Alpha Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

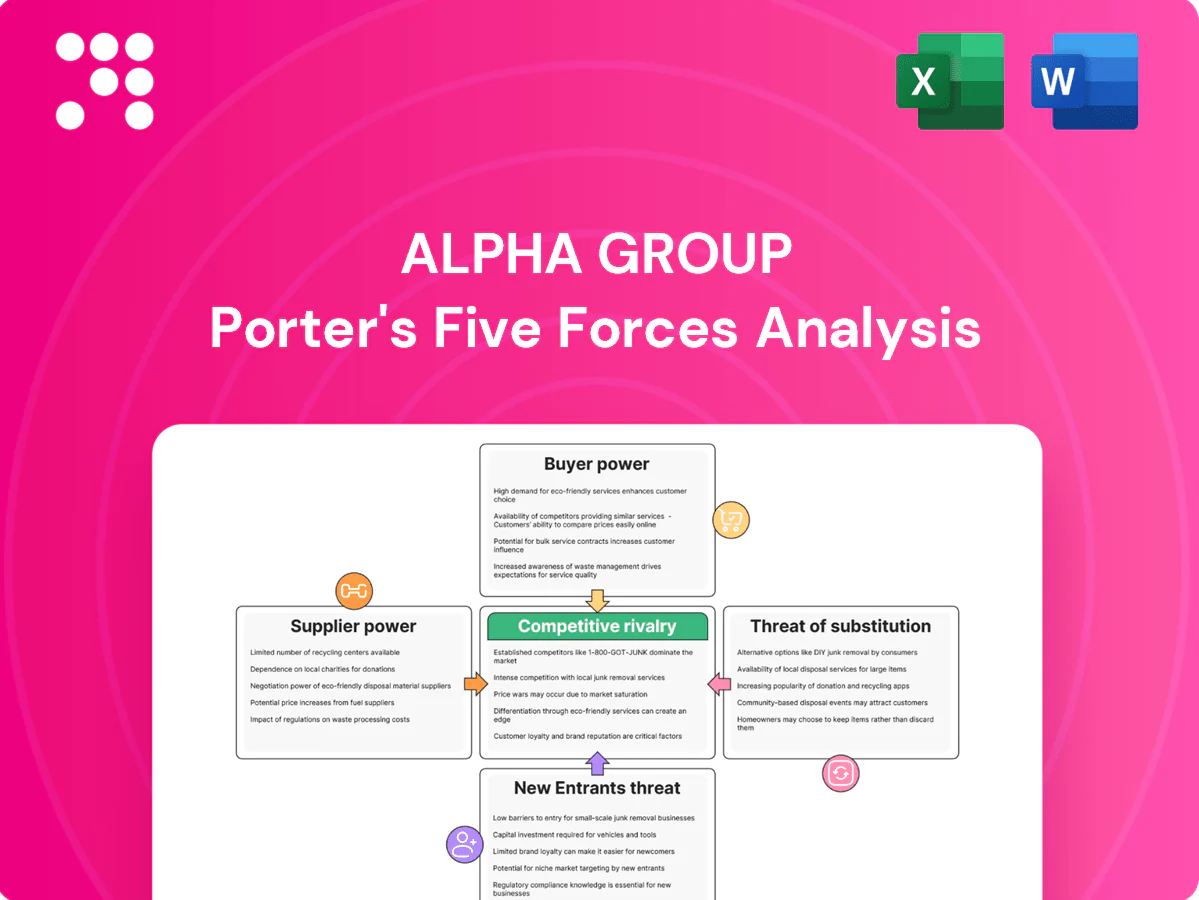

Alpha Group’s Porter’s Five Forces snapshot highlights intense rivalry, moderate supplier power, rising substitute threats, constrained buyer leverage, and significant barriers for new entrants that shape profitability. These forces map strategic vulnerabilities and growth levers critical for investors and managers. This brief whets the appetite—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy. Purchase the complete report to inform smarter decisions.

