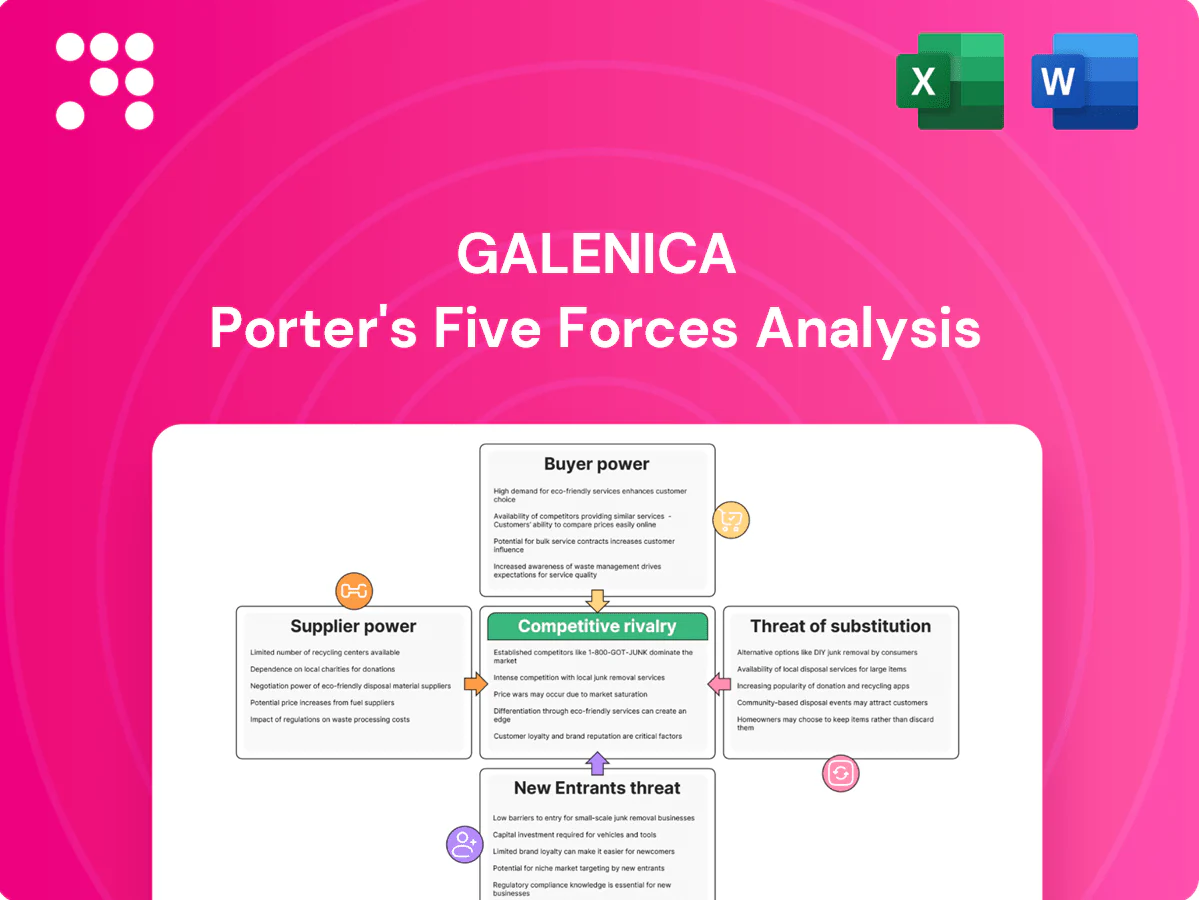

Galenica Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Galenica faces moderate supplier power, high buyer expectations, regulatory nuances, limited substitutes for core services, and evolving competitive threats. This snapshot highlights where profitability is constrained and where strategic levers exist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Galenica’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Patent pharma concentration

Originator drug makers with patented portfolios command favorable terms because limited alternatives and largely inelastic demand give them pricing power; IQVIA estimates global pharma sales around 1.6 trillion USD in 2024, concentrating value with patent holders. Brand equity and regulatory exclusivity (patent terms up to 20 years) elevate leverage over prices and supply allocations. Galenica’s scale aids negotiation, but reliance on single‑source molecules and periodic shortages keeps supplier power elevated.

