Gale Pacific Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

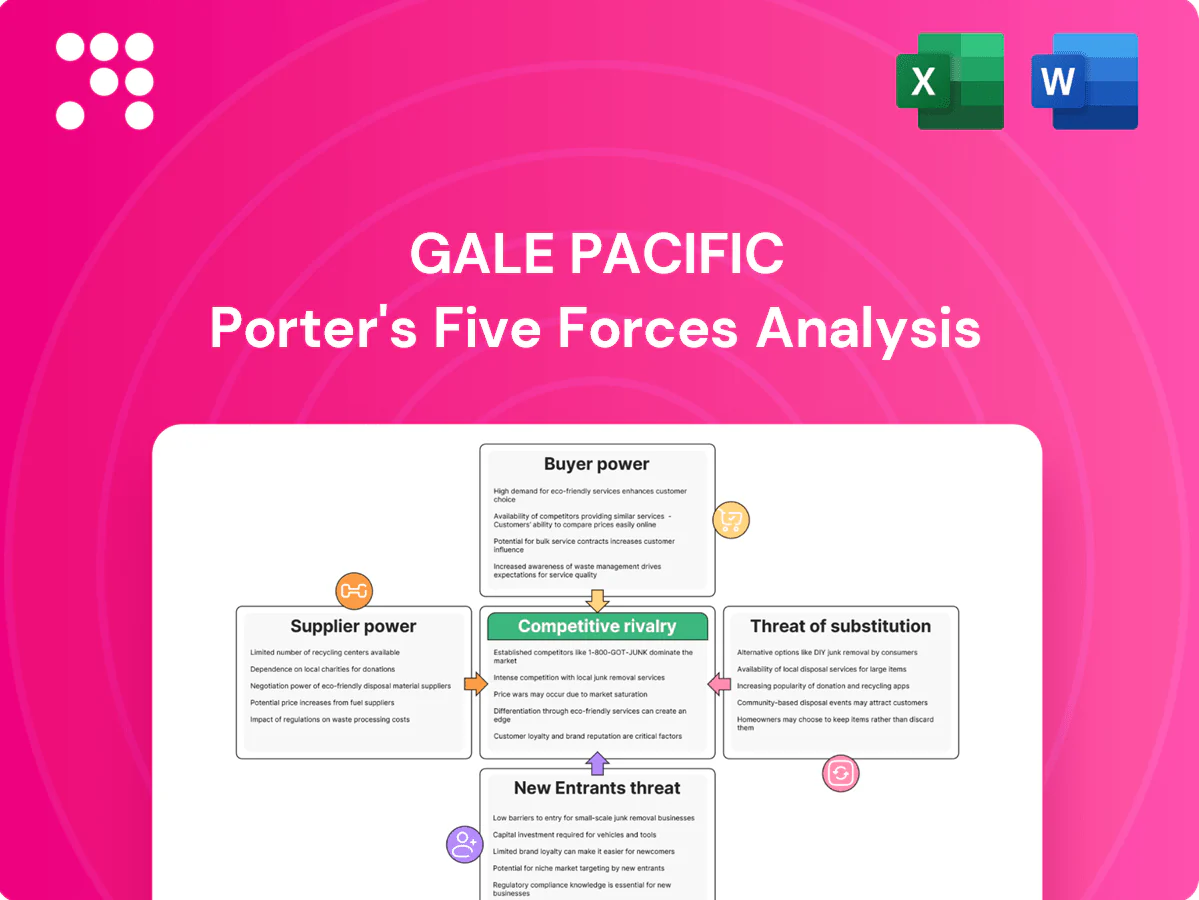

Gale Pacific’s Porter’s Five Forces snapshot highlights buyer and supplier power, substitution risk, rivalry intensity, and barriers to entry shaping its competitive landscape. Our concise view flags key vulnerabilities and strategic levers for growth. This brief only scratches the surface—unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights. Purchase the complete report to inform smarter strategy and investment decisions.

Suppliers Bargaining Power

Concentration in polymers and UV additives

Key inputs like HDPE resins, UV stabilizers and pigments are supplied by a relatively concentrated group of chemical majors; top 5 resin producers held roughly 40% of global HDPE capacity in 2024, tightening leverage. This concentration raises switching costs and limits Gale Pacific’s bargaining latitude. Long-term contracts and dual-sourcing reduce risk but may not fully offset specialty-additive scarcity. Supplier qualification for performance and compliance further entrenches these relationships.

