Gee Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

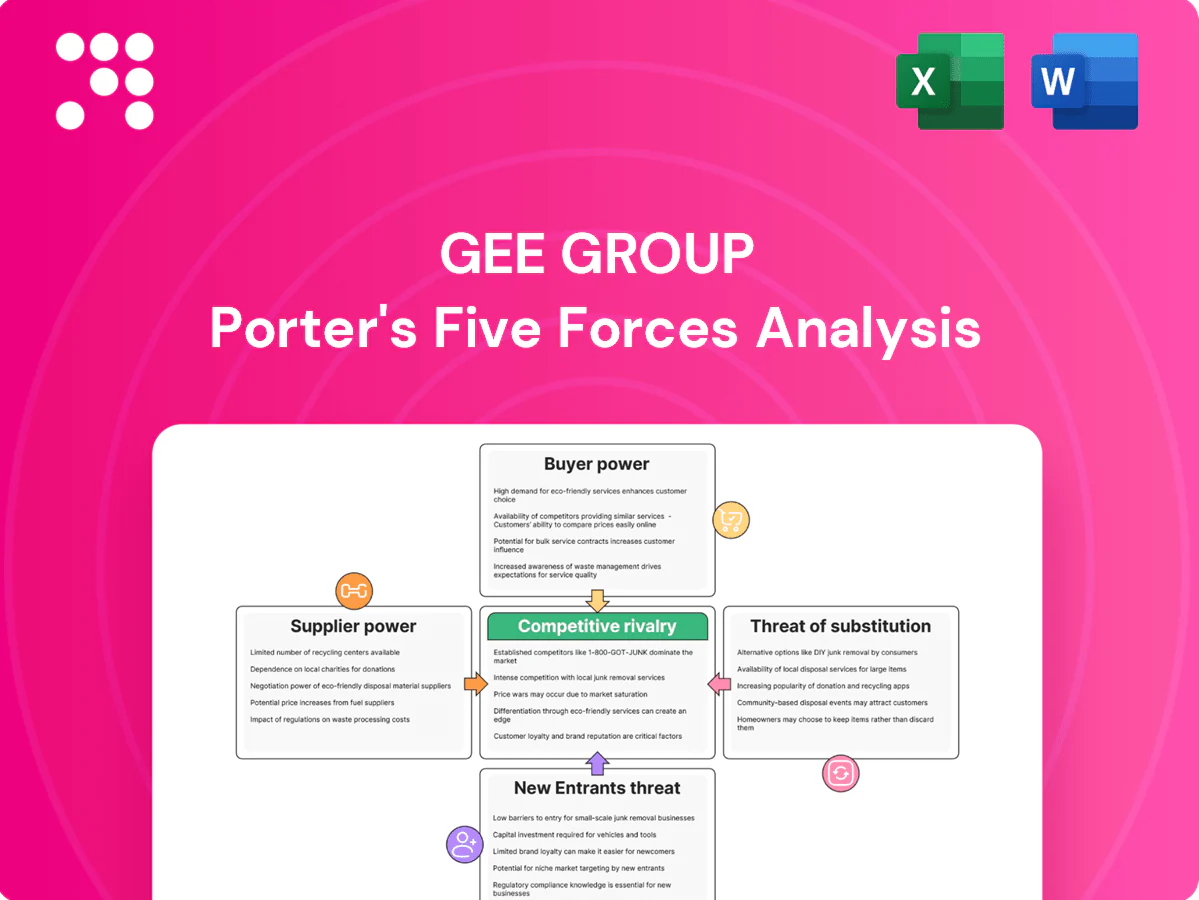

Gee Group faces moderate buyer power, fragmented suppliers, niche substitutes, regulatory entry barriers and heated rivalry—this snapshot highlights core dynamics shaping its margins and strategy. The full Porter's Five Forces Analysis decodes force-by-force intensity, visual ratings and tailored strategic implications for Gee Group. Unlock the complete report to inform smarter investment and business decisions.

