Grupo Bimbo Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

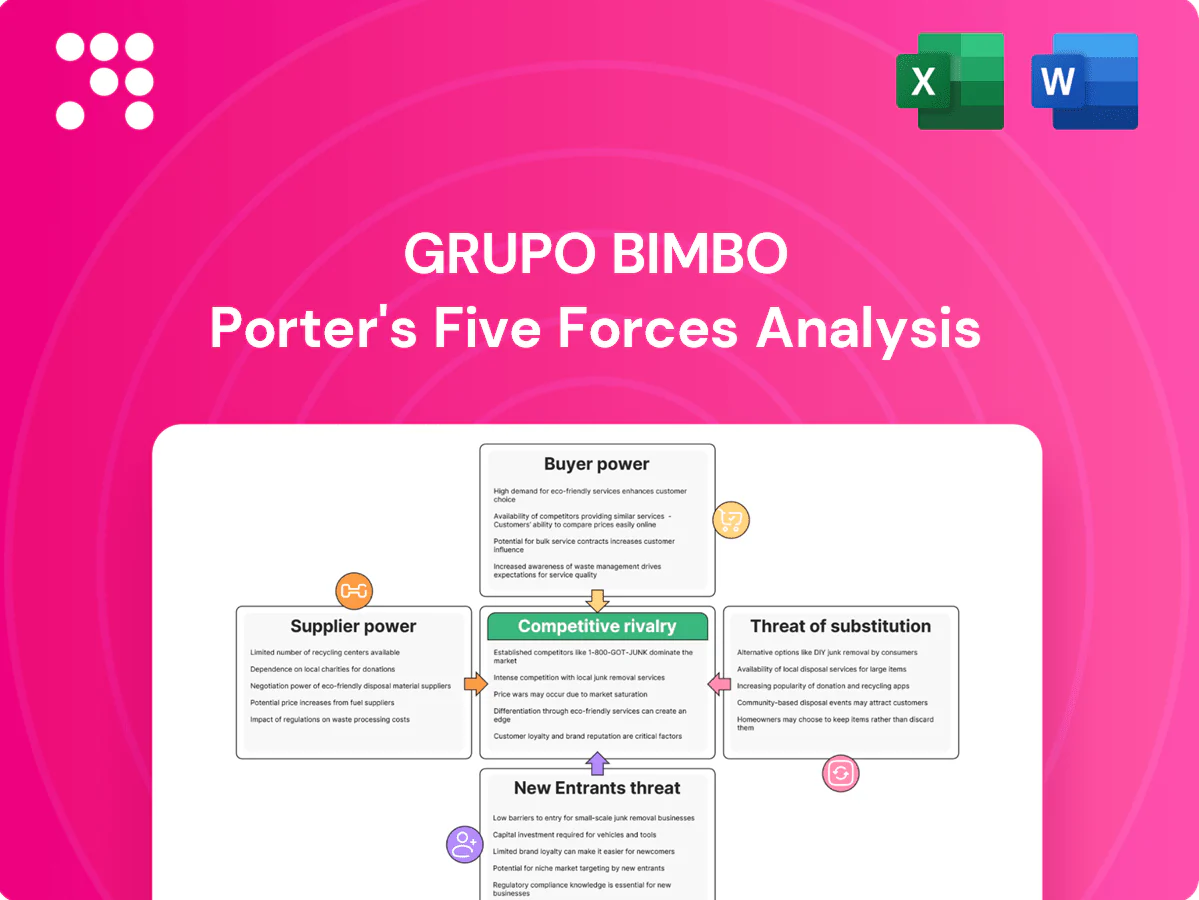

Grupo Bimbo’s Five Forces snapshot shows intense industry rivalry, moderate supplier leverage, growing buyer sophistication, limited substitutes for staples but rising niche threats, and meaningful barriers to entry; strategic nuances matter. This preview only scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights. Purchase the full report to inform investment and strategy.

Suppliers Bargaining Power

Input concentration

Core inputs such as wheat, sugar and vegetable oils are sourced from large agro-commodities players, creating moderate concentration risk. The top four global grain traders (ADM, Bunge, Cargill, Louis Dreyfus) account for roughly 70 percent of global grain trade, allowing influence over terms in tight cycles. Bimbo uses multi-sourcing and hedging to mitigate exposure, but global price spikes still transmit into its cost base. Scale improves negotiation power, yet reliance on a few key categories limits leverage.

