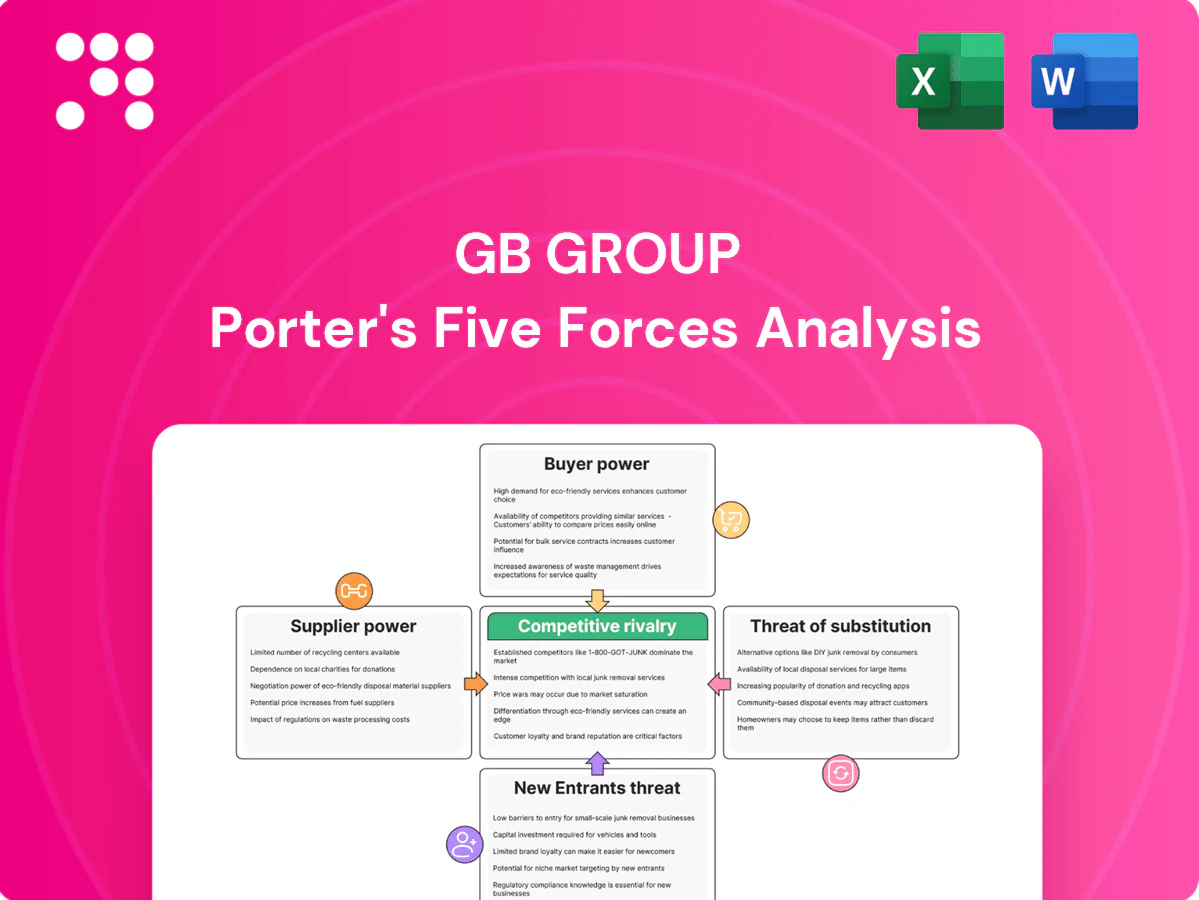

GB Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

GB Group faces moderate buyer power, concentrated supplier relationships, and rising substitute threats from digital identity rivals. Competitive rivalry is intense—scale, data access and regulation shape advantage. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GB Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Data source concentration

GBG depends on critical identity and location feeds from a small set of credit bureaus, telcos and government registries that operate under tight regulation, creating concentrated data sourcing. Limited alternative suppliers give those providers pricing and contractual leverage, while long renewal cycles and exclusive agreements can lock GBG into specific feeds. Loss or degradation of any major feed can immediately reduce coverage and verification accuracy, harming service delivery.

