GE HealthCare Technologies Business Model Canvas

Unlock the strategic blueprint of a leading medical-tech business model and recurring revenue.

Unlock the full strategic blueprint behind GE HealthCare Technologies' business model. This concise Business Model Canvas reveals how the firm creates value, scales medical technology, and captures recurring revenue—ideal for investors, consultants, and founders. Download the complete Word/Excel canvas for a section-by-section, actionable playbook you can apply today.

Partnerships

Academic and clinical research institutions

Collaborations with leading hospitals and universities accelerate clinical validation and co-development of imaging protocols, AI algorithms, and workflows, leveraging GE HealthCare’s scale (FY 2024 revenue ~$18.5B) to access diverse multi‑site datasets that improve model generalizability and regulatory robustness; joint publications and trials boost clinician and payer credibility and shorten time‑to‑evidence for new indications.

Pharmaceutical and biotech companies

Alliances with pharmaceutical and biotech companies support companion diagnostics, imaging biomarkers and CDx development across oncology and cardiology, with GE HealthCare collaborating in over 100 programs by 2024. Co-creation in drug discovery and bioprocessing enables end-to-end solutions from target ID to manufacturing, while integrated cell and gene therapy programs use process analytics for real-time monitoring across clinical sites. Revenue sharing and milestone models, often structured 50/50 to 70/30, align incentives and accelerate go-to-market timelines.

Suppliers and contract manufacturers

Strategic sourcing of semiconductors, detectors, probes and contrast agents ensures quality and continuity for GE HealthCare Technologies, which was spun off from GE in 2023. Dual-sourcing and contract manufacturer partnerships provide capacity flexibility and cost efficiency. Co-engineering with suppliers improves manufacturability and reliability of critical subsystems. Long-term supply agreements stabilize pricing and lead times.

Cloud, AI, and interoperability partners

Partnerships with hyperscalers (AWS, Azure, Google Cloud) enable secure hosting, advanced analytics and HL7/FHIR integration, supported by a 2024 Gartner finding that the big three hold ~65% of cloud IaaS market. App marketplaces expand imaging and monitoring ecosystems while cybersecurity partners harden devices and networks; US regulation in 2024 mandates FHIR APIs, easing interoperability.

- Hyperscalers: secure hosting, analytics, FHIR

- Marketplaces: broaden apps for imaging/monitoring

- Cybersecurity: device/network hardening

- Alliances: reduce deployment friction, boost adoption

Distributors, group purchasing organizations, and government agencies

Channel partners extend GE HealthCare reach in fragmented and emerging markets, supporting distribution in areas where direct sales are costly; GE HealthCare reported 2024 revenue of about $20 billion, underscoring scale advantages.

GPOs, which serve over 80% of US hospitals, and public tenders streamline procurement and improve price competitiveness for capital equipment.

Public health agencies enable large-scale screening and vaccination programs reaching millions; local partners aid regulatory navigation and provide after-sales coverage and spare-parts logistics.

- Channel reach: expands market access in emerging regions

- GPOs/tenders: >80% hospital coverage, better pricing

- Public agencies: enable mass screening programs

- Local partners: regulatory support & after-sales

Clinical-pharma-cloud alliances scale > 100 CDx programs and cover > 80% US hospitals

Clinical and academic collaborations scale multi‑site validation (FY2024 revenue ~$18.5B) and shorten evidence timelines; pharma/biotech alliances support >100 CDx/drug programs and revenue‑share models; suppliers/hyperscalers (big 3 ~65% IaaS) secure components, cloud and FHIR interoperability; channels/GPOs (>80% US hospitals) expand access and pricing leverage.

