F.W. Webb Porter's Five Forces Analysis

From Overview to Strategy Blueprint

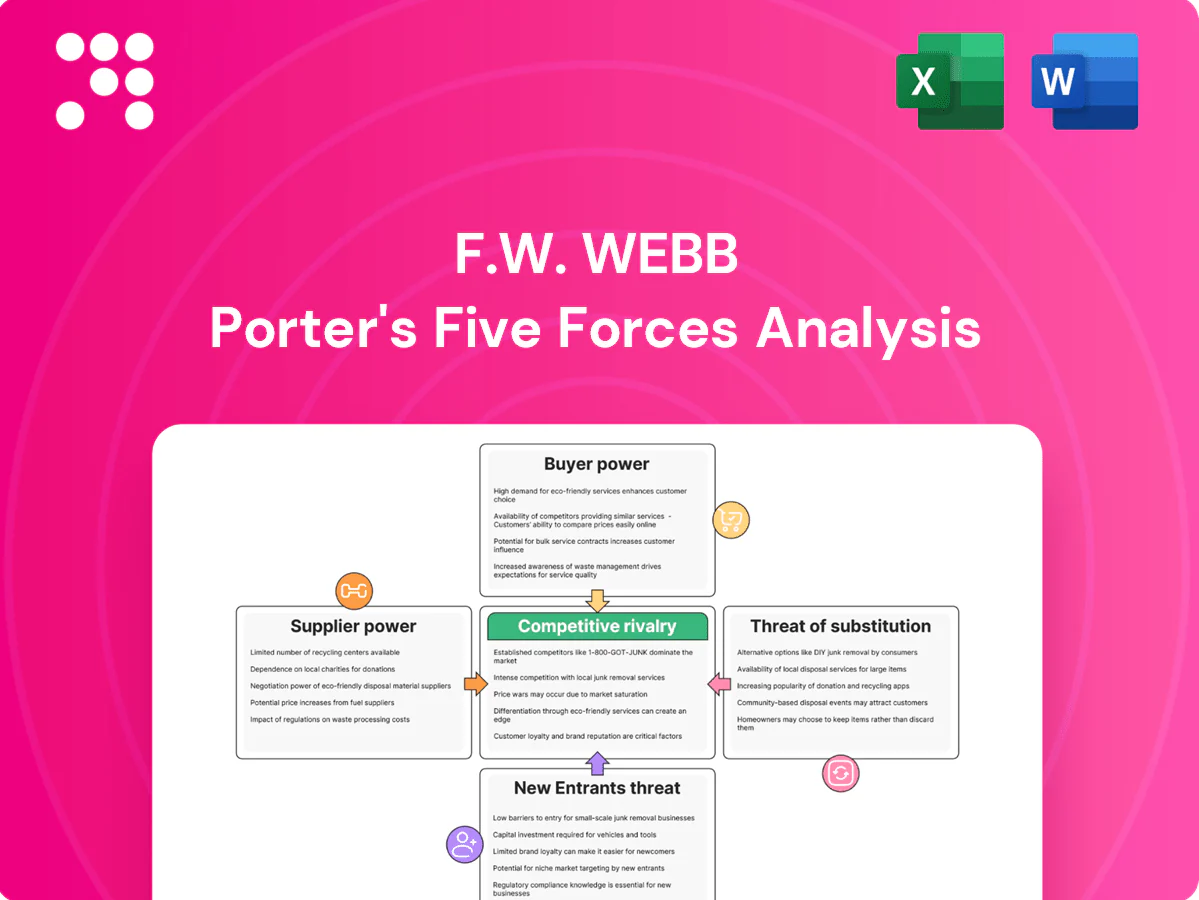

F.W. Webb faces moderate supplier power, strong buyer bargaining in commercial plumbing channels, and persistent rivalry from regional distributors; substitutive threats are limited while entry barriers remain capital-intensive. This snapshot highlights key competitive levers and weaknesses. Ready to move beyond the basics? Get a full strategic breakdown of F.W. Webb’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

OEM concentration and brand sway

Leading HVAC, plumbing and PVF OEMs (Carrier, Trane, Daikin, Emerson) remain concentrated and brand-driven, granting pricing and allocation leverage over distributors. High-spec boilers, chillers and specialty valves commonly require authorized distribution, constraining switching and pressuring margins in exchange for marquee lines. Webb offsets this by a broad line card and multi-brand sourcing; Webb reported roughly $6 billion in sales in 2024, supporting supplier diversification.