Cloud and tooling dependence

Core GBG services run on hyperscale clouds and third‑party ML/analytics stacks; AWS, Microsoft Azure and Google Cloud together account for over 60% of the market (roughly 32%/22%/11% respectively), and the global public cloud services market is projected near $623B in 2024, making switching costly due to re‑architecture, latency SLAs and compliance; compute, storage and egress price shifts can squeeze margins while preferred partner programs reduce costs yet deepen dependency.

Verification tech vendors

Specialized inputs — OCR, biometrics, device intelligence and geolocation — come from niche vendors, with best‑in‑class accuracy concentrated in a small set of suppliers, elevating their bargaining power. Multi‑vendor orchestration lowers dependency risk but raises integration and ongoing costs. Performance updates or price shifts from these suppliers can quickly affect GBG’s verification success rates and margins; the identity verification market is projected to reach about USD 22.7bn by 2027.

Regulatory data gatekeepers

Access to PEP/sanctions, civil registries and eID schemes is largely controlled by public bodies or licensed aggregators, creating gatekeeper leverage; major sanctions sources remain UN, EU and US OFAC. Policy shifts can change access rights, pricing or permitted data uses; FATF had 39 member bodies in 2024, reflecting regulatory pressure. High compliance overhead raises supplier switching costs and jurisdictional fragmentation (eIDAS covers 27 EU states) complicates global negotiations.

- Gatekeepers: public bodies/licensed aggregators

- Key sources: UN, EU, OFAC

- Regulatory facts: FATF 39 members (2024); eIDAS 27 states

- Impact: higher switching costs, complex cross‑jurisdiction deals

Quality and freshness requirements

Identity accuracy hinges on data timeliness and match rates, with industry data decay ~22% annually making freshness crucial for onboarding; suppliers guaranteeing higher freshness and QA therefore hold greater negotiation power. SLAs for 99.9% uptime and sub-300ms median latency are pivotal for live verification flows. GB Group may accept premiums to secure superior data fidelity in key markets to protect conversion and fraud metrics.

- data decay ~22%/yr

- SLA target 99.9% uptime

- latency target <300ms

- premium paid for higher match rates

Suppliers hold leverage: cloud vendor concentration, data decay, and regulatory gatekeepers

Suppliers hold significant leverage: concentrated data feeds, hyperscaler/cloud dependence (cloud market ~USD 623B in 2024; AWS ~32%/Azure ~22%/GCP ~11%) and niche biometric/OCR providers raise switching costs and margin risk. Regulatory gatekeepers (FATF 39 members in 2024; eIDAS 27 states) further strengthen suppliers. Data decay ~22%/yr makes freshness-priced feeds strategic for GBG.

| Metric | Value | Impact |

|---|---|---|

| Public cloud 2024 | ~USD 623B | High infra dependence |

| AWS/Azure/GCP | 32%/22%/11% | Vendor concentration |

| Data decay | ~22%/yr | Premium for freshness |

| FATF members (2024) | 39 | Regulatory gatekeeping |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to GB Group that uncovers competitive drivers, buyer/supplier power, entry barriers and substitutes, identifies emerging threats and strategic levers to protect market share and inform investor or internal strategy materials.

A concise, one-sheet Porter's Five Forces for GB Group that pinpoints competitive pain points and strategic levers—ready to customize, drop into decks, or duplicate for different market scenarios.

Customers Bargaining Power

Enterprise RFP leverage

Large banks, fintechs, marketplaces and governments run competitive RFPs with stringent SLAs, and their multi‑year contracts—often exceeding $1m annually—give them strong price negotiation and bespoke terms. Their volume and scale enable demands for audits, bespoke integrations and roadmap influence, while losing a marquee client can materially remove revenue visibility for providers.

Switching costs vs modularity

Deep workflow integrations, rules, and compliance mappings in GB Group products materially raise switching costs, embedding vendors in identity and fraud workflows. Yet 2024 Postman data shows about 67% of organizations prioritize API-first architectures, enabling buyers to multi-source and A/B route traffic. This duality moderates but does not eliminate buyer power, as orchestration layers can swap vendors based on price and performance.