Generics and OTC fragmentation

Generic manufacturers and OTC suppliers remain highly fragmented, with generics accounting for over 80% of prescriptions by volume in many European markets in 2024, enabling competitive bidding and multisourcing that weakens supplier power on commoditized molecules.

Galenica can rotate SKUs and expand private-label penetration to pressure margins; parallel import options across EU/CH where permitted add tangible negotiating leverage against single-source suppliers.

Vertical integration buffer

Galenica’s vertical integration — own brands and wholesale via Galexis — strengthened its bargaining position in 2024 by reducing reliance on external suppliers and increasing private‑label penetration, improving margin capture across retail channels.

Controlled distribution through Galexis and in‑house brands shifts margin upstream but cannot substitute specialist Rx therapies or patented medicines that remain supplier‑dependent.

Thus integration moderates supplier power rather than eliminating it, leaving key therapeutic categories exposed to supplier constraints in 2024.

Regulatory and quality constraints

Strict GDP/GMP and Swissmedic requirements make supplier switching slow, raising effective lock‑in for sterile, cold‑chain and serialized products; by 2024 onboarding commonly requires 6–12 months. Qualification, audits and serialization add frictions and one‑time compliance costs often in the tens of thousands CHF, which entrenches incumbents and modestly increases supplier leverage in sensitive segments.

- Lock‑in: long qualification cycles (6–12 months)

- Costs: serialization/audits often tens of thousands CHF

- Result: modestly higher supplier bargaining power in regulated segments

Non-pharma vendors’ influence

IT platforms, logistics partners and medical device OEMs can exert significant leverage over Galenica when solutions require deep integration, certified interfaces, or regulated device support, creating lock‑in through transition costs and SLA commitments.

Galenica reduces supplier power via multi‑vendor procurement, selective in‑house development and strategic backups, yet niche technologies and certified medical OEMs continue to command premium pricing.

- Vendor lock‑in: transition and integration costs

- Service risk: SLA dependence on key partners

- Mitigation: multi‑vendor + in‑house capability

- Residual risk: niche OEMs retain pricing power

Originator patents drive pricing power; generics volume (>80%) fragments supplier leverage

Originator patent holders command pricing power (global pharma sales ~1.6 trillion USD in 2024, IQVIA) while generics/OTC fragmentation (>80% RX by volume in many EU markets, 2024) softens supplier leverage. Galenica’s vertical integration and private‑label growth moderate but do not remove dependence on single‑source patented therapies. Regulatory onboarding (6–12 months) and serialization/audits (tens of thousands CHF) sustain supplier lock‑in in sensitive segments.

| Metric | 2024 |

|---|---|

| Global pharma sales | ~1.6 trillion USD (IQVIA) |

| EU generics share | >80% prescriptions by volume |

| Onboarding time | 6–12 months |

| Compliance costs | Tens of thousands CHF |

What is included in the product

Concise Porter's Five Forces assessment of Galenica, uncovering competitive intensity, buyer/supplier power, substitute threats, and entry barriers shaping its profitability. Actionable insights highlight disruptive entrants, pricing leverage, and strategic defenses to sustain market position.

One-sheet Galenica Porter's Five Forces summarizes competitive pressures with an interactive spider chart and customizable pressure levels—clean, no-code layout ready to drop into decks or dashboards.

Customers Bargaining Power

Fragmented consumers, regulated Rx

End‑consumers are numerous and individually weak, and in Switzerland Rx prices and reimbursement remain regulated by the Federal Office of Public Health (FOPH) as of 2024, keeping buyer power on prescriptions low; choice is driven by prescribers and formularies. In OTC and beauty segments price sensitivity is higher, increasing bargaining power. Retail loyalty programs and store proximity materially reduce switching.

Institutional B2B purchasers

Institutional B2B purchasers such as hospitals, physician networks and pharmacy groups wield volume-based leverage, using tenders and framework contracts that in 2024 commonly span 12–36 months and compress wholesale margins by up to mid-single digits.

Consolidation of providers—greater regional hospital group concentration—intensifies bargaining pressure, making service differentiation, guaranteed fill rates and same‑day delivery performance critical to defend pricing.

Insurers and formularies

In 2024 Swiss insurers under LAMal cover >90% of the 8.8 million population and shape demand through reimbursement, reference pricing and therapeutic substitution, limiting Galenica’s ability to upsell premium brands. Co‑pay rules—10% coinsurance up to CHF 700/year—shift patients toward lower‑cost OTC and Rx alternatives. Insurer negotiations upstream compress supplier prices, passing margin pressure downstream to Galenica.

