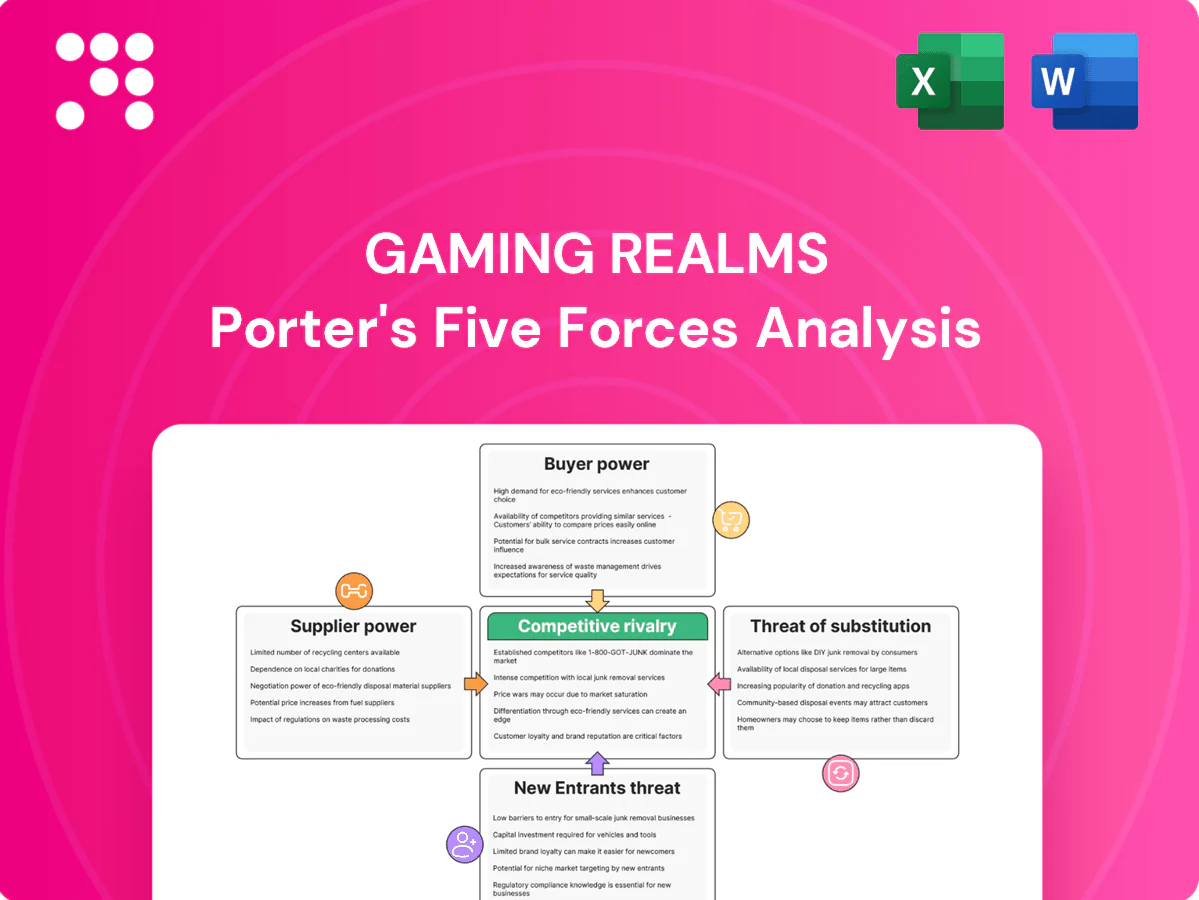

Gaming Realms Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Gaming Realms faces intense platform and distributor dependence, rising substitute entertainment, and moderate barriers to entry—this snapshot highlights key competitive pressures and strategic levers. For investor-grade depth, the full Porter's Five Forces Analysis quantifies each force, maps threats and opportunities, and outlines tactical responses. Unlock the complete report to translate these dynamics into actionable strategy and informed investment decisions.

