funai uses vendor-managed inventory and S&OP to improve turns, asset-light EMS partnerships to reduce fixed-capex exposure, and a strict ROIC target to guide portfolio pruning.

- Lead time ~12 weeks (2024)

- VMI + S&OP improve turns

- EMS partnerships lower fixed capex

- ROIC-driven portfolio cuts

Semiconductor friend-shoring rises amid US–China controls; subsidies ¥1.35T and $52.7bn

Consumer TV/printer demand is cyclical and mature, pressuring volumes while B2B/solutions yield steadier margins. Input inflation and logistics volatility squeeze gross margins; Drewry WCI fell from US$10,377 (Sep 2021) to ~US$1,900 (2023–24). USD/JPY ~145 (2024) raised COGS; consumables ≈60% of OEM profit. Semiconductor lead time ~12 weeks (2024).

| Metric | Value |

|---|---|

| USD/JPY (2024) | ~145 |

| Drewry WCI (2023–24) | ~US$1,900 |

| Consumables profit | ≈60% |

| Semiconductor lead time (2024) | ~12 wks |

Preview Before You Purchase

Funai PESTLE Analysis

The preview shown here is the exact Funai PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or surprises. After checkout you’ll instantly receive this finished, professionally structured document to apply directly to your research or strategy work.