Outcome‑based expectations

Buyers demand outcome‑based verification: they scrutinize pass rates, fraud catch and false positives by country and product and insist on transparent, outcome‑linked pricing. Contracts in 2024 commonly include SLAs that allow rapid vendor rebalancing when detection falls short, and clients expect continuous model tuning rather than major price hikes. Underperformance often triggers request for remediation within weeks.

Regulatory burden transfer

Clients now insist GBG demonstrably meets evolving KYC/AML, eIDAS and privacy standards, pushing liability caps, data residency and audit rights into contract negotiations and shifting compliance risk onto GBG; in 2024, 68% of enterprise RFPs cited audit or residency clauses, strengthening buyer leverage.

Heightened buyer demands mean failed audits or noncompliance can directly endanger renewals and revenue streams, increasing churn risk and pressuring GBG to accept tighter liabilities and operational controls.

- liability caps

- data residency

- audit rights

- renewal risk

SMB price sensitivity

SMB buyers prioritize unit price and rapid setup; with c.5.5m UK SMEs in 2024 and SaaS SMB churn averaging ~30% annually (2023–24), GBG risks higher churn if costs rise or volumes fall; rivals bundling verification in marketplaces can undercut GBG’s price premium, so self‑serve funnels must prove fast ROI to retain these customers.

- SMB focus: unit price, ease

- Churn: ~30% SaaS SMBs

- Marketplace bundling: downward pressure

- Fix: fast-value self‑serve

Enterprises wield leverage via >$1m deals; 67% API-first enables multi-sourcing

Large enterprise buyers wield strong price and terms power via multi‑year >$1m contracts and bespoke SLAs. High integration raises switching costs, but 67% API‑first adoption enables multi‑sourcing and vendor swapping. 68% of 2024 RFPs cite audit/residency clauses, while c.5.5m UK SMEs and ~30% SMB SaaS churn pressure price‑sensitive segments.

| Metric | 2024 value |

|---|---|

| API‑first adoption | 67% |

| RFPs citing audit/residency | 68% |

| UK SMEs | ≈5.5m |

| SMB SaaS churn | ≈30% |

| Marquee contract size | >$1m pa |

Preview Before You Purchase

GB Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for GB Group you'll receive immediately after purchase—no placeholders or condensed samples. The document is the full, professionally formatted analysis covering competitive rivalry, buyer power, supplier power, threat of substitutes, and threat of new entrants, ready for download and use. Purchase grants instant access to this same file.

From Overview to Strategy Blueprint

GB Group faces moderate buyer power, concentrated supplier relationships, and rising substitute threats from digital identity rivals. Competitive rivalry is intense—scale, data access and regulation shape advantage. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GB Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Data source concentration

GBG depends on critical identity and location feeds from a small set of credit bureaus, telcos and government registries that operate under tight regulation, creating concentrated data sourcing. Limited alternative suppliers give those providers pricing and contractual leverage, while long renewal cycles and exclusive agreements can lock GBG into specific feeds. Loss or degradation of any major feed can immediately reduce coverage and verification accuracy, harming service delivery.

Cloud and tooling dependence

Core GBG services run on hyperscale clouds and third‑party ML/analytics stacks; AWS, Microsoft Azure and Google Cloud together account for over 60% of the market (roughly 32%/22%/11% respectively), and the global public cloud services market is projected near $623B in 2024, making switching costly due to re‑architecture, latency SLAs and compliance; compute, storage and egress price shifts can squeeze margins while preferred partner programs reduce costs yet deepen dependency.

Verification tech vendors

Specialized inputs — OCR, biometrics, device intelligence and geolocation — come from niche vendors, with best‑in‑class accuracy concentrated in a small set of suppliers, elevating their bargaining power. Multi‑vendor orchestration lowers dependency risk but raises integration and ongoing costs. Performance updates or price shifts from these suppliers can quickly affect GBG’s verification success rates and margins; the identity verification market is projected to reach about USD 22.7bn by 2027.

Regulatory data gatekeepers

Access to PEP/sanctions, civil registries and eID schemes is largely controlled by public bodies or licensed aggregators, creating gatekeeper leverage; major sanctions sources remain UN, EU and US OFAC. Policy shifts can change access rights, pricing or permitted data uses; FATF had 39 member bodies in 2024, reflecting regulatory pressure. High compliance overhead raises supplier switching costs and jurisdictional fragmentation (eIDAS covers 27 EU states) complicates global negotiations.