Suppliers Bargaining Power

Key tech and engine vendors

Gaming Realms depends on two dominant engine vendors (Unity, Unreal), middleware, RNG/cert labs and cloud/CDN partners; major cloud providers held ~31.8% (AWS), 23.8% (Azure) and 10.6% (GCP) of global IaaS in 2024 (Canalys), concentrating supplier influence. These vendors can affect timelines and costs via tooling updates or certification queues. Switching is feasible but costly due to tech debt and re‑certification needs. Net supplier power is moderate: alternatives exist but lock‑in remains non‑trivial.

Branded IP licensors

High-profile brands used within Slingo variants can command premium royalties and restrictive terms, giving licensors intermittent leverage; scarcity of top-tier IP further concentrates bargaining power among a few owners. Gaming Realms’ ownership of the Slingo trademark and extensive proprietary catalogue reduces persistent dependence on external IP. Net effect: episodic high supplier power when marquee IP is sought, but limited for core product lines.

Distribution aggregators

Content aggregators and RGS partners control critical operator access for Gaming Realms, setting technical and commercial requirements that can dictate revenue share and certification timelines in 2024.

Their gatekeeping and roadmap priorities can delay launches by months, making go-to-market timing dependent on aggregator pipelines.

Multi-aggregator strategies reduce single-supplier risk but increase integration overhead and maintenance; supplier power stays meaningful where exclusive pipes or priority placements exist.

Payment/fraud and data tools

Anti-fraud, analytics and payments tooling materially shape player experience and compliance; vendor certification and PCI/ISO pedigrees allow some pricing power, while a crowded market of 1,000+ payment/fraud providers in 2024 keeps supplier leverage moderate. Switching carries real data-loss and operational disruption risks, elevating negotiation friction despite competitive pressures.

- Vendor differentiation: certification-driven pricing power

- Market density: 1,000+ providers in 2024 limits dominance

- Switching risk: data loss and downtime

Creative and math modeling talent

Specialist game designers, mathematicians and producers are scarce relative to demand, increasing supplier power. Talent mobility raises wage pressure and timeline risk; the global games market exceeded $200bn in 2024, intensifying competition for skills. Strong IP and culture improve retention and reduce contractor-like supplier power, leaving overall bargaining power moderate-to-high in tight labor markets.

- Scarcity: high demand for specialist roles

- Pressure: mobility → higher wages, schedule risk

- Mitigation: strong IP/culture lowers contractor leverage

Moderate supplier power: cloud concentration, engine risk; payment diversity caps leverage

Supplier power for Gaming Realms is moderate: cloud/middleware concentration (AWS 31.8%, Azure 23.8%, GCP 10.6% IaaS 2024) and engine vendors drive cost/timing risk, while alternatives exist but switching requires re‑certification. Premium IP licensors exert episodic leverage; Gaming Realms’ own Slingo IP limits dependence. Payments/fraud market (>1,000 providers 2024) tempers vendor dominance but switching risks persist.

| Category | 2024 Metric |

|---|---|

| Cloud IaaS share | AWS 31.8% / Azure 23.8% / GCP 10.6% |

| Payments/fraud | 1,000+ providers |

| Global games market | >$200bn |

What is included in the product

Tailored exclusively for Gaming Realms, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its pricing power and profitability in the online gaming market.

A concise one-sheet Porter’s Five Forces for Gaming Realms that pinpoints competitive pressures and strategic levers for rapid decisions—customizable metrics and radar visuals make it boardroom-ready.

Customers Bargaining Power

Concentrated casino operators

Concentrated casino operators (top five controlling ~60% of distribution) dictate placement and promo budgets, forcing Gaming Realms into aggressive rev-share talks and risking delisting; Gaming Realms reported 2023 revenue of £35.9m, making dependence on key accounts material. Must-have titles reduce but do not eliminate leverage, with operators commonly demanding volume discounts and short-term exclusives to extract concessions.