Commodity price volatility and pass-through

Resin and energy price swings (Brent ~85 USD/bbl in 2024) directly inflate Gale Pacific’s fabric costs, with polymer feedstock volatility up markedly versus 2023; weak pass-through clauses would force margin compression and raise supplier leverage. Hedging and extra inventory can blunt spikes but add carrying costs and capital strain. Suppliers may time increases or add surcharges in tight markets, amplifying short-term pricing power.

Specialized machinery and tooling

Knitting, weaving, coating and extrusion lines require specialized OEM parts and service, concentrating supply for key components. Dependence on a few machinery vendors creates hold-up risks during maintenance or upgrades. Lead times for tooling and spares, often up to 24 weeks, elevate supplier power during outages. Tight SLAs and strengthened in-house maintenance capabilities help rebalance that power.

Sustainability and compliance inputs

Sustainability and compliance inputs shrink Gale Pacific’s qualified supplier pool as 2024 demand for recycled content and low‑VOC coatings rises, letting certified suppliers command price premiums or allocation priority and increasing supplier leverage.

Higher qualification costs and extended testing cycles elevate switching friction and supplier influence, pressuring margins and lead times.

- 2024 trend: certified materials command premiums; longer approval cycles raise sourcing costs

- Effect: fewer suppliers, higher switching friction, stronger supplier bargaining power

Logistics and freight constraints

Supply-side freight leverage rose as global liner fleet reached about 27.9m TEU in 2024 with capacity up ~3.5% year-on-year (Alphaliner), meaning port congestion and elevated container rates amplify supplier bargaining power and allow carriers to pass costs via INCOTERMS.

Nearshoring and diversified lanes lower exposure but demand planning and capital; reliability premiums often spike in peak seasons and may be unavoidable for timely supply to Gale Pacific.

- Global fleet 2024: ~27.9m TEU, +3.5% YoY

- Freight terms (INCOTERMS) enable cost/delivery pass-through

- Nearshoring reduces risk but increases capex/lead-time

- Peak-season reliability premiums common

Supply risk: Top-5 HDPE ~40%, Brent ~85 USD/bbl

Supplier concentration (top‑5 HDPE ~40% global capacity in 2024), resin/feedstock price volatility (Brent ~85 USD/bbl) and scarce certified inputs raise switching costs and margin risk; long lead times (spares/tooling up to 24 weeks) and carrier leverage (global fleet ~27.9m TEU, +3.5% YoY) amplify supplier power despite nearshoring and hedging mitigants.

| Metric | 2024 value | Impact |

|---|---|---|

| Top‑5 HDPE share | ~40% | High concentration |

| Brent | ~85 USD/bbl | Cost pass‑through risk |

| Global fleet | 27.9m TEU (+3.5%) | Freight leverage |

| Lead times | Up to 24 wks | Hold‑up risk |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Gale Pacific; evaluates supplier and buyer power, substitutes, rivalry, and barriers to entry while identifying disruptive threats and strategic levers to protect profitability and market share.

A one-sheet Porter's Five Forces for Gale Pacific—quickly reveal competitive pressures and strategic levers to alleviate decision paralysis. Customizable scores and an instant radar chart make scenario updates simple and slide-ready for boardrooms or investor decks.

Customers Bargaining Power

Large retailers and distributors

Big-box chains, DIY retailers and wholesalers negotiate steep discounts and terms, with the top 3 customers often representing over 20% of supplier sales; private-label deals and shelf allocation magnify buyer leverage. Vendor scorecards and chargebacks (commonly 1–5% of invoice value) force concessions, and losing a single key account can cut plant utilization by roughly 15–30%.

Professional specifiers and project buyers

Architects, builders and facility managers often dictate brand choice via specs, with 2024 surveys showing about 70% of commercial projects being spec-driven; they demand proven UV performance, certifications and 10-year-plus warranties, enabling direct price comparisons. Project-based procurement increases bidding and discounting pressure, with tender-driven projects seeing average bid discounts of 5–12% in 2024. Late-stage value-engineering commonly substitutes lower grades to cut costs.

