Guangdong Construction Engineering Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

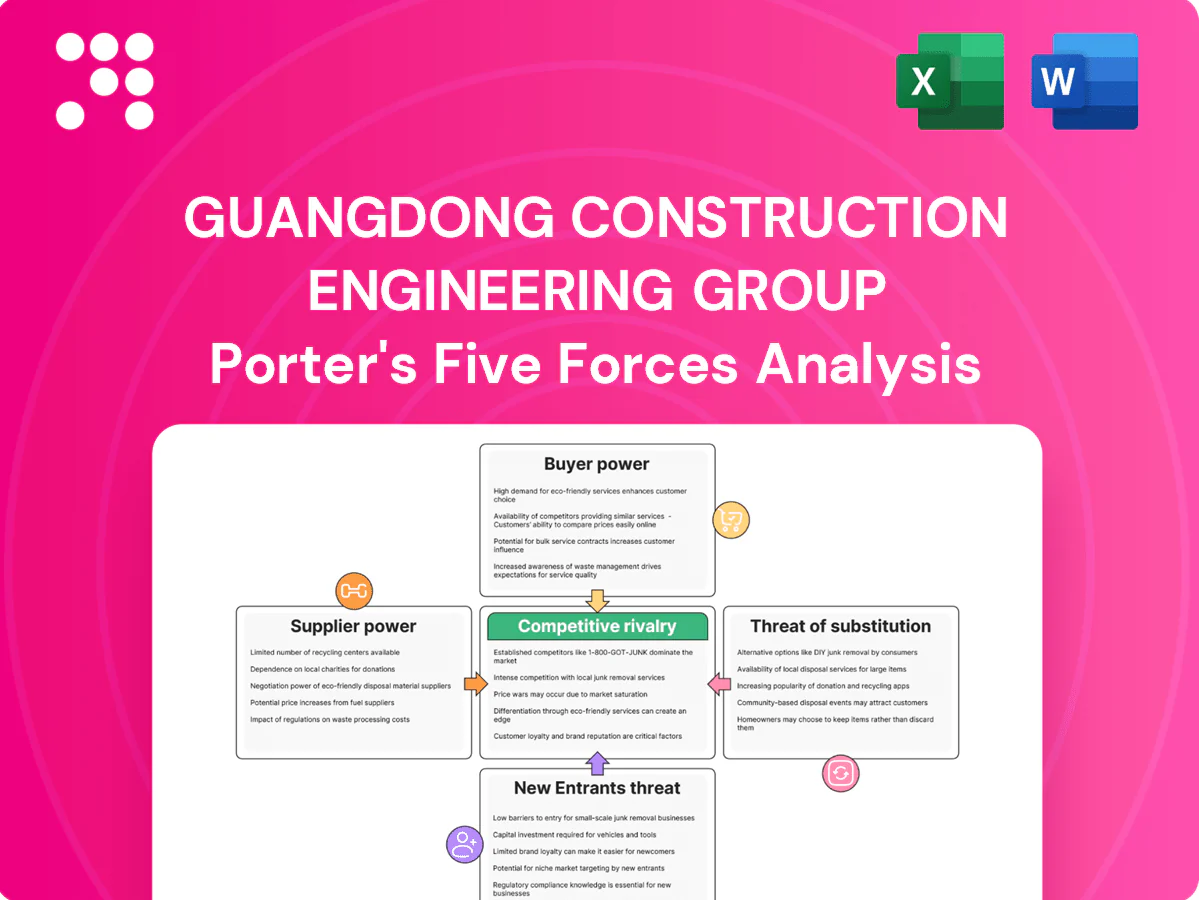

Guangdong Construction Engineering Group faces moderate buyer power, high supplier specialization in materials and equipment, intense rivalry among large contractors, modest threat from new entrants due to scale requirements, and emerging substitute pressures from design-build innovations. This brief snapshot highlights key competitive dynamics and strategic risks. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement and asphalt suppliers are relatively concentrated in China—China produced about 1.02 billion tonnes of crude steel and roughly 2.2 billion tonnes of cement in 2023—giving suppliers pricing influence in upcycles. Guangdong Construction can mitigate through bulk procurement and SOE purchasing alliances to secure volume discounts. Commodity volatility can pass to fixed-price projects; index-linked contract clauses and hedging reduce exposure and stabilize margins.