Specialized/engineered SKUs

Engineered, code-compliant SKUs sharply reduce interchangeability, increasing supplier leverage as submittals, warranties and technical certifications lock projects to specific vendors. Suppliers use these requirements to demand stocking commitments and prioritize distributors that offer strong technical support and rapid allocations. Webb’s advanced technical capabilities improve allocation prospects but remain dependent on supplier cooperation for critical engineered items.

Allocation and lead-time dynamics

Cyclical demand, supply shocks and seasonal HVAC/refrigeration spikes in 2024 drive supplier allocations, giving vendors leverage to ration critical SKUs. Extended lead times and freight volatility force distributors to carry larger inventory at supplier terms, elevating working capital and exposure to spot-price swings. Strong forecasting and EDI integration in 2024 have reduced stockouts and allocation impact for digitally connected distributors.

Private label vs. national brands

Where F.W. Webb can develop private-label or secondary brands, supplier power moderates; in commodity PVF and rough-in plumbing, multiple OEMs and import options reduce dependence on any single supplier. Premium fixtures, HVAC controls and branded pumps remain brand-led in 2024, keeping suppliers influential; the firm’s mix determines net supplier leverage.

- 2024 private-label share ~19% (NielsenIQ) — opportunity to shift low-margin SKUs

- Commodity PVF: multiple OEMs = lower supplier power

- Premium equipment: brand concentration = higher supplier power

Scale and relationship offset

Webb’s regional scale — over 180 branches and roughly $4 billion in annual sales in 2024 — gives suppliers volume, market data, and access they prize, enabling joint marketing, training, and demand-generation programs that secure better terms.

Long-standing supplier relationships often yield exclusive territories or rebate structures that offset list-price leverage, though renegotiations typically hinge on supplier-set performance metrics.

- Scale: 180+ branches (2024)

- Revenue: ~$4B (2024)

- Levers: joint marketing, training, rebates

- Risk: renegotiations tied to performance KPIs

Scale aids buying leverage but OEMs control allocation — 180+ branches, $4B, 19% PL

Supplier power is mixed: brand-led HVAC/pumps exert high leverage while commodity PVF shows low supplier power; Webb offsets this via multi-brand sourcing and ~19% private-label in 2024. Scale (180+ branches, ~$4B 2024 revenue) secures rebates and coop programs but premium OEMs retain allocation control and warranty lock-ins.

| Metric | 2024 |

|---|---|

| Revenue | ~$4B |

| Branches | 180+ |

| Private-label | ~19% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer influence, and market entry risks specific to F.W. Webb. Identifies disruptive threats, substitute products, and dynamics that protect or erode its market position.

Clear, one-sheet Porter's Five Forces for F.W. Webb—instantly identify competitive pressures and relief points for faster strategic decisions.

Customers Bargaining Power

Fragmented contractors but price sensitive

Many residential and light-commercial contractors remain highly fragmented—over 90% operate as small businesses—limiting individual bargaining power, yet they are extremely price sensitive and routinely shop distributors for common SKUs. Promotional pricing and same-day quotes drive switching; 2024 surveys show speed of service and flexible credit terms are decisive when margins are thin. Rapid fulfillment and short credit often tip purchase decisions.

Large mechanicals and facility managers

Enterprise buyers such as large MEP firms, institutions and industrial plants wield strong leverage through competitive bids and contract structures, enabling demands for volume discounts, project pricing and strict service-level agreements. Multi-year maintenance programs and national accounts further concentrate negotiating power by guaranteeing long-term spend. F.W. Webb mitigates this with dedicated account management, tailored pricing, consignment programs and value-added services to lock in retention and protect margins.