Switching costs and product comparability

For commoditized shade cloth and screens perceived switching costs are low, and with comparable performance claims buyers often select on price; the global shade cloth market was estimated at about USD 1.1 billion in 2024, underscoring price sensitivity. Proprietary fabric technologies and branded accessories increase stickiness through system integration and can justify 10–30% price premiums. Robust after-sales support and warranties (multi-year coverage) further reduce churn.

Information transparency and e-commerce

Online marketplaces expose prices, reviews and alternatives, empowering buyers and contributing to global e-commerce reaching 22.3% of retail sales in 2024 (Statista). Direct-to-consumer channels compress margins when price parity is expected, while high-quality content and strong brand reputation still justify premiums. Dynamic pricing across channels requires careful governance to avoid channel conflict and margin erosion.

- Price transparency: comparison-enabled shopping

- D2C impact: margin compression risk

- Brand/content: premium justification

- Dynamic pricing: need for channel rules

Demand cyclicality and seasonality

Seasonal peaks let buyers time purchases for discounts or leverage forecast uncertainty, while weather-driven demand shocks can force Gale Pacific into excess inventory markdowns. Pre-season commitments and vendor-managed inventory reduce buyer bargaining but shift working capital and inventory risk back to Gale Pacific. Flexible production scheduling and rapid fulfilment help sustain service levels during volatile demand.

- Buyers time purchases for discounts

- Weather shocks cause markdowns

- Pre-season/VMI shifts capital to Gale

- Flexible scheduling sustains service

Concentration, chargebacks and e-commerce pressure margins; proprietary tech can command premiums

Buyers hold high leverage: top 3 customers >20% of sales, chargebacks 1–5% of invoices and losing one account can cut utilization 15–30%. Spec-driven procurement (≈70% commercial projects in 2024) and price-focused commoditized products compress margins, while proprietary tech and warranties can command 10–30% premiums. E-commerce exposure (22.3% of retail sales in 2024) increases price transparency and D2C margin pressure.

| Metric | 2024 value | Impact |

|---|---|---|

| Top-3 customer share | >20% | Concentration risk |

| Chargebacks | 1–5% invoice | Profit erosion |

| Spec-driven projects | ≈70% | Procurement control |

| Market size | USD 1.1B | Price sensitivity |

| E-commerce | 22.3% | Transparency |

Same Document Delivered

Gale Pacific Porter's Five Forces Analysis

This preview shows the exact Gale Pacific Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. No placeholders, mockups, or samples. You'll get instant access to this identical, professionally prepared file upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Gale Pacific’s Porter’s Five Forces snapshot highlights buyer and supplier power, substitution risk, rivalry intensity, and barriers to entry shaping its competitive landscape. Our concise view flags key vulnerabilities and strategic levers for growth. This brief only scratches the surface—unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights. Purchase the complete report to inform smarter strategy and investment decisions.

Suppliers Bargaining Power

Concentration in polymers and UV additives

Key inputs like HDPE resins, UV stabilizers and pigments are supplied by a relatively concentrated group of chemical majors; top 5 resin producers held roughly 40% of global HDPE capacity in 2024, tightening leverage. This concentration raises switching costs and limits Gale Pacific’s bargaining latitude. Long-term contracts and dual-sourcing reduce risk but may not fully offset specialty-additive scarcity. Supplier qualification for performance and compliance further entrenches these relationships.

Commodity price volatility and pass-through

Resin and energy price swings (Brent ~85 USD/bbl in 2024) directly inflate Gale Pacific’s fabric costs, with polymer feedstock volatility up markedly versus 2023; weak pass-through clauses would force margin compression and raise supplier leverage. Hedging and extra inventory can blunt spikes but add carrying costs and capital strain. Suppliers may time increases or add surcharges in tight markets, amplifying short-term pricing power.

Specialized machinery and tooling

Knitting, weaving, coating and extrusion lines require specialized OEM parts and service, concentrating supply for key components. Dependence on a few machinery vendors creates hold-up risks during maintenance or upgrades. Lead times for tooling and spares, often up to 24 weeks, elevate supplier power during outages. Tight SLAs and strengthened in-house maintenance capabilities help rebalance that power.

Sustainability and compliance inputs

Sustainability and compliance inputs shrink Gale Pacific’s qualified supplier pool as 2024 demand for recycled content and low‑VOC coatings rises, letting certified suppliers command price premiums or allocation priority and increasing supplier leverage.