Equipment and tech OEMs

Heavy machinery and specialized equipment (TBMs, cranes) are sourced from a handful of OEMs—top suppliers account for roughly 70% of the market—giving suppliers leverage. Long-term leases and maintenance contracts (commonly 3–7 years) lock in costs and service terms. The firm’s scale supports multi-vendor sourcing, but switching can cause weeks of downtime and training costs often 1–2% of equipment value. 2024 localization rules pushed domestic OEM share in state projects to about 60%

Skilled subcontractors

EP, facade and specialty subcontractors can exert outsized leverage on Guangdong Construction Engineering Group on complex port and infrastructure projects, driving schedule risk and higher costs; Guangdong reported a GDP of about 13.63 trillion CNY in 2023, underscoring project scale and demand pressure. Capacity tightness in peak cycles raises rates and delays. Framework agreements and prequalification pools stabilize supply and performance. Payment discipline and milestone-based releases align incentives and reduce disputes.

Regulatory and utility gatekeepers

Permitting bodies and utilities function as non-traditional suppliers of access, with connection approvals routinely adding months to timelines and raising project costs by an estimated 1–4% on large infrastructure jobs in China in 2024. As a state-owned enterprise, Guangdong Construction Engineering Group gains coordination advantages with provincial agencies but remains exposed to procedural rigidity and standard audit cycles. Early engagement and documented compliance reduced bottlenecks on recent provincial projects.

- Permit delays: months

- Cost impact: 1–4%

- SOE advantage: stronger coordination

- Mitigation: early engagement, compliance excellence

Materials innovation and standards

Adoption of prefabrication and low-carbon materials shifts Guangdong Construction Engineering Group’s supplier mix toward specialized manufacturers, reducing commodity spend but raising strategic dependence on certified providers; China’s coastal pilots since 2022 accelerated low-carbon material use aligned with national carbon goals. Proprietary systems from few vendors can increase lock-in, while co-developing specs and approving multiple equivalents preserves leverage. Internal testing labs and BIM libraries cut lead times and enable faster supplier substitution.

- prefab/low-carbon shift: lowers commodity but ups specialist reliance

- proprietary systems: risk of vendor lock-in

- co-development: preserves bargaining power

- internal labs/BIM: enable rapid substitution

China scale lifts supplier power; state OEM ~60%, permits add 1-4% cost

Supplier power is moderate‑high: China produced ~1.02bn t steel and ~2.2bn t cement in 2023, with 2024 state‑project domestic OEM share ~60%, enabling price influence in upcycles. Permit/utility delays add ~1–4% cost and months of delay. Mitigants: bulk SOE procurement, index‑linked contracts, prequalified pools.

| Tag | Metric | Value |

|---|---|---|

| Steel/Cement | 2023 output | 1.02bn t / 2.2bn t |

| OEM share | 2024 state projects | ~60% |

| Permit impact | Cost | 1–4% |

What is included in the product

Tailored Porter's Five Forces analysis for Guangdong Construction Engineering Group uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, market positioning and risk mitigation.

A concise Porter's Five Forces one-sheet for Guangdong Construction Engineering Group that visualizes competitive pressure with an editable spider chart—ideal for quick strategy decisions, pitch decks, or board slides and easily updated as market or regulatory conditions change.

Customers Bargaining Power

Government owners dominate

In 2024 public-sector agencies remained the primary source of large infrastructure tenders in Guangdong, using competitive bidding to enforce strict technical specifications, price compression and extended payment terms. As a state-owned enterprise the group secures awards by aligning with provincial policy priorities but faces heightened compliance and audit requirements. Historical performance metrics and delivery records are decisive for repeat awards and contract scale.