Specification-driven projects

When engineers specify brands in specification-driven projects, buyer switching power falls sharply for those product lines, locking distributors into narrower negotiations; Webb reported roughly $3.5 billion in 2024 sales, reflecting strong demand in specified MEP categories. Customers can still pressure distributor margins on the specified bill of materials, trimming markups even when brands are fixed. Pre-bid value engineering often re-opens competition at the component level, recovering cost savings. Webb’s engineering support and spec influence reduce pure price haggling by shifting discussions to performance and lifecycle value.

Service, logistics, and credit expectations

Same-day delivery, jobsite staging, will-call, and extended credit are table stakes in 2024; customers use service metrics to extract price and payment concessions. Superior fill rates and technical support allow F.W. Webb to command premiums and blunt buyer power. Weak service increases buyer leverage and churn risk.

- Service as differentiator

- Fill rate = pricing power

- Credit terms = switching force

Digital transparency and e-procurement

Digital transparency and e-procurement make online pricing, availability tools, and device-friendly ordering increase buyer comparability and power; by 2024 more than 60% of B2B buyers rely on digital channels for purchase decisions, raising expectations for real-time inventory and instant ordering across devices.

Integration with contractor estimating and PO systems creates sticky workflows that raise switching costs in Webb’s favor, while branches or suppliers lacking digital parity cede leverage back to informed buyers.

- Online pricing: higher comparability, faster negotiation

- Real-time inventory: expected by >60% of buyers (2024)

- Integration: contractor software raises switching costs for buyers

- Digital gaps: empower buyers, risk margin pressure

Speed, credit and fill-rate win: contractors switch for same-day quotes; digital buying rises

Contractors are fragmented (>90% small businesses) and price-sensitive but rapidly switch for same-day quotes; speed, credit and fill rates decide purchases. Large MEP and national accounts force volume discounts; F.W. Webb reported $3.5B revenue in 2024, reflecting spec-driven demand. Over 60% of B2B buyers use digital channels in 2024, raising price transparency. Strong service and integrations increase switching costs and preserve margins.

| Metric | 2024 |

|---|---|

| FW Webb sales | $3.5B |

| Buyers using digital | >60% |

| Contractors small biz | >90% |

What You See Is What You Get

F.W. Webb Porter's Five Forces Analysis

This F.W. Webb Porter's Five Forces Analysis evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and industry-specific bargaining dynamics to clarify strategic positioning. It includes data-driven insights, risk scoring, and tactical recommendations tailored to plumbing, HVAC, and MRO distribution channels. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

From Overview to Strategy Blueprint

F.W. Webb faces moderate supplier power, strong buyer bargaining in commercial plumbing channels, and persistent rivalry from regional distributors; substitutive threats are limited while entry barriers remain capital-intensive. This snapshot highlights key competitive levers and weaknesses. Ready to move beyond the basics? Get a full strategic breakdown of F.W. Webb’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

OEM concentration and brand sway

Leading HVAC, plumbing and PVF OEMs (Carrier, Trane, Daikin, Emerson) remain concentrated and brand-driven, granting pricing and allocation leverage over distributors. High-spec boilers, chillers and specialty valves commonly require authorized distribution, constraining switching and pressuring margins in exchange for marquee lines. Webb offsets this by a broad line card and multi-brand sourcing; Webb reported roughly $6 billion in sales in 2024, supporting supplier diversification.

Specialized/engineered SKUs

Engineered, code-compliant SKUs sharply reduce interchangeability, increasing supplier leverage as submittals, warranties and technical certifications lock projects to specific vendors. Suppliers use these requirements to demand stocking commitments and prioritize distributors that offer strong technical support and rapid allocations. Webb’s advanced technical capabilities improve allocation prospects but remain dependent on supplier cooperation for critical engineered items.

Allocation and lead-time dynamics

Cyclical demand, supply shocks and seasonal HVAC/refrigeration spikes in 2024 drive supplier allocations, giving vendors leverage to ration critical SKUs. Extended lead times and freight volatility force distributors to carry larger inventory at supplier terms, elevating working capital and exposure to spot-price swings. Strong forecasting and EDI integration in 2024 have reduced stockouts and allocation impact for digitally connected distributors.