Suppliers Bargaining Power

Concentrated OEMs

Alpha Group depends on contract manufacturers in China and Southeast Asia; as of 2024 China accounted for roughly two-thirds of global toy production, concentrating high-quality, safety-compliant OEM capacity. This concentration gives top-tier suppliers leverage over lead times and minimum order quantities, especially for licensed SKUs. Long-standing relationships and consolidated volume purchases help Alpha mitigate direct price pressure and secure capacity.

Specialized creative talent

Specialized creative talent—animators, writers, voice actors and showrunners with proven kids’ hits—are scarce, letting star creators and premium studios extract favorable fees, schedules and back-end participation; top showrunners can command six-figure per-episode fees. The 2023 BLS median wage for animators was $78,790 and localization demand rose with global streaming rollouts. In-house pipelines reduce but do not eliminate this supplier power.

Raw material volatility

Plastics (ABS/PP), resins, electronics and packaging inputs are tightly tied to petrochemical and commodity cycles—Brent crude averaged about 86 USD/bbl in 2024—so suppliers routinely pass cost spikes through, squeezing OEM margins. Tooling and molds demand significant upfront supplier investment, raising dependency and switching costs. Hedging and multi-year contracts mitigate but do not eliminate price volatility.

Licensing and tech stack

- Switching cost: entrenched tool ecosystems

- Cloud share 2024: AWS ~32% / Azure ~23% / Google ~10%

- Peak pressure: traffic surges >3x in 2024

- Mitigation: proprietary stack = reduced vendor risk but high CapEx/time

Logistics and compliance

Global shipping, customs brokers and testing labs (EN71, ASTM, CCC) are essential inputs for Alpha Group; 2024 global container throughput is ~790m TEU, keeping ocean capacity tight and spot volatility elevated. Tight holiday calendars and port congestion (avg. vessel delay up to 2–4 days in major hubs in 2024) strengthen logistics providers’ negotiating position. Compliance labs add fixed costs and 4–8 week lead times, creating schedule risk, while preferred-partner programs trade 5–15% price concessions for forecasted volume certainty.

- Essential: global shipping, customs brokers, testing labs

- 2024 throughput: ~790m TEU; port delays 2–4 days

- Compliance: 4–8 week lab lead times; certification costs vary

- Mitigation: preferred-partner programs yield 5–15% price relief

Supplier concentration, talent premium squeeze margins; deals save 5–15%

Alpha faces concentrated OEM power (China ≈66% of toy production in 2024) and high switching costs for tooling and lead times, limiting price flexibility. Creative talent and specialized studios command premium fees (animator median wage $78,790 in 2023/2024), while cloud and logistics concentration (AWS 32%/Azure 23%/GCP 10%; 790m TEU, 2–4d delays) sustain supplier leverage. Multi-year contracts, hedges and preferred-partner programs (5–15% price relief) partially mitigate risk.

| Supplier | Key metric (2024) |

|---|---|

| OEMs | China ≈66% toy production |

| Cloud | AWS 32% / Azure 23% / GCP 10% |

| Shipping | 790m TEU, delays 2–4 days |

| Talent | Animator median $78,790 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Alpha Group. Evaluates supplier and buyer power, substitutes, and new-entrant threats to clarify pricing, profitability, and strategic defenses.

A single-sheet Alpha Group Porter's Five Forces summary unpacks competitive pressures for fast strategic decisions; customizable force levels and an instant radar chart let you model scenarios, swap in your data, and drop clean visuals straight into decks.

Customers Bargaining Power

Retailer consolidation

Mass merchants and e-commerce platforms dominate shelf and search visibility—Amazon held about 38% of US e-commerce sales in 2024 and the top 10 retailers comprised roughly 60% of US retail sales, concentrating negotiating power. Large accounts routinely extract lower prices, co-op funding and flexible returns, pressuring margins. Delisting risk forces additional concessions as shelf space tightens. Expanding into D2C and specialty channels cuts dependence and recaptures margin.

Platform gatekeepers

Streaming platforms negotiate licensing fees and windowing with dominant players like Netflix (~260 million subscribers in 2024) and YouTube (2+ billion monthly users) setting market terms.

Algorithmic promotion accounts for roughly 70% of discovery/viewing, materially shaping franchise visibility and downstream toy demand.

