GAIL India Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

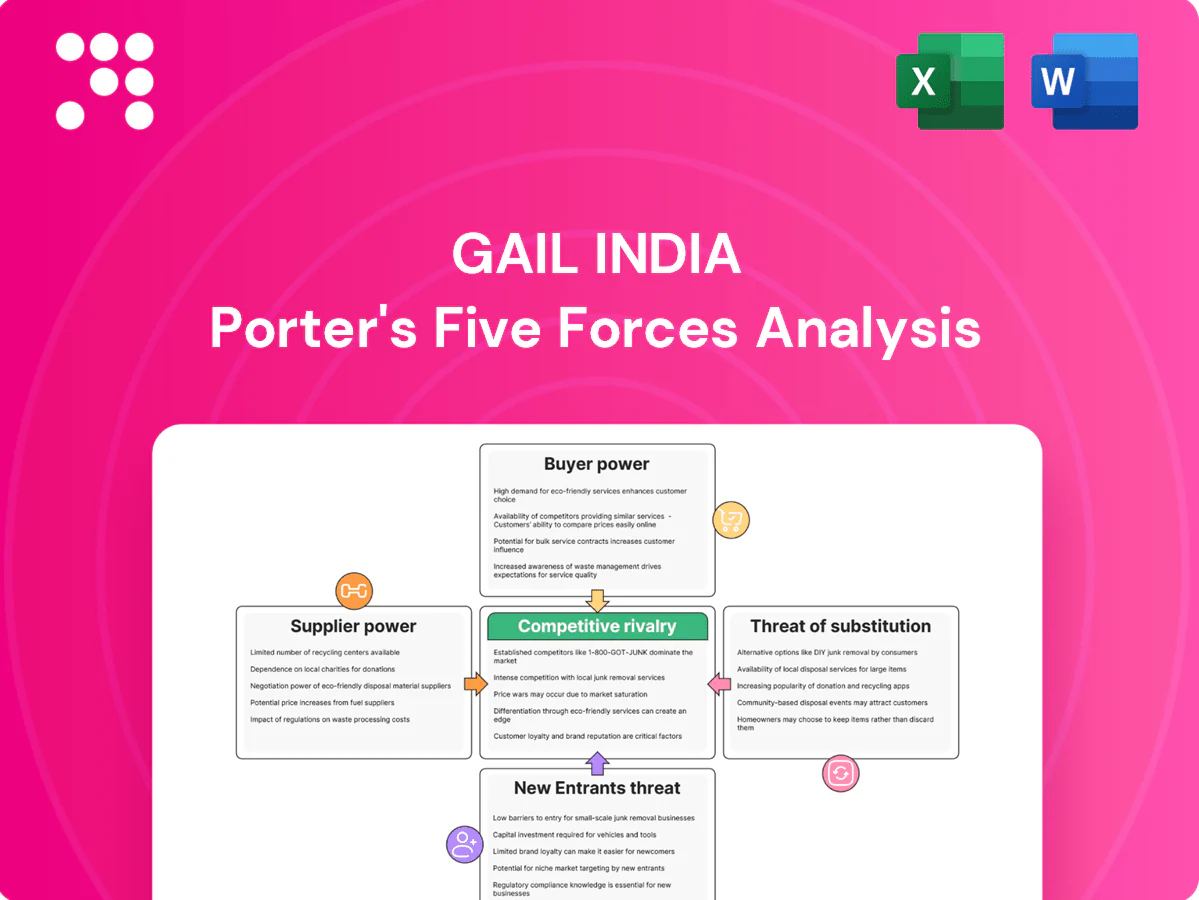

GAIL India's Porter's Five Forces snapshot highlights strong supplier influence from global gas producers, moderate buyer power amid regulated tariffs, limited threat of new entrants due to high infrastructure barriers, and pressure from substitutes like renewables; rivalry is moderate given state-backed scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore GAIL India’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated upstream gas sources

Domestic gas in India is produced predominantly by a small set of players — ONGC, OIL and Reliance-BP — concentrating upstream leverage; imports are similarly focused toward major LNG suppliers such as Qatar and the US, increasing supplier power during tight global markets. Scarcity episodes in 2022–24 saw spot LNG spikes that shifted pricing upstream, pressuring buyers. GAIL reduces risk through diversified sourcing, long‑term contracts and portfolio optimization.