Private label vs. national brands

Where F.W. Webb can develop private-label or secondary brands, supplier power moderates; in commodity PVF and rough-in plumbing, multiple OEMs and import options reduce dependence on any single supplier. Premium fixtures, HVAC controls and branded pumps remain brand-led in 2024, keeping suppliers influential; the firm’s mix determines net supplier leverage.

- 2024 private-label share ~19% (NielsenIQ) — opportunity to shift low-margin SKUs

- Commodity PVF: multiple OEMs = lower supplier power

- Premium equipment: brand concentration = higher supplier power

Scale and relationship offset

Webb’s regional scale — over 180 branches and roughly $4 billion in annual sales in 2024 — gives suppliers volume, market data, and access they prize, enabling joint marketing, training, and demand-generation programs that secure better terms.

Long-standing supplier relationships often yield exclusive territories or rebate structures that offset list-price leverage, though renegotiations typically hinge on supplier-set performance metrics.

- Scale: 180+ branches (2024)

- Revenue: ~$4B (2024)

- Levers: joint marketing, training, rebates

- Risk: renegotiations tied to performance KPIs

Scale aids buying leverage but OEMs control allocation — 180+ branches, $4B, 19% PL

Supplier power is mixed: brand-led HVAC/pumps exert high leverage while commodity PVF shows low supplier power; Webb offsets this via multi-brand sourcing and ~19% private-label in 2024. Scale (180+ branches, ~$4B 2024 revenue) secures rebates and coop programs but premium OEMs retain allocation control and warranty lock-ins.

| Metric | 2024 |

|---|---|

| Revenue | ~$4B |

| Branches | 180+ |

| Private-label | ~19% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer influence, and market entry risks specific to F.W. Webb. Identifies disruptive threats, substitute products, and dynamics that protect or erode its market position.

Clear, one-sheet Porter's Five Forces for F.W. Webb—instantly identify competitive pressures and relief points for faster strategic decisions.

Customers Bargaining Power

Fragmented contractors but price sensitive

Many residential and light-commercial contractors remain highly fragmented—over 90% operate as small businesses—limiting individual bargaining power, yet they are extremely price sensitive and routinely shop distributors for common SKUs. Promotional pricing and same-day quotes drive switching; 2024 surveys show speed of service and flexible credit terms are decisive when margins are thin. Rapid fulfillment and short credit often tip purchase decisions.

Large mechanicals and facility managers

Enterprise buyers such as large MEP firms, institutions and industrial plants wield strong leverage through competitive bids and contract structures, enabling demands for volume discounts, project pricing and strict service-level agreements. Multi-year maintenance programs and national accounts further concentrate negotiating power by guaranteeing long-term spend. F.W. Webb mitigates this with dedicated account management, tailored pricing, consignment programs and value-added services to lock in retention and protect margins.

Specification-driven projects

When engineers specify brands in specification-driven projects, buyer switching power falls sharply for those product lines, locking distributors into narrower negotiations; Webb reported roughly $3.5 billion in 2024 sales, reflecting strong demand in specified MEP categories. Customers can still pressure distributor margins on the specified bill of materials, trimming markups even when brands are fixed. Pre-bid value engineering often re-opens competition at the component level, recovering cost savings. Webb’s engineering support and spec influence reduce pure price haggling by shifting discussions to performance and lifecycle value.

Service, logistics, and credit expectations

Same-day delivery, jobsite staging, will-call, and extended credit are table stakes in 2024; customers use service metrics to extract price and payment concessions. Superior fill rates and technical support allow F.W. Webb to command premiums and blunt buyer power. Weak service increases buyer leverage and churn risk.

- Service as differentiator

- Fill rate = pricing power

- Credit terms = switching force

Digital transparency and e-procurement

Digital transparency and e-procurement make online pricing, availability tools, and device-friendly ordering increase buyer comparability and power; by 2024 more than 60% of B2B buyers rely on digital channels for purchase decisions, raising expectations for real-time inventory and instant ordering across devices.

Integration with contractor estimating and PO systems creates sticky workflows that raise switching costs in Webb’s favor, while branches or suppliers lacking digital parity cede leverage back to informed buyers.

