Guangzhou Automobile Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

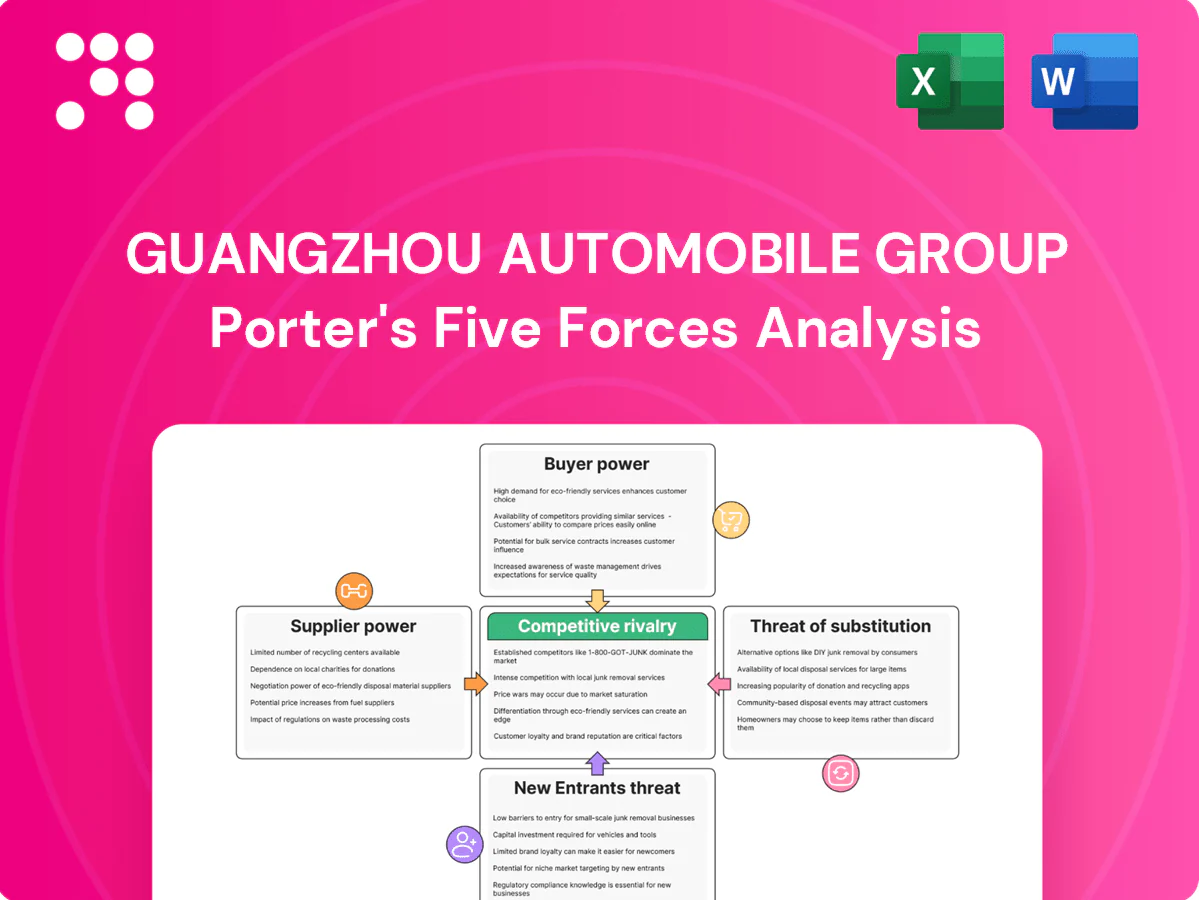

Guangzhou Automobile Group faces intense competitive rivalry, evolving buyer preferences, and moderate supplier leverage amid electrification and JV dynamics; threats from new entrants and substitutes are rising as tech and EV startups scale. This snapshot scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Battery suppliers highly concentrated

EV cell/pack supply is highly concentrated—CATL held about 31% global market share in 2024 and BYD roughly 20%—giving suppliers pricing and allocation leverage. GAC’s Aion expansion raises dependence on high‑nickel/LFP chemistries and secure lithium; long‑term contracts and co‑development lower but do not remove exposure, and raw‑material swings (lithium spot moves >40% 2022–24) quickly hit costs and margins.