Long-term LNG contracts vs spot volatility

GAIL’s multi-year LNG contracts underpin the bulk of its supply, stabilizing volumes and base pricing, while the 2022–23 global spot surge (peak spot TTF/Asia prices exceeded 60 USD/MMBtu) illustrated how spot spikes can compress margins and prompt renegotiation pressure. Contract flexibility and destination-swap clauses plus portfolio hedging temper short-term exposure, but cyclical spot swings continue to impact margins during tight markets.

Regulatory pricing frameworks

APM pricing and government caps/floors materially influence domestic gas transfer prices, so policy changes can curtail or enhance supplier bargaining power; examples include administered pricing linkages and occasional cap directives affecting LNG swaps. GAIL’s transmission tariffs are regulated by PNGRB, partially insulating pipeline revenues, while its pipeline network of about 14,000 km (circa 2024) keeps throughput fees stable. Upstream price revisions, however, directly ripple through GAIL’s marketing margins and trading book.

Specialized equipment and EPC inputs

Pipelines, compressors and cryogenic equipment are sourced from a narrow vendor base, with typical 2024 lead times of 12–18 months that, together with volatile global steel cycles, materially influence project costs and schedules.

Vendor prequalification lowers operational risk but further restricts suppliers; GAIL’s scale purchasing and large annual procurement volumes partially offset supplier leverage.

- Limited vendor pool increases supplier power

- Lead times 12–18 months (2024)

- Steel cycle volatility impacts capex and timelines

- Prequalification reduces risk but narrows options

- Scale purchasing provides countervailing buying power

Infrastructure and terminal access

- 42 MTPA India regas capacity (2024)

- 13,747 km GAIL pipeline (2024)

- Long-term access = higher bargaining power

- Capacity additions reduce supplier leverage

Supplier leverage rising; long‑term LNG contracts and 13,747 km pipeline reduce shock risk

Upstream supply is concentrated (ONGC, OIL, Reliance‑BP), raising supplier leverage; spot LNG shocks (peak >60 USD/MMBtu in 2022–23) stressed margins. GAIL offsets via long‑term LNG contracts, swaps and a 13,747 km pipeline (2024). Vendor lead times 12–18 months and steel cycles raise capex risk despite scale purchasing.

| Metric | 2024 |

|---|---|

| Regas capacity | 42 MTPA |

| GAIL pipeline | 13,747 km |

| Lead times | 12–18 months |

| Spot peak | >60 USD/MMBtu (2022–23) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to GAIL India; evaluates supplier and buyer power, threat of substitutes and new entrants, and competitive rivalry, highlighting disruptive forces and strategic implications for pricing, margins, and market share.

Clear one-sheet Porter's Five Forces for GAIL India—condenses supplier, buyer, entrant, substitute and rivalry pressures into a decision-ready snapshot to speed strategy and investment calls.

Customers Bargaining Power

Large, concentrated industrial offtakers

Fertilizer, power, refineries and major industrials take sizable volumes from GAIL, giving them strong bargaining leverage through scale and alternative-fuel options, especially as India expands LNG imports; GAIL operates a pipeline network exceeding 13,000 km (2024). Take-or-pay contracts and allocation priorities, however, limit immediate buyer power. Deep operational relationships and reliability remain key differentiators for GAIL.

CGD and city gas demand dynamics

Over 200 CGD entities operate as of 2024, increasing buyer clout and price sensitivity versus suppliers; many procure via short-term contracts and push for volume discounts. Related-party or strategic-partner CGDs (joint ventures with marketing or distribution links) soften pure adversarial bargaining. Regulatory pass-throughs of feedstock and transportation tariffs dampen end-customer elasticity, while multiple competing CGDs in some geographies intensify negotiations.

Fuel-switching alternatives

Buyers can substitute gas with coal, LPG, naphtha or renewables where feasible, keeping gas demand elastic; coal still supplies about 70% of India’s power (IEA 2023) while gas is roughly 6% of primary energy (IEA 2022). Relative price spreads—spot LNG vs domestic fuels—drive procurement quarter to quarter, prompting fuel swaps when coal or naphtha becomes cheaper. Pipeline and burner infrastructure create switching frictions but do not prevent shifts. Gradual carbon policies and rising non‑fossil capacity improve gas economics over time.