- Online pricing: higher comparability, faster negotiation

- Real-time inventory: expected by >60% of buyers (2024)

- Integration: contractor software raises switching costs for buyers

- Digital gaps: empower buyers, risk margin pressure

Speed, credit and fill-rate win: contractors switch for same-day quotes; digital buying rises

Contractors are fragmented (>90% small businesses) and price-sensitive but rapidly switch for same-day quotes; speed, credit and fill rates decide purchases. Large MEP and national accounts force volume discounts; F.W. Webb reported $3.5B revenue in 2024, reflecting spec-driven demand. Over 60% of B2B buyers use digital channels in 2024, raising price transparency. Strong service and integrations increase switching costs and preserve margins.

| Metric | 2024 |

|---|---|

| FW Webb sales | $3.5B |

| Buyers using digital | >60% |

| Contractors small biz | >90% |

What You See Is What You Get

F.W. Webb Porter's Five Forces Analysis

This F.W. Webb Porter's Five Forces Analysis evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and industry-specific bargaining dynamics to clarify strategic positioning. It includes data-driven insights, risk scoring, and tactical recommendations tailored to plumbing, HVAC, and MRO distribution channels. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

F.W. Webb faces moderate supplier power, strong buyer bargaining in commercial plumbing channels, and persistent rivalry from regional distributors; substitutive threats are limited while entry barriers remain capital-intensive. This snapshot highlights key competitive levers and weaknesses. Ready to move beyond the basics? Get a full strategic breakdown of F.W. Webb’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

OEM concentration and brand sway

Leading HVAC, plumbing and PVF OEMs (Carrier, Trane, Daikin, Emerson) remain concentrated and brand-driven, granting pricing and allocation leverage over distributors. High-spec boilers, chillers and specialty valves commonly require authorized distribution, constraining switching and pressuring margins in exchange for marquee lines. Webb offsets this by a broad line card and multi-brand sourcing; Webb reported roughly $6 billion in sales in 2024, supporting supplier diversification.

Specialized/engineered SKUs

Engineered, code-compliant SKUs sharply reduce interchangeability, increasing supplier leverage as submittals, warranties and technical certifications lock projects to specific vendors. Suppliers use these requirements to demand stocking commitments and prioritize distributors that offer strong technical support and rapid allocations. Webb’s advanced technical capabilities improve allocation prospects but remain dependent on supplier cooperation for critical engineered items.

Allocation and lead-time dynamics

Cyclical demand, supply shocks and seasonal HVAC/refrigeration spikes in 2024 drive supplier allocations, giving vendors leverage to ration critical SKUs. Extended lead times and freight volatility force distributors to carry larger inventory at supplier terms, elevating working capital and exposure to spot-price swings. Strong forecasting and EDI integration in 2024 have reduced stockouts and allocation impact for digitally connected distributors.

Private label vs. national brands

Where F.W. Webb can develop private-label or secondary brands, supplier power moderates; in commodity PVF and rough-in plumbing, multiple OEMs and import options reduce dependence on any single supplier. Premium fixtures, HVAC controls and branded pumps remain brand-led in 2024, keeping suppliers influential; the firm’s mix determines net supplier leverage.

- 2024 private-label share ~19% (NielsenIQ) — opportunity to shift low-margin SKUs

- Commodity PVF: multiple OEMs = lower supplier power

- Premium equipment: brand concentration = higher supplier power

Scale and relationship offset

Webb’s regional scale — over 180 branches and roughly $4 billion in annual sales in 2024 — gives suppliers volume, market data, and access they prize, enabling joint marketing, training, and demand-generation programs that secure better terms.

Long-standing supplier relationships often yield exclusive territories or rebate structures that offset list-price leverage, though renegotiations typically hinge on supplier-set performance metrics.