Higher qualification costs and extended testing cycles elevate switching friction and supplier influence, pressuring margins and lead times.

- 2024 trend: certified materials command premiums; longer approval cycles raise sourcing costs

- Effect: fewer suppliers, higher switching friction, stronger supplier bargaining power

Logistics and freight constraints

Supply-side freight leverage rose as global liner fleet reached about 27.9m TEU in 2024 with capacity up ~3.5% year-on-year (Alphaliner), meaning port congestion and elevated container rates amplify supplier bargaining power and allow carriers to pass costs via INCOTERMS.

Nearshoring and diversified lanes lower exposure but demand planning and capital; reliability premiums often spike in peak seasons and may be unavoidable for timely supply to Gale Pacific.

- Global fleet 2024: ~27.9m TEU, +3.5% YoY

- Freight terms (INCOTERMS) enable cost/delivery pass-through

- Nearshoring reduces risk but increases capex/lead-time

- Peak-season reliability premiums common

Supply risk: Top-5 HDPE ~40%, Brent ~85 USD/bbl

Supplier concentration (top‑5 HDPE ~40% global capacity in 2024), resin/feedstock price volatility (Brent ~85 USD/bbl) and scarce certified inputs raise switching costs and margin risk; long lead times (spares/tooling up to 24 weeks) and carrier leverage (global fleet ~27.9m TEU, +3.5% YoY) amplify supplier power despite nearshoring and hedging mitigants.

| Metric | 2024 value | Impact |

|---|---|---|

| Top‑5 HDPE share | ~40% | High concentration |

| Brent | ~85 USD/bbl | Cost pass‑through risk |

| Global fleet | 27.9m TEU (+3.5%) | Freight leverage |

| Lead times | Up to 24 wks | Hold‑up risk |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Gale Pacific; evaluates supplier and buyer power, substitutes, rivalry, and barriers to entry while identifying disruptive threats and strategic levers to protect profitability and market share.

A one-sheet Porter's Five Forces for Gale Pacific—quickly reveal competitive pressures and strategic levers to alleviate decision paralysis. Customizable scores and an instant radar chart make scenario updates simple and slide-ready for boardrooms or investor decks.

Customers Bargaining Power

Large retailers and distributors

Big-box chains, DIY retailers and wholesalers negotiate steep discounts and terms, with the top 3 customers often representing over 20% of supplier sales; private-label deals and shelf allocation magnify buyer leverage. Vendor scorecards and chargebacks (commonly 1–5% of invoice value) force concessions, and losing a single key account can cut plant utilization by roughly 15–30%.

Professional specifiers and project buyers

Architects, builders and facility managers often dictate brand choice via specs, with 2024 surveys showing about 70% of commercial projects being spec-driven; they demand proven UV performance, certifications and 10-year-plus warranties, enabling direct price comparisons. Project-based procurement increases bidding and discounting pressure, with tender-driven projects seeing average bid discounts of 5–12% in 2024. Late-stage value-engineering commonly substitutes lower grades to cut costs.

Switching costs and product comparability

For commoditized shade cloth and screens perceived switching costs are low, and with comparable performance claims buyers often select on price; the global shade cloth market was estimated at about USD 1.1 billion in 2024, underscoring price sensitivity. Proprietary fabric technologies and branded accessories increase stickiness through system integration and can justify 10–30% price premiums. Robust after-sales support and warranties (multi-year coverage) further reduce churn.

Information transparency and e-commerce

Online marketplaces expose prices, reviews and alternatives, empowering buyers and contributing to global e-commerce reaching 22.3% of retail sales in 2024 (Statista). Direct-to-consumer channels compress margins when price parity is expected, while high-quality content and strong brand reputation still justify premiums. Dynamic pricing across channels requires careful governance to avoid channel conflict and margin erosion.

- Price transparency: comparison-enabled shopping

- D2C impact: margin compression risk

- Brand/content: premium justification

- Dynamic pricing: need for channel rules

Demand cyclicality and seasonality

Seasonal peaks let buyers time purchases for discounts or leverage forecast uncertainty, while weather-driven demand shocks can force Gale Pacific into excess inventory markdowns. Pre-season commitments and vendor-managed inventory reduce buyer bargaining but shift working capital and inventory risk back to Gale Pacific. Flexible production scheduling and rapid fulfilment help sustain service levels during volatile demand.