Commodity price volatility

Weather, geopolitics and energy costs have driven large swings in flour and edible oil prices—wheat futures experienced intra-year moves exceeding 25% in 2023–2024 and vegetable oil benchmarks showed similar volatility, boosting supplier leverage. When Bimbo’s inventories tighten, that volatility translates into stronger supplier power and shorter negotiating windows. Forward contracts and futures mitigate spikes but cannot erase price shocks, leaving residual exposure. Cost pass-through to retail varies materially by market, reflecting local competition and regulatory constraints.

Specialized packaging and equipment

Specialized high-speed ovens, slicers and barrier films come from few vendors, and switching can trigger weeks of downtime, certification hurdles and capex often exceeding USD 1m per line, giving suppliers measurable leverage; Grupo Bimbo, present in 33+ countries, mitigates this through long-term agreements and global procurement that concentrate purchasing power. Standardization programs across factories have reduced supplier lock-in over recent years.

Logistics and cold-chain services

Sustainability and quality standards

Sustainability-driven traceability requirements and demand for RSPO oils and regenerative grains have narrowed qualified supplier pools; by 2024 RSPO membership exceeded 4,000 entities, tightening certified volume access and raising compliance costs that can shift upstream and increase supplier leverage. Bimbo’s supplier development programs expand its base but require multiple years to scale; lapses in certification create substitution frictions and short-term cost spikes.

- Traceability: tighter supplier shortlist

- RSPO: >4,000 members by 2024

- Compliance: upstream cost pass-through

- Supplier development: slows leverage but time-consuming

- Certification lapses: substitution frictions

Concentrated grain traders, volatile wheat and driver shortages squeeze major bakery margins

Suppliers hold moderate power: top-four grain traders control ~70% of global grain trade, creating concentration risk, while wheat futures swung >25% intra-year in 2023–24, transmitting price shocks into Bimbo’s costs. Capital-intensive ovens/films and refrigerated carriers (driver shortage ~80,000) limit quick switching; Grupo Bimbo’s scale, multi-sourcing, hedging and owned routes mitigate but do not eliminate supplier leverage. RSPO membership >4,000 by 2024 narrows certified oil supply, raising compliance costs.

| Metric | 2023–24 / 2024 |

|---|---|

| Top-4 grain traders share | ~70% |

| Wheat futures intra-year move | >25% |

| RSPO membership | >4,000 |

| Grupo Bimbo footprint | 33+ countries |

What is included in the product

Tailored exclusively for Grupo Bimbo, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes and entry risks, and highlights disruptive threats and market dynamics shaping the company's pricing power and profitability.

A concise one-sheet Porter's Five Forces for Grupo Bimbo—clarifies supplier, buyer, competitor, entrant, and substitute pressures for rapid strategic decisions. Customizable pressure levels and a ready-to-use radar chart make it easy to update with new data and drop directly into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated retail chains

Big-box and supermarket groups such as Walmart (FY2024 revenue $611.3B) and major chains in Mexico and Europe command shelf space and forceful trade terms; their scale enables aggressive negotiations on price, promotions and slotting. Bimbo’s must-have brands provide leverage but do not fully offset dependence on large accounts, which remain influential over volume and margins in 2024.

Private label alternatives

Retailers increasingly push store brands in bread and snacks, with private-label share rising to about 20% in key markets in 2024, increasing retailer leverage over Grupo Bimbo. Comparable quality at value tiers narrows differentiation and pressures Bimbo’s margin structure. Bimbo must accelerate branding and product innovation to justify price premiums, since observed price gaps drive rapid switching among value-conscious consumers.

Route-to-market and DSD reach

Direct-store-delivery (DSD) gives Grupo Bimbo freshness and on-shelf merchandising that lowers buyer power at fragmented outlets; Bimbo reported DSD reach to roughly 1.7 million points of sale in 2024, sustaining frequent drops and trade credit that constrain small retailers’ bargaining. In modern trade DSD is less decisive, with large chains (accounting for ~40–50% of sales) regaining leverage through centralized procurement. Overall channel mix dictates customer power.

