Cubic Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

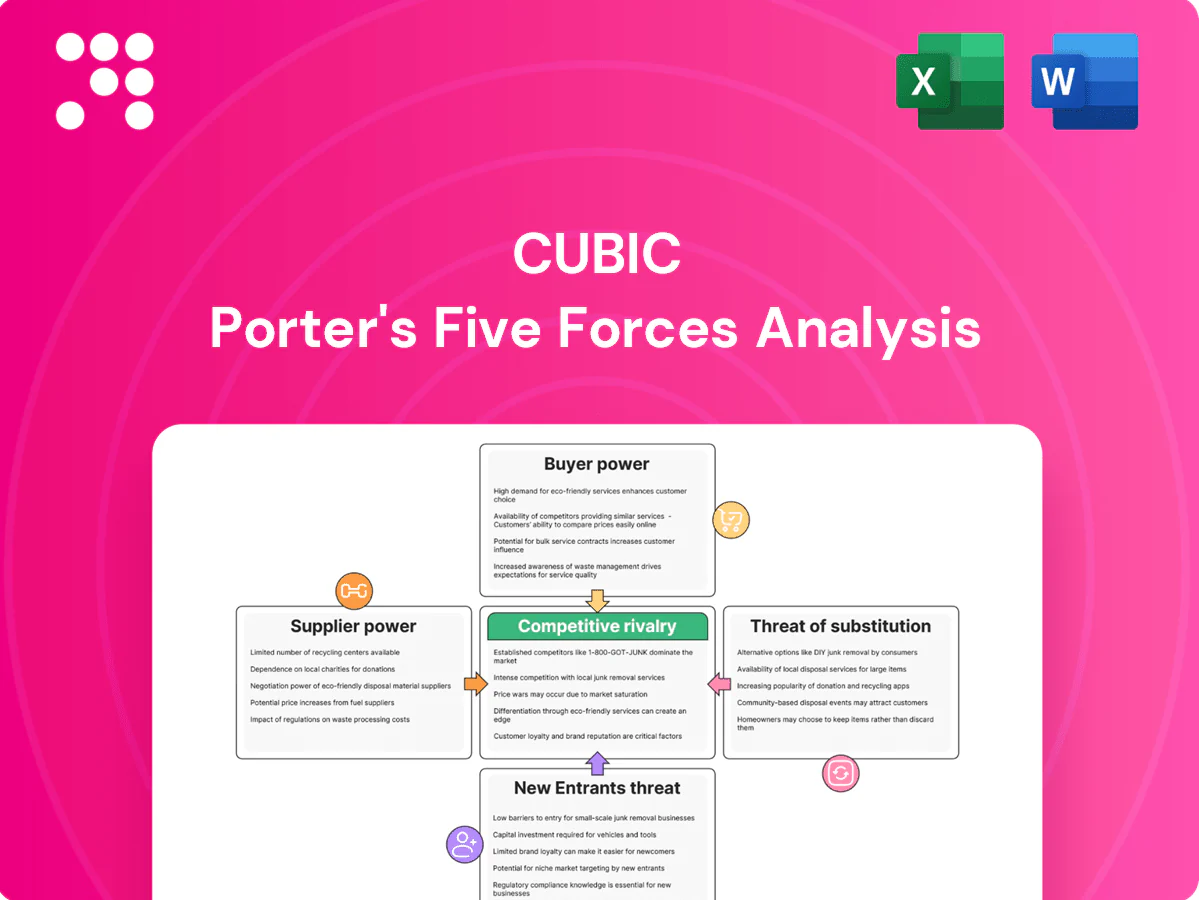

Cubic’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, barriers to entry, and substitute pressures shaping its defense and transport businesses. The analysis surfaces strategic risks and growth levers investors and managers must know. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized optics and detectors

NDIR modules depend on niche IR sources, thermopiles/pyroelectrics and narrow-band filters supplied by a concentrated set of specialists such as Hamamatsu and Excelitas, giving suppliers pricing and technical leverage. Qualification cycles are long—commonly exceeding 12 months in 2024—so switching suppliers is costly and risky. Multi-sourcing reduces single-supplier risk but can dilute performance consistency and complicate calibration across batches.