- Buyers time purchases for discounts

- Weather shocks cause markdowns

- Pre-season/VMI shifts capital to Gale

- Flexible scheduling sustains service

Concentration, chargebacks and e-commerce pressure margins; proprietary tech can command premiums

Buyers hold high leverage: top 3 customers >20% of sales, chargebacks 1–5% of invoices and losing one account can cut utilization 15–30%. Spec-driven procurement (≈70% commercial projects in 2024) and price-focused commoditized products compress margins, while proprietary tech and warranties can command 10–30% premiums. E-commerce exposure (22.3% of retail sales in 2024) increases price transparency and D2C margin pressure.

| Metric | 2024 value | Impact |

|---|---|---|

| Top-3 customer share | >20% | Concentration risk |

| Chargebacks | 1–5% invoice | Profit erosion |

| Spec-driven projects | ≈70% | Procurement control |

| Market size | USD 1.1B | Price sensitivity |

| E-commerce | 22.3% | Transparency |

Same Document Delivered

Gale Pacific Porter's Five Forces Analysis

This preview shows the exact Gale Pacific Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. No placeholders, mockups, or samples. You'll get instant access to this identical, professionally prepared file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Gale Pacific’s Porter’s Five Forces snapshot highlights buyer and supplier power, substitution risk, rivalry intensity, and barriers to entry shaping its competitive landscape. Our concise view flags key vulnerabilities and strategic levers for growth. This brief only scratches the surface—unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable insights. Purchase the complete report to inform smarter strategy and investment decisions.

Suppliers Bargaining Power

Concentration in polymers and UV additives

Key inputs like HDPE resins, UV stabilizers and pigments are supplied by a relatively concentrated group of chemical majors; top 5 resin producers held roughly 40% of global HDPE capacity in 2024, tightening leverage. This concentration raises switching costs and limits Gale Pacific’s bargaining latitude. Long-term contracts and dual-sourcing reduce risk but may not fully offset specialty-additive scarcity. Supplier qualification for performance and compliance further entrenches these relationships.

Commodity price volatility and pass-through

Resin and energy price swings (Brent ~85 USD/bbl in 2024) directly inflate Gale Pacific’s fabric costs, with polymer feedstock volatility up markedly versus 2023; weak pass-through clauses would force margin compression and raise supplier leverage. Hedging and extra inventory can blunt spikes but add carrying costs and capital strain. Suppliers may time increases or add surcharges in tight markets, amplifying short-term pricing power.

Specialized machinery and tooling

Knitting, weaving, coating and extrusion lines require specialized OEM parts and service, concentrating supply for key components. Dependence on a few machinery vendors creates hold-up risks during maintenance or upgrades. Lead times for tooling and spares, often up to 24 weeks, elevate supplier power during outages. Tight SLAs and strengthened in-house maintenance capabilities help rebalance that power.

Sustainability and compliance inputs

Sustainability and compliance inputs shrink Gale Pacific’s qualified supplier pool as 2024 demand for recycled content and low‑VOC coatings rises, letting certified suppliers command price premiums or allocation priority and increasing supplier leverage.

Higher qualification costs and extended testing cycles elevate switching friction and supplier influence, pressuring margins and lead times.

- 2024 trend: certified materials command premiums; longer approval cycles raise sourcing costs

- Effect: fewer suppliers, higher switching friction, stronger supplier bargaining power

Logistics and freight constraints

Supply-side freight leverage rose as global liner fleet reached about 27.9m TEU in 2024 with capacity up ~3.5% year-on-year (Alphaliner), meaning port congestion and elevated container rates amplify supplier bargaining power and allow carriers to pass costs via INCOTERMS.

Nearshoring and diversified lanes lower exposure but demand planning and capital; reliability premiums often spike in peak seasons and may be unavoidable for timely supply to Gale Pacific.