- Gatekeepers: public bodies/licensed aggregators

- Key sources: UN, EU, OFAC

- Regulatory facts: FATF 39 members (2024); eIDAS 27 states

- Impact: higher switching costs, complex cross‑jurisdiction deals

Quality and freshness requirements

Identity accuracy hinges on data timeliness and match rates, with industry data decay ~22% annually making freshness crucial for onboarding; suppliers guaranteeing higher freshness and QA therefore hold greater negotiation power. SLAs for 99.9% uptime and sub-300ms median latency are pivotal for live verification flows. GB Group may accept premiums to secure superior data fidelity in key markets to protect conversion and fraud metrics.

- data decay ~22%/yr

- SLA target 99.9% uptime

- latency target <300ms

- premium paid for higher match rates

Suppliers hold leverage: cloud vendor concentration, data decay, and regulatory gatekeepers

Suppliers hold significant leverage: concentrated data feeds, hyperscaler/cloud dependence (cloud market ~USD 623B in 2024; AWS ~32%/Azure ~22%/GCP ~11%) and niche biometric/OCR providers raise switching costs and margin risk. Regulatory gatekeepers (FATF 39 members in 2024; eIDAS 27 states) further strengthen suppliers. Data decay ~22%/yr makes freshness-priced feeds strategic for GBG.

| Metric | Value | Impact |

|---|---|---|

| Public cloud 2024 | ~USD 623B | High infra dependence |

| AWS/Azure/GCP | 32%/22%/11% | Vendor concentration |

| Data decay | ~22%/yr | Premium for freshness |

| FATF members (2024) | 39 | Regulatory gatekeeping |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to GB Group that uncovers competitive drivers, buyer/supplier power, entry barriers and substitutes, identifies emerging threats and strategic levers to protect market share and inform investor or internal strategy materials.

A concise, one-sheet Porter's Five Forces for GB Group that pinpoints competitive pain points and strategic levers—ready to customize, drop into decks, or duplicate for different market scenarios.

Customers Bargaining Power

Enterprise RFP leverage

Large banks, fintechs, marketplaces and governments run competitive RFPs with stringent SLAs, and their multi‑year contracts—often exceeding $1m annually—give them strong price negotiation and bespoke terms. Their volume and scale enable demands for audits, bespoke integrations and roadmap influence, while losing a marquee client can materially remove revenue visibility for providers.

Switching costs vs modularity

Deep workflow integrations, rules, and compliance mappings in GB Group products materially raise switching costs, embedding vendors in identity and fraud workflows. Yet 2024 Postman data shows about 67% of organizations prioritize API-first architectures, enabling buyers to multi-source and A/B route traffic. This duality moderates but does not eliminate buyer power, as orchestration layers can swap vendors based on price and performance.

Outcome‑based expectations

Buyers demand outcome‑based verification: they scrutinize pass rates, fraud catch and false positives by country and product and insist on transparent, outcome‑linked pricing. Contracts in 2024 commonly include SLAs that allow rapid vendor rebalancing when detection falls short, and clients expect continuous model tuning rather than major price hikes. Underperformance often triggers request for remediation within weeks.

Regulatory burden transfer

Clients now insist GBG demonstrably meets evolving KYC/AML, eIDAS and privacy standards, pushing liability caps, data residency and audit rights into contract negotiations and shifting compliance risk onto GBG; in 2024, 68% of enterprise RFPs cited audit or residency clauses, strengthening buyer leverage.

Heightened buyer demands mean failed audits or noncompliance can directly endanger renewals and revenue streams, increasing churn risk and pressuring GBG to accept tighter liabilities and operational controls.

- liability caps

- data residency

- audit rights

- renewal risk

SMB price sensitivity

SMB buyers prioritize unit price and rapid setup; with c.5.5m UK SMEs in 2024 and SaaS SMB churn averaging ~30% annually (2023–24), GBG risks higher churn if costs rise or volumes fall; rivals bundling verification in marketplaces can undercut GBG’s price premium, so self‑serve funnels must prove fast ROI to retain these customers.