Precision manufacturing equipment

Calibration benches, alignment tooling, and environmental test systems are concentrated among a few vendors, giving suppliers outsized pricing power and lead times commonly of 6–12 months in 2024. Long waits can bottleneck expansion and increase cost of delay. Preventive buys or vendor-managed inventory mitigate risk but can lock up 3–9% of working capital. Strategic partnerships typically secure roadmaps and priority allocations.

Materials and calibration gases

Stable calibration gases (typically 99.999% purity) and specialty materials like optical coatings are critical to accuracy and yield, with the top 5 suppliers controlling roughly 60% of the market in 2024, limiting alternatives. Purity/stability specs and 8–12 week lead times constrain switching, while indexation to commodity prices has driven input cost swings of 10–20% recently. Long-term contracts with buffer stock cut volatility exposure but incur 2–5% annual carrying costs.

Geopolitics and compliance

Export controls tightened by the US and EU in 2024 constrain detector arrays and IR emitter exports, lengthening lead times and raising freight costs; compliance with RoHS and REACH further narrows suppliers to certified providers, increasing dependency. Regionalization in 2024 drove duplication of capacity and a reported 62% of tech manufacturers shifting production closer to end markets, raising unit costs but lowering single-point failure risk. Diversified geographies reduce supplier concentration and outage exposure.

- Export controls: 2024 tightening raises lead times

- Compliance: RoHS/REACH narrows certified suppliers

- Regionalization: ~62% shifting production (2024)

- Mitigation: geographic diversification lowers single-point failure risk

Potential for backward integration

Vertical integration into optics or detector packaging is technically feasible but capital intensive; 2024 industry reports note CapEx typically runs from tens to hundreds of millions for advanced packaging and cleanroom tooling, while steep learning curves and yield risks can erode expected margin gains.

- Selective integration (filter assembly) reduces supplier power with lower CapEx and faster ROI

- JV/partnership models capture value without full CapEx burden

- Yield ramp delays commonly drive 12–24 month payback uncertainty

Supplier leverage: concentrated IR supply, export controls, long qualification 12+ months

Suppliers hold high leverage due to concentrated IR source, detector and calibration-equipment markets, long qualification cycles (12+ months in 2024) and tight export/compliance constraints, driving lead times and input cost volatility. Multi-sourcing and selective vertical integration reduce risk but raise CapEx and working capital needs.

| Metric | 2024 |

|---|---|

| Qualification cycle | 12+ months |

| Top-5 supplier share (gases/coatings) | ~60% |

| Regionalization share | 62% |

| CapEx (packaging) | tens–hundreds $M |

What is included in the product

Concise Porter's Five Forces analysis tailored for Cubic, revealing competitive intensity, buyer/supplier power, threat of substitutes and new entrants, plus strategic implications and emerging disruptors affecting its pricing, margins, and market position.

Cubic Porter's Five Forces gives a single-sheet, customizable view with pressure sliders and an instant spider chart—clean, no-code layout you can drop into decks or dashboards for rapid, board-ready strategic decisions.

Customers Bargaining Power

Large OEMs and tenders

Large OEMs and public tenders in HVAC and safety, with the global HVAC market ~USD 200B in 2024, buy at scale and run aggressive competitive tenders that compress supplier margins. Multi-year framework agreements (commonly 3–5 years) lock pricing and service levels, reducing short-term pricing flexibility. Losing a major bid can materially swing utilization and revenue, while value-added services and differentiated specifications often secure 5–15% price premiums and protect against commoditization.

Switching and qualification costs

System integration, field certification, and firmware tuning create switching friction for Cubic because design-in plus safety and compliance testing typically add 3–9 months and $50k–$500k in 2024, making mid-cycle supplier changes painful. Once a component is designed-in, buyer leverage falls as replacement triggers revalidation and recall risk. Pre-compliance documentation and multi-year support agreements further increase customer stickiness and reduce churn.