Developers and industrial clients

Private developers and industrial clients pit bids on cost, schedule and turnkey capability, frequently demanding EPC/design-build and warranties that shift execution risk to contractors. Bundling property management can raise project value but expands scope and liabilities. Repeat-client frameworks now represent about 50% of province-level project volume in Guangdong, which helps smooth margin volatility. Strong buyer bargaining keeps margins under pressure.

Price transparency in tenders

Open bidding platforms in Guangdong standardize pricing and documentation, compressing evaluation spreads to about 1–3 points in many 2024 tenders and increasing buyer leverage on price and penalties. Narrow score differentials force contractors to compete mainly on price, while differentiation through BIM, safety records and green certifications can command modest premiums of roughly 2–5%. Strict bid/no-bid discipline on high-risk packages helps Guangdong Construction Engineering Group protect margins and avoid penalty exposure.

Payment and retention terms

Owners use retention (commonly 5–10% in 2024), liquidated‑damages clauses (typical 0.03–0.05% of contract value per day) and milestone gating to control contractors; these mechanisms amplify cash‑flow pressure on long‑duration infrastructure contracts. Strong balance sheets and non‑recourse/project financing reduce dependency on early cash releases. Prompt payment compliance policies materially shorten receivables and lower DSO.

- Retention: 5–10% (2024)

- Liquidated damages: ~0.03–0.05%/day

- DSO pressure: long projects often 90–180 days

- Mitigation: strong balance sheet, project finance, prompt payment policies

Quality and ESG requirements

Buyers compress spreads to 1–3 pts; repeat clients ~50%; ESG adds 2–5% premium

Buyers (public and private) exert high leverage in 2024: standardized open bidding compresses spreads to 1–3 pts, repeat clients account for ~50% of provincial volume, and retention/LDs (5–10%; 0.03–0.05%/day) tighten contractor cash flow. ESG and digital capabilities provide 2–5% premium but raise compliance costs, keeping margins under pressure.

| Metric | 2024 Value |

|---|---|

| Bid spread | 1–3 pts |

| Repeat share | ~50% |

| Retention | 5–10% |

| Liquidated damages | 0.03–0.05%/day |

| DSO (long projects) | 90–180 days |

| ESG premium | 2–5% |

Preview Before You Purchase

Guangdong Construction Engineering Group Porter's Five Forces Analysis

This preview shows the exact Guangdong Construction Engineering Group Porter’s Five Forces analysis you’ll receive—comprehensive, professionally formatted, and ready for use. It includes industry rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic implications. No placeholders or mockups. Purchase grants immediate access to this identical file.

A Must-Have Tool for Decision-Makers

Guangdong Construction Engineering Group faces moderate buyer power, high supplier specialization in materials and equipment, intense rivalry among large contractors, modest threat from new entrants due to scale requirements, and emerging substitute pressures from design-build innovations. This brief snapshot highlights key competitive dynamics and strategic risks. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement and asphalt suppliers are relatively concentrated in China—China produced about 1.02 billion tonnes of crude steel and roughly 2.2 billion tonnes of cement in 2023—giving suppliers pricing influence in upcycles. Guangdong Construction can mitigate through bulk procurement and SOE purchasing alliances to secure volume discounts. Commodity volatility can pass to fixed-price projects; index-linked contract clauses and hedging reduce exposure and stabilize margins.

Equipment and tech OEMs

Heavy machinery and specialized equipment (TBMs, cranes) are sourced from a handful of OEMs—top suppliers account for roughly 70% of the market—giving suppliers leverage. Long-term leases and maintenance contracts (commonly 3–7 years) lock in costs and service terms. The firm’s scale supports multi-vendor sourcing, but switching can cause weeks of downtime and training costs often 1–2% of equipment value. 2024 localization rules pushed domestic OEM share in state projects to about 60%

Skilled subcontractors

EP, facade and specialty subcontractors can exert outsized leverage on Guangdong Construction Engineering Group on complex port and infrastructure projects, driving schedule risk and higher costs; Guangdong reported a GDP of about 13.63 trillion CNY in 2023, underscoring project scale and demand pressure. Capacity tightness in peak cycles raises rates and delays. Framework agreements and prequalification pools stabilize supply and performance. Payment discipline and milestone-based releases align incentives and reduce disputes.