- Scale: 180+ branches (2024)

- Revenue: ~$4B (2024)

- Levers: joint marketing, training, rebates

- Risk: renegotiations tied to performance KPIs

Scale aids buying leverage but OEMs control allocation — 180+ branches, $4B, 19% PL

Supplier power is mixed: brand-led HVAC/pumps exert high leverage while commodity PVF shows low supplier power; Webb offsets this via multi-brand sourcing and ~19% private-label in 2024. Scale (180+ branches, ~$4B 2024 revenue) secures rebates and coop programs but premium OEMs retain allocation control and warranty lock-ins.

| Metric | 2024 |

|---|---|

| Revenue | ~$4B |

| Branches | 180+ |

| Private-label | ~19% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer influence, and market entry risks specific to F.W. Webb. Identifies disruptive threats, substitute products, and dynamics that protect or erode its market position.

Clear, one-sheet Porter's Five Forces for F.W. Webb—instantly identify competitive pressures and relief points for faster strategic decisions.

Customers Bargaining Power

Fragmented contractors but price sensitive

Many residential and light-commercial contractors remain highly fragmented—over 90% operate as small businesses—limiting individual bargaining power, yet they are extremely price sensitive and routinely shop distributors for common SKUs. Promotional pricing and same-day quotes drive switching; 2024 surveys show speed of service and flexible credit terms are decisive when margins are thin. Rapid fulfillment and short credit often tip purchase decisions.

Large mechanicals and facility managers

Enterprise buyers such as large MEP firms, institutions and industrial plants wield strong leverage through competitive bids and contract structures, enabling demands for volume discounts, project pricing and strict service-level agreements. Multi-year maintenance programs and national accounts further concentrate negotiating power by guaranteeing long-term spend. F.W. Webb mitigates this with dedicated account management, tailored pricing, consignment programs and value-added services to lock in retention and protect margins.

Specification-driven projects

When engineers specify brands in specification-driven projects, buyer switching power falls sharply for those product lines, locking distributors into narrower negotiations; Webb reported roughly $3.5 billion in 2024 sales, reflecting strong demand in specified MEP categories. Customers can still pressure distributor margins on the specified bill of materials, trimming markups even when brands are fixed. Pre-bid value engineering often re-opens competition at the component level, recovering cost savings. Webb’s engineering support and spec influence reduce pure price haggling by shifting discussions to performance and lifecycle value.

Service, logistics, and credit expectations

Same-day delivery, jobsite staging, will-call, and extended credit are table stakes in 2024; customers use service metrics to extract price and payment concessions. Superior fill rates and technical support allow F.W. Webb to command premiums and blunt buyer power. Weak service increases buyer leverage and churn risk.

- Service as differentiator

- Fill rate = pricing power

- Credit terms = switching force

Digital transparency and e-procurement

Digital transparency and e-procurement make online pricing, availability tools, and device-friendly ordering increase buyer comparability and power; by 2024 more than 60% of B2B buyers rely on digital channels for purchase decisions, raising expectations for real-time inventory and instant ordering across devices.

Integration with contractor estimating and PO systems creates sticky workflows that raise switching costs in Webb’s favor, while branches or suppliers lacking digital parity cede leverage back to informed buyers.

- Online pricing: higher comparability, faster negotiation

- Real-time inventory: expected by >60% of buyers (2024)

- Integration: contractor software raises switching costs for buyers

- Digital gaps: empower buyers, risk margin pressure

Speed, credit and fill-rate win: contractors switch for same-day quotes; digital buying rises

Contractors are fragmented (>90% small businesses) and price-sensitive but rapidly switch for same-day quotes; speed, credit and fill rates decide purchases. Large MEP and national accounts force volume discounts; F.W. Webb reported $3.5B revenue in 2024, reflecting spec-driven demand. Over 60% of B2B buyers use digital channels in 2024, raising price transparency. Strong service and integrations increase switching costs and preserve margins.

| Metric | 2024 |

|---|---|

| FW Webb sales | $3.5B |

| Buyers using digital | >60% |

| Contractors small biz | >90% |

What You See Is What You Get

F.W. Webb Porter's Five Forces Analysis

This F.W. Webb Porter's Five Forces Analysis evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and industry-specific bargaining dynamics to clarify strategic positioning. It includes data-driven insights, risk scoring, and tactical recommendations tailored to plumbing, HVAC, and MRO distribution channels. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.