Price sensitivity and elasticity

Bread and tortillas are daily staples with high purchase frequency and moderate elasticity; in Mexico 2024 headline inflation ~4.2%, driving visible trade-down behavior that pressures Grupo Bimbo's price realization. Promotional depth, not small list-price moves, drives short-term volume; premium segments (artisan/whole-grain) show lower sensitivity and sustain margins.

- High frequency, moderate elasticity

- 2024 Mexico inflation ~4.2% → trade-down

- Promotions boost volume > list-price cuts

- Premium niches = lower sensitivity

Data and category management

Loyalty data and shelf analytics arm major retailers in negotiations, enabling precise SKU-level asks and tighter promotions; Grupo Bimbo, present in 33 countries and reporting 2023 net sales of about US$17.7 billion, faces demands for joint business plans and performance-based fees that shift promotional and inventory risk onto suppliers. Bimbo’s category leadership supplies actionable insights but also creates accountability as data parity from digital shelf tools narrows information advantages.

- Retailer leverage: loyalty + shelf analytics

- Risk shift: joint plans, performance fees

- Bimbo scale: 33 countries, US$17.7B 2023 sales

- Data parity reduces supplier information edge

Retail giants' slotting and private-labels squeeze suppliers; DSD and analytics shift promo risk

Large retailers (Walmart FY2024 revenue US$611.3B) exert strong price and slotting pressure; modern trade is ~40–50% of Bimbo sales (2024) limiting supplier leverage. Private-labels ~20% in key markets (2024) compress margins; DSD (~1.7M POS) cushions power in fragmented outlets but not with centralized buyers. Loyalty/shelf analytics shift promotional risk to suppliers; Bimbo 2023 sales US$17.7B.

| Metric | Value |

|---|---|

| Modern trade share | 40–50% (2024) |

| DSD reach | ~1.7M POS (2024) |

| Private-label | ~20% key markets (2024) |

| Grupo Bimbo sales | US$17.7B (2023) |

| Walmart revenue | US$611.3B (FY2024) |

Same Document Delivered

Grupo Bimbo Porter's Five Forces Analysis

This preview shows the exact Grupo Bimbo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is professionally formatted, fully referenced and ready for download and use the moment you buy. What you see is the final deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupo Bimbo’s Five Forces snapshot shows intense industry rivalry, moderate supplier leverage, growing buyer sophistication, limited substitutes for staples but rising niche threats, and meaningful barriers to entry; strategic nuances matter. This preview only scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights. Purchase the full report to inform investment and strategy.

Suppliers Bargaining Power

Input concentration

Core inputs such as wheat, sugar and vegetable oils are sourced from large agro-commodities players, creating moderate concentration risk. The top four global grain traders (ADM, Bunge, Cargill, Louis Dreyfus) account for roughly 70 percent of global grain trade, allowing influence over terms in tight cycles. Bimbo uses multi-sourcing and hedging to mitigate exposure, but global price spikes still transmit into its cost base. Scale improves negotiation power, yet reliance on a few key categories limits leverage.

Commodity price volatility

Weather, geopolitics and energy costs have driven large swings in flour and edible oil prices—wheat futures experienced intra-year moves exceeding 25% in 2023–2024 and vegetable oil benchmarks showed similar volatility, boosting supplier leverage. When Bimbo’s inventories tighten, that volatility translates into stronger supplier power and shorter negotiating windows. Forward contracts and futures mitigate spikes but cannot erase price shocks, leaving residual exposure. Cost pass-through to retail varies materially by market, reflecting local competition and regulatory constraints.

Specialized packaging and equipment

Specialized high-speed ovens, slicers and barrier films come from few vendors, and switching can trigger weeks of downtime, certification hurdles and capex often exceeding USD 1m per line, giving suppliers measurable leverage; Grupo Bimbo, present in 33+ countries, mitigates this through long-term agreements and global procurement that concentrate purchasing power. Standardization programs across factories have reduced supplier lock-in over recent years.

Logistics and cold-chain services

Sustainability and quality standards

Sustainability-driven traceability requirements and demand for RSPO oils and regenerative grains have narrowed qualified supplier pools; by 2024 RSPO membership exceeded 4,000 entities, tightening certified volume access and raising compliance costs that can shift upstream and increase supplier leverage. Bimbo’s supplier development programs expand its base but require multiple years to scale; lapses in certification create substitution frictions and short-term cost spikes.

- Traceability: tighter supplier shortlist

- RSPO: >4,000 members by 2024

- Compliance: upstream cost pass-through

- Supplier development: slows leverage but time-consuming

- Certification lapses: substitution frictions

Concentrated grain traders, volatile wheat and driver shortages squeeze major bakery margins

Suppliers hold moderate power: top-four grain traders control ~70% of global grain trade, creating concentration risk, while wheat futures swung >25% intra-year in 2023–24, transmitting price shocks into Bimbo’s costs. Capital-intensive ovens/films and refrigerated carriers (driver shortage ~80,000) limit quick switching; Grupo Bimbo’s scale, multi-sourcing, hedging and owned routes mitigate but do not eliminate supplier leverage. RSPO membership >4,000 by 2024 narrows certified oil supply, raising compliance costs.

| Metric | 2023–24 / 2024 |

|---|---|

| Top-4 grain traders share | ~70% |

| Wheat futures intra-year move | >25% |

| RSPO membership | >4,000 |

| Grupo Bimbo footprint | 33+ countries |

What is included in the product

Tailored exclusively for Grupo Bimbo, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes and entry risks, and highlights disruptive threats and market dynamics shaping the company's pricing power and profitability.

A concise one-sheet Porter's Five Forces for Grupo Bimbo—clarifies supplier, buyer, competitor, entrant, and substitute pressures for rapid strategic decisions. Customizable pressure levels and a ready-to-use radar chart make it easy to update with new data and drop directly into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated retail chains

Big-box and supermarket groups such as Walmart (FY2024 revenue $611.3B) and major chains in Mexico and Europe command shelf space and forceful trade terms; their scale enables aggressive negotiations on price, promotions and slotting. Bimbo’s must-have brands provide leverage but do not fully offset dependence on large accounts, which remain influential over volume and margins in 2024.

Private label alternatives

Retailers increasingly push store brands in bread and snacks, with private-label share rising to about 20% in key markets in 2024, increasing retailer leverage over Grupo Bimbo. Comparable quality at value tiers narrows differentiation and pressures Bimbo’s margin structure. Bimbo must accelerate branding and product innovation to justify price premiums, since observed price gaps drive rapid switching among value-conscious consumers.

Route-to-market and DSD reach

Direct-store-delivery (DSD) gives Grupo Bimbo freshness and on-shelf merchandising that lowers buyer power at fragmented outlets; Bimbo reported DSD reach to roughly 1.7 million points of sale in 2024, sustaining frequent drops and trade credit that constrain small retailers’ bargaining. In modern trade DSD is less decisive, with large chains (accounting for ~40–50% of sales) regaining leverage through centralized procurement. Overall channel mix dictates customer power.

Price sensitivity and elasticity

Bread and tortillas are daily staples with high purchase frequency and moderate elasticity; in Mexico 2024 headline inflation ~4.2%, driving visible trade-down behavior that pressures Grupo Bimbo's price realization. Promotional depth, not small list-price moves, drives short-term volume; premium segments (artisan/whole-grain) show lower sensitivity and sustain margins.

- High frequency, moderate elasticity

- 2024 Mexico inflation ~4.2% → trade-down

- Promotions boost volume > list-price cuts

- Premium niches = lower sensitivity

Data and category management

Loyalty data and shelf analytics arm major retailers in negotiations, enabling precise SKU-level asks and tighter promotions; Grupo Bimbo, present in 33 countries and reporting 2023 net sales of about US$17.7 billion, faces demands for joint business plans and performance-based fees that shift promotional and inventory risk onto suppliers. Bimbo’s category leadership supplies actionable insights but also creates accountability as data parity from digital shelf tools narrows information advantages.

- Retailer leverage: loyalty + shelf analytics

- Risk shift: joint plans, performance fees

- Bimbo scale: 33 countries, US$17.7B 2023 sales

- Data parity reduces supplier information edge

Retail giants' slotting and private-labels squeeze suppliers; DSD and analytics shift promo risk

Large retailers (Walmart FY2024 revenue US$611.3B) exert strong price and slotting pressure; modern trade is ~40–50% of Bimbo sales (2024) limiting supplier leverage. Private-labels ~20% in key markets (2024) compress margins; DSD (~1.7M POS) cushions power in fragmented outlets but not with centralized buyers. Loyalty/shelf analytics shift promotional risk to suppliers; Bimbo 2023 sales US$17.7B.

| Metric | Value |

|---|---|

| Modern trade share | 40–50% (2024) |

| DSD reach | ~1.7M POS (2024) |

| Private-label | ~20% key markets (2024) |

| Grupo Bimbo sales | US$17.7B (2023) |

| Walmart revenue | US$611.3B (FY2024) |

Same Document Delivered

Grupo Bimbo Porter's Five Forces Analysis

This preview shows the exact Grupo Bimbo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is professionally formatted, fully referenced and ready for download and use the moment you buy. What you see is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupo Bimbo’s Five Forces snapshot shows intense industry rivalry, moderate supplier leverage, growing buyer sophistication, limited substitutes for staples but rising niche threats, and meaningful barriers to entry; strategic nuances matter. This preview only scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights. Purchase the full report to inform investment and strategy.

Suppliers Bargaining Power

Input concentration

Core inputs such as wheat, sugar and vegetable oils are sourced from large agro-commodities players, creating moderate concentration risk. The top four global grain traders (ADM, Bunge, Cargill, Louis Dreyfus) account for roughly 70 percent of global grain trade, allowing influence over terms in tight cycles. Bimbo uses multi-sourcing and hedging to mitigate exposure, but global price spikes still transmit into its cost base. Scale improves negotiation power, yet reliance on a few key categories limits leverage.

Commodity price volatility

Weather, geopolitics and energy costs have driven large swings in flour and edible oil prices—wheat futures experienced intra-year moves exceeding 25% in 2023–2024 and vegetable oil benchmarks showed similar volatility, boosting supplier leverage. When Bimbo’s inventories tighten, that volatility translates into stronger supplier power and shorter negotiating windows. Forward contracts and futures mitigate spikes but cannot erase price shocks, leaving residual exposure. Cost pass-through to retail varies materially by market, reflecting local competition and regulatory constraints.

Specialized packaging and equipment

Specialized high-speed ovens, slicers and barrier films come from few vendors, and switching can trigger weeks of downtime, certification hurdles and capex often exceeding USD 1m per line, giving suppliers measurable leverage; Grupo Bimbo, present in 33+ countries, mitigates this through long-term agreements and global procurement that concentrate purchasing power. Standardization programs across factories have reduced supplier lock-in over recent years.

Logistics and cold-chain services

Sustainability and quality standards

Sustainability-driven traceability requirements and demand for RSPO oils and regenerative grains have narrowed qualified supplier pools; by 2024 RSPO membership exceeded 4,000 entities, tightening certified volume access and raising compliance costs that can shift upstream and increase supplier leverage. Bimbo’s supplier development programs expand its base but require multiple years to scale; lapses in certification create substitution frictions and short-term cost spikes.

- Traceability: tighter supplier shortlist

- RSPO: >4,000 members by 2024

- Compliance: upstream cost pass-through

- Supplier development: slows leverage but time-consuming

- Certification lapses: substitution frictions

Concentrated grain traders, volatile wheat and driver shortages squeeze major bakery margins

Suppliers hold moderate power: top-four grain traders control ~70% of global grain trade, creating concentration risk, while wheat futures swung >25% intra-year in 2023–24, transmitting price shocks into Bimbo’s costs. Capital-intensive ovens/films and refrigerated carriers (driver shortage ~80,000) limit quick switching; Grupo Bimbo’s scale, multi-sourcing, hedging and owned routes mitigate but do not eliminate supplier leverage. RSPO membership >4,000 by 2024 narrows certified oil supply, raising compliance costs.

| Metric | 2023–24 / 2024 |

|---|---|

| Top-4 grain traders share | ~70% |

| Wheat futures intra-year move | >25% |

| RSPO membership | >4,000 |

| Grupo Bimbo footprint | 33+ countries |

What is included in the product

Tailored exclusively for Grupo Bimbo, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, substitutes and entry risks, and highlights disruptive threats and market dynamics shaping the company's pricing power and profitability.

A concise one-sheet Porter's Five Forces for Grupo Bimbo—clarifies supplier, buyer, competitor, entrant, and substitute pressures for rapid strategic decisions. Customizable pressure levels and a ready-to-use radar chart make it easy to update with new data and drop directly into pitch decks or boardroom slides.

Customers Bargaining Power

Concentrated retail chains

Big-box and supermarket groups such as Walmart (FY2024 revenue $611.3B) and major chains in Mexico and Europe command shelf space and forceful trade terms; their scale enables aggressive negotiations on price, promotions and slotting. Bimbo’s must-have brands provide leverage but do not fully offset dependence on large accounts, which remain influential over volume and margins in 2024.

Private label alternatives

Retailers increasingly push store brands in bread and snacks, with private-label share rising to about 20% in key markets in 2024, increasing retailer leverage over Grupo Bimbo. Comparable quality at value tiers narrows differentiation and pressures Bimbo’s margin structure. Bimbo must accelerate branding and product innovation to justify price premiums, since observed price gaps drive rapid switching among value-conscious consumers.

Route-to-market and DSD reach

Direct-store-delivery (DSD) gives Grupo Bimbo freshness and on-shelf merchandising that lowers buyer power at fragmented outlets; Bimbo reported DSD reach to roughly 1.7 million points of sale in 2024, sustaining frequent drops and trade credit that constrain small retailers’ bargaining. In modern trade DSD is less decisive, with large chains (accounting for ~40–50% of sales) regaining leverage through centralized procurement. Overall channel mix dictates customer power.

Price sensitivity and elasticity

Bread and tortillas are daily staples with high purchase frequency and moderate elasticity; in Mexico 2024 headline inflation ~4.2%, driving visible trade-down behavior that pressures Grupo Bimbo's price realization. Promotional depth, not small list-price moves, drives short-term volume; premium segments (artisan/whole-grain) show lower sensitivity and sustain margins.

- High frequency, moderate elasticity

- 2024 Mexico inflation ~4.2% → trade-down

- Promotions boost volume > list-price cuts

- Premium niches = lower sensitivity

Data and category management

Loyalty data and shelf analytics arm major retailers in negotiations, enabling precise SKU-level asks and tighter promotions; Grupo Bimbo, present in 33 countries and reporting 2023 net sales of about US$17.7 billion, faces demands for joint business plans and performance-based fees that shift promotional and inventory risk onto suppliers. Bimbo’s category leadership supplies actionable insights but also creates accountability as data parity from digital shelf tools narrows information advantages.

- Retailer leverage: loyalty + shelf analytics

- Risk shift: joint plans, performance fees

- Bimbo scale: 33 countries, US$17.7B 2023 sales

- Data parity reduces supplier information edge

Retail giants' slotting and private-labels squeeze suppliers; DSD and analytics shift promo risk

Large retailers (Walmart FY2024 revenue US$611.3B) exert strong price and slotting pressure; modern trade is ~40–50% of Bimbo sales (2024) limiting supplier leverage. Private-labels ~20% in key markets (2024) compress margins; DSD (~1.7M POS) cushions power in fragmented outlets but not with centralized buyers. Loyalty/shelf analytics shift promotional risk to suppliers; Bimbo 2023 sales US$17.7B.

| Metric | Value |

|---|---|

| Modern trade share | 40–50% (2024) |

| DSD reach | ~1.7M POS (2024) |

| Private-label | ~20% key markets (2024) |

| Grupo Bimbo sales | US$17.7B (2023) |

| Walmart revenue | US$611.3B (FY2024) |

Same Document Delivered

Grupo Bimbo Porter's Five Forces Analysis

This preview shows the exact Grupo Bimbo Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is professionally formatted, fully referenced and ready for download and use the moment you buy. What you see is the final deliverable.