Price sensitivity in HVAC

Price sensitivity in HVAC is acute as the IAQ market, valued at about USD 15.7 billion in 2023, drives high-volume CO2 sensing procurement and amplifies buyer bargaining power; industry buyers report single-digit ASP cuts often sway design wins, so total cost of ownership arguments—power draw, stability, recalibration intervals—are pivotal, and bundled analytics can shift purchasing from unit price to lifecycle value.

Performance-driven niches

Performance-driven niches see high customer bargaining power because industrial safety and environmental monitoring buyers prioritize accuracy, low drift, and robustness; in 2024 surveys buyers paid 15–25% premiums for certified reliability and traceable calibration. Custom firmware and protocols increase switching costs and lock-in, while service-level guarantees and documented calibration reduce incident risk and justify higher margins.

- Accuracy priority: 15–25% premium (2024)

- Lock-in: custom firmware/protocols

- Trust builders: SLAs + traceable calibration

Information transparency

- Benchmarks/reviews: easier comparison

- Standards (Modbus, UART, I2C): multi-sourcing

- Datasheets: reduced differentiation

- App notes: steer to proprietary advantage

HVAC tenders squeeze margins; IAQ growth and reliability premiums bolster supplier leverage

Large OEMs and public tenders in HVAC (global market ~USD 200B in 2024) create strong price pressure via multi-year competitive bids. Design-in plus compliance typically add 3–9 months and $50k–$500k (2024), raising switching costs and reducing buyer leverage. IAQ market (~USD 15.7B in 2023) and certified reliability premiums (15–25% in 2024) restore some supplier power.

| Metric | Value | Impact |

|---|---|---|

| HVAC market | ~USD 200B (2024) | High buyer scale |

| IAQ market | ~USD 15.7B (2023) | Volume purchases |

| Design-in cost/time | $50k–$500k; 3–9m (2024) | High switching cost |

| Reliability premium | 15–25% (2024) | Supplier leverage |

What You See Is What You Get

Cubic Porter's Five Forces Analysis

This preview shows the exact Cubic Porter’s Five Forces Analysis you’ll receive—no mockups or placeholders. The document displayed is fully formatted, professionally written, and ready for immediate download after purchase. You’re looking at the final deliverable, unchanged and ready to use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cubic’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, barriers to entry, and substitute pressures shaping its defense and transport businesses. The analysis surfaces strategic risks and growth levers investors and managers must know. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized optics and detectors

NDIR modules depend on niche IR sources, thermopiles/pyroelectrics and narrow-band filters supplied by a concentrated set of specialists such as Hamamatsu and Excelitas, giving suppliers pricing and technical leverage. Qualification cycles are long—commonly exceeding 12 months in 2024—so switching suppliers is costly and risky. Multi-sourcing reduces single-supplier risk but can dilute performance consistency and complicate calibration across batches.

Precision manufacturing equipment

Calibration benches, alignment tooling, and environmental test systems are concentrated among a few vendors, giving suppliers outsized pricing power and lead times commonly of 6–12 months in 2024. Long waits can bottleneck expansion and increase cost of delay. Preventive buys or vendor-managed inventory mitigate risk but can lock up 3–9% of working capital. Strategic partnerships typically secure roadmaps and priority allocations.

Materials and calibration gases

Stable calibration gases (typically 99.999% purity) and specialty materials like optical coatings are critical to accuracy and yield, with the top 5 suppliers controlling roughly 60% of the market in 2024, limiting alternatives. Purity/stability specs and 8–12 week lead times constrain switching, while indexation to commodity prices has driven input cost swings of 10–20% recently. Long-term contracts with buffer stock cut volatility exposure but incur 2–5% annual carrying costs.