- SMB focus: unit price, ease

- Churn: ~30% SaaS SMBs

- Marketplace bundling: downward pressure

- Fix: fast-value self‑serve

Enterprises wield leverage via >$1m deals; 67% API-first enables multi-sourcing

Large enterprise buyers wield strong price and terms power via multi‑year >$1m contracts and bespoke SLAs. High integration raises switching costs, but 67% API‑first adoption enables multi‑sourcing and vendor swapping. 68% of 2024 RFPs cite audit/residency clauses, while c.5.5m UK SMEs and ~30% SMB SaaS churn pressure price‑sensitive segments.

| Metric | 2024 value |

|---|---|

| API‑first adoption | 67% |

| RFPs citing audit/residency | 68% |

| UK SMEs | ≈5.5m |

| SMB SaaS churn | ≈30% |

| Marquee contract size | >$1m pa |

Preview Before You Purchase

GB Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for GB Group you'll receive immediately after purchase—no placeholders or condensed samples. The document is the full, professionally formatted analysis covering competitive rivalry, buyer power, supplier power, threat of substitutes, and threat of new entrants, ready for download and use. Purchase grants instant access to this same file.

Description

From Overview to Strategy Blueprint

GB Group faces moderate buyer power, concentrated supplier relationships, and rising substitute threats from digital identity rivals. Competitive rivalry is intense—scale, data access and regulation shape advantage. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GB Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Data source concentration

GBG depends on critical identity and location feeds from a small set of credit bureaus, telcos and government registries that operate under tight regulation, creating concentrated data sourcing. Limited alternative suppliers give those providers pricing and contractual leverage, while long renewal cycles and exclusive agreements can lock GBG into specific feeds. Loss or degradation of any major feed can immediately reduce coverage and verification accuracy, harming service delivery.

Cloud and tooling dependence

Core GBG services run on hyperscale clouds and third‑party ML/analytics stacks; AWS, Microsoft Azure and Google Cloud together account for over 60% of the market (roughly 32%/22%/11% respectively), and the global public cloud services market is projected near $623B in 2024, making switching costly due to re‑architecture, latency SLAs and compliance; compute, storage and egress price shifts can squeeze margins while preferred partner programs reduce costs yet deepen dependency.

Verification tech vendors

Specialized inputs — OCR, biometrics, device intelligence and geolocation — come from niche vendors, with best‑in‑class accuracy concentrated in a small set of suppliers, elevating their bargaining power. Multi‑vendor orchestration lowers dependency risk but raises integration and ongoing costs. Performance updates or price shifts from these suppliers can quickly affect GBG’s verification success rates and margins; the identity verification market is projected to reach about USD 22.7bn by 2027.

Regulatory data gatekeepers

Access to PEP/sanctions, civil registries and eID schemes is largely controlled by public bodies or licensed aggregators, creating gatekeeper leverage; major sanctions sources remain UN, EU and US OFAC. Policy shifts can change access rights, pricing or permitted data uses; FATF had 39 member bodies in 2024, reflecting regulatory pressure. High compliance overhead raises supplier switching costs and jurisdictional fragmentation (eIDAS covers 27 EU states) complicates global negotiations.

- Gatekeepers: public bodies/licensed aggregators

- Key sources: UN, EU, OFAC

- Regulatory facts: FATF 39 members (2024); eIDAS 27 states

- Impact: higher switching costs, complex cross‑jurisdiction deals

Quality and freshness requirements

Identity accuracy hinges on data timeliness and match rates, with industry data decay ~22% annually making freshness crucial for onboarding; suppliers guaranteeing higher freshness and QA therefore hold greater negotiation power. SLAs for 99.9% uptime and sub-300ms median latency are pivotal for live verification flows. GB Group may accept premiums to secure superior data fidelity in key markets to protect conversion and fraud metrics.