Regulatory and utility gatekeepers

Permitting bodies and utilities function as non-traditional suppliers of access, with connection approvals routinely adding months to timelines and raising project costs by an estimated 1–4% on large infrastructure jobs in China in 2024. As a state-owned enterprise, Guangdong Construction Engineering Group gains coordination advantages with provincial agencies but remains exposed to procedural rigidity and standard audit cycles. Early engagement and documented compliance reduced bottlenecks on recent provincial projects.

- Permit delays: months

- Cost impact: 1–4%

- SOE advantage: stronger coordination

- Mitigation: early engagement, compliance excellence

Materials innovation and standards

Adoption of prefabrication and low-carbon materials shifts Guangdong Construction Engineering Group’s supplier mix toward specialized manufacturers, reducing commodity spend but raising strategic dependence on certified providers; China’s coastal pilots since 2022 accelerated low-carbon material use aligned with national carbon goals. Proprietary systems from few vendors can increase lock-in, while co-developing specs and approving multiple equivalents preserves leverage. Internal testing labs and BIM libraries cut lead times and enable faster supplier substitution.

- prefab/low-carbon shift: lowers commodity but ups specialist reliance

- proprietary systems: risk of vendor lock-in

- co-development: preserves bargaining power

- internal labs/BIM: enable rapid substitution

China scale lifts supplier power; state OEM ~60%, permits add 1-4% cost

Supplier power is moderate‑high: China produced ~1.02bn t steel and ~2.2bn t cement in 2023, with 2024 state‑project domestic OEM share ~60%, enabling price influence in upcycles. Permit/utility delays add ~1–4% cost and months of delay. Mitigants: bulk SOE procurement, index‑linked contracts, prequalified pools.

| Tag | Metric | Value |

|---|---|---|

| Steel/Cement | 2023 output | 1.02bn t / 2.2bn t |

| OEM share | 2024 state projects | ~60% |

| Permit impact | Cost | 1–4% |

What is included in the product

Tailored Porter's Five Forces analysis for Guangdong Construction Engineering Group uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, market positioning and risk mitigation.

A concise Porter's Five Forces one-sheet for Guangdong Construction Engineering Group that visualizes competitive pressure with an editable spider chart—ideal for quick strategy decisions, pitch decks, or board slides and easily updated as market or regulatory conditions change.

Customers Bargaining Power

Government owners dominate

In 2024 public-sector agencies remained the primary source of large infrastructure tenders in Guangdong, using competitive bidding to enforce strict technical specifications, price compression and extended payment terms. As a state-owned enterprise the group secures awards by aligning with provincial policy priorities but faces heightened compliance and audit requirements. Historical performance metrics and delivery records are decisive for repeat awards and contract scale.

Developers and industrial clients

Private developers and industrial clients pit bids on cost, schedule and turnkey capability, frequently demanding EPC/design-build and warranties that shift execution risk to contractors. Bundling property management can raise project value but expands scope and liabilities. Repeat-client frameworks now represent about 50% of province-level project volume in Guangdong, which helps smooth margin volatility. Strong buyer bargaining keeps margins under pressure.

Price transparency in tenders

Open bidding platforms in Guangdong standardize pricing and documentation, compressing evaluation spreads to about 1–3 points in many 2024 tenders and increasing buyer leverage on price and penalties. Narrow score differentials force contractors to compete mainly on price, while differentiation through BIM, safety records and green certifications can command modest premiums of roughly 2–5%. Strict bid/no-bid discipline on high-risk packages helps Guangdong Construction Engineering Group protect margins and avoid penalty exposure.

Payment and retention terms

Owners use retention (commonly 5–10% in 2024), liquidated‑damages clauses (typical 0.03–0.05% of contract value per day) and milestone gating to control contractors; these mechanisms amplify cash‑flow pressure on long‑duration infrastructure contracts. Strong balance sheets and non‑recourse/project financing reduce dependency on early cash releases. Prompt payment compliance policies materially shorten receivables and lower DSO.