Aggregator-driven purchasing

Aggregator-driven purchasing lets operators swap Gaming Realms titles with minimal friction, amplifying price transparency and customer bargaining power. While aggregators expand Gaming Realms reach across multiple platforms, they compress margins and compete for limited release slots. Bundled aggregator deals often dilute per-title economics and increase pressure on headline revenue contribution.

End-user low switching costs

Players can move between games instantly driven by novelty and perception of RTP, which for online slots typically ranges 92–97%. Low loyalty outside flagship titles limits pricing power, with engagement concentrated in top-performing releases. Slingo, created in 1994, gives brand recognition that softens but does not eliminate churn. Continuous content refresh is required to retain users.

Demand for localization and compliance

Operators demand jurisdictional certifications, language/currency support and robust responsible-gaming tools, shifting compliance costs onto suppliers; in 2024 more than 30 regulated jurisdictions raise these standards and strengthen operator leverage. Slow certification timelines frequently determine pricing, SLAs and contract terms.

- Compliance costs shift to supplier

- 30+ regulated jurisdictions (2024)

- Certification speed alters contract terms

Data-driven performance accountability

Operators benchmark titles on KPIs like GGR, retention and session length, delisting underperformers within weeks which concentrates bargaining power with buyers who demand lower rates and richer promos; transparency in telemetry makes rate negotiation more data-driven. Hit concentration raises dependence on a few SKUs, amplifying buyer leverage over pricing and promotional terms.

- GGR-driven placement

- Quick delisting of losers

- High hit concentration

- Promos/rate pressure

Top-5 ~60% control forces rev-share cuts; 30+ regs up costs

Concentrated operators (~60% distribution by top five) and aggregator deals force Gaming Realms into aggressive rev-share and promo concessions; 2023 revenue £35.9m makes key-account dependence material. Player churn (RTP 92–97%) and fast delisting raise buyer leverage, while 30+ regulated jurisdictions (2024) shift compliance costs to suppliers.

| Metric | Value |

|---|---|

| 2023 revenue | £35.9m |

| Top-5 operator share | ~60% |

| Regulated jurisdictions (2024) | 30+ |

| Typical RTP | 92–97% |

What You See Is What You Get

Gaming Realms Porter's Five Forces Analysis

This preview shows the exact Gaming Realms Porter's Five Forces Analysis you'll receive after purchase—fully formatted, comprehensive and ready to use. No placeholders or excerpts: the file you see is the file you'll download. Instant access upon payment, professional and complete.

Don't Miss the Bigger Picture

Gaming Realms faces intense platform and distributor dependence, rising substitute entertainment, and moderate barriers to entry—this snapshot highlights key competitive pressures and strategic levers. For investor-grade depth, the full Porter's Five Forces Analysis quantifies each force, maps threats and opportunities, and outlines tactical responses. Unlock the complete report to translate these dynamics into actionable strategy and informed investment decisions.

Suppliers Bargaining Power

Key tech and engine vendors

Gaming Realms depends on two dominant engine vendors (Unity, Unreal), middleware, RNG/cert labs and cloud/CDN partners; major cloud providers held ~31.8% (AWS), 23.8% (Azure) and 10.6% (GCP) of global IaaS in 2024 (Canalys), concentrating supplier influence. These vendors can affect timelines and costs via tooling updates or certification queues. Switching is feasible but costly due to tech debt and re‑certification needs. Net supplier power is moderate: alternatives exist but lock‑in remains non‑trivial.

Branded IP licensors

High-profile brands used within Slingo variants can command premium royalties and restrictive terms, giving licensors intermittent leverage; scarcity of top-tier IP further concentrates bargaining power among a few owners. Gaming Realms’ ownership of the Slingo trademark and extensive proprietary catalogue reduces persistent dependence on external IP. Net effect: episodic high supplier power when marquee IP is sought, but limited for core product lines.

Distribution aggregators

Content aggregators and RGS partners control critical operator access for Gaming Realms, setting technical and commercial requirements that can dictate revenue share and certification timelines in 2024.

Their gatekeeping and roadmap priorities can delay launches by months, making go-to-market timing dependent on aggregator pipelines.

