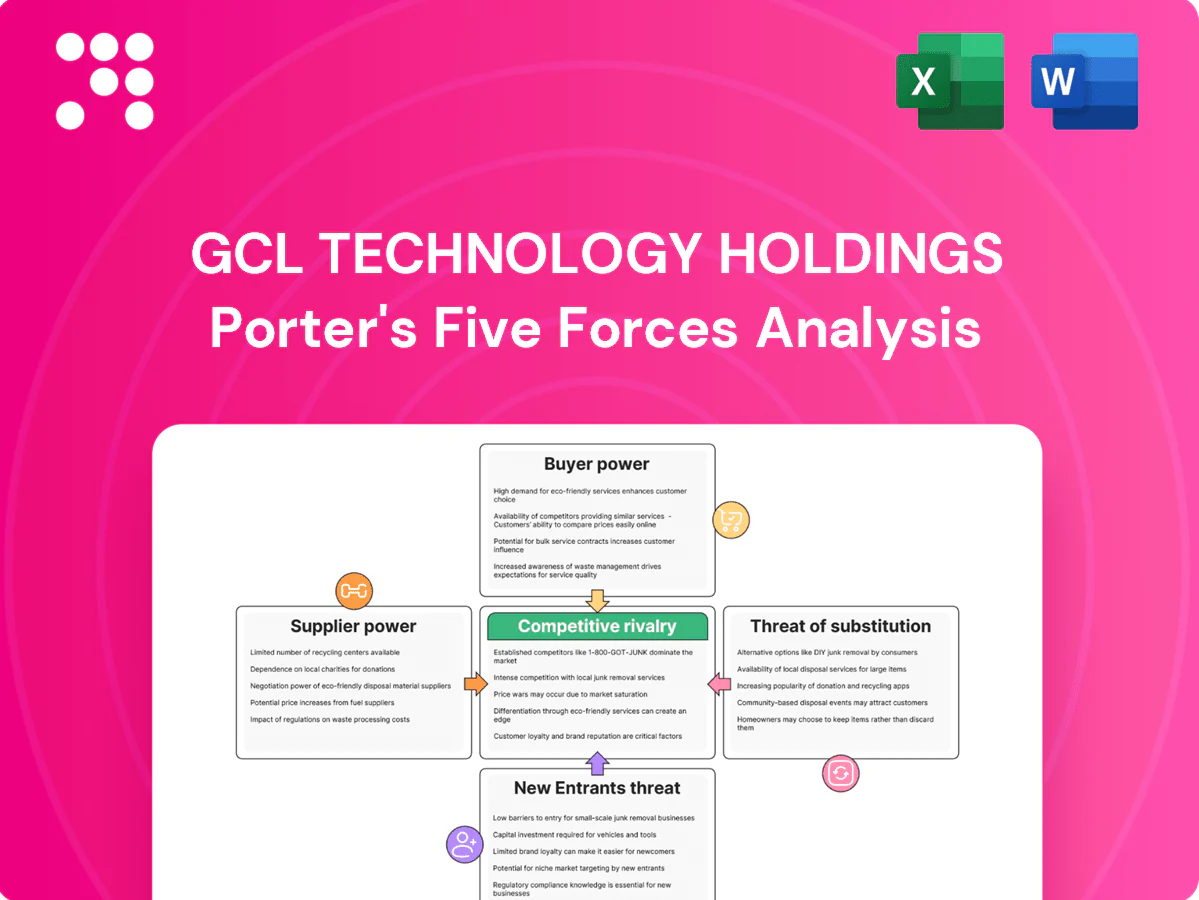

GCL Technology Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

GCL Technology Holdings faces moderate supplier power, rising rivalry in solar polysilicon and downstream pressure from large buyers — dynamics that will shape margins and growth. Competitive intensity and substitute threats warrant strategic clarity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Energy and utilities concentration

GCL’s polysilicon output is highly electricity- and gas-intensive, with power costs typically representing roughly 30–40% of production cash costs and China accounting for about 85% of global polysilicon capacity in 2024, linking GCL to regional utilities and tariffs. Where low-cost renewables or captive power are limited, suppliers can push price and availability pressure. Long-term PPAs and on-site generation reduce this leverage. Grid curtailment or policy-driven tariff changes can still swing bargaining power back to utilities.

Silicon metal and chemical inputs

Metallurgical-grade silicon, chlorine, hydrogen and specialty gases remain largely commoditized and cyclical; 2024 feedstock tightness saw manufacturers pass through cost increases rapidly, compressing peer gross margins by roughly 150–300 basis points in supply crunches. Diversified sourcing and index-linked contracts materially reduce volatility, while inventory buffers mitigate short shocks, though prolonged price spikes still elevate supplier bargaining power.

Specialized equipment vendors

Specialized reactors (eg. Siemens/FBR), quartzware, graphite parts and automation are sourced from a small pool of qualified vendors, giving suppliers leverage as tool lead times commonly run 6–12 months and qualification cycles 6–18 months. Multi-vendor sourcing and in-house engineering at GCL Technology reduce dependence and procurement risk. However, 2024 ramp of N-type grade purity equipment created temporary supply bottlenecks for next-gen tools.

Logistics and materials purity

Ultra-high purity (eg 6N grade) for crucibles, liners and filtration media raises switching costs and makes replacements disruptive; vendor certification and yield sensitivity elevate the value of proven suppliers and strengthen supplier bargaining power. Long-term contracts and co-development with key vendors partially offset this pressure.

- High purity raises switching costs

- Certification boosts supplier value

- Yield sensitivity increases leverage

- Long-term ties/co-dev reduce risk

Environmental and permitting constraints

Chemical handling, emissions control and waste treatment for GCL rely on specialized contractors, and tightening 2024 environmental rules has increased vendor leverage; the global environmental services market exceeded $150 billion in 2024, raising input-cost pressure. Vertical integration of utilities and EHS capabilities can reduce supplier pricing power, but persistent compliance dependencies sustain baseline supplier influence.

- Specialized service reliance

- 2024 market >$150bn

- Regulatory tightening ↑ supplier leverage

- Vertical integration mitigates risk

30–40% power share; China ~85% capacity tightens margins

GCL’s polysilicon power costs ~30–40% of cash costs; China held ~85% of global capacity in 2024, tying GCL to regional utilities and tariffs. Commoditized feedstocks caused 2024 margin hits of ~150–300bps during tightness. Specialized tools and 6N materials have 6–18 month qualification cycles, boosting supplier leverage despite long-term contracts.

| Metric | 2024 |

|---|---|

| Power cost share | 30–40% |

| China capacity | ~85% |

| Peer margin hit | 150–300bps |

| Env services market | >$150bn |

What is included in the product

Tailored Porter's Five Forces analysis for GCL Technology Holdings that uncovers key competitive drivers, supplier and buyer influence on pricing, and barriers protecting incumbents, while identifying disruptive substitutes and emerging threats to market share. Fully editable for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter’s Five Forces for GCL Technology Holdings—instantly highlights supplier power, buyer leverage, competitive rivalry, threat of entrants and substitutes to speed strategic decisions and address industry pain points.

Customers Bargaining Power

Concentrated Tier-1 customers

Concentrated Tier-1 customers—large vertically integrated wafer and module makers—buy in bulk and push hard on pricing and specs; top five module suppliers captured over 60% of global shipments in 2024, enabling cross-supplier price benchmarking. Their concentration raises leverage on contractual terms and quality, and losing a single top account can materially depress utilization and realized prices for suppliers like GCL Technology.

Commodity pricing and spot volatility

Polysilicon prices swing with capacity cycles, and in 2024 spot quotes averaged roughly $8/kg, shifting bargaining power to buyers during oversupply. Buyers lean on transparent spot benchmarks to renegotiate terms or defer offtake, increasing optionality. Take-or-pay and floor-price clauses can defend margins but are not universal, so volatility squeezes producers in downcycles.

Low switching costs for qualified grades

Once qualified, buyers can switch among producers for P-type and increasingly for N-type grades, and in 2024 industry qualification cycles shortened to weeks as standardization and mature QA reduced frictions. Differentiation through ultra-low impurity and granular silicon narrows substitutability for premium customers. For mainstream grades, however, buyers retain notable bargaining power, pressuring prices and spot margins.

Forward contracts vs spot mix

Long-term forward contracts give GCL volume visibility but lock in discounts and performance penalties; buyers push for flexible delivery windows to match module demand, increasing negotiation leverage. In 2024 heightened spot volatility (price swings up to 25%) amplified buyer pressure during downturns, so optimizing forward vs spot mix is critical to moderate customer bargaining power.

- Forward contracts: volume certainty, lower margins

- Spot exposure: higher price risk, boosts buyer leverage

- 2024 volatility: ~25% peak price swings

- Optimal mix: balance margin stability and delivery flexibility

Technical roadmaps and purity demands

N-type/TOPCon and HJT transitions push wafer purity and tighter oxygen/metallic limits, with TOPCon adoption ~30% and HJT ~7% of global cell production in 2024; buyers leverage evolving specs to demand improved price-performance. Suppliers consistently meeting sub-ppm impurity targets can reclaim negotiating power, while 6–12 month qualification lead times often anchor supplier-buyer ties and moderate short-term buyer leverage.

- Purity pressure: sub-ppm impurity targets

- Market mix 2024: TOPCon ~30%, HJT ~7%

- Buyer leverage: drives price-performance demands

- Supplier edge: consistent spec compliance restores power

- Qualification lag: 6–12 months moderates churn

Top-5 buyers control >60% shipments; polysilicon $8/kg, ~25% swings

Concentrated Tier-1 buyers (top5 >60% global shipments 2024) exert strong price/spec leverage; losing one client cuts utilization materially. Polysilicon averaged $8/kg in 2024 with ~25% peak spot swings, boosting buyer bargaining. TOPCon ~30% and HJT ~7% of cell mix 2024; 6–12 month qualification windows partly limit churn.

| Metric | 2024 |

|---|---|

| Top5 module share | >60% |

| Polysilicon spot | $8/kg |

| Spot volatility | ~25% |

| TOPCon/HJT mix | 30% / 7% |

| Qualification lag | 6–12 months |

Preview Before You Purchase

GCL Technology Holdings Porter's Five Forces Analysis

This preview shows the exact GCL Technology Holdings Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full document is professionally formatted, complete with supplier, buyer, rivalry, threat of entry and substitute assessments. Instant download and ready for use upon payment.

A Must-Have Tool for Decision-Makers

GCL Technology Holdings faces moderate supplier power, rising rivalry in solar polysilicon and downstream pressure from large buyers — dynamics that will shape margins and growth. Competitive intensity and substitute threats warrant strategic clarity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Energy and utilities concentration

GCL’s polysilicon output is highly electricity- and gas-intensive, with power costs typically representing roughly 30–40% of production cash costs and China accounting for about 85% of global polysilicon capacity in 2024, linking GCL to regional utilities and tariffs. Where low-cost renewables or captive power are limited, suppliers can push price and availability pressure. Long-term PPAs and on-site generation reduce this leverage. Grid curtailment or policy-driven tariff changes can still swing bargaining power back to utilities.

Silicon metal and chemical inputs

Metallurgical-grade silicon, chlorine, hydrogen and specialty gases remain largely commoditized and cyclical; 2024 feedstock tightness saw manufacturers pass through cost increases rapidly, compressing peer gross margins by roughly 150–300 basis points in supply crunches. Diversified sourcing and index-linked contracts materially reduce volatility, while inventory buffers mitigate short shocks, though prolonged price spikes still elevate supplier bargaining power.

Specialized equipment vendors

Specialized reactors (eg. Siemens/FBR), quartzware, graphite parts and automation are sourced from a small pool of qualified vendors, giving suppliers leverage as tool lead times commonly run 6–12 months and qualification cycles 6–18 months. Multi-vendor sourcing and in-house engineering at GCL Technology reduce dependence and procurement risk. However, 2024 ramp of N-type grade purity equipment created temporary supply bottlenecks for next-gen tools.

Logistics and materials purity

Ultra-high purity (eg 6N grade) for crucibles, liners and filtration media raises switching costs and makes replacements disruptive; vendor certification and yield sensitivity elevate the value of proven suppliers and strengthen supplier bargaining power. Long-term contracts and co-development with key vendors partially offset this pressure.

- High purity raises switching costs

- Certification boosts supplier value

- Yield sensitivity increases leverage

- Long-term ties/co-dev reduce risk

Environmental and permitting constraints

Chemical handling, emissions control and waste treatment for GCL rely on specialized contractors, and tightening 2024 environmental rules has increased vendor leverage; the global environmental services market exceeded $150 billion in 2024, raising input-cost pressure. Vertical integration of utilities and EHS capabilities can reduce supplier pricing power, but persistent compliance dependencies sustain baseline supplier influence.

- Specialized service reliance

- 2024 market >$150bn

- Regulatory tightening ↑ supplier leverage

- Vertical integration mitigates risk

30–40% power share; China ~85% capacity tightens margins

GCL’s polysilicon power costs ~30–40% of cash costs; China held ~85% of global capacity in 2024, tying GCL to regional utilities and tariffs. Commoditized feedstocks caused 2024 margin hits of ~150–300bps during tightness. Specialized tools and 6N materials have 6–18 month qualification cycles, boosting supplier leverage despite long-term contracts.

| Metric | 2024 |

|---|---|

| Power cost share | 30–40% |

| China capacity | ~85% |

| Peer margin hit | 150–300bps |

| Env services market | >$150bn |

What is included in the product

Tailored Porter's Five Forces analysis for GCL Technology Holdings that uncovers key competitive drivers, supplier and buyer influence on pricing, and barriers protecting incumbents, while identifying disruptive substitutes and emerging threats to market share. Fully editable for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter’s Five Forces for GCL Technology Holdings—instantly highlights supplier power, buyer leverage, competitive rivalry, threat of entrants and substitutes to speed strategic decisions and address industry pain points.

Customers Bargaining Power

Concentrated Tier-1 customers

Concentrated Tier-1 customers—large vertically integrated wafer and module makers—buy in bulk and push hard on pricing and specs; top five module suppliers captured over 60% of global shipments in 2024, enabling cross-supplier price benchmarking. Their concentration raises leverage on contractual terms and quality, and losing a single top account can materially depress utilization and realized prices for suppliers like GCL Technology.

Commodity pricing and spot volatility

Polysilicon prices swing with capacity cycles, and in 2024 spot quotes averaged roughly $8/kg, shifting bargaining power to buyers during oversupply. Buyers lean on transparent spot benchmarks to renegotiate terms or defer offtake, increasing optionality. Take-or-pay and floor-price clauses can defend margins but are not universal, so volatility squeezes producers in downcycles.

Low switching costs for qualified grades

Once qualified, buyers can switch among producers for P-type and increasingly for N-type grades, and in 2024 industry qualification cycles shortened to weeks as standardization and mature QA reduced frictions. Differentiation through ultra-low impurity and granular silicon narrows substitutability for premium customers. For mainstream grades, however, buyers retain notable bargaining power, pressuring prices and spot margins.

Forward contracts vs spot mix

Long-term forward contracts give GCL volume visibility but lock in discounts and performance penalties; buyers push for flexible delivery windows to match module demand, increasing negotiation leverage. In 2024 heightened spot volatility (price swings up to 25%) amplified buyer pressure during downturns, so optimizing forward vs spot mix is critical to moderate customer bargaining power.

- Forward contracts: volume certainty, lower margins

- Spot exposure: higher price risk, boosts buyer leverage

- 2024 volatility: ~25% peak price swings

- Optimal mix: balance margin stability and delivery flexibility

Technical roadmaps and purity demands

N-type/TOPCon and HJT transitions push wafer purity and tighter oxygen/metallic limits, with TOPCon adoption ~30% and HJT ~7% of global cell production in 2024; buyers leverage evolving specs to demand improved price-performance. Suppliers consistently meeting sub-ppm impurity targets can reclaim negotiating power, while 6–12 month qualification lead times often anchor supplier-buyer ties and moderate short-term buyer leverage.

- Purity pressure: sub-ppm impurity targets

- Market mix 2024: TOPCon ~30%, HJT ~7%

- Buyer leverage: drives price-performance demands

- Supplier edge: consistent spec compliance restores power

- Qualification lag: 6–12 months moderates churn

Top-5 buyers control >60% shipments; polysilicon $8/kg, ~25% swings

Concentrated Tier-1 buyers (top5 >60% global shipments 2024) exert strong price/spec leverage; losing one client cuts utilization materially. Polysilicon averaged $8/kg in 2024 with ~25% peak spot swings, boosting buyer bargaining. TOPCon ~30% and HJT ~7% of cell mix 2024; 6–12 month qualification windows partly limit churn.

| Metric | 2024 |

|---|---|

| Top5 module share | >60% |

| Polysilicon spot | $8/kg |

| Spot volatility | ~25% |

| TOPCon/HJT mix | 30% / 7% |

| Qualification lag | 6–12 months |

Preview Before You Purchase

GCL Technology Holdings Porter's Five Forces Analysis

This preview shows the exact GCL Technology Holdings Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full document is professionally formatted, complete with supplier, buyer, rivalry, threat of entry and substitute assessments. Instant download and ready for use upon payment.

Description

A Must-Have Tool for Decision-Makers

GCL Technology Holdings faces moderate supplier power, rising rivalry in solar polysilicon and downstream pressure from large buyers — dynamics that will shape margins and growth. Competitive intensity and substitute threats warrant strategic clarity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Energy and utilities concentration

GCL’s polysilicon output is highly electricity- and gas-intensive, with power costs typically representing roughly 30–40% of production cash costs and China accounting for about 85% of global polysilicon capacity in 2024, linking GCL to regional utilities and tariffs. Where low-cost renewables or captive power are limited, suppliers can push price and availability pressure. Long-term PPAs and on-site generation reduce this leverage. Grid curtailment or policy-driven tariff changes can still swing bargaining power back to utilities.

Silicon metal and chemical inputs

Metallurgical-grade silicon, chlorine, hydrogen and specialty gases remain largely commoditized and cyclical; 2024 feedstock tightness saw manufacturers pass through cost increases rapidly, compressing peer gross margins by roughly 150–300 basis points in supply crunches. Diversified sourcing and index-linked contracts materially reduce volatility, while inventory buffers mitigate short shocks, though prolonged price spikes still elevate supplier bargaining power.

Specialized equipment vendors

Specialized reactors (eg. Siemens/FBR), quartzware, graphite parts and automation are sourced from a small pool of qualified vendors, giving suppliers leverage as tool lead times commonly run 6–12 months and qualification cycles 6–18 months. Multi-vendor sourcing and in-house engineering at GCL Technology reduce dependence and procurement risk. However, 2024 ramp of N-type grade purity equipment created temporary supply bottlenecks for next-gen tools.

Logistics and materials purity

Ultra-high purity (eg 6N grade) for crucibles, liners and filtration media raises switching costs and makes replacements disruptive; vendor certification and yield sensitivity elevate the value of proven suppliers and strengthen supplier bargaining power. Long-term contracts and co-development with key vendors partially offset this pressure.

- High purity raises switching costs

- Certification boosts supplier value

- Yield sensitivity increases leverage

- Long-term ties/co-dev reduce risk

Environmental and permitting constraints

Chemical handling, emissions control and waste treatment for GCL rely on specialized contractors, and tightening 2024 environmental rules has increased vendor leverage; the global environmental services market exceeded $150 billion in 2024, raising input-cost pressure. Vertical integration of utilities and EHS capabilities can reduce supplier pricing power, but persistent compliance dependencies sustain baseline supplier influence.

- Specialized service reliance

- 2024 market >$150bn

- Regulatory tightening ↑ supplier leverage

- Vertical integration mitigates risk

30–40% power share; China ~85% capacity tightens margins

GCL’s polysilicon power costs ~30–40% of cash costs; China held ~85% of global capacity in 2024, tying GCL to regional utilities and tariffs. Commoditized feedstocks caused 2024 margin hits of ~150–300bps during tightness. Specialized tools and 6N materials have 6–18 month qualification cycles, boosting supplier leverage despite long-term contracts.

| Metric | 2024 |

|---|---|

| Power cost share | 30–40% |

| China capacity | ~85% |

| Peer margin hit | 150–300bps |

| Env services market | >$150bn |

What is included in the product

Tailored Porter's Five Forces analysis for GCL Technology Holdings that uncovers key competitive drivers, supplier and buyer influence on pricing, and barriers protecting incumbents, while identifying disruptive substitutes and emerging threats to market share. Fully editable for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter’s Five Forces for GCL Technology Holdings—instantly highlights supplier power, buyer leverage, competitive rivalry, threat of entrants and substitutes to speed strategic decisions and address industry pain points.

Customers Bargaining Power

Concentrated Tier-1 customers

Concentrated Tier-1 customers—large vertically integrated wafer and module makers—buy in bulk and push hard on pricing and specs; top five module suppliers captured over 60% of global shipments in 2024, enabling cross-supplier price benchmarking. Their concentration raises leverage on contractual terms and quality, and losing a single top account can materially depress utilization and realized prices for suppliers like GCL Technology.

Commodity pricing and spot volatility

Polysilicon prices swing with capacity cycles, and in 2024 spot quotes averaged roughly $8/kg, shifting bargaining power to buyers during oversupply. Buyers lean on transparent spot benchmarks to renegotiate terms or defer offtake, increasing optionality. Take-or-pay and floor-price clauses can defend margins but are not universal, so volatility squeezes producers in downcycles.

Low switching costs for qualified grades

Once qualified, buyers can switch among producers for P-type and increasingly for N-type grades, and in 2024 industry qualification cycles shortened to weeks as standardization and mature QA reduced frictions. Differentiation through ultra-low impurity and granular silicon narrows substitutability for premium customers. For mainstream grades, however, buyers retain notable bargaining power, pressuring prices and spot margins.

Forward contracts vs spot mix

Long-term forward contracts give GCL volume visibility but lock in discounts and performance penalties; buyers push for flexible delivery windows to match module demand, increasing negotiation leverage. In 2024 heightened spot volatility (price swings up to 25%) amplified buyer pressure during downturns, so optimizing forward vs spot mix is critical to moderate customer bargaining power.

- Forward contracts: volume certainty, lower margins

- Spot exposure: higher price risk, boosts buyer leverage

- 2024 volatility: ~25% peak price swings

- Optimal mix: balance margin stability and delivery flexibility

Technical roadmaps and purity demands

N-type/TOPCon and HJT transitions push wafer purity and tighter oxygen/metallic limits, with TOPCon adoption ~30% and HJT ~7% of global cell production in 2024; buyers leverage evolving specs to demand improved price-performance. Suppliers consistently meeting sub-ppm impurity targets can reclaim negotiating power, while 6–12 month qualification lead times often anchor supplier-buyer ties and moderate short-term buyer leverage.

- Purity pressure: sub-ppm impurity targets

- Market mix 2024: TOPCon ~30%, HJT ~7%

- Buyer leverage: drives price-performance demands

- Supplier edge: consistent spec compliance restores power

- Qualification lag: 6–12 months moderates churn

Top-5 buyers control >60% shipments; polysilicon $8/kg, ~25% swings

Concentrated Tier-1 buyers (top5 >60% global shipments 2024) exert strong price/spec leverage; losing one client cuts utilization materially. Polysilicon averaged $8/kg in 2024 with ~25% peak spot swings, boosting buyer bargaining. TOPCon ~30% and HJT ~7% of cell mix 2024; 6–12 month qualification windows partly limit churn.

| Metric | 2024 |

|---|---|

| Top5 module share | >60% |

| Polysilicon spot | $8/kg |

| Spot volatility | ~25% |

| TOPCon/HJT mix | 30% / 7% |

| Qualification lag | 6–12 months |

Preview Before You Purchase

GCL Technology Holdings Porter's Five Forces Analysis

This preview shows the exact GCL Technology Holdings Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full document is professionally formatted, complete with supplier, buyer, rivalry, threat of entry and substitute assessments. Instant download and ready for use upon payment.