Platforms leverage granular viewer data to demand exclusivity and tougher revenue splits, while multi-platform distribution (streaming, linear, retail) can restore negotiating balance.

Price-sensitive parents

Price-sensitive parents in a $114 billion global toy market (2023, Statista) face abundant alternatives so end buyers are value-driven and switching costs are low, compressing pricing power. Online reviews and social proof sway demand rapidly—over 90% consult reviews before buying (BrightLocal 2023). Bundles and loyalty programs raise perceived value and can recover margin pressure.

Children’s fickle tastes

Children’s preferences shift rapidly with trends and peer influence, causing demand spikes and rapid fade-outs that complicate forecasting and inventory planning; Alpha Group must absorb high SKU churn and shorter selling windows in 2024. Buyers exploit this volatility to negotiate shorter commitments and lower minimums, while fast concept testing and agile supply chains reduce markdowns and shorten cash conversion cycles.

- High SKU churn

- Shorter purchase commitments

- Need for rapid testing

- Agile supply mitigates markdowns

Data-rich intermediaries

Retailers and platforms own granular sell-through and engagement data — Amazon held about 40% of US e-commerce in 2024 — and they leverage those insights to press suppliers on assortment and pricing, creating a marked information asymmetry that weakens Alpha Group’s negotiating stance.

- Data control: platforms capture transaction and behavioral signals at scale

- Negotiation leverage: retailers use analytics to demand price/promotional concessions

- Countermeasures: first-party apps and D2C channels build proprietary customer data to reduce asymmetry

Retail platforms concentrate leverage; D2C and rapid testing help toy brands regain pricing power

Retailers/platforms concentrate leverage (Amazon ~38% US e-commerce 2024; top 10 retailers ~60% US retail sales), extracting price/promotional concessions and data-driven terms. End buyers are value-driven in a $114B global toy market (2023), low switching costs compress pricing. D2C, multi-platform distribution and rapid testing partially restore bargaining balance.

| Metric | Value |

|---|---|

| Amazon share (US e‑commerce, 2024) | 38% |

| Top10 retailers share (US retail) | ~60% |

| Global toy market (2023) | $114B |

Same Document Delivered

Alpha Group Porter's Five Forces Analysis

This preview shows the exact Alpha Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written and ready for download and use the moment you buy. You're previewing the final deliverable: the same complete file available instantly after payment.

A Must-Have Tool for Decision-Makers

Alpha Group’s Porter’s Five Forces snapshot highlights intense rivalry, moderate supplier power, rising substitute threats, constrained buyer leverage, and significant barriers for new entrants that shape profitability. These forces map strategic vulnerabilities and growth levers critical for investors and managers. This brief whets the appetite—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy. Purchase the complete report to inform smarter decisions.

Suppliers Bargaining Power

Concentrated OEMs

Alpha Group depends on contract manufacturers in China and Southeast Asia; as of 2024 China accounted for roughly two-thirds of global toy production, concentrating high-quality, safety-compliant OEM capacity. This concentration gives top-tier suppliers leverage over lead times and minimum order quantities, especially for licensed SKUs. Long-standing relationships and consolidated volume purchases help Alpha mitigate direct price pressure and secure capacity.

Specialized creative talent

Specialized creative talent—animators, writers, voice actors and showrunners with proven kids’ hits—are scarce, letting star creators and premium studios extract favorable fees, schedules and back-end participation; top showrunners can command six-figure per-episode fees. The 2023 BLS median wage for animators was $78,790 and localization demand rose with global streaming rollouts. In-house pipelines reduce but do not eliminate this supplier power.

Raw material volatility

Plastics (ABS/PP), resins, electronics and packaging inputs are tightly tied to petrochemical and commodity cycles—Brent crude averaged about 86 USD/bbl in 2024—so suppliers routinely pass cost spikes through, squeezing OEM margins. Tooling and molds demand significant upfront supplier investment, raising dependency and switching costs. Hedging and multi-year contracts mitigate but do not eliminate price volatility.