Contract structures and flexibility

Contract structures such as take-or-pay (typically 70–90% cover), ship-or-pay and indexation to JKM/TTF limit buyer leverage, locking revenue. Buyers negotiate flexibility on volumes, make-up gas and regas slots; sophisticated purchasers demand hybrid pricing and portfolio options. GAIL reported ~80% pipeline utilization in 2024, balancing utilization stability with commercial agility.

- Take-or-pay: 70–90% capacity cover

- Indexation: JKM/TTF-linked contracts

- Flexibility: volumes, make-up gas, re-gas slots

- Buyers: seek hybrid pricing/portfolio solutions

Service quality and reliability

Pipeline uptime and pressure maintenance drive buyer stickiness for GAIL; reported transmission availability exceeded 99% in 2024, materially lowering customers’ willingness to switch. Scheduling discipline and value-added services like portfolio optimization and balancing—handling ~13,700 km of pipeline and ~40 bcm throughput in 2024—increase retention. Even short outages or curtailments rapidly erode that leverage.

- Uptime: >99% (2024)

- Network: ~13,700 km (2024)

- Throughput: ~40 bcm (2024)

- Value-added: balancing, portfolio optimization

13,700 km network, 40 bcm throughput curb buyer leverage

Large industrials, fertiliser, power and 200+ CGDs (2024) exert significant bargaining via volume and alternatives, but take-or-pay (70–90%) and ~80% pipeline utilization limit short-term leverage. GAIL’s ~13,700 km network, >99% uptime and ~40 bcm throughput (2024) increase customer stickiness. Indexation to JKM/TTF and spot LNG spreads keep price sensitivity high.

| Metric | 2024 |

|---|---|

| Pipeline km | ~13,700 |

| Throughput | ~40 bcm |

| Uptime | >99% |

| CGDs | >200 |

| Take-or-pay | 70–90% |

| Utilization | ~80% |

Full Version Awaits

GAIL India Porter's Five Forces Analysis

This Porter’s Five Forces analysis of GAIL India evaluates competitive rivalry, supplier and buyer power, threat of substitutes and barriers to entry to determine industry attractiveness and strategic risks. It blends quantitative and qualitative insights for investors, analysts and executives to support valuation and strategic decisions. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file.

A Must-Have Tool for Decision-Makers

GAIL India's Porter's Five Forces snapshot highlights strong supplier influence from global gas producers, moderate buyer power amid regulated tariffs, limited threat of new entrants due to high infrastructure barriers, and pressure from substitutes like renewables; rivalry is moderate given state-backed scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore GAIL India’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated upstream gas sources

Domestic gas in India is produced predominantly by a small set of players — ONGC, OIL and Reliance-BP — concentrating upstream leverage; imports are similarly focused toward major LNG suppliers such as Qatar and the US, increasing supplier power during tight global markets. Scarcity episodes in 2022–24 saw spot LNG spikes that shifted pricing upstream, pressuring buyers. GAIL reduces risk through diversified sourcing, long‑term contracts and portfolio optimization.

Long-term LNG contracts vs spot volatility

GAIL’s multi-year LNG contracts underpin the bulk of its supply, stabilizing volumes and base pricing, while the 2022–23 global spot surge (peak spot TTF/Asia prices exceeded 60 USD/MMBtu) illustrated how spot spikes can compress margins and prompt renegotiation pressure. Contract flexibility and destination-swap clauses plus portfolio hedging temper short-term exposure, but cyclical spot swings continue to impact margins during tight markets.

Regulatory pricing frameworks

APM pricing and government caps/floors materially influence domestic gas transfer prices, so policy changes can curtail or enhance supplier bargaining power; examples include administered pricing linkages and occasional cap directives affecting LNG swaps. GAIL’s transmission tariffs are regulated by PNGRB, partially insulating pipeline revenues, while its pipeline network of about 14,000 km (circa 2024) keeps throughput fees stable. Upstream price revisions, however, directly ripple through GAIL’s marketing margins and trading book.

Specialized equipment and EPC inputs

Pipelines, compressors and cryogenic equipment are sourced from a narrow vendor base, with typical 2024 lead times of 12–18 months that, together with volatile global steel cycles, materially influence project costs and schedules.