Suppliers Bargaining Power

Scarce high-skill talent

In 2024 specialized IT, engineering and healthcare candidates remain scarce, driving 15–30% pay premiums and tighter fill rates as vacancy-to-application ratios decline; supplier power increases materially. GEE Group must proactively court passive talent—roughly 70% of the workforce—and market compelling assignments to win hires. Wage inflation risk in hot niches shows annual pay growth of about 6–12%, pressuring margins.

General labor abundance

Industrial and office support roles access large candidate pools, reducing supplier power; UK unemployment was about 4.2% in 2024, keeping labor relatively available. Local unemployment and seasonal peaks still cause short-term tightness. Rapid sourcing and temp pools offset churn, while continuous pay-rate benchmarking preserves margins.

Credentialing and licensing

Healthcare and specialized engineering roles often require strict certifications; BLS data shows registered nurses had a median annual wage of $81,220 (May 2023), underscoring wage leverage for credentialed staff. Candidates with scarce credentials command pay and contractual leverage, compressing agency margins. Compliance, credentialing and credential transfer can add 4–8 weeks to time-to-start and raise per-hire costs, constraining supply elasticity.

Platforms and intermediaries

Platforms like job boards, social networks and talent marketplaces — LinkedIn surpassed 1 billion members in 2024 — let candidates compare offers and market pay, strengthening supplier (candidate) bargaining power, while visible competing pay rates increase leverage. Agency curation and screening remain valued for quality and speed. Strong recruiter relationships and exclusive talent pools can mitigate platform-driven disintermediation.

- Platforms: candidate price discovery up, transparency rises

- Curation: agencies add screening value, preserve margins

- Recruiter ties: reduce risk of direct hire via marketplaces

Geography and remote work

Remote and hybrid models expand Gee Group’s talent pool beyond local scarcity, with 2024 platforms showing roughly 20% of global job ads listed remote/hybrid roles. Top remote talent faces national competition, keeping supplier power balanced; relocation barriers drop while compensation bands widen by role and market. Gee must tune sourcing, screening and pay frameworks to flexible work norms.

- 2024 remote/hybrid job ads ~20%

- National competition limits supplier leverage

- Wider compensation dispersion by market

- Require flexible sourcing and pay calibration

Specialist scarcity lifts pay 15–30%, fuels 6–12%

Specialized IT, healthcare and engineering scarcity drives 15–30% pay premiums and 6–12% annual pay growth in 2024, raising supplier power. Large pools for industrial/office roles and UK unemployment ~4.2% (2024) reduce leverage; temp pools and rapid sourcing mitigate churn. Platforms (LinkedIn 1bn members, 2024) and ~20% remote job ads increase transparency, while agency curation and recruiter ties preserve margins.

| Metric | Value |

|---|---|

| Specialist pay premium | 15–30% |

| Annual pay growth (hot niches) | 6–12% |

| UK unemployment (2024) | 4.2% |

| LinkedIn members (2024) | ~1,000,000,000 |

| Remote/hybrid job ads (2024) | ~20% |

| Credentialing delay | +4–8 weeks |

What is included in the product

Tailored Porter’s Five Forces analysis for Gee Group uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers that affect its pricing, margins and market position.

One-sheet Porter’s Five Forces for Gee Group—instantly spot competitive pressures and relieve strategic uncertainty with customizable force levels, a clean slide-ready layout, and no complex code so non-finance teams can act fast.

Customers Bargaining Power

Many alternatives

Clients can pick from global firms, regional specialists and boutiques, and with the global staffing market topping $500 billion in 2024 this abundant choice raises price sensitivity and switching behavior. Differentiation via speed, quality and vertical expertise is essential to retain contracts. Multi-sourcing by buyers—commonly splitting spends across 2–4 vendors—further compresses margins.

MSP/VMS procurement

MSP/VMS procurement standardizes rates and SLAs, increasing transparency and shrinking bargaining room; VMS now channels about 55% of contingent workforce spend (SIA 2024). Standardization shifts competition to service metrics, with fill-rate targets typically 80–90% and compliance scores above 90% driving renewals. Volume and steadier requisitions offset rate compression by improving utilization and revenue predictability.