| Partner | Role | 2024 Metric |

|---|---|---|

| Hospitals/Univ | Validation | Multi‑site datasets |

| Pharma | CDx/co‑dev | >100 programs |

| Hyperscalers | Cloud/FHIR | ~65% IaaS |

| GPOs/Channels | Distribution | >80% US hospitals |

What is included in the product

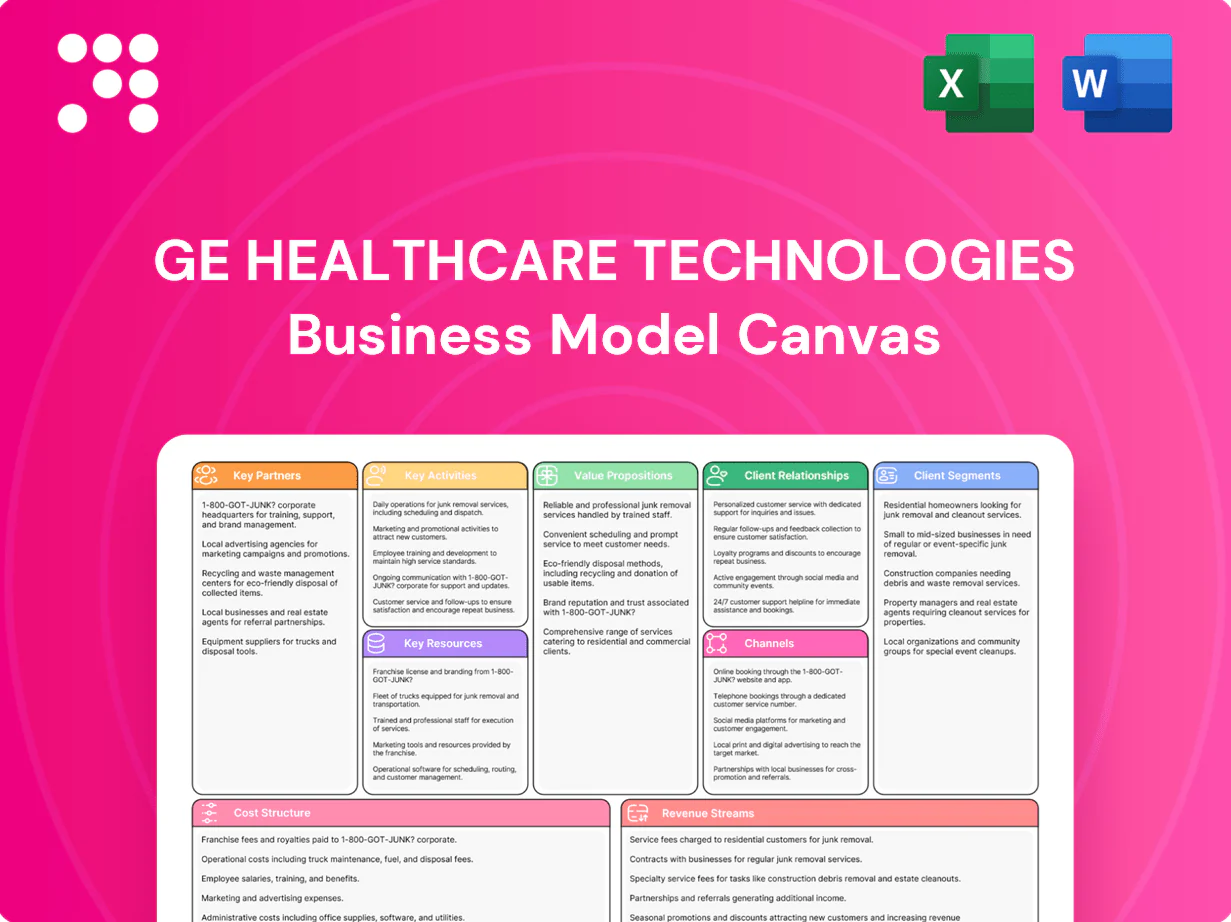

A concise Business Model Canvas for GE HealthCare Technologies mapping nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned to its imaging, diagnostics, and digital-health strategy. It highlights competitive advantages, revenue drivers, operational enablers, and linked SWOT insights for investor and strategic decision-making.

High-level view of GE HealthCare's business model with editable cells, highlighting how its integrated imaging, AI, services, and financing solutions relieve clinical workflow bottlenecks and cost pressures for providers and health systems.

Activities

R&D in imaging, monitoring, and diagnostics

Continuous R&D across MRI, CT, ultrasound and patient monitoring targets accuracy and speed, with AI-enabled reconstruction cutting MRI acquisition/reconstruction times by up to 50% and improving throughput. AI decision-support tools have shown radiologist productivity gains around 20–30% in real-world pilots. Pipeline work advances molecular imaging and quantitative biomarkers, and hundreds of clinical studies support safety, efficacy and regulatory submissions.

Design, manufacturing, and quality assurance

Lean operations enable GE HealthCare to produce complex capital equipment and consumables at scale, backed by a global footprint serving 160+ countries and over 50,000 employees (2024). Strict QMS and GMP practices ensure reliability and regulatory compliance. Localization of builds reduces tariffs and lead times, while ongoing value engineering cuts COGS without performance loss.