Vendor prequalification lowers operational risk but further restricts suppliers; GAIL’s scale purchasing and large annual procurement volumes partially offset supplier leverage.

- Limited vendor pool increases supplier power

- Lead times 12–18 months (2024)

- Steel cycle volatility impacts capex and timelines

- Prequalification reduces risk but narrows options

- Scale purchasing provides countervailing buying power

Infrastructure and terminal access

- 42 MTPA India regas capacity (2024)

- 13,747 km GAIL pipeline (2024)

- Long-term access = higher bargaining power

- Capacity additions reduce supplier leverage

Supplier leverage rising; long‑term LNG contracts and 13,747 km pipeline reduce shock risk

Upstream supply is concentrated (ONGC, OIL, Reliance‑BP), raising supplier leverage; spot LNG shocks (peak >60 USD/MMBtu in 2022–23) stressed margins. GAIL offsets via long‑term LNG contracts, swaps and a 13,747 km pipeline (2024). Vendor lead times 12–18 months and steel cycles raise capex risk despite scale purchasing.

| Metric | 2024 |

|---|---|

| Regas capacity | 42 MTPA |

| GAIL pipeline | 13,747 km |

| Lead times | 12–18 months |

| Spot peak | >60 USD/MMBtu (2022–23) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to GAIL India; evaluates supplier and buyer power, threat of substitutes and new entrants, and competitive rivalry, highlighting disruptive forces and strategic implications for pricing, margins, and market share.

Clear one-sheet Porter's Five Forces for GAIL India—condenses supplier, buyer, entrant, substitute and rivalry pressures into a decision-ready snapshot to speed strategy and investment calls.

Customers Bargaining Power

Large, concentrated industrial offtakers

Fertilizer, power, refineries and major industrials take sizable volumes from GAIL, giving them strong bargaining leverage through scale and alternative-fuel options, especially as India expands LNG imports; GAIL operates a pipeline network exceeding 13,000 km (2024). Take-or-pay contracts and allocation priorities, however, limit immediate buyer power. Deep operational relationships and reliability remain key differentiators for GAIL.

CGD and city gas demand dynamics

Over 200 CGD entities operate as of 2024, increasing buyer clout and price sensitivity versus suppliers; many procure via short-term contracts and push for volume discounts. Related-party or strategic-partner CGDs (joint ventures with marketing or distribution links) soften pure adversarial bargaining. Regulatory pass-throughs of feedstock and transportation tariffs dampen end-customer elasticity, while multiple competing CGDs in some geographies intensify negotiations.

Fuel-switching alternatives

Buyers can substitute gas with coal, LPG, naphtha or renewables where feasible, keeping gas demand elastic; coal still supplies about 70% of India’s power (IEA 2023) while gas is roughly 6% of primary energy (IEA 2022). Relative price spreads—spot LNG vs domestic fuels—drive procurement quarter to quarter, prompting fuel swaps when coal or naphtha becomes cheaper. Pipeline and burner infrastructure create switching frictions but do not prevent shifts. Gradual carbon policies and rising non‑fossil capacity improve gas economics over time.

Contract structures and flexibility

Contract structures such as take-or-pay (typically 70–90% cover), ship-or-pay and indexation to JKM/TTF limit buyer leverage, locking revenue. Buyers negotiate flexibility on volumes, make-up gas and regas slots; sophisticated purchasers demand hybrid pricing and portfolio options. GAIL reported ~80% pipeline utilization in 2024, balancing utilization stability with commercial agility.

- Take-or-pay: 70–90% capacity cover

- Indexation: JKM/TTF-linked contracts

- Flexibility: volumes, make-up gas, re-gas slots

- Buyers: seek hybrid pricing/portfolio solutions

Service quality and reliability

Pipeline uptime and pressure maintenance drive buyer stickiness for GAIL; reported transmission availability exceeded 99% in 2024, materially lowering customers’ willingness to switch. Scheduling discipline and value-added services like portfolio optimization and balancing—handling ~13,700 km of pipeline and ~40 bcm throughput in 2024—increase retention. Even short outages or curtailments rapidly erode that leverage.