Channel transparency and e-commerce

Price comparison tools and online pharmacies boost transparency, raising buyer power in OTC and wellness; the global online pharmacy market is estimated to grow at about 11% CAGR (2024–2030), amplifying consumer leverage. Click‑and‑collect and mail‑order lower switching costs, while fast service and convenience (same‑day/next‑day delivery) can offset pure price sensitivity.

- Price comparison use ~60% (2023)

- Online pharmacy CAGR ~11% (2024–2030)

- Click‑and‑collect/mail‑order reduce switching friction

- Speed/convenience mitigates price focus

Private label acceptance

Consumer openness to private label gives Galenica a counterweight against buyer power: growing acceptance improves margins and weakens buyers' price leverage. Store brands deliver value and differentiation, reducing direct price comparability, but quality slippage risks switches back to national brands. Maintaining trust through quality and transparency preserves this leverage; private-label share in Swiss retail reached about 41% in 2024 (NielsenIQ).

- Counterweight vs buyers: higher margins

- Differentiation: lowers price comparability

- Risk: quality slip → brand switching

- 2024: private-label share ~41%

Swiss pharmacy market - low Rx bargaining; LAMal >90%, private-label 41%, online CAGR ~11%

Swiss end‑consumers are fragmented with low Rx bargaining power due to FOPH price/reimbursement rules and prescriber-driven choice; insurers under LAMal cover >90% of 8.8M (2024). OTC/beauty buyers are more price‑sensitive and online tools raise transparency; private‑label share ~41% (2024), online pharmacy CAGR ~11% (2024–2030).

| Metric | Value |

|---|---|

| Population covered by LAMal | >90% |

| Swiss population | 8.8M (2024) |

| Private‑label share | 41% (2024) |

| Price comparison use | ~60% (2023) |

| Online pharmacy CAGR | ~11% (2024–2030) |

Preview the Actual Deliverable

Galenica Porter's Five Forces Analysis

This preview shows the exact Galenica Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It provides a professional, fully formatted evaluation of industry rivalry, supplier and buyer power, and the threats of entry and substitutes, with clear strategic implications. The document is ready for download and use the moment you buy. You're viewing the final deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Galenica faces moderate supplier power, high buyer expectations, regulatory nuances, limited substitutes for core services, and evolving competitive threats. This snapshot highlights where profitability is constrained and where strategic levers exist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Galenica’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Patent pharma concentration

Originator drug makers with patented portfolios command favorable terms because limited alternatives and largely inelastic demand give them pricing power; IQVIA estimates global pharma sales around 1.6 trillion USD in 2024, concentrating value with patent holders. Brand equity and regulatory exclusivity (patent terms up to 20 years) elevate leverage over prices and supply allocations. Galenica’s scale aids negotiation, but reliance on single‑source molecules and periodic shortages keeps supplier power elevated.

Generics and OTC fragmentation

Generic manufacturers and OTC suppliers remain highly fragmented, with generics accounting for over 80% of prescriptions by volume in many European markets in 2024, enabling competitive bidding and multisourcing that weakens supplier power on commoditized molecules.

Galenica can rotate SKUs and expand private-label penetration to pressure margins; parallel import options across EU/CH where permitted add tangible negotiating leverage against single-source suppliers.

Vertical integration buffer

Galenica’s vertical integration — own brands and wholesale via Galexis — strengthened its bargaining position in 2024 by reducing reliance on external suppliers and increasing private‑label penetration, improving margin capture across retail channels.

Controlled distribution through Galexis and in‑house brands shifts margin upstream but cannot substitute specialist Rx therapies or patented medicines that remain supplier‑dependent.

Thus integration moderates supplier power rather than eliminating it, leaving key therapeutic categories exposed to supplier constraints in 2024.

Regulatory and quality constraints

Strict GDP/GMP and Swissmedic requirements make supplier switching slow, raising effective lock‑in for sterile, cold‑chain and serialized products; by 2024 onboarding commonly requires 6–12 months. Qualification, audits and serialization add frictions and one‑time compliance costs often in the tens of thousands CHF, which entrenches incumbents and modestly increases supplier leverage in sensitive segments.