Geopolitics and compliance

Export controls tightened by the US and EU in 2024 constrain detector arrays and IR emitter exports, lengthening lead times and raising freight costs; compliance with RoHS and REACH further narrows suppliers to certified providers, increasing dependency. Regionalization in 2024 drove duplication of capacity and a reported 62% of tech manufacturers shifting production closer to end markets, raising unit costs but lowering single-point failure risk. Diversified geographies reduce supplier concentration and outage exposure.

- Export controls: 2024 tightening raises lead times

- Compliance: RoHS/REACH narrows certified suppliers

- Regionalization: ~62% shifting production (2024)

- Mitigation: geographic diversification lowers single-point failure risk

Potential for backward integration

Vertical integration into optics or detector packaging is technically feasible but capital intensive; 2024 industry reports note CapEx typically runs from tens to hundreds of millions for advanced packaging and cleanroom tooling, while steep learning curves and yield risks can erode expected margin gains.

- Selective integration (filter assembly) reduces supplier power with lower CapEx and faster ROI

- JV/partnership models capture value without full CapEx burden

- Yield ramp delays commonly drive 12–24 month payback uncertainty

Supplier leverage: concentrated IR supply, export controls, long qualification 12+ months

Suppliers hold high leverage due to concentrated IR source, detector and calibration-equipment markets, long qualification cycles (12+ months in 2024) and tight export/compliance constraints, driving lead times and input cost volatility. Multi-sourcing and selective vertical integration reduce risk but raise CapEx and working capital needs.

| Metric | 2024 |

|---|---|

| Qualification cycle | 12+ months |

| Top-5 supplier share (gases/coatings) | ~60% |

| Regionalization share | 62% |

| CapEx (packaging) | tens–hundreds $M |

What is included in the product

Concise Porter's Five Forces analysis tailored for Cubic, revealing competitive intensity, buyer/supplier power, threat of substitutes and new entrants, plus strategic implications and emerging disruptors affecting its pricing, margins, and market position.

Cubic Porter's Five Forces gives a single-sheet, customizable view with pressure sliders and an instant spider chart—clean, no-code layout you can drop into decks or dashboards for rapid, board-ready strategic decisions.

Customers Bargaining Power

Large OEMs and tenders

Large OEMs and public tenders in HVAC and safety, with the global HVAC market ~USD 200B in 2024, buy at scale and run aggressive competitive tenders that compress supplier margins. Multi-year framework agreements (commonly 3–5 years) lock pricing and service levels, reducing short-term pricing flexibility. Losing a major bid can materially swing utilization and revenue, while value-added services and differentiated specifications often secure 5–15% price premiums and protect against commoditization.

Switching and qualification costs

System integration, field certification, and firmware tuning create switching friction for Cubic because design-in plus safety and compliance testing typically add 3–9 months and $50k–$500k in 2024, making mid-cycle supplier changes painful. Once a component is designed-in, buyer leverage falls as replacement triggers revalidation and recall risk. Pre-compliance documentation and multi-year support agreements further increase customer stickiness and reduce churn.

Price sensitivity in HVAC

Price sensitivity in HVAC is acute as the IAQ market, valued at about USD 15.7 billion in 2023, drives high-volume CO2 sensing procurement and amplifies buyer bargaining power; industry buyers report single-digit ASP cuts often sway design wins, so total cost of ownership arguments—power draw, stability, recalibration intervals—are pivotal, and bundled analytics can shift purchasing from unit price to lifecycle value.

Performance-driven niches

Performance-driven niches see high customer bargaining power because industrial safety and environmental monitoring buyers prioritize accuracy, low drift, and robustness; in 2024 surveys buyers paid 15–25% premiums for certified reliability and traceable calibration. Custom firmware and protocols increase switching costs and lock-in, while service-level guarantees and documented calibration reduce incident risk and justify higher margins.