Semiconductor and software dependence

Advanced MCUs, ADAS/autopilot chips and domain controllers remain concentrated among a few global suppliers (NXP, Renesas, Infineon), keeping supplier leverage high; the global automotive semiconductor market was ~US$62 billion in 2024, underlining scale and concentration. Although broad chip shortages eased by 2024, specialized automotive-grade parts still command longer lead times and premium pricing. Critical software stacks—maps, OS, OTA—create parallel dependence on tech partners and cloud providers. GAC is localizing supply but scaling domestic alternatives will take multiple years and sustained R&D investment.

Critical materials and Tier-1 tooling

Steel, aluminum and precision tooling for GAC are concentrated among qualified Tier-1s that meet stringent PPAP and safety standards; China produced over half of global crude steel and primary aluminum and about 70% of rare-earths, reinforcing supplier concentration. High switching costs from validation and compliance keep leverage with Tier-1s, while supplier quality or delivery failures can halt JIT lines. GAC’s dual-sourcing lowers but does not eliminate supplier bargaining power.

JV technology gatekeeping

GAC’s JVs depend on foreign partners for powertrain, safety and software IP, with technology transfer terms in 2024 still limiting access to core modules and creating supplier-like leverage inside JV ecosystems; negotiation leverage revolves around volume commitments and localization roadmaps tied to model targets and capex schedules.

- JV tech dependence: foreign IP controls key modules

- Bargaining levers: volume commitments, localization % targets

- Practical impact: constrained module customization and margin pressure

Vertical integration only partial

GAC vertically integrates e-axles and portions of vehicle electronics but depends on external leaders for batteries, chips and sensors; CATL held roughly 40% of China’s EV battery market in 2024, so upstream concentration persists. Partial integration trims costs and improves margins but cannot negate supplier clout; full-stack capability would need multi-year, multi-billion RMB capex.

- Partial vertical integration: in-house e-axles/electronics

- Key dependency: batteries/chips/sensors — CATL ~40% China battery share (2024)

- Impact: better cost control but suppliers keep bargaining power

- Barrier: full vertical requires heavy capex and years

High supplier power: concentrated batteries, volatile lithium, tight auto-semi supply

Supplier power is high: CATL ~31% global/≈40% China battery share (2024) and BYD ~20% concentrate cells; lithium spot swings >40% (2022–24) pressure margins. Auto semis market ≈US$62bn (2024) with few suppliers, extending lead times and premiums. Tier‑1 metals/tooling validation creates switching costs; JV foreign IP limits module access despite partial vertical integration.

| Supplier | Concentration | 2024 metric | Impact |

|---|---|---|---|

| Batteries | High | CATL 31% global / ≈40% China | Pricing/allocation leverage |

| Semiconductors | High | Market ≈US$62bn | Lead times, premiums |

| Metals/Tooling | Moderate | China >50% steel | Switching costs |

What is included in the product

Concise Porter's Five Forces analysis of Guangzhou Automobile Group, assessing competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and identifying industry dynamics and strategic levers that shape its pricing, margins, and market resilience.

A concise, one-sheet Porter's Five Forces for Guangzhou Automobile Group highlighting supplier/buyer power, competitive rivalry, new entrant threats and regulatory pressure—perfect for quick strategic decisions; customizable pressure levels and an instant radar chart make it easy to drop into decks or Excel dashboards.

Customers Bargaining Power

Price-sensitive, choice-rich consumers

China’s market offered thousands of models across segments in 2024, enabling easy switching; online platforms and JD/Taobao comparisons make specs and price transparency routine, forcing discount pressure. NEV sales topped 11 million in 2024, pushing reference prices down and anchoring ICE/PHEV pricing; GAC must match feature-value parity or concede margin.

Fleet and ride-hailing procurement

Large fleets and ride-hailing platforms in China (over 400 million users across apps in 2024) extract volume discounts and bundled service packs, compressing per-unit margins while improving utilization and visibility. Standardized specs force GAC to accept tighter prices but scale benefits; after-sales uptime SLAs further shift bargaining power to buyers. To compete GAC must offer tailored financing and explicit TCO guarantees tied to uptime metrics.