Low switching costs

Low switching costs mean clients can trial multiple agencies with minimal lock-in, and a 2024 industry survey found about 42% of employers sampled tested two or more recruitment partners before committing. Poor performance therefore quickly loses desks—clients moved 28% of contingent spend year-on-year in some sectors in 2024. Strong referenceability and niche credibility mitigate churn, so contract terms must balance flexibility with margin protection.

Cyclical demand

Cyclical demand means hiring slows in downturns, amplifying buyer leverage on price and terms, while in expansions urgent hiring needs improve agency negotiating position; mid-2024 US unemployment around 4.1% highlighted softer hiring that boosted client bargaining power. Diversification across sectors and a shift toward contract-to-hire smooth revenue volatility and preserve margins versus pure direct-hire.

- Downturn: higher buyer leverage

- Expansion: urgent demand raises agency leverage

- Diversification smooths cycles

- Contract-to-hire = greater resilience

Outcome and compliance focus

Buyers in 2024 insist on fast time-to-fill, demonstrable quality and strict risk controls; in markets like Australia where unemployment was ~3.7% in 2024, speed and compliance drive supplier selection. Robust onboarding, background checks and safety programs build trust and reduce client churn. Data-backed performance reporting shifts competition away from price, while sector expertise secures 10–30% higher realized rates on specialist roles.

- Fast fills

- Compliance

- Data reporting

- Sector premium

Buyers dominate: $500B+, VMS 55%, 42% test partners

Buyers have strong leverage: global market >$500B (2024) and VMS channels ~55% of contingent spend, raising price transparency and switching. 42% of employers trial multiple agencies and some sectors saw 28% YoY spend moves in 2024, compressing margins; sector expertise can secure 10–30% rate premiums. Cyclical hiring (US unemployment ~4.1%, AU ~3.7% in 2024) shifts bargaining power with demand.

| Metric | 2024 Value |

|---|---|

| Global staffing market | $500B+ |

| VMS share | 55% |

| Employers testing partners | 42% |

| YoY spend moves (some sectors) | 28% |

| Sector rate premium | 10–30% |

| US unemployment | 4.1% |

| AU unemployment | 3.7% |

Preview the Actual Deliverable

Gee Group Porter's Five Forces Analysis

This preview shows the exact Gee Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, actionable, and ready for download the moment you buy. You're viewing the final deliverable, identical to the file you'll get instantly upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Gee Group faces moderate buyer power, fragmented suppliers, niche substitutes, regulatory entry barriers and heated rivalry—this snapshot highlights core dynamics shaping its margins and strategy. The full Porter's Five Forces Analysis decodes force-by-force intensity, visual ratings and tailored strategic implications for Gee Group. Unlock the complete report to inform smarter investment and business decisions.

Suppliers Bargaining Power

Scarce high-skill talent

In 2024 specialized IT, engineering and healthcare candidates remain scarce, driving 15–30% pay premiums and tighter fill rates as vacancy-to-application ratios decline; supplier power increases materially. GEE Group must proactively court passive talent—roughly 70% of the workforce—and market compelling assignments to win hires. Wage inflation risk in hot niches shows annual pay growth of about 6–12%, pressuring margins.

General labor abundance

Industrial and office support roles access large candidate pools, reducing supplier power; UK unemployment was about 4.2% in 2024, keeping labor relatively available. Local unemployment and seasonal peaks still cause short-term tightness. Rapid sourcing and temp pools offset churn, while continuous pay-rate benchmarking preserves margins.

Credentialing and licensing

Healthcare and specialized engineering roles often require strict certifications; BLS data shows registered nurses had a median annual wage of $81,220 (May 2023), underscoring wage leverage for credentialed staff. Candidates with scarce credentials command pay and contractual leverage, compressing agency margins. Compliance, credentialing and credential transfer can add 4–8 weeks to time-to-start and raise per-hire costs, constraining supply elasticity.