Software development and platform integration

Cloud-native PACS/VNA, workflow orchestration, and analytics unify multimodal data and support DICOM/HL7 FHIR interoperability by design; cybersecurity and privacy are embedded across the stack. Continuous delivery accelerates updates and feature releases, while open APIs enable partners to extend functionality — GE HealthCare reported approximately $19.8 billion revenue in 2024, underpinning these platform investments.

Regulatory, clinical, and market access

Global submissions to FDA, EMA and other authorities are coordinated to meet region-specific data and clinical requirements; GE HealthCare operates in more than 140 countries (2024). Health economics and outcomes research produces value dossiers to support pricing and formulary decisions. Reimbursement strategy maps features to CPT/DRG codes and emerging payment models while post-market surveillance sustains MDR/IVDR and FDA postmarket compliance and customer trust.

- Global submissions: multi-jurisdiction coordination

- HEOR: value dossiers for pricing and adoption

- Reimbursement: CPT/DRG alignment, bundled payments

- Post-market: MDR/IVDR and FDA postmarket surveillance

Service, training, and lifecycle management

Installation, calibration, and preventive maintenance maximize equipment uptime (clinical uptime often >95%) and cut emergency repairs by up to 40%. Remote monitoring and field service resolve ~30% of issues remotely, reducing downtime and service costs. Education programs upskill thousands of clinicians and biomedical engineers annually, while structured upgrade paths extend asset life and improve ROI.

- uptime: >95%

- remote fixes: ~30%

- repair reduction: up to 40%

- training: thousands/year

AI MRI: scan time down 50%, radiologist +20-30%, $19.8B backing

Continuous R&D (AI MRI accel up to 50%, radiologist productivity +20–30%) and global manufacturing/support (50,000 employees; 160+ countries, 2024) fund cloud-native platforms, HEOR, and coordinated FDA/EMA filings; 2024 revenue ~$19.8B underpins product, regulatory and service investments. Field services deliver >95% uptime, ~30% remote fixes, and training for thousands annually.

| Metric | 2024 / Impact |

|---|---|

| Revenue | $19.8B |

| Employees | ~50,000 |

| Global reach | 160+ countries |

| MRI time reduction | up to 50% |

| Radiologist productivity | +20–30% |

| Uptime | >95% |

| Remote fixes | ~30% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual GE HealthCare Technologies Business Model Canvas you'll receive—no mockup or sample. Upon purchase you'll download the complete, editable file (Word and Excel), formatted exactly as shown, ready to present, edit, and apply.

Unlock the strategic blueprint of a leading medical-tech business model and recurring revenue.

Unlock the full strategic blueprint behind GE HealthCare Technologies' business model. This concise Business Model Canvas reveals how the firm creates value, scales medical technology, and captures recurring revenue—ideal for investors, consultants, and founders. Download the complete Word/Excel canvas for a section-by-section, actionable playbook you can apply today.

Partnerships

Academic and clinical research institutions

Collaborations with leading hospitals and universities accelerate clinical validation and co-development of imaging protocols, AI algorithms, and workflows, leveraging GE HealthCare’s scale (FY 2024 revenue ~$18.5B) to access diverse multi‑site datasets that improve model generalizability and regulatory robustness; joint publications and trials boost clinician and payer credibility and shorten time‑to‑evidence for new indications.

Pharmaceutical and biotech companies

Alliances with pharmaceutical and biotech companies support companion diagnostics, imaging biomarkers and CDx development across oncology and cardiology, with GE HealthCare collaborating in over 100 programs by 2024. Co-creation in drug discovery and bioprocessing enables end-to-end solutions from target ID to manufacturing, while integrated cell and gene therapy programs use process analytics for real-time monitoring across clinical sites. Revenue sharing and milestone models, often structured 50/50 to 70/30, align incentives and accelerate go-to-market timelines.

Suppliers and contract manufacturers

Strategic sourcing of semiconductors, detectors, probes and contrast agents ensures quality and continuity for GE HealthCare Technologies, which was spun off from GE in 2023. Dual-sourcing and contract manufacturer partnerships provide capacity flexibility and cost efficiency. Co-engineering with suppliers improves manufacturability and reliability of critical subsystems. Long-term supply agreements stabilize pricing and lead times.