- Lock‑in: long qualification cycles (6–12 months)

- Costs: serialization/audits often tens of thousands CHF

- Result: modestly higher supplier bargaining power in regulated segments

Non-pharma vendors’ influence

IT platforms, logistics partners and medical device OEMs can exert significant leverage over Galenica when solutions require deep integration, certified interfaces, or regulated device support, creating lock‑in through transition costs and SLA commitments.

Galenica reduces supplier power via multi‑vendor procurement, selective in‑house development and strategic backups, yet niche technologies and certified medical OEMs continue to command premium pricing.

- Vendor lock‑in: transition and integration costs

- Service risk: SLA dependence on key partners

- Mitigation: multi‑vendor + in‑house capability

- Residual risk: niche OEMs retain pricing power

Originator patents drive pricing power; generics volume (>80%) fragments supplier leverage

Originator patent holders command pricing power (global pharma sales ~1.6 trillion USD in 2024, IQVIA) while generics/OTC fragmentation (>80% RX by volume in many EU markets, 2024) softens supplier leverage. Galenica’s vertical integration and private‑label growth moderate but do not remove dependence on single‑source patented therapies. Regulatory onboarding (6–12 months) and serialization/audits (tens of thousands CHF) sustain supplier lock‑in in sensitive segments.

| Metric | 2024 |

|---|---|

| Global pharma sales | ~1.6 trillion USD (IQVIA) |

| EU generics share | >80% prescriptions by volume |

| Onboarding time | 6–12 months |

| Compliance costs | Tens of thousands CHF |

What is included in the product

Concise Porter's Five Forces assessment of Galenica, uncovering competitive intensity, buyer/supplier power, substitute threats, and entry barriers shaping its profitability. Actionable insights highlight disruptive entrants, pricing leverage, and strategic defenses to sustain market position.

One-sheet Galenica Porter's Five Forces summarizes competitive pressures with an interactive spider chart and customizable pressure levels—clean, no-code layout ready to drop into decks or dashboards.

Customers Bargaining Power

Fragmented consumers, regulated Rx

End‑consumers are numerous and individually weak, and in Switzerland Rx prices and reimbursement remain regulated by the Federal Office of Public Health (FOPH) as of 2024, keeping buyer power on prescriptions low; choice is driven by prescribers and formularies. In OTC and beauty segments price sensitivity is higher, increasing bargaining power. Retail loyalty programs and store proximity materially reduce switching.

Institutional B2B purchasers

Institutional B2B purchasers such as hospitals, physician networks and pharmacy groups wield volume-based leverage, using tenders and framework contracts that in 2024 commonly span 12–36 months and compress wholesale margins by up to mid-single digits.

Consolidation of providers—greater regional hospital group concentration—intensifies bargaining pressure, making service differentiation, guaranteed fill rates and same‑day delivery performance critical to defend pricing.

Insurers and formularies

In 2024 Swiss insurers under LAMal cover >90% of the 8.8 million population and shape demand through reimbursement, reference pricing and therapeutic substitution, limiting Galenica’s ability to upsell premium brands. Co‑pay rules—10% coinsurance up to CHF 700/year—shift patients toward lower‑cost OTC and Rx alternatives. Insurer negotiations upstream compress supplier prices, passing margin pressure downstream to Galenica.

Channel transparency and e-commerce

Price comparison tools and online pharmacies boost transparency, raising buyer power in OTC and wellness; the global online pharmacy market is estimated to grow at about 11% CAGR (2024–2030), amplifying consumer leverage. Click‑and‑collect and mail‑order lower switching costs, while fast service and convenience (same‑day/next‑day delivery) can offset pure price sensitivity.

- Price comparison use ~60% (2023)

- Online pharmacy CAGR ~11% (2024–2030)

- Click‑and‑collect/mail‑order reduce switching friction

- Speed/convenience mitigates price focus

Private label acceptance

Consumer openness to private label gives Galenica a counterweight against buyer power: growing acceptance improves margins and weakens buyers' price leverage. Store brands deliver value and differentiation, reducing direct price comparability, but quality slippage risks switches back to national brands. Maintaining trust through quality and transparency preserves this leverage; private-label share in Swiss retail reached about 41% in 2024 (NielsenIQ).