Multi-aggregator strategies reduce single-supplier risk but increase integration overhead and maintenance; supplier power stays meaningful where exclusive pipes or priority placements exist.

Payment/fraud and data tools

Anti-fraud, analytics and payments tooling materially shape player experience and compliance; vendor certification and PCI/ISO pedigrees allow some pricing power, while a crowded market of 1,000+ payment/fraud providers in 2024 keeps supplier leverage moderate. Switching carries real data-loss and operational disruption risks, elevating negotiation friction despite competitive pressures.

- Vendor differentiation: certification-driven pricing power

- Market density: 1,000+ providers in 2024 limits dominance

- Switching risk: data loss and downtime

Creative and math modeling talent

Specialist game designers, mathematicians and producers are scarce relative to demand, increasing supplier power. Talent mobility raises wage pressure and timeline risk; the global games market exceeded $200bn in 2024, intensifying competition for skills. Strong IP and culture improve retention and reduce contractor-like supplier power, leaving overall bargaining power moderate-to-high in tight labor markets.

- Scarcity: high demand for specialist roles

- Pressure: mobility → higher wages, schedule risk

- Mitigation: strong IP/culture lowers contractor leverage

Moderate supplier power: cloud concentration, engine risk; payment diversity caps leverage

Supplier power for Gaming Realms is moderate: cloud/middleware concentration (AWS 31.8%, Azure 23.8%, GCP 10.6% IaaS 2024) and engine vendors drive cost/timing risk, while alternatives exist but switching requires re‑certification. Premium IP licensors exert episodic leverage; Gaming Realms’ own Slingo IP limits dependence. Payments/fraud market (>1,000 providers 2024) tempers vendor dominance but switching risks persist.

| Category | 2024 Metric |

|---|---|

| Cloud IaaS share | AWS 31.8% / Azure 23.8% / GCP 10.6% |

| Payments/fraud | 1,000+ providers |

| Global games market | >$200bn |

What is included in the product

Tailored exclusively for Gaming Realms, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its pricing power and profitability in the online gaming market.

A concise one-sheet Porter’s Five Forces for Gaming Realms that pinpoints competitive pressures and strategic levers for rapid decisions—customizable metrics and radar visuals make it boardroom-ready.

Customers Bargaining Power

Concentrated casino operators

Concentrated casino operators (top five controlling ~60% of distribution) dictate placement and promo budgets, forcing Gaming Realms into aggressive rev-share talks and risking delisting; Gaming Realms reported 2023 revenue of £35.9m, making dependence on key accounts material. Must-have titles reduce but do not eliminate leverage, with operators commonly demanding volume discounts and short-term exclusives to extract concessions.

Aggregator-driven purchasing

Aggregator-driven purchasing lets operators swap Gaming Realms titles with minimal friction, amplifying price transparency and customer bargaining power. While aggregators expand Gaming Realms reach across multiple platforms, they compress margins and compete for limited release slots. Bundled aggregator deals often dilute per-title economics and increase pressure on headline revenue contribution.

End-user low switching costs

Players can move between games instantly driven by novelty and perception of RTP, which for online slots typically ranges 92–97%. Low loyalty outside flagship titles limits pricing power, with engagement concentrated in top-performing releases. Slingo, created in 1994, gives brand recognition that softens but does not eliminate churn. Continuous content refresh is required to retain users.

Demand for localization and compliance

Operators demand jurisdictional certifications, language/currency support and robust responsible-gaming tools, shifting compliance costs onto suppliers; in 2024 more than 30 regulated jurisdictions raise these standards and strengthen operator leverage. Slow certification timelines frequently determine pricing, SLAs and contract terms.

- Compliance costs shift to supplier

- 30+ regulated jurisdictions (2024)

- Certification speed alters contract terms

Data-driven performance accountability

Operators benchmark titles on KPIs like GGR, retention and session length, delisting underperformers within weeks which concentrates bargaining power with buyers who demand lower rates and richer promos; transparency in telemetry makes rate negotiation more data-driven. Hit concentration raises dependence on a few SKUs, amplifying buyer leverage over pricing and promotional terms.