After-sales and financing expectations

Buyers now insist on competitive warranties, bundled maintenance and low-rate auto finance, pressuring GAC to match market offers. GAC’s captive finance eases acquisition and retention, but tight industry spreads and peer comparisons compress yields. OTA updates and digital services are baseline expectations, and gaps in ecosystem services increase churn risk at renewal cycles.

Brand and resale value scrutiny

Consumers track residual values and perceived reliability closely; in China NEV leaders like BYD (roughly 30% retail share in 2024) show stronger resale, forcing rivals including GAC to use incentives to protect turnover. Any quality recall immediately raises buyer leverage and incentive demands. Building durable brand equity and verified reliability data is essential to soften price pushback.

- Residual value focus: customers track 3–5 year resale

- Market pressure: BYD ~30% retail share (2024)

- Recalls increase negotiation leverage

- Brand equity reduces discounting need

Corporate and government standards

Institutional buyers force strict safety, emissions (China VI since 2021) and data-compliance specs that raise GAC’s per-unit production costs and often cannot be fully passed to buyers; procurement cycles are competitive tenders with transparent scoring, institutionalizing buyer bargaining power in fleet and government segments.

- Public procurement ≈ 15% of GDP (World Bank)

- China VI emissions standard enforced since 2021

- Tenders use transparent technical/price scoring

China NEV 2024: 11m sales; fleets & procurement squeeze margins

China’s 2024 market (≈11m NEVs) gives buyers high switching power; online transparency and BYD’s ~30% retail share compress pricing and margins. Large fleets/ride‑hailing (≈400m users) and public procurement (~15% GDP) force volume discounts and strict specs, raising GAC’s per‑unit costs. Captive finance and TCO guarantees mitigate but OTA/services and resale (3–5y focus) drive negotiation.

| Metric | 2024 value | Impact |

|---|---|---|

| NEV sales | ≈11,000,000 | Price anchoring, lower ICE/PHEV pricing |

| BYD retail share | ≈30% | Stronger resale, pricing leverage |

| Ride‑hailing users | ≈400,000,000 | Volume discounts, SLAs |

| Public procurement | ≈15% GDP | Competitive tenders, spec costs |

| Resale focus | 3–5 years | Incentive pressure |

Preview Before You Purchase

Guangzhou Automobile Group Porter's Five Forces Analysis

This preview shows the exact Guangzhou Automobile Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or edits. The full document is professionally formatted and ready for download and use upon payment. It delivers a detailed assessment of competitive rivalry, supplier and buyer power, and threats of entry and substitution.

A Must-Have Tool for Decision-Makers

Guangzhou Automobile Group faces intense competitive rivalry, evolving buyer preferences, and moderate supplier leverage amid electrification and JV dynamics; threats from new entrants and substitutes are rising as tech and EV startups scale. This snapshot scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Battery suppliers highly concentrated

EV cell/pack supply is highly concentrated—CATL held about 31% global market share in 2024 and BYD roughly 20%—giving suppliers pricing and allocation leverage. GAC’s Aion expansion raises dependence on high‑nickel/LFP chemistries and secure lithium; long‑term contracts and co‑development lower but do not remove exposure, and raw‑material swings (lithium spot moves >40% 2022–24) quickly hit costs and margins.

Semiconductor and software dependence

Advanced MCUs, ADAS/autopilot chips and domain controllers remain concentrated among a few global suppliers (NXP, Renesas, Infineon), keeping supplier leverage high; the global automotive semiconductor market was ~US$62 billion in 2024, underlining scale and concentration. Although broad chip shortages eased by 2024, specialized automotive-grade parts still command longer lead times and premium pricing. Critical software stacks—maps, OS, OTA—create parallel dependence on tech partners and cloud providers. GAC is localizing supply but scaling domestic alternatives will take multiple years and sustained R&D investment.

Critical materials and Tier-1 tooling

Steel, aluminum and precision tooling for GAC are concentrated among qualified Tier-1s that meet stringent PPAP and safety standards; China produced over half of global crude steel and primary aluminum and about 70% of rare-earths, reinforcing supplier concentration. High switching costs from validation and compliance keep leverage with Tier-1s, while supplier quality or delivery failures can halt JIT lines. GAC’s dual-sourcing lowers but does not eliminate supplier bargaining power.