- data decay ~22%/yr

- SLA target 99.9% uptime

- latency target <300ms

- premium paid for higher match rates

Suppliers hold leverage: cloud vendor concentration, data decay, and regulatory gatekeepers

Suppliers hold significant leverage: concentrated data feeds, hyperscaler/cloud dependence (cloud market ~USD 623B in 2024; AWS ~32%/Azure ~22%/GCP ~11%) and niche biometric/OCR providers raise switching costs and margin risk. Regulatory gatekeepers (FATF 39 members in 2024; eIDAS 27 states) further strengthen suppliers. Data decay ~22%/yr makes freshness-priced feeds strategic for GBG.

| Metric | Value | Impact |

|---|---|---|

| Public cloud 2024 | ~USD 623B | High infra dependence |

| AWS/Azure/GCP | 32%/22%/11% | Vendor concentration |

| Data decay | ~22%/yr | Premium for freshness |

| FATF members (2024) | 39 | Regulatory gatekeeping |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to GB Group that uncovers competitive drivers, buyer/supplier power, entry barriers and substitutes, identifies emerging threats and strategic levers to protect market share and inform investor or internal strategy materials.

A concise, one-sheet Porter's Five Forces for GB Group that pinpoints competitive pain points and strategic levers—ready to customize, drop into decks, or duplicate for different market scenarios.

Customers Bargaining Power

Enterprise RFP leverage

Large banks, fintechs, marketplaces and governments run competitive RFPs with stringent SLAs, and their multi‑year contracts—often exceeding $1m annually—give them strong price negotiation and bespoke terms. Their volume and scale enable demands for audits, bespoke integrations and roadmap influence, while losing a marquee client can materially remove revenue visibility for providers.

Switching costs vs modularity

Deep workflow integrations, rules, and compliance mappings in GB Group products materially raise switching costs, embedding vendors in identity and fraud workflows. Yet 2024 Postman data shows about 67% of organizations prioritize API-first architectures, enabling buyers to multi-source and A/B route traffic. This duality moderates but does not eliminate buyer power, as orchestration layers can swap vendors based on price and performance.

Outcome‑based expectations

Buyers demand outcome‑based verification: they scrutinize pass rates, fraud catch and false positives by country and product and insist on transparent, outcome‑linked pricing. Contracts in 2024 commonly include SLAs that allow rapid vendor rebalancing when detection falls short, and clients expect continuous model tuning rather than major price hikes. Underperformance often triggers request for remediation within weeks.

Regulatory burden transfer

Clients now insist GBG demonstrably meets evolving KYC/AML, eIDAS and privacy standards, pushing liability caps, data residency and audit rights into contract negotiations and shifting compliance risk onto GBG; in 2024, 68% of enterprise RFPs cited audit or residency clauses, strengthening buyer leverage.

Heightened buyer demands mean failed audits or noncompliance can directly endanger renewals and revenue streams, increasing churn risk and pressuring GBG to accept tighter liabilities and operational controls.

- liability caps

- data residency

- audit rights

- renewal risk

SMB price sensitivity

SMB buyers prioritize unit price and rapid setup; with c.5.5m UK SMEs in 2024 and SaaS SMB churn averaging ~30% annually (2023–24), GBG risks higher churn if costs rise or volumes fall; rivals bundling verification in marketplaces can undercut GBG’s price premium, so self‑serve funnels must prove fast ROI to retain these customers.

- SMB focus: unit price, ease

- Churn: ~30% SaaS SMBs

- Marketplace bundling: downward pressure

- Fix: fast-value self‑serve

Enterprises wield leverage via >$1m deals; 67% API-first enables multi-sourcing

Large enterprise buyers wield strong price and terms power via multi‑year >$1m contracts and bespoke SLAs. High integration raises switching costs, but 67% API‑first adoption enables multi‑sourcing and vendor swapping. 68% of 2024 RFPs cite audit/residency clauses, while c.5.5m UK SMEs and ~30% SMB SaaS churn pressure price‑sensitive segments.

| Metric | 2024 value |

|---|---|

| API‑first adoption | 67% |

| RFPs citing audit/residency | 68% |

| UK SMEs | ≈5.5m |

| SMB SaaS churn | ≈30% |

| Marquee contract size | >$1m pa |

Preview Before You Purchase

GB Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for GB Group you'll receive immediately after purchase—no placeholders or condensed samples. The document is the full, professionally formatted analysis covering competitive rivalry, buyer power, supplier power, threat of substitutes, and threat of new entrants, ready for download and use. Purchase grants instant access to this same file.