Platforms and intermediaries

Platforms like job boards, social networks and talent marketplaces — LinkedIn surpassed 1 billion members in 2024 — let candidates compare offers and market pay, strengthening supplier (candidate) bargaining power, while visible competing pay rates increase leverage. Agency curation and screening remain valued for quality and speed. Strong recruiter relationships and exclusive talent pools can mitigate platform-driven disintermediation.

- Platforms: candidate price discovery up, transparency rises

- Curation: agencies add screening value, preserve margins

- Recruiter ties: reduce risk of direct hire via marketplaces

Geography and remote work

Remote and hybrid models expand Gee Group’s talent pool beyond local scarcity, with 2024 platforms showing roughly 20% of global job ads listed remote/hybrid roles. Top remote talent faces national competition, keeping supplier power balanced; relocation barriers drop while compensation bands widen by role and market. Gee must tune sourcing, screening and pay frameworks to flexible work norms.

- 2024 remote/hybrid job ads ~20%

- National competition limits supplier leverage

- Wider compensation dispersion by market

- Require flexible sourcing and pay calibration

Specialist scarcity lifts pay 15–30%, fuels 6–12%

Specialized IT, healthcare and engineering scarcity drives 15–30% pay premiums and 6–12% annual pay growth in 2024, raising supplier power. Large pools for industrial/office roles and UK unemployment ~4.2% (2024) reduce leverage; temp pools and rapid sourcing mitigate churn. Platforms (LinkedIn 1bn members, 2024) and ~20% remote job ads increase transparency, while agency curation and recruiter ties preserve margins.

| Metric | Value |

|---|---|

| Specialist pay premium | 15–30% |

| Annual pay growth (hot niches) | 6–12% |

| UK unemployment (2024) | 4.2% |

| LinkedIn members (2024) | ~1,000,000,000 |

| Remote/hybrid job ads (2024) | ~20% |

| Credentialing delay | +4–8 weeks |

What is included in the product

Tailored Porter’s Five Forces analysis for Gee Group uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers that affect its pricing, margins and market position.

One-sheet Porter’s Five Forces for Gee Group—instantly spot competitive pressures and relieve strategic uncertainty with customizable force levels, a clean slide-ready layout, and no complex code so non-finance teams can act fast.

Customers Bargaining Power

Many alternatives

Clients can pick from global firms, regional specialists and boutiques, and with the global staffing market topping $500 billion in 2024 this abundant choice raises price sensitivity and switching behavior. Differentiation via speed, quality and vertical expertise is essential to retain contracts. Multi-sourcing by buyers—commonly splitting spends across 2–4 vendors—further compresses margins.

MSP/VMS procurement

MSP/VMS procurement standardizes rates and SLAs, increasing transparency and shrinking bargaining room; VMS now channels about 55% of contingent workforce spend (SIA 2024). Standardization shifts competition to service metrics, with fill-rate targets typically 80–90% and compliance scores above 90% driving renewals. Volume and steadier requisitions offset rate compression by improving utilization and revenue predictability.

Low switching costs

Low switching costs mean clients can trial multiple agencies with minimal lock-in, and a 2024 industry survey found about 42% of employers sampled tested two or more recruitment partners before committing. Poor performance therefore quickly loses desks—clients moved 28% of contingent spend year-on-year in some sectors in 2024. Strong referenceability and niche credibility mitigate churn, so contract terms must balance flexibility with margin protection.

Cyclical demand

Cyclical demand means hiring slows in downturns, amplifying buyer leverage on price and terms, while in expansions urgent hiring needs improve agency negotiating position; mid-2024 US unemployment around 4.1% highlighted softer hiring that boosted client bargaining power. Diversification across sectors and a shift toward contract-to-hire smooth revenue volatility and preserve margins versus pure direct-hire.

- Downturn: higher buyer leverage

- Expansion: urgent demand raises agency leverage

- Diversification smooths cycles

- Contract-to-hire = greater resilience

Outcome and compliance focus

Buyers in 2024 insist on fast time-to-fill, demonstrable quality and strict risk controls; in markets like Australia where unemployment was ~3.7% in 2024, speed and compliance drive supplier selection. Robust onboarding, background checks and safety programs build trust and reduce client churn. Data-backed performance reporting shifts competition away from price, while sector expertise secures 10–30% higher realized rates on specialist roles.