- Counterweight vs buyers: higher margins

- Differentiation: lowers price comparability

- Risk: quality slip → brand switching

- 2024: private-label share ~41%

Swiss pharmacy market - low Rx bargaining; LAMal >90%, private-label 41%, online CAGR ~11%

Swiss end‑consumers are fragmented with low Rx bargaining power due to FOPH price/reimbursement rules and prescriber-driven choice; insurers under LAMal cover >90% of 8.8M (2024). OTC/beauty buyers are more price‑sensitive and online tools raise transparency; private‑label share ~41% (2024), online pharmacy CAGR ~11% (2024–2030).

| Metric | Value |

|---|---|

| Population covered by LAMal | >90% |

| Swiss population | 8.8M (2024) |

| Private‑label share | 41% (2024) |

| Price comparison use | ~60% (2023) |

| Online pharmacy CAGR | ~11% (2024–2030) |

Preview the Actual Deliverable

Galenica Porter's Five Forces Analysis

This preview shows the exact Galenica Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It provides a professional, fully formatted evaluation of industry rivalry, supplier and buyer power, and the threats of entry and substitutes, with clear strategic implications. The document is ready for download and use the moment you buy. You're viewing the final deliverable.

Description

Go Beyond the Preview—Access the Full Strategic Report

Galenica faces moderate supplier power, high buyer expectations, regulatory nuances, limited substitutes for core services, and evolving competitive threats. This snapshot highlights where profitability is constrained and where strategic levers exist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Galenica’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Patent pharma concentration

Originator drug makers with patented portfolios command favorable terms because limited alternatives and largely inelastic demand give them pricing power; IQVIA estimates global pharma sales around 1.6 trillion USD in 2024, concentrating value with patent holders. Brand equity and regulatory exclusivity (patent terms up to 20 years) elevate leverage over prices and supply allocations. Galenica’s scale aids negotiation, but reliance on single‑source molecules and periodic shortages keeps supplier power elevated.

Generics and OTC fragmentation

Generic manufacturers and OTC suppliers remain highly fragmented, with generics accounting for over 80% of prescriptions by volume in many European markets in 2024, enabling competitive bidding and multisourcing that weakens supplier power on commoditized molecules.

Galenica can rotate SKUs and expand private-label penetration to pressure margins; parallel import options across EU/CH where permitted add tangible negotiating leverage against single-source suppliers.

Vertical integration buffer

Galenica’s vertical integration — own brands and wholesale via Galexis — strengthened its bargaining position in 2024 by reducing reliance on external suppliers and increasing private‑label penetration, improving margin capture across retail channels.

Controlled distribution through Galexis and in‑house brands shifts margin upstream but cannot substitute specialist Rx therapies or patented medicines that remain supplier‑dependent.

Thus integration moderates supplier power rather than eliminating it, leaving key therapeutic categories exposed to supplier constraints in 2024.

Regulatory and quality constraints

Strict GDP/GMP and Swissmedic requirements make supplier switching slow, raising effective lock‑in for sterile, cold‑chain and serialized products; by 2024 onboarding commonly requires 6–12 months. Qualification, audits and serialization add frictions and one‑time compliance costs often in the tens of thousands CHF, which entrenches incumbents and modestly increases supplier leverage in sensitive segments.

- Lock‑in: long qualification cycles (6–12 months)

- Costs: serialization/audits often tens of thousands CHF

- Result: modestly higher supplier bargaining power in regulated segments

Non-pharma vendors’ influence

IT platforms, logistics partners and medical device OEMs can exert significant leverage over Galenica when solutions require deep integration, certified interfaces, or regulated device support, creating lock‑in through transition costs and SLA commitments.

Galenica reduces supplier power via multi‑vendor procurement, selective in‑house development and strategic backups, yet niche technologies and certified medical OEMs continue to command premium pricing.