- GGR-driven placement

- Quick delisting of losers

- High hit concentration

- Promos/rate pressure

Top-5 ~60% control forces rev-share cuts; 30+ regs up costs

Concentrated operators (~60% distribution by top five) and aggregator deals force Gaming Realms into aggressive rev-share and promo concessions; 2023 revenue £35.9m makes key-account dependence material. Player churn (RTP 92–97%) and fast delisting raise buyer leverage, while 30+ regulated jurisdictions (2024) shift compliance costs to suppliers.

| Metric | Value |

|---|---|

| 2023 revenue | £35.9m |

| Top-5 operator share | ~60% |

| Regulated jurisdictions (2024) | 30+ |

| Typical RTP | 92–97% |

What You See Is What You Get

Gaming Realms Porter's Five Forces Analysis

This preview shows the exact Gaming Realms Porter's Five Forces Analysis you'll receive after purchase—fully formatted, comprehensive and ready to use. No placeholders or excerpts: the file you see is the file you'll download. Instant access upon payment, professional and complete.

Description

Don't Miss the Bigger Picture

Gaming Realms faces intense platform and distributor dependence, rising substitute entertainment, and moderate barriers to entry—this snapshot highlights key competitive pressures and strategic levers. For investor-grade depth, the full Porter's Five Forces Analysis quantifies each force, maps threats and opportunities, and outlines tactical responses. Unlock the complete report to translate these dynamics into actionable strategy and informed investment decisions.

Suppliers Bargaining Power

Key tech and engine vendors

Gaming Realms depends on two dominant engine vendors (Unity, Unreal), middleware, RNG/cert labs and cloud/CDN partners; major cloud providers held ~31.8% (AWS), 23.8% (Azure) and 10.6% (GCP) of global IaaS in 2024 (Canalys), concentrating supplier influence. These vendors can affect timelines and costs via tooling updates or certification queues. Switching is feasible but costly due to tech debt and re‑certification needs. Net supplier power is moderate: alternatives exist but lock‑in remains non‑trivial.

Branded IP licensors

High-profile brands used within Slingo variants can command premium royalties and restrictive terms, giving licensors intermittent leverage; scarcity of top-tier IP further concentrates bargaining power among a few owners. Gaming Realms’ ownership of the Slingo trademark and extensive proprietary catalogue reduces persistent dependence on external IP. Net effect: episodic high supplier power when marquee IP is sought, but limited for core product lines.

Distribution aggregators

Content aggregators and RGS partners control critical operator access for Gaming Realms, setting technical and commercial requirements that can dictate revenue share and certification timelines in 2024.

Their gatekeeping and roadmap priorities can delay launches by months, making go-to-market timing dependent on aggregator pipelines.

Multi-aggregator strategies reduce single-supplier risk but increase integration overhead and maintenance; supplier power stays meaningful where exclusive pipes or priority placements exist.

Payment/fraud and data tools

Anti-fraud, analytics and payments tooling materially shape player experience and compliance; vendor certification and PCI/ISO pedigrees allow some pricing power, while a crowded market of 1,000+ payment/fraud providers in 2024 keeps supplier leverage moderate. Switching carries real data-loss and operational disruption risks, elevating negotiation friction despite competitive pressures.

- Vendor differentiation: certification-driven pricing power

- Market density: 1,000+ providers in 2024 limits dominance

- Switching risk: data loss and downtime

Creative and math modeling talent

Specialist game designers, mathematicians and producers are scarce relative to demand, increasing supplier power. Talent mobility raises wage pressure and timeline risk; the global games market exceeded $200bn in 2024, intensifying competition for skills. Strong IP and culture improve retention and reduce contractor-like supplier power, leaving overall bargaining power moderate-to-high in tight labor markets.