- Fast fills

- Compliance

- Data reporting

- Sector premium

Buyers dominate: $500B+, VMS 55%, 42% test partners

Buyers have strong leverage: global market >$500B (2024) and VMS channels ~55% of contingent spend, raising price transparency and switching. 42% of employers trial multiple agencies and some sectors saw 28% YoY spend moves in 2024, compressing margins; sector expertise can secure 10–30% rate premiums. Cyclical hiring (US unemployment ~4.1%, AU ~3.7% in 2024) shifts bargaining power with demand.

| Metric | 2024 Value |

|---|---|

| Global staffing market | $500B+ |

| VMS share | 55% |

| Employers testing partners | 42% |

| YoY spend moves (some sectors) | 28% |

| Sector rate premium | 10–30% |

| US unemployment | 4.1% |

| AU unemployment | 3.7% |

Preview the Actual Deliverable

Gee Group Porter's Five Forces Analysis

This preview shows the exact Gee Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, actionable, and ready for download the moment you buy. You're viewing the final deliverable, identical to the file you'll get instantly upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Gee Group faces moderate buyer power, fragmented suppliers, niche substitutes, regulatory entry barriers and heated rivalry—this snapshot highlights core dynamics shaping its margins and strategy. The full Porter's Five Forces Analysis decodes force-by-force intensity, visual ratings and tailored strategic implications for Gee Group. Unlock the complete report to inform smarter investment and business decisions.

Suppliers Bargaining Power

Scarce high-skill talent

In 2024 specialized IT, engineering and healthcare candidates remain scarce, driving 15–30% pay premiums and tighter fill rates as vacancy-to-application ratios decline; supplier power increases materially. GEE Group must proactively court passive talent—roughly 70% of the workforce—and market compelling assignments to win hires. Wage inflation risk in hot niches shows annual pay growth of about 6–12%, pressuring margins.

General labor abundance

Industrial and office support roles access large candidate pools, reducing supplier power; UK unemployment was about 4.2% in 2024, keeping labor relatively available. Local unemployment and seasonal peaks still cause short-term tightness. Rapid sourcing and temp pools offset churn, while continuous pay-rate benchmarking preserves margins.

Credentialing and licensing

Healthcare and specialized engineering roles often require strict certifications; BLS data shows registered nurses had a median annual wage of $81,220 (May 2023), underscoring wage leverage for credentialed staff. Candidates with scarce credentials command pay and contractual leverage, compressing agency margins. Compliance, credentialing and credential transfer can add 4–8 weeks to time-to-start and raise per-hire costs, constraining supply elasticity.

Platforms and intermediaries

Platforms like job boards, social networks and talent marketplaces — LinkedIn surpassed 1 billion members in 2024 — let candidates compare offers and market pay, strengthening supplier (candidate) bargaining power, while visible competing pay rates increase leverage. Agency curation and screening remain valued for quality and speed. Strong recruiter relationships and exclusive talent pools can mitigate platform-driven disintermediation.

- Platforms: candidate price discovery up, transparency rises

- Curation: agencies add screening value, preserve margins

- Recruiter ties: reduce risk of direct hire via marketplaces

Geography and remote work

Remote and hybrid models expand Gee Group’s talent pool beyond local scarcity, with 2024 platforms showing roughly 20% of global job ads listed remote/hybrid roles. Top remote talent faces national competition, keeping supplier power balanced; relocation barriers drop while compensation bands widen by role and market. Gee must tune sourcing, screening and pay frameworks to flexible work norms.