- Global fleet 2024: ~27.9m TEU, +3.5% YoY

- Freight terms (INCOTERMS) enable cost/delivery pass-through

- Nearshoring reduces risk but increases capex/lead-time

- Peak-season reliability premiums common

Supply risk: Top-5 HDPE ~40%, Brent ~85 USD/bbl

Supplier concentration (top‑5 HDPE ~40% global capacity in 2024), resin/feedstock price volatility (Brent ~85 USD/bbl) and scarce certified inputs raise switching costs and margin risk; long lead times (spares/tooling up to 24 weeks) and carrier leverage (global fleet ~27.9m TEU, +3.5% YoY) amplify supplier power despite nearshoring and hedging mitigants.

| Metric | 2024 value | Impact |

|---|---|---|

| Top‑5 HDPE share | ~40% | High concentration |

| Brent | ~85 USD/bbl | Cost pass‑through risk |

| Global fleet | 27.9m TEU (+3.5%) | Freight leverage |

| Lead times | Up to 24 wks | Hold‑up risk |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Gale Pacific; evaluates supplier and buyer power, substitutes, rivalry, and barriers to entry while identifying disruptive threats and strategic levers to protect profitability and market share.

A one-sheet Porter's Five Forces for Gale Pacific—quickly reveal competitive pressures and strategic levers to alleviate decision paralysis. Customizable scores and an instant radar chart make scenario updates simple and slide-ready for boardrooms or investor decks.

Customers Bargaining Power

Large retailers and distributors

Big-box chains, DIY retailers and wholesalers negotiate steep discounts and terms, with the top 3 customers often representing over 20% of supplier sales; private-label deals and shelf allocation magnify buyer leverage. Vendor scorecards and chargebacks (commonly 1–5% of invoice value) force concessions, and losing a single key account can cut plant utilization by roughly 15–30%.

Professional specifiers and project buyers

Architects, builders and facility managers often dictate brand choice via specs, with 2024 surveys showing about 70% of commercial projects being spec-driven; they demand proven UV performance, certifications and 10-year-plus warranties, enabling direct price comparisons. Project-based procurement increases bidding and discounting pressure, with tender-driven projects seeing average bid discounts of 5–12% in 2024. Late-stage value-engineering commonly substitutes lower grades to cut costs.

Switching costs and product comparability

For commoditized shade cloth and screens perceived switching costs are low, and with comparable performance claims buyers often select on price; the global shade cloth market was estimated at about USD 1.1 billion in 2024, underscoring price sensitivity. Proprietary fabric technologies and branded accessories increase stickiness through system integration and can justify 10–30% price premiums. Robust after-sales support and warranties (multi-year coverage) further reduce churn.

Information transparency and e-commerce

Online marketplaces expose prices, reviews and alternatives, empowering buyers and contributing to global e-commerce reaching 22.3% of retail sales in 2024 (Statista). Direct-to-consumer channels compress margins when price parity is expected, while high-quality content and strong brand reputation still justify premiums. Dynamic pricing across channels requires careful governance to avoid channel conflict and margin erosion.

- Price transparency: comparison-enabled shopping

- D2C impact: margin compression risk

- Brand/content: premium justification

- Dynamic pricing: need for channel rules

Demand cyclicality and seasonality

Seasonal peaks let buyers time purchases for discounts or leverage forecast uncertainty, while weather-driven demand shocks can force Gale Pacific into excess inventory markdowns. Pre-season commitments and vendor-managed inventory reduce buyer bargaining but shift working capital and inventory risk back to Gale Pacific. Flexible production scheduling and rapid fulfilment help sustain service levels during volatile demand.

- Buyers time purchases for discounts

- Weather shocks cause markdowns

- Pre-season/VMI shifts capital to Gale

- Flexible scheduling sustains service

Concentration, chargebacks and e-commerce pressure margins; proprietary tech can command premiums

Buyers hold high leverage: top 3 customers >20% of sales, chargebacks 1–5% of invoices and losing one account can cut utilization 15–30%. Spec-driven procurement (≈70% commercial projects in 2024) and price-focused commoditized products compress margins, while proprietary tech and warranties can command 10–30% premiums. E-commerce exposure (22.3% of retail sales in 2024) increases price transparency and D2C margin pressure.

| Metric | 2024 value | Impact |

|---|---|---|

| Top-3 customer share | >20% | Concentration risk |

| Chargebacks | 1–5% invoice | Profit erosion |

| Spec-driven projects | ≈70% | Procurement control |

| Market size | USD 1.1B | Price sensitivity |

| E-commerce | 22.3% | Transparency |

Same Document Delivered

Gale Pacific Porter's Five Forces Analysis

This preview shows the exact Gale Pacific Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted and ready to use. No placeholders, mockups, or samples. You'll get instant access to this identical, professionally prepared file upon payment.