- Uptime: >99% (2024)

- Network: ~13,700 km (2024)

- Throughput: ~40 bcm (2024)

- Value-added: balancing, portfolio optimization

13,700 km network, 40 bcm throughput curb buyer leverage

Large industrials, fertiliser, power and 200+ CGDs (2024) exert significant bargaining via volume and alternatives, but take-or-pay (70–90%) and ~80% pipeline utilization limit short-term leverage. GAIL’s ~13,700 km network, >99% uptime and ~40 bcm throughput (2024) increase customer stickiness. Indexation to JKM/TTF and spot LNG spreads keep price sensitivity high.

| Metric | 2024 |

|---|---|

| Pipeline km | ~13,700 |

| Throughput | ~40 bcm |

| Uptime | >99% |

| CGDs | >200 |

| Take-or-pay | 70–90% |

| Utilization | ~80% |

Full Version Awaits

GAIL India Porter's Five Forces Analysis

This Porter’s Five Forces analysis of GAIL India evaluates competitive rivalry, supplier and buyer power, threat of substitutes and barriers to entry to determine industry attractiveness and strategic risks. It blends quantitative and qualitative insights for investors, analysts and executives to support valuation and strategic decisions. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file.

Description

A Must-Have Tool for Decision-Makers

GAIL India's Porter's Five Forces snapshot highlights strong supplier influence from global gas producers, moderate buyer power amid regulated tariffs, limited threat of new entrants due to high infrastructure barriers, and pressure from substitutes like renewables; rivalry is moderate given state-backed scale. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore GAIL India’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated upstream gas sources

Domestic gas in India is produced predominantly by a small set of players — ONGC, OIL and Reliance-BP — concentrating upstream leverage; imports are similarly focused toward major LNG suppliers such as Qatar and the US, increasing supplier power during tight global markets. Scarcity episodes in 2022–24 saw spot LNG spikes that shifted pricing upstream, pressuring buyers. GAIL reduces risk through diversified sourcing, long‑term contracts and portfolio optimization.

Long-term LNG contracts vs spot volatility

GAIL’s multi-year LNG contracts underpin the bulk of its supply, stabilizing volumes and base pricing, while the 2022–23 global spot surge (peak spot TTF/Asia prices exceeded 60 USD/MMBtu) illustrated how spot spikes can compress margins and prompt renegotiation pressure. Contract flexibility and destination-swap clauses plus portfolio hedging temper short-term exposure, but cyclical spot swings continue to impact margins during tight markets.

Regulatory pricing frameworks

APM pricing and government caps/floors materially influence domestic gas transfer prices, so policy changes can curtail or enhance supplier bargaining power; examples include administered pricing linkages and occasional cap directives affecting LNG swaps. GAIL’s transmission tariffs are regulated by PNGRB, partially insulating pipeline revenues, while its pipeline network of about 14,000 km (circa 2024) keeps throughput fees stable. Upstream price revisions, however, directly ripple through GAIL’s marketing margins and trading book.

Specialized equipment and EPC inputs

Pipelines, compressors and cryogenic equipment are sourced from a narrow vendor base, with typical 2024 lead times of 12–18 months that, together with volatile global steel cycles, materially influence project costs and schedules.

Vendor prequalification lowers operational risk but further restricts suppliers; GAIL’s scale purchasing and large annual procurement volumes partially offset supplier leverage.

- Limited vendor pool increases supplier power

- Lead times 12–18 months (2024)

- Steel cycle volatility impacts capex and timelines

- Prequalification reduces risk but narrows options

- Scale purchasing provides countervailing buying power

Infrastructure and terminal access

- 42 MTPA India regas capacity (2024)

- 13,747 km GAIL pipeline (2024)

- Long-term access = higher bargaining power

- Capacity additions reduce supplier leverage

Supplier leverage rising; long‑term LNG contracts and 13,747 km pipeline reduce shock risk

Upstream supply is concentrated (ONGC, OIL, Reliance‑BP), raising supplier leverage; spot LNG shocks (peak >60 USD/MMBtu in 2022–23) stressed margins. GAIL offsets via long‑term LNG contracts, swaps and a 13,747 km pipeline (2024). Vendor lead times 12–18 months and steel cycles raise capex risk despite scale purchasing.

| Metric | 2024 |

|---|---|

| Regas capacity | 42 MTPA |

| GAIL pipeline | 13,747 km |

| Lead times | 12–18 months |

| Spot peak | >60 USD/MMBtu (2022–23) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to GAIL India; evaluates supplier and buyer power, threat of substitutes and new entrants, and competitive rivalry, highlighting disruptive forces and strategic implications for pricing, margins, and market share.