- 2024 remote/hybrid job ads ~20%

- National competition limits supplier leverage

- Wider compensation dispersion by market

- Require flexible sourcing and pay calibration

Specialist scarcity lifts pay 15–30%, fuels 6–12%

Specialized IT, healthcare and engineering scarcity drives 15–30% pay premiums and 6–12% annual pay growth in 2024, raising supplier power. Large pools for industrial/office roles and UK unemployment ~4.2% (2024) reduce leverage; temp pools and rapid sourcing mitigate churn. Platforms (LinkedIn 1bn members, 2024) and ~20% remote job ads increase transparency, while agency curation and recruiter ties preserve margins.

| Metric | Value |

|---|---|

| Specialist pay premium | 15–30% |

| Annual pay growth (hot niches) | 6–12% |

| UK unemployment (2024) | 4.2% |

| LinkedIn members (2024) | ~1,000,000,000 |

| Remote/hybrid job ads (2024) | ~20% |

| Credentialing delay | +4–8 weeks |

What is included in the product

Tailored Porter’s Five Forces analysis for Gee Group uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers that affect its pricing, margins and market position.

One-sheet Porter’s Five Forces for Gee Group—instantly spot competitive pressures and relieve strategic uncertainty with customizable force levels, a clean slide-ready layout, and no complex code so non-finance teams can act fast.

Customers Bargaining Power

Many alternatives

Clients can pick from global firms, regional specialists and boutiques, and with the global staffing market topping $500 billion in 2024 this abundant choice raises price sensitivity and switching behavior. Differentiation via speed, quality and vertical expertise is essential to retain contracts. Multi-sourcing by buyers—commonly splitting spends across 2–4 vendors—further compresses margins.

MSP/VMS procurement

MSP/VMS procurement standardizes rates and SLAs, increasing transparency and shrinking bargaining room; VMS now channels about 55% of contingent workforce spend (SIA 2024). Standardization shifts competition to service metrics, with fill-rate targets typically 80–90% and compliance scores above 90% driving renewals. Volume and steadier requisitions offset rate compression by improving utilization and revenue predictability.

Low switching costs

Low switching costs mean clients can trial multiple agencies with minimal lock-in, and a 2024 industry survey found about 42% of employers sampled tested two or more recruitment partners before committing. Poor performance therefore quickly loses desks—clients moved 28% of contingent spend year-on-year in some sectors in 2024. Strong referenceability and niche credibility mitigate churn, so contract terms must balance flexibility with margin protection.

Cyclical demand

Cyclical demand means hiring slows in downturns, amplifying buyer leverage on price and terms, while in expansions urgent hiring needs improve agency negotiating position; mid-2024 US unemployment around 4.1% highlighted softer hiring that boosted client bargaining power. Diversification across sectors and a shift toward contract-to-hire smooth revenue volatility and preserve margins versus pure direct-hire.

- Downturn: higher buyer leverage

- Expansion: urgent demand raises agency leverage

- Diversification smooths cycles

- Contract-to-hire = greater resilience

Outcome and compliance focus

Buyers in 2024 insist on fast time-to-fill, demonstrable quality and strict risk controls; in markets like Australia where unemployment was ~3.7% in 2024, speed and compliance drive supplier selection. Robust onboarding, background checks and safety programs build trust and reduce client churn. Data-backed performance reporting shifts competition away from price, while sector expertise secures 10–30% higher realized rates on specialist roles.

- Fast fills

- Compliance

- Data reporting

- Sector premium

Buyers dominate: $500B+, VMS 55%, 42% test partners

Buyers have strong leverage: global market >$500B (2024) and VMS channels ~55% of contingent spend, raising price transparency and switching. 42% of employers trial multiple agencies and some sectors saw 28% YoY spend moves in 2024, compressing margins; sector expertise can secure 10–30% rate premiums. Cyclical hiring (US unemployment ~4.1%, AU ~3.7% in 2024) shifts bargaining power with demand.

| Metric | 2024 Value |

|---|---|

| Global staffing market | $500B+ |

| VMS share | 55% |

| Employers testing partners | 42% |

| YoY spend moves (some sectors) | 28% |

| Sector rate premium | 10–30% |

| US unemployment | 4.1% |

| AU unemployment | 3.7% |

Preview the Actual Deliverable

Gee Group Porter's Five Forces Analysis

This preview shows the exact Gee Group Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, actionable, and ready for download the moment you buy. You're viewing the final deliverable, identical to the file you'll get instantly upon payment.