Cloud, AI, and interoperability partners

Partnerships with hyperscalers (AWS, Azure, Google Cloud) enable secure hosting, advanced analytics and HL7/FHIR integration, supported by a 2024 Gartner finding that the big three hold ~65% of cloud IaaS market. App marketplaces expand imaging and monitoring ecosystems while cybersecurity partners harden devices and networks; US regulation in 2024 mandates FHIR APIs, easing interoperability.

- Hyperscalers: secure hosting, analytics, FHIR

- Marketplaces: broaden apps for imaging/monitoring

- Cybersecurity: device/network hardening

- Alliances: reduce deployment friction, boost adoption

Distributors, group purchasing organizations, and government agencies

Channel partners extend GE HealthCare reach in fragmented and emerging markets, supporting distribution in areas where direct sales are costly; GE HealthCare reported 2024 revenue of about $20 billion, underscoring scale advantages.

GPOs, which serve over 80% of US hospitals, and public tenders streamline procurement and improve price competitiveness for capital equipment.

Public health agencies enable large-scale screening and vaccination programs reaching millions; local partners aid regulatory navigation and provide after-sales coverage and spare-parts logistics.

- Channel reach: expands market access in emerging regions

- GPOs/tenders: >80% hospital coverage, better pricing

- Public agencies: enable mass screening programs

- Local partners: regulatory support & after-sales

Clinical-pharma-cloud alliances scale > 100 CDx programs and cover > 80% US hospitals

Clinical and academic collaborations scale multi‑site validation (FY2024 revenue ~$18.5B) and shorten evidence timelines; pharma/biotech alliances support >100 CDx/drug programs and revenue‑share models; suppliers/hyperscalers (big 3 ~65% IaaS) secure components, cloud and FHIR interoperability; channels/GPOs (>80% US hospitals) expand access and pricing leverage.

| Partner | Role | 2024 Metric |

|---|---|---|

| Hospitals/Univ | Validation | Multi‑site datasets |

| Pharma | CDx/co‑dev | >100 programs |

| Hyperscalers | Cloud/FHIR | ~65% IaaS |

| GPOs/Channels | Distribution | >80% US hospitals |

What is included in the product

A concise Business Model Canvas for GE HealthCare Technologies mapping nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned to its imaging, diagnostics, and digital-health strategy. It highlights competitive advantages, revenue drivers, operational enablers, and linked SWOT insights for investor and strategic decision-making.

High-level view of GE HealthCare's business model with editable cells, highlighting how its integrated imaging, AI, services, and financing solutions relieve clinical workflow bottlenecks and cost pressures for providers and health systems.

Activities

R&D in imaging, monitoring, and diagnostics

Continuous R&D across MRI, CT, ultrasound and patient monitoring targets accuracy and speed, with AI-enabled reconstruction cutting MRI acquisition/reconstruction times by up to 50% and improving throughput. AI decision-support tools have shown radiologist productivity gains around 20–30% in real-world pilots. Pipeline work advances molecular imaging and quantitative biomarkers, and hundreds of clinical studies support safety, efficacy and regulatory submissions.

Design, manufacturing, and quality assurance

Lean operations enable GE HealthCare to produce complex capital equipment and consumables at scale, backed by a global footprint serving 160+ countries and over 50,000 employees (2024). Strict QMS and GMP practices ensure reliability and regulatory compliance. Localization of builds reduces tariffs and lead times, while ongoing value engineering cuts COGS without performance loss.

Software development and platform integration

Cloud-native PACS/VNA, workflow orchestration, and analytics unify multimodal data and support DICOM/HL7 FHIR interoperability by design; cybersecurity and privacy are embedded across the stack. Continuous delivery accelerates updates and feature releases, while open APIs enable partners to extend functionality — GE HealthCare reported approximately $19.8 billion revenue in 2024, underpinning these platform investments.

Regulatory, clinical, and market access

Global submissions to FDA, EMA and other authorities are coordinated to meet region-specific data and clinical requirements; GE HealthCare operates in more than 140 countries (2024). Health economics and outcomes research produces value dossiers to support pricing and formulary decisions. Reimbursement strategy maps features to CPT/DRG codes and emerging payment models while post-market surveillance sustains MDR/IVDR and FDA postmarket compliance and customer trust.

- Global submissions: multi-jurisdiction coordination

- HEOR: value dossiers for pricing and adoption

- Reimbursement: CPT/DRG alignment, bundled payments

- Post-market: MDR/IVDR and FDA postmarket surveillance

Service