- Scarcity: high demand for specialist roles

- Pressure: mobility → higher wages, schedule risk

- Mitigation: strong IP/culture lowers contractor leverage

Moderate supplier power: cloud concentration, engine risk; payment diversity caps leverage

Supplier power for Gaming Realms is moderate: cloud/middleware concentration (AWS 31.8%, Azure 23.8%, GCP 10.6% IaaS 2024) and engine vendors drive cost/timing risk, while alternatives exist but switching requires re‑certification. Premium IP licensors exert episodic leverage; Gaming Realms’ own Slingo IP limits dependence. Payments/fraud market (>1,000 providers 2024) tempers vendor dominance but switching risks persist.

| Category | 2024 Metric |

|---|---|

| Cloud IaaS share | AWS 31.8% / Azure 23.8% / GCP 10.6% |

| Payments/fraud | 1,000+ providers |

| Global games market | >$200bn |

What is included in the product

Tailored exclusively for Gaming Realms, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its pricing power and profitability in the online gaming market.

A concise one-sheet Porter’s Five Forces for Gaming Realms that pinpoints competitive pressures and strategic levers for rapid decisions—customizable metrics and radar visuals make it boardroom-ready.

Customers Bargaining Power

Concentrated casino operators

Concentrated casino operators (top five controlling ~60% of distribution) dictate placement and promo budgets, forcing Gaming Realms into aggressive rev-share talks and risking delisting; Gaming Realms reported 2023 revenue of £35.9m, making dependence on key accounts material. Must-have titles reduce but do not eliminate leverage, with operators commonly demanding volume discounts and short-term exclusives to extract concessions.

Aggregator-driven purchasing

Aggregator-driven purchasing lets operators swap Gaming Realms titles with minimal friction, amplifying price transparency and customer bargaining power. While aggregators expand Gaming Realms reach across multiple platforms, they compress margins and compete for limited release slots. Bundled aggregator deals often dilute per-title economics and increase pressure on headline revenue contribution.

End-user low switching costs

Players can move between games instantly driven by novelty and perception of RTP, which for online slots typically ranges 92–97%. Low loyalty outside flagship titles limits pricing power, with engagement concentrated in top-performing releases. Slingo, created in 1994, gives brand recognition that softens but does not eliminate churn. Continuous content refresh is required to retain users.

Demand for localization and compliance

Operators demand jurisdictional certifications, language/currency support and robust responsible-gaming tools, shifting compliance costs onto suppliers; in 2024 more than 30 regulated jurisdictions raise these standards and strengthen operator leverage. Slow certification timelines frequently determine pricing, SLAs and contract terms.

- Compliance costs shift to supplier

- 30+ regulated jurisdictions (2024)

- Certification speed alters contract terms

Data-driven performance accountability

Operators benchmark titles on KPIs like GGR, retention and session length, delisting underperformers within weeks which concentrates bargaining power with buyers who demand lower rates and richer promos; transparency in telemetry makes rate negotiation more data-driven. Hit concentration raises dependence on a few SKUs, amplifying buyer leverage over pricing and promotional terms.

- GGR-driven placement

- Quick delisting of losers

- High hit concentration

- Promos/rate pressure

Top-5 ~60% control forces rev-share cuts; 30+ regs up costs

Concentrated operators (~60% distribution by top five) and aggregator deals force Gaming Realms into aggressive rev-share and promo concessions; 2023 revenue £35.9m makes key-account dependence material. Player churn (RTP 92–97%) and fast delisting raise buyer leverage, while 30+ regulated jurisdictions (2024) shift compliance costs to suppliers.

| Metric | Value |

|---|---|

| 2023 revenue | £35.9m |

| Top-5 operator share | ~60% |

| Regulated jurisdictions (2024) | 30+ |

| Typical RTP | 92–97% |

What You See Is What You Get

Gaming Realms Porter's Five Forces Analysis

This preview shows the exact Gaming Realms Porter's Five Forces Analysis you'll receive after purchase—fully formatted, comprehensive and ready to use. No placeholders or excerpts: the file you see is the file you'll download. Instant access upon payment, professional and complete.