Licensing and tech stack

- Switching cost: entrenched tool ecosystems

- Cloud share 2024: AWS ~32% / Azure ~23% / Google ~10%

- Peak pressure: traffic surges >3x in 2024

- Mitigation: proprietary stack = reduced vendor risk but high CapEx/time

Logistics and compliance

Global shipping, customs brokers and testing labs (EN71, ASTM, CCC) are essential inputs for Alpha Group; 2024 global container throughput is ~790m TEU, keeping ocean capacity tight and spot volatility elevated. Tight holiday calendars and port congestion (avg. vessel delay up to 2–4 days in major hubs in 2024) strengthen logistics providers’ negotiating position. Compliance labs add fixed costs and 4–8 week lead times, creating schedule risk, while preferred-partner programs trade 5–15% price concessions for forecasted volume certainty.

- Essential: global shipping, customs brokers, testing labs

- 2024 throughput: ~790m TEU; port delays 2–4 days

- Compliance: 4–8 week lab lead times; certification costs vary

- Mitigation: preferred-partner programs yield 5–15% price relief

Supplier concentration, talent premium squeeze margins; deals save 5–15%

Alpha faces concentrated OEM power (China ≈66% of toy production in 2024) and high switching costs for tooling and lead times, limiting price flexibility. Creative talent and specialized studios command premium fees (animator median wage $78,790 in 2023/2024), while cloud and logistics concentration (AWS 32%/Azure 23%/GCP 10%; 790m TEU, 2–4d delays) sustain supplier leverage. Multi-year contracts, hedges and preferred-partner programs (5–15% price relief) partially mitigate risk.

| Supplier | Key metric (2024) |

|---|---|

| OEMs | China ≈66% toy production |

| Cloud | AWS 32% / Azure 23% / GCP 10% |

| Shipping | 790m TEU, delays 2–4 days |

| Talent | Animator median $78,790 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Alpha Group. Evaluates supplier and buyer power, substitutes, and new-entrant threats to clarify pricing, profitability, and strategic defenses.

A single-sheet Alpha Group Porter's Five Forces summary unpacks competitive pressures for fast strategic decisions; customizable force levels and an instant radar chart let you model scenarios, swap in your data, and drop clean visuals straight into decks.

Customers Bargaining Power

Retailer consolidation

Mass merchants and e-commerce platforms dominate shelf and search visibility—Amazon held about 38% of US e-commerce sales in 2024 and the top 10 retailers comprised roughly 60% of US retail sales, concentrating negotiating power. Large accounts routinely extract lower prices, co-op funding and flexible returns, pressuring margins. Delisting risk forces additional concessions as shelf space tightens. Expanding into D2C and specialty channels cuts dependence and recaptures margin.

Platform gatekeepers

Streaming platforms negotiate licensing fees and windowing with dominant players like Netflix (~260 million subscribers in 2024) and YouTube (2+ billion monthly users) setting market terms.

Algorithmic promotion accounts for roughly 70% of discovery/viewing, materially shaping franchise visibility and downstream toy demand.

Platforms leverage granular viewer data to demand exclusivity and tougher revenue splits, while multi-platform distribution (streaming, linear, retail) can restore negotiating balance.

Price-sensitive parents

Price-sensitive parents in a $114 billion global toy market (2023, Statista) face abundant alternatives so end buyers are value-driven and switching costs are low, compressing pricing power. Online reviews and social proof sway demand rapidly—over 90% consult reviews before buying (BrightLocal 2023). Bundles and loyalty programs raise perceived value and can recover margin pressure.

Children’s fickle tastes

Children’s preferences shift rapidly with trends and peer influence, causing demand spikes and rapid fade-outs that complicate forecasting and inventory planning; Alpha Group must absorb high SKU churn and shorter selling windows in 2024. Buyers exploit this volatility to negotiate shorter commitments and lower minimums, while fast concept testing and agile supply chains reduce markdowns and shorten cash conversion cycles.

- High SKU churn

- Shorter purchase commitments

- Need for rapid testing

- Agile supply mitigates markdowns

Data-rich intermediaries

Retailers and platforms own granular sell-through and engagement data — Amazon held about 40% of US e-commerce in 2024 — and they leverage those insights to press suppliers on assortment and pricing, creating a marked information asymmetry that weakens Alpha Group’s negotiating stance.