- Vendor lock‑in: transition and integration costs

- Service risk: SLA dependence on key partners

- Mitigation: multi‑vendor + in‑house capability

- Residual risk: niche OEMs retain pricing power

Originator patents drive pricing power; generics volume (>80%) fragments supplier leverage

Originator patent holders command pricing power (global pharma sales ~1.6 trillion USD in 2024, IQVIA) while generics/OTC fragmentation (>80% RX by volume in many EU markets, 2024) softens supplier leverage. Galenica’s vertical integration and private‑label growth moderate but do not remove dependence on single‑source patented therapies. Regulatory onboarding (6–12 months) and serialization/audits (tens of thousands CHF) sustain supplier lock‑in in sensitive segments.

| Metric | 2024 |

|---|---|

| Global pharma sales | ~1.6 trillion USD (IQVIA) |

| EU generics share | >80% prescriptions by volume |

| Onboarding time | 6–12 months |

| Compliance costs | Tens of thousands CHF |

What is included in the product

Concise Porter's Five Forces assessment of Galenica, uncovering competitive intensity, buyer/supplier power, substitute threats, and entry barriers shaping its profitability. Actionable insights highlight disruptive entrants, pricing leverage, and strategic defenses to sustain market position.

One-sheet Galenica Porter's Five Forces summarizes competitive pressures with an interactive spider chart and customizable pressure levels—clean, no-code layout ready to drop into decks or dashboards.

Customers Bargaining Power

Fragmented consumers, regulated Rx

End‑consumers are numerous and individually weak, and in Switzerland Rx prices and reimbursement remain regulated by the Federal Office of Public Health (FOPH) as of 2024, keeping buyer power on prescriptions low; choice is driven by prescribers and formularies. In OTC and beauty segments price sensitivity is higher, increasing bargaining power. Retail loyalty programs and store proximity materially reduce switching.

Institutional B2B purchasers

Institutional B2B purchasers such as hospitals, physician networks and pharmacy groups wield volume-based leverage, using tenders and framework contracts that in 2024 commonly span 12–36 months and compress wholesale margins by up to mid-single digits.

Consolidation of providers—greater regional hospital group concentration—intensifies bargaining pressure, making service differentiation, guaranteed fill rates and same‑day delivery performance critical to defend pricing.

Insurers and formularies

In 2024 Swiss insurers under LAMal cover >90% of the 8.8 million population and shape demand through reimbursement, reference pricing and therapeutic substitution, limiting Galenica’s ability to upsell premium brands. Co‑pay rules—10% coinsurance up to CHF 700/year—shift patients toward lower‑cost OTC and Rx alternatives. Insurer negotiations upstream compress supplier prices, passing margin pressure downstream to Galenica.

Channel transparency and e-commerce

Price comparison tools and online pharmacies boost transparency, raising buyer power in OTC and wellness; the global online pharmacy market is estimated to grow at about 11% CAGR (2024–2030), amplifying consumer leverage. Click‑and‑collect and mail‑order lower switching costs, while fast service and convenience (same‑day/next‑day delivery) can offset pure price sensitivity.

- Price comparison use ~60% (2023)

- Online pharmacy CAGR ~11% (2024–2030)

- Click‑and‑collect/mail‑order reduce switching friction

- Speed/convenience mitigates price focus

Private label acceptance

Consumer openness to private label gives Galenica a counterweight against buyer power: growing acceptance improves margins and weakens buyers' price leverage. Store brands deliver value and differentiation, reducing direct price comparability, but quality slippage risks switches back to national brands. Maintaining trust through quality and transparency preserves this leverage; private-label share in Swiss retail reached about 41% in 2024 (NielsenIQ).

- Counterweight vs buyers: higher margins

- Differentiation: lowers price comparability

- Risk: quality slip → brand switching

- 2024: private-label share ~41%

Swiss pharmacy market - low Rx bargaining; LAMal >90%, private-label 41%, online CAGR ~11%

Swiss end‑consumers are fragmented with low Rx bargaining power due to FOPH price/reimbursement rules and prescriber-driven choice; insurers under LAMal cover >90% of 8.8M (2024). OTC/beauty buyers are more price‑sensitive and online tools raise transparency; private‑label share ~41% (2024), online pharmacy CAGR ~11% (2024–2030).

| Metric | Value |

|---|---|

| Population covered by LAMal | >90% |

| Swiss population | 8.8M (2024) |

| Private‑label share | 41% (2024) |

| Price comparison use | ~60% (2023) |

| Online pharmacy CAGR | ~11% (2024–2030) |

Preview the Actual Deliverable

Galenica Porter's Five Forces Analysis

This preview shows the exact Galenica Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It provides a professional, fully formatted evaluation of industry rivalry, supplier and buyer power, and the threats of entry and substitutes, with clear strategic implications. The document is ready for download and use the moment you buy. You're viewing the final deliverable.