- Accuracy priority: 15–25% premium (2024)

- Lock-in: custom firmware/protocols

- Trust builders: SLAs + traceable calibration

Information transparency

- Benchmarks/reviews: easier comparison

- Standards (Modbus, UART, I2C): multi-sourcing

- Datasheets: reduced differentiation

- App notes: steer to proprietary advantage

HVAC tenders squeeze margins; IAQ growth and reliability premiums bolster supplier leverage

Large OEMs and public tenders in HVAC (global market ~USD 200B in 2024) create strong price pressure via multi-year competitive bids. Design-in plus compliance typically add 3–9 months and $50k–$500k (2024), raising switching costs and reducing buyer leverage. IAQ market (~USD 15.7B in 2023) and certified reliability premiums (15–25% in 2024) restore some supplier power.

| Metric | Value | Impact |

|---|---|---|

| HVAC market | ~USD 200B (2024) | High buyer scale |

| IAQ market | ~USD 15.7B (2023) | Volume purchases |

| Design-in cost/time | $50k–$500k; 3–9m (2024) | High switching cost |

| Reliability premium | 15–25% (2024) | Supplier leverage |

What You See Is What You Get

Cubic Porter's Five Forces Analysis

This preview shows the exact Cubic Porter’s Five Forces Analysis you’ll receive—no mockups or placeholders. The document displayed is fully formatted, professionally written, and ready for immediate download after purchase. You’re looking at the final deliverable, unchanged and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cubic’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer leverage, barriers to entry, and substitute pressures shaping its defense and transport businesses. The analysis surfaces strategic risks and growth levers investors and managers must know. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized optics and detectors

NDIR modules depend on niche IR sources, thermopiles/pyroelectrics and narrow-band filters supplied by a concentrated set of specialists such as Hamamatsu and Excelitas, giving suppliers pricing and technical leverage. Qualification cycles are long—commonly exceeding 12 months in 2024—so switching suppliers is costly and risky. Multi-sourcing reduces single-supplier risk but can dilute performance consistency and complicate calibration across batches.

Precision manufacturing equipment

Calibration benches, alignment tooling, and environmental test systems are concentrated among a few vendors, giving suppliers outsized pricing power and lead times commonly of 6–12 months in 2024. Long waits can bottleneck expansion and increase cost of delay. Preventive buys or vendor-managed inventory mitigate risk but can lock up 3–9% of working capital. Strategic partnerships typically secure roadmaps and priority allocations.

Materials and calibration gases

Stable calibration gases (typically 99.999% purity) and specialty materials like optical coatings are critical to accuracy and yield, with the top 5 suppliers controlling roughly 60% of the market in 2024, limiting alternatives. Purity/stability specs and 8–12 week lead times constrain switching, while indexation to commodity prices has driven input cost swings of 10–20% recently. Long-term contracts with buffer stock cut volatility exposure but incur 2–5% annual carrying costs.

Geopolitics and compliance

Export controls tightened by the US and EU in 2024 constrain detector arrays and IR emitter exports, lengthening lead times and raising freight costs; compliance with RoHS and REACH further narrows suppliers to certified providers, increasing dependency. Regionalization in 2024 drove duplication of capacity and a reported 62% of tech manufacturers shifting production closer to end markets, raising unit costs but lowering single-point failure risk. Diversified geographies reduce supplier concentration and outage exposure.

- Export controls: 2024 tightening raises lead times

- Compliance: RoHS/REACH narrows certified suppliers

- Regionalization: ~62% shifting production (2024)

- Mitigation: geographic diversification lowers single-point failure risk

Potential for backward integration

Vertical integration into optics or detector packaging is technically feasible but capital intensive; 2024 industry reports note CapEx typically runs from tens to hundreds of millions for advanced packaging and cleanroom tooling, while steep learning curves and yield risks can erode expected margin gains.