- Data control: platforms capture transaction and behavioral signals at scale

- Negotiation leverage: retailers use analytics to demand price/promotional concessions

- Countermeasures: first-party apps and D2C channels build proprietary customer data to reduce asymmetry

Retail platforms concentrate leverage; D2C and rapid testing help toy brands regain pricing power

Retailers/platforms concentrate leverage (Amazon ~38% US e-commerce 2024; top 10 retailers ~60% US retail sales), extracting price/promotional concessions and data-driven terms. End buyers are value-driven in a $114B global toy market (2023), low switching costs compress pricing. D2C, multi-platform distribution and rapid testing partially restore bargaining balance.

| Metric | Value |

|---|---|

| Amazon share (US e‑commerce, 2024) | 38% |

| Top10 retailers share (US retail) | ~60% |

| Global toy market (2023) | $114B |

Same Document Delivered

Alpha Group Porter's Five Forces Analysis

This preview shows the exact Alpha Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written and ready for download and use the moment you buy. You're previewing the final deliverable: the same complete file available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Alpha Group’s Porter’s Five Forces snapshot highlights intense rivalry, moderate supplier power, rising substitute threats, constrained buyer leverage, and significant barriers for new entrants that shape profitability. These forces map strategic vulnerabilities and growth levers critical for investors and managers. This brief whets the appetite—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy. Purchase the complete report to inform smarter decisions.

Suppliers Bargaining Power

Concentrated OEMs

Alpha Group depends on contract manufacturers in China and Southeast Asia; as of 2024 China accounted for roughly two-thirds of global toy production, concentrating high-quality, safety-compliant OEM capacity. This concentration gives top-tier suppliers leverage over lead times and minimum order quantities, especially for licensed SKUs. Long-standing relationships and consolidated volume purchases help Alpha mitigate direct price pressure and secure capacity.

Specialized creative talent

Specialized creative talent—animators, writers, voice actors and showrunners with proven kids’ hits—are scarce, letting star creators and premium studios extract favorable fees, schedules and back-end participation; top showrunners can command six-figure per-episode fees. The 2023 BLS median wage for animators was $78,790 and localization demand rose with global streaming rollouts. In-house pipelines reduce but do not eliminate this supplier power.

Raw material volatility

Plastics (ABS/PP), resins, electronics and packaging inputs are tightly tied to petrochemical and commodity cycles—Brent crude averaged about 86 USD/bbl in 2024—so suppliers routinely pass cost spikes through, squeezing OEM margins. Tooling and molds demand significant upfront supplier investment, raising dependency and switching costs. Hedging and multi-year contracts mitigate but do not eliminate price volatility.

Licensing and tech stack

- Switching cost: entrenched tool ecosystems

- Cloud share 2024: AWS ~32% / Azure ~23% / Google ~10%

- Peak pressure: traffic surges >3x in 2024

- Mitigation: proprietary stack = reduced vendor risk but high CapEx/time

Logistics and compliance

Global shipping, customs brokers and testing labs (EN71, ASTM, CCC) are essential inputs for Alpha Group; 2024 global container throughput is ~790m TEU, keeping ocean capacity tight and spot volatility elevated. Tight holiday calendars and port congestion (avg. vessel delay up to 2–4 days in major hubs in 2024) strengthen logistics providers’ negotiating position. Compliance labs add fixed costs and 4–8 week lead times, creating schedule risk, while preferred-partner programs trade 5–15% price concessions for forecasted volume certainty.