Clear one-sheet Porter's Five Forces for GAIL India—condenses supplier, buyer, entrant, substitute and rivalry pressures into a decision-ready snapshot to speed strategy and investment calls.

Customers Bargaining Power

Large, concentrated industrial offtakers

Fertilizer, power, refineries and major industrials take sizable volumes from GAIL, giving them strong bargaining leverage through scale and alternative-fuel options, especially as India expands LNG imports; GAIL operates a pipeline network exceeding 13,000 km (2024). Take-or-pay contracts and allocation priorities, however, limit immediate buyer power. Deep operational relationships and reliability remain key differentiators for GAIL.

CGD and city gas demand dynamics

Over 200 CGD entities operate as of 2024, increasing buyer clout and price sensitivity versus suppliers; many procure via short-term contracts and push for volume discounts. Related-party or strategic-partner CGDs (joint ventures with marketing or distribution links) soften pure adversarial bargaining. Regulatory pass-throughs of feedstock and transportation tariffs dampen end-customer elasticity, while multiple competing CGDs in some geographies intensify negotiations.

Fuel-switching alternatives

Buyers can substitute gas with coal, LPG, naphtha or renewables where feasible, keeping gas demand elastic; coal still supplies about 70% of India’s power (IEA 2023) while gas is roughly 6% of primary energy (IEA 2022). Relative price spreads—spot LNG vs domestic fuels—drive procurement quarter to quarter, prompting fuel swaps when coal or naphtha becomes cheaper. Pipeline and burner infrastructure create switching frictions but do not prevent shifts. Gradual carbon policies and rising non‑fossil capacity improve gas economics over time.

Contract structures and flexibility

Contract structures such as take-or-pay (typically 70–90% cover), ship-or-pay and indexation to JKM/TTF limit buyer leverage, locking revenue. Buyers negotiate flexibility on volumes, make-up gas and regas slots; sophisticated purchasers demand hybrid pricing and portfolio options. GAIL reported ~80% pipeline utilization in 2024, balancing utilization stability with commercial agility.

- Take-or-pay: 70–90% capacity cover

- Indexation: JKM/TTF-linked contracts

- Flexibility: volumes, make-up gas, re-gas slots

- Buyers: seek hybrid pricing/portfolio solutions

Service quality and reliability

Pipeline uptime and pressure maintenance drive buyer stickiness for GAIL; reported transmission availability exceeded 99% in 2024, materially lowering customers’ willingness to switch. Scheduling discipline and value-added services like portfolio optimization and balancing—handling ~13,700 km of pipeline and ~40 bcm throughput in 2024—increase retention. Even short outages or curtailments rapidly erode that leverage.

- Uptime: >99% (2024)

- Network: ~13,700 km (2024)

- Throughput: ~40 bcm (2024)

- Value-added: balancing, portfolio optimization

13,700 km network, 40 bcm throughput curb buyer leverage

Large industrials, fertiliser, power and 200+ CGDs (2024) exert significant bargaining via volume and alternatives, but take-or-pay (70–90%) and ~80% pipeline utilization limit short-term leverage. GAIL’s ~13,700 km network, >99% uptime and ~40 bcm throughput (2024) increase customer stickiness. Indexation to JKM/TTF and spot LNG spreads keep price sensitivity high.

| Metric | 2024 |

|---|---|

| Pipeline km | ~13,700 |

| Throughput | ~40 bcm |

| Uptime | >99% |

| CGDs | >200 |

| Take-or-pay | 70–90% |

| Utilization | ~80% |

Full Version Awaits

GAIL India Porter's Five Forces Analysis

This Porter’s Five Forces analysis of GAIL India evaluates competitive rivalry, supplier and buyer power, threat of substitutes and barriers to entry to determine industry attractiveness and strategic risks. It blends quantitative and qualitative insights for investors, analysts and executives to support valuation and strategic decisions. You're looking at the actual document. Once you complete your purchase, you’ll get instant access to this exact file.