JV technology gatekeeping

GAC’s JVs depend on foreign partners for powertrain, safety and software IP, with technology transfer terms in 2024 still limiting access to core modules and creating supplier-like leverage inside JV ecosystems; negotiation leverage revolves around volume commitments and localization roadmaps tied to model targets and capex schedules.

- JV tech dependence: foreign IP controls key modules

- Bargaining levers: volume commitments, localization % targets

- Practical impact: constrained module customization and margin pressure

Vertical integration only partial

GAC vertically integrates e-axles and portions of vehicle electronics but depends on external leaders for batteries, chips and sensors; CATL held roughly 40% of China’s EV battery market in 2024, so upstream concentration persists. Partial integration trims costs and improves margins but cannot negate supplier clout; full-stack capability would need multi-year, multi-billion RMB capex.

- Partial vertical integration: in-house e-axles/electronics

- Key dependency: batteries/chips/sensors — CATL ~40% China battery share (2024)

- Impact: better cost control but suppliers keep bargaining power

- Barrier: full vertical requires heavy capex and years

High supplier power: concentrated batteries, volatile lithium, tight auto-semi supply

Supplier power is high: CATL ~31% global/≈40% China battery share (2024) and BYD ~20% concentrate cells; lithium spot swings >40% (2022–24) pressure margins. Auto semis market ≈US$62bn (2024) with few suppliers, extending lead times and premiums. Tier‑1 metals/tooling validation creates switching costs; JV foreign IP limits module access despite partial vertical integration.

| Supplier | Concentration | 2024 metric | Impact |

|---|---|---|---|

| Batteries | High | CATL 31% global / ≈40% China | Pricing/allocation leverage |

| Semiconductors | High | Market ≈US$62bn | Lead times, premiums |

| Metals/Tooling | Moderate | China >50% steel | Switching costs |

What is included in the product

Concise Porter's Five Forces analysis of Guangzhou Automobile Group, assessing competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and identifying industry dynamics and strategic levers that shape its pricing, margins, and market resilience.

A concise, one-sheet Porter's Five Forces for Guangzhou Automobile Group highlighting supplier/buyer power, competitive rivalry, new entrant threats and regulatory pressure—perfect for quick strategic decisions; customizable pressure levels and an instant radar chart make it easy to drop into decks or Excel dashboards.

Customers Bargaining Power

Price-sensitive, choice-rich consumers

China’s market offered thousands of models across segments in 2024, enabling easy switching; online platforms and JD/Taobao comparisons make specs and price transparency routine, forcing discount pressure. NEV sales topped 11 million in 2024, pushing reference prices down and anchoring ICE/PHEV pricing; GAC must match feature-value parity or concede margin.

Fleet and ride-hailing procurement

Large fleets and ride-hailing platforms in China (over 400 million users across apps in 2024) extract volume discounts and bundled service packs, compressing per-unit margins while improving utilization and visibility. Standardized specs force GAC to accept tighter prices but scale benefits; after-sales uptime SLAs further shift bargaining power to buyers. To compete GAC must offer tailored financing and explicit TCO guarantees tied to uptime metrics.

After-sales and financing expectations

Buyers now insist on competitive warranties, bundled maintenance and low-rate auto finance, pressuring GAC to match market offers. GAC’s captive finance eases acquisition and retention, but tight industry spreads and peer comparisons compress yields. OTA updates and digital services are baseline expectations, and gaps in ecosystem services increase churn risk at renewal cycles.

Brand and resale value scrutiny

Consumers track residual values and perceived reliability closely; in China NEV leaders like BYD (roughly 30% retail share in 2024) show stronger resale, forcing rivals including GAC to use incentives to protect turnover. Any quality recall immediately raises buyer leverage and incentive demands. Building durable brand equity and verified reliability data is essential to soften price pushback.

- Residual value focus: customers track 3–5 year resale

- Market pressure: BYD ~30% retail share (2024)

- Recalls increase negotiation leverage

- Brand equity reduces discounting need

Corporate and government standards

Institutional buyers force strict safety, emissions (China VI since 2021) and data-compliance specs that raise GAC’s per-unit production costs and often cannot be fully passed to buyers; procurement cycles are competitive tenders with transparent scoring, institutionalizing buyer bargaining power in fleet and government segments.