- Selective integration (filter assembly) reduces supplier power with lower CapEx and faster ROI

- JV/partnership models capture value without full CapEx burden

- Yield ramp delays commonly drive 12–24 month payback uncertainty

Supplier leverage: concentrated IR supply, export controls, long qualification 12+ months

Suppliers hold high leverage due to concentrated IR source, detector and calibration-equipment markets, long qualification cycles (12+ months in 2024) and tight export/compliance constraints, driving lead times and input cost volatility. Multi-sourcing and selective vertical integration reduce risk but raise CapEx and working capital needs.

| Metric | 2024 |

|---|---|

| Qualification cycle | 12+ months |

| Top-5 supplier share (gases/coatings) | ~60% |

| Regionalization share | 62% |

| CapEx (packaging) | tens–hundreds $M |

What is included in the product

Concise Porter's Five Forces analysis tailored for Cubic, revealing competitive intensity, buyer/supplier power, threat of substitutes and new entrants, plus strategic implications and emerging disruptors affecting its pricing, margins, and market position.

Cubic Porter's Five Forces gives a single-sheet, customizable view with pressure sliders and an instant spider chart—clean, no-code layout you can drop into decks or dashboards for rapid, board-ready strategic decisions.

Customers Bargaining Power

Large OEMs and tenders

Large OEMs and public tenders in HVAC and safety, with the global HVAC market ~USD 200B in 2024, buy at scale and run aggressive competitive tenders that compress supplier margins. Multi-year framework agreements (commonly 3–5 years) lock pricing and service levels, reducing short-term pricing flexibility. Losing a major bid can materially swing utilization and revenue, while value-added services and differentiated specifications often secure 5–15% price premiums and protect against commoditization.

Switching and qualification costs

System integration, field certification, and firmware tuning create switching friction for Cubic because design-in plus safety and compliance testing typically add 3–9 months and $50k–$500k in 2024, making mid-cycle supplier changes painful. Once a component is designed-in, buyer leverage falls as replacement triggers revalidation and recall risk. Pre-compliance documentation and multi-year support agreements further increase customer stickiness and reduce churn.

Price sensitivity in HVAC

Price sensitivity in HVAC is acute as the IAQ market, valued at about USD 15.7 billion in 2023, drives high-volume CO2 sensing procurement and amplifies buyer bargaining power; industry buyers report single-digit ASP cuts often sway design wins, so total cost of ownership arguments—power draw, stability, recalibration intervals—are pivotal, and bundled analytics can shift purchasing from unit price to lifecycle value.

Performance-driven niches

Performance-driven niches see high customer bargaining power because industrial safety and environmental monitoring buyers prioritize accuracy, low drift, and robustness; in 2024 surveys buyers paid 15–25% premiums for certified reliability and traceable calibration. Custom firmware and protocols increase switching costs and lock-in, while service-level guarantees and documented calibration reduce incident risk and justify higher margins.

- Accuracy priority: 15–25% premium (2024)

- Lock-in: custom firmware/protocols

- Trust builders: SLAs + traceable calibration

Information transparency

- Benchmarks/reviews: easier comparison

- Standards (Modbus, UART, I2C): multi-sourcing

- Datasheets: reduced differentiation

- App notes: steer to proprietary advantage

HVAC tenders squeeze margins; IAQ growth and reliability premiums bolster supplier leverage

Large OEMs and public tenders in HVAC (global market ~USD 200B in 2024) create strong price pressure via multi-year competitive bids. Design-in plus compliance typically add 3–9 months and $50k–$500k (2024), raising switching costs and reducing buyer leverage. IAQ market (~USD 15.7B in 2023) and certified reliability premiums (15–25% in 2024) restore some supplier power.

| Metric | Value | Impact |

|---|---|---|

| HVAC market | ~USD 200B (2024) | High buyer scale |

| IAQ market | ~USD 15.7B (2023) | Volume purchases |

| Design-in cost/time | $50k–$500k; 3–9m (2024) | High switching cost |

| Reliability premium | 15–25% (2024) | Supplier leverage |

What You See Is What You Get

Cubic Porter's Five Forces Analysis

This preview shows the exact Cubic Porter’s Five Forces Analysis you’ll receive—no mockups or placeholders. The document displayed is fully formatted, professionally written, and ready for immediate download after purchase. You’re looking at the final deliverable, unchanged and ready to use.