- Retention: 5–10% (2024)

- Liquidated damages: ~0.03–0.05%/day

- DSO pressure: long projects often 90–180 days

- Mitigation: strong balance sheet, project finance, prompt payment policies

Quality and ESG requirements

Buyers compress spreads to 1–3 pts; repeat clients ~50%; ESG adds 2–5% premium

Buyers (public and private) exert high leverage in 2024: standardized open bidding compresses spreads to 1–3 pts, repeat clients account for ~50% of provincial volume, and retention/LDs (5–10%; 0.03–0.05%/day) tighten contractor cash flow. ESG and digital capabilities provide 2–5% premium but raise compliance costs, keeping margins under pressure.

| Metric | 2024 Value |

|---|---|

| Bid spread | 1–3 pts |

| Repeat share | ~50% |

| Retention | 5–10% |

| Liquidated damages | 0.03–0.05%/day |

| DSO (long projects) | 90–180 days |

| ESG premium | 2–5% |

Preview Before You Purchase

Guangdong Construction Engineering Group Porter's Five Forces Analysis

This preview shows the exact Guangdong Construction Engineering Group Porter’s Five Forces analysis you’ll receive—comprehensive, professionally formatted, and ready for use. It includes industry rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic implications. No placeholders or mockups. Purchase grants immediate access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Guangdong Construction Engineering Group faces moderate buyer power, high supplier specialization in materials and equipment, intense rivalry among large contractors, modest threat from new entrants due to scale requirements, and emerging substitute pressures from design-build innovations. This brief snapshot highlights key competitive dynamics and strategic risks. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated core materials

Steel, cement and asphalt suppliers are relatively concentrated in China—China produced about 1.02 billion tonnes of crude steel and roughly 2.2 billion tonnes of cement in 2023—giving suppliers pricing influence in upcycles. Guangdong Construction can mitigate through bulk procurement and SOE purchasing alliances to secure volume discounts. Commodity volatility can pass to fixed-price projects; index-linked contract clauses and hedging reduce exposure and stabilize margins.

Equipment and tech OEMs

Heavy machinery and specialized equipment (TBMs, cranes) are sourced from a handful of OEMs—top suppliers account for roughly 70% of the market—giving suppliers leverage. Long-term leases and maintenance contracts (commonly 3–7 years) lock in costs and service terms. The firm’s scale supports multi-vendor sourcing, but switching can cause weeks of downtime and training costs often 1–2% of equipment value. 2024 localization rules pushed domestic OEM share in state projects to about 60%

Skilled subcontractors

EP, facade and specialty subcontractors can exert outsized leverage on Guangdong Construction Engineering Group on complex port and infrastructure projects, driving schedule risk and higher costs; Guangdong reported a GDP of about 13.63 trillion CNY in 2023, underscoring project scale and demand pressure. Capacity tightness in peak cycles raises rates and delays. Framework agreements and prequalification pools stabilize supply and performance. Payment discipline and milestone-based releases align incentives and reduce disputes.

Regulatory and utility gatekeepers

Permitting bodies and utilities function as non-traditional suppliers of access, with connection approvals routinely adding months to timelines and raising project costs by an estimated 1–4% on large infrastructure jobs in China in 2024. As a state-owned enterprise, Guangdong Construction Engineering Group gains coordination advantages with provincial agencies but remains exposed to procedural rigidity and standard audit cycles. Early engagement and documented compliance reduced bottlenecks on recent provincial projects.

- Permit delays: months

- Cost impact: 1–4%

- SOE advantage: stronger coordination

- Mitigation: early engagement, compliance excellence

Materials innovation and standards

Adoption of prefabrication and low-carbon materials shifts Guangdong Construction Engineering Group’s supplier mix toward specialized manufacturers, reducing commodity spend but raising strategic dependence on certified providers; China’s coastal pilots since 2022 accelerated low-carbon material use aligned with national carbon goals. Proprietary systems from few vendors can increase lock-in, while co-developing specs and approving multiple equivalents preserves leverage. Internal testing labs and BIM libraries cut lead times and enable faster supplier substitution.

- prefab/low-carbon shift: lowers commodity but ups specialist reliance

- proprietary systems: risk of vendor lock-in

- co-development: preserves bargaining power

- internal labs/BIM: enable rapid substitution

China scale lifts supplier power; state OEM ~60%, permits add 1-4% cost

Supplier power is moderate‑high: China produced ~1.02bn t steel and ~2.2bn t cement in 2023, with 2024 state‑project domestic OEM share ~60%, enabling price influence in upcycles. Permit/utility delays add ~1–4% cost and months of delay. Mitigants: bulk SOE procurement, index‑linked contracts, prequalified pools.

| Tag | Metric | Value |

|---|---|---|

| Steel/Cement | 2023 output | 1.02bn t / 2.2bn t |

| OEM share | 2024 state projects | ~60% |

| Permit impact | Cost | 1–4% |

What is included in the product

Tailored Porter's Five Forces analysis for Guangdong Construction Engineering Group uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, market positioning and risk mitigation.

A concise Porter's Five Forces one-sheet for Guangdong Construction Engineering Group that visualizes competitive pressure with an editable spider chart—ideal for quick strategy decisions, pitch decks, or board slides and easily updated as market or regulatory conditions change.

Customers Bargaining Power

Government owners dominate

In 2024 public-sector agencies remained the primary source of large infrastructure tenders in Guangdong, using competitive bidding to enforce strict technical specifications, price compression and extended payment terms. As a state-owned enterprise the group secures awards by aligning with provincial policy priorities but faces heightened compliance and audit requirements. Historical performance metrics and delivery records are decisive for repeat awards and contract scale.

Developers and industrial clients

Private developers and industrial clients pit bids on cost, schedule and turnkey capability, frequently demanding EPC/design-build and warranties that shift execution risk to contractors. Bundling property management can raise project value but expands scope and liabilities. Repeat-client frameworks now represent about 50% of province-level project volume in Guangdong, which helps smooth margin volatility. Strong buyer bargaining keeps margins under pressure.

Price transparency in tenders

Open bidding platforms in Guangdong standardize pricing and documentation, compressing evaluation spreads to about 1–3 points in many 2024 tenders and increasing buyer leverage on price and penalties. Narrow score differentials force contractors to compete mainly on price, while differentiation through BIM, safety records and green certifications can command modest premiums of roughly 2–5%. Strict bid/no-bid discipline on high-risk packages helps Guangdong Construction Engineering Group protect margins and avoid penalty exposure.

Payment and retention terms

Owners use retention (commonly 5–10% in 2024), liquidated‑damages clauses (typical 0.03–0.05% of contract value per day) and milestone gating to control contractors; these mechanisms amplify cash‑flow pressure on long‑duration infrastructure contracts. Strong balance sheets and non‑recourse/project financing reduce dependency on early cash releases. Prompt payment compliance policies materially shorten receivables and lower DSO.

- Retention: 5–10% (2024)

- Liquidated damages: ~0.03–0.05%/day

- DSO pressure: long projects often 90–180 days

- Mitigation: strong balance sheet, project finance, prompt payment policies

Quality and ESG requirements

Buyers compress spreads to 1–3 pts; repeat clients ~50%; ESG adds 2–5% premium

Buyers (public and private) exert high leverage in 2024: standardized open bidding compresses spreads to 1–3 pts, repeat clients account for ~50% of provincial volume, and retention/LDs (5–10%; 0.03–0.05%/day) tighten contractor cash flow. ESG and digital capabilities provide 2–5% premium but raise compliance costs, keeping margins under pressure.

| Metric | 2024 Value |

|---|---|

| Bid spread | 1–3 pts |

| Repeat share | ~50% |

| Retention | 5–10% |

| Liquidated damages | 0.03–0.05%/day |

| DSO (long projects) | 90–180 days |

| ESG premium | 2–5% |

Preview Before You Purchase

Guangdong Construction Engineering Group Porter's Five Forces Analysis

This preview shows the exact Guangdong Construction Engineering Group Porter’s Five Forces analysis you’ll receive—comprehensive, professionally formatted, and ready for use. It includes industry rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic implications. No placeholders or mockups. Purchase grants immediate access to this identical file.