- Public procurement ≈ 15% of GDP (World Bank)

- China VI emissions standard enforced since 2021

- Tenders use transparent technical/price scoring

China NEV 2024: 11m sales; fleets & procurement squeeze margins

China’s 2024 market (≈11m NEVs) gives buyers high switching power; online transparency and BYD’s ~30% retail share compress pricing and margins. Large fleets/ride‑hailing (≈400m users) and public procurement (~15% GDP) force volume discounts and strict specs, raising GAC’s per‑unit costs. Captive finance and TCO guarantees mitigate but OTA/services and resale (3–5y focus) drive negotiation.

| Metric | 2024 value | Impact |

|---|---|---|

| NEV sales | ≈11,000,000 | Price anchoring, lower ICE/PHEV pricing |

| BYD retail share | ≈30% | Stronger resale, pricing leverage |

| Ride‑hailing users | ≈400,000,000 | Volume discounts, SLAs |

| Public procurement | ≈15% GDP | Competitive tenders, spec costs |

| Resale focus | 3–5 years | Incentive pressure |

Preview Before You Purchase

Guangzhou Automobile Group Porter's Five Forces Analysis

This preview shows the exact Guangzhou Automobile Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or edits. The full document is professionally formatted and ready for download and use upon payment. It delivers a detailed assessment of competitive rivalry, supplier and buyer power, and threats of entry and substitution.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Guangzhou Automobile Group faces intense competitive rivalry, evolving buyer preferences, and moderate supplier leverage amid electrification and JV dynamics; threats from new entrants and substitutes are rising as tech and EV startups scale. This snapshot scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Battery suppliers highly concentrated

EV cell/pack supply is highly concentrated—CATL held about 31% global market share in 2024 and BYD roughly 20%—giving suppliers pricing and allocation leverage. GAC’s Aion expansion raises dependence on high‑nickel/LFP chemistries and secure lithium; long‑term contracts and co‑development lower but do not remove exposure, and raw‑material swings (lithium spot moves >40% 2022–24) quickly hit costs and margins.

Semiconductor and software dependence

Advanced MCUs, ADAS/autopilot chips and domain controllers remain concentrated among a few global suppliers (NXP, Renesas, Infineon), keeping supplier leverage high; the global automotive semiconductor market was ~US$62 billion in 2024, underlining scale and concentration. Although broad chip shortages eased by 2024, specialized automotive-grade parts still command longer lead times and premium pricing. Critical software stacks—maps, OS, OTA—create parallel dependence on tech partners and cloud providers. GAC is localizing supply but scaling domestic alternatives will take multiple years and sustained R&D investment.

Critical materials and Tier-1 tooling

Steel, aluminum and precision tooling for GAC are concentrated among qualified Tier-1s that meet stringent PPAP and safety standards; China produced over half of global crude steel and primary aluminum and about 70% of rare-earths, reinforcing supplier concentration. High switching costs from validation and compliance keep leverage with Tier-1s, while supplier quality or delivery failures can halt JIT lines. GAC’s dual-sourcing lowers but does not eliminate supplier bargaining power.

JV technology gatekeeping

GAC’s JVs depend on foreign partners for powertrain, safety and software IP, with technology transfer terms in 2024 still limiting access to core modules and creating supplier-like leverage inside JV ecosystems; negotiation leverage revolves around volume commitments and localization roadmaps tied to model targets and capex schedules.

- JV tech dependence: foreign IP controls key modules

- Bargaining levers: volume commitments, localization % targets

- Practical impact: constrained module customization and margin pressure

Vertical integration only partial

GAC vertically integrates e-axles and portions of vehicle electronics but depends on external leaders for batteries, chips and sensors; CATL held roughly 40% of China’s EV battery market in 2024, so upstream concentration persists. Partial integration trims costs and improves margins but cannot negate supplier clout; full-stack capability would need multi-year, multi-billion RMB capex.

- Partial vertical integration: in-house e-axles/electronics

- Key dependency: batteries/chips/sensors — CATL ~40% China battery share (2024)

- Impact: better cost control but suppliers keep bargaining power

- Barrier: full vertical requires heavy capex and years

High supplier power: concentrated batteries, volatile lithium, tight auto-semi supply

Supplier power is high: CATL ~31% global/≈40% China battery share (2024) and BYD ~20% concentrate cells; lithium spot swings >40% (2022–24) pressure margins. Auto semis market ≈US$62bn (2024) with few suppliers, extending lead times and premiums. Tier‑1 metals/tooling validation creates switching costs; JV foreign IP limits module access despite partial vertical integration.

| Supplier | Concentration | 2024 metric | Impact |

|---|---|---|---|

| Batteries | High | CATL 31% global / ≈40% China | Pricing/allocation leverage |

| Semiconductors | High | Market ≈US$62bn | Lead times, premiums |

| Metals/Tooling | Moderate | China >50% steel | Switching costs |

What is included in the product

Concise Porter's Five Forces analysis of Guangzhou Automobile Group, assessing competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and identifying industry dynamics and strategic levers that shape its pricing, margins, and market resilience.

A concise, one-sheet Porter's Five Forces for Guangzhou Automobile Group highlighting supplier/buyer power, competitive rivalry, new entrant threats and regulatory pressure—perfect for quick strategic decisions; customizable pressure levels and an instant radar chart make it easy to drop into decks or Excel dashboards.

Customers Bargaining Power

Price-sensitive, choice-rich consumers

China’s market offered thousands of models across segments in 2024, enabling easy switching; online platforms and JD/Taobao comparisons make specs and price transparency routine, forcing discount pressure. NEV sales topped 11 million in 2024, pushing reference prices down and anchoring ICE/PHEV pricing; GAC must match feature-value parity or concede margin.

Fleet and ride-hailing procurement

Large fleets and ride-hailing platforms in China (over 400 million users across apps in 2024) extract volume discounts and bundled service packs, compressing per-unit margins while improving utilization and visibility. Standardized specs force GAC to accept tighter prices but scale benefits; after-sales uptime SLAs further shift bargaining power to buyers. To compete GAC must offer tailored financing and explicit TCO guarantees tied to uptime metrics.

After-sales and financing expectations

Buyers now insist on competitive warranties, bundled maintenance and low-rate auto finance, pressuring GAC to match market offers. GAC’s captive finance eases acquisition and retention, but tight industry spreads and peer comparisons compress yields. OTA updates and digital services are baseline expectations, and gaps in ecosystem services increase churn risk at renewal cycles.

Brand and resale value scrutiny

Consumers track residual values and perceived reliability closely; in China NEV leaders like BYD (roughly 30% retail share in 2024) show stronger resale, forcing rivals including GAC to use incentives to protect turnover. Any quality recall immediately raises buyer leverage and incentive demands. Building durable brand equity and verified reliability data is essential to soften price pushback.

- Residual value focus: customers track 3–5 year resale

- Market pressure: BYD ~30% retail share (2024)

- Recalls increase negotiation leverage

- Brand equity reduces discounting need

Corporate and government standards

Institutional buyers force strict safety, emissions (China VI since 2021) and data-compliance specs that raise GAC’s per-unit production costs and often cannot be fully passed to buyers; procurement cycles are competitive tenders with transparent scoring, institutionalizing buyer bargaining power in fleet and government segments.

- Public procurement ≈ 15% of GDP (World Bank)

- China VI emissions standard enforced since 2021

- Tenders use transparent technical/price scoring

China NEV 2024: 11m sales; fleets & procurement squeeze margins

China’s 2024 market (≈11m NEVs) gives buyers high switching power; online transparency and BYD’s ~30% retail share compress pricing and margins. Large fleets/ride‑hailing (≈400m users) and public procurement (~15% GDP) force volume discounts and strict specs, raising GAC’s per‑unit costs. Captive finance and TCO guarantees mitigate but OTA/services and resale (3–5y focus) drive negotiation.

| Metric | 2024 value | Impact |

|---|---|---|

| NEV sales | ≈11,000,000 | Price anchoring, lower ICE/PHEV pricing |

| BYD retail share | ≈30% | Stronger resale, pricing leverage |

| Ride‑hailing users | ≈400,000,000 | Volume discounts, SLAs |

| Public procurement | ≈15% GDP | Competitive tenders, spec costs |

| Resale focus | 3–5 years | Incentive pressure |

Preview Before You Purchase

Guangzhou Automobile Group Porter's Five Forces Analysis

This preview shows the exact Guangzhou Automobile Group Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or edits. The full document is professionally formatted and ready for download and use upon payment. It delivers a detailed assessment of competitive rivalry, supplier and buyer power, and threats of entry and substitution.