- Essential: global shipping, customs brokers, testing labs

- 2024 throughput: ~790m TEU; port delays 2–4 days

- Compliance: 4–8 week lab lead times; certification costs vary

- Mitigation: preferred-partner programs yield 5–15% price relief

Supplier concentration, talent premium squeeze margins; deals save 5–15%

Alpha faces concentrated OEM power (China ≈66% of toy production in 2024) and high switching costs for tooling and lead times, limiting price flexibility. Creative talent and specialized studios command premium fees (animator median wage $78,790 in 2023/2024), while cloud and logistics concentration (AWS 32%/Azure 23%/GCP 10%; 790m TEU, 2–4d delays) sustain supplier leverage. Multi-year contracts, hedges and preferred-partner programs (5–15% price relief) partially mitigate risk.

| Supplier | Key metric (2024) |

|---|---|

| OEMs | China ≈66% toy production |

| Cloud | AWS 32% / Azure 23% / GCP 10% |

| Shipping | 790m TEU, delays 2–4 days |

| Talent | Animator median $78,790 |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Alpha Group. Evaluates supplier and buyer power, substitutes, and new-entrant threats to clarify pricing, profitability, and strategic defenses.

A single-sheet Alpha Group Porter's Five Forces summary unpacks competitive pressures for fast strategic decisions; customizable force levels and an instant radar chart let you model scenarios, swap in your data, and drop clean visuals straight into decks.

Customers Bargaining Power

Retailer consolidation

Mass merchants and e-commerce platforms dominate shelf and search visibility—Amazon held about 38% of US e-commerce sales in 2024 and the top 10 retailers comprised roughly 60% of US retail sales, concentrating negotiating power. Large accounts routinely extract lower prices, co-op funding and flexible returns, pressuring margins. Delisting risk forces additional concessions as shelf space tightens. Expanding into D2C and specialty channels cuts dependence and recaptures margin.

Platform gatekeepers

Streaming platforms negotiate licensing fees and windowing with dominant players like Netflix (~260 million subscribers in 2024) and YouTube (2+ billion monthly users) setting market terms.

Algorithmic promotion accounts for roughly 70% of discovery/viewing, materially shaping franchise visibility and downstream toy demand.

Platforms leverage granular viewer data to demand exclusivity and tougher revenue splits, while multi-platform distribution (streaming, linear, retail) can restore negotiating balance.

Price-sensitive parents

Price-sensitive parents in a $114 billion global toy market (2023, Statista) face abundant alternatives so end buyers are value-driven and switching costs are low, compressing pricing power. Online reviews and social proof sway demand rapidly—over 90% consult reviews before buying (BrightLocal 2023). Bundles and loyalty programs raise perceived value and can recover margin pressure.

Children’s fickle tastes

Children’s preferences shift rapidly with trends and peer influence, causing demand spikes and rapid fade-outs that complicate forecasting and inventory planning; Alpha Group must absorb high SKU churn and shorter selling windows in 2024. Buyers exploit this volatility to negotiate shorter commitments and lower minimums, while fast concept testing and agile supply chains reduce markdowns and shorten cash conversion cycles.

- High SKU churn

- Shorter purchase commitments

- Need for rapid testing

- Agile supply mitigates markdowns

Data-rich intermediaries

Retailers and platforms own granular sell-through and engagement data — Amazon held about 40% of US e-commerce in 2024 — and they leverage those insights to press suppliers on assortment and pricing, creating a marked information asymmetry that weakens Alpha Group’s negotiating stance.

- Data control: platforms capture transaction and behavioral signals at scale

- Negotiation leverage: retailers use analytics to demand price/promotional concessions

- Countermeasures: first-party apps and D2C channels build proprietary customer data to reduce asymmetry

Retail platforms concentrate leverage; D2C and rapid testing help toy brands regain pricing power

Retailers/platforms concentrate leverage (Amazon ~38% US e-commerce 2024; top 10 retailers ~60% US retail sales), extracting price/promotional concessions and data-driven terms. End buyers are value-driven in a $114B global toy market (2023), low switching costs compress pricing. D2C, multi-platform distribution and rapid testing partially restore bargaining balance.

| Metric | Value |

|---|---|

| Amazon share (US e‑commerce, 2024) | 38% |

| Top10 retailers share (US retail) | ~60% |

| Global toy market (2023) | $114B |

Same Document Delivered

Alpha Group Porter's Five Forces Analysis

This preview shows the exact Alpha Group Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written and ready for download and use the moment you buy. You're previewing the final deliverable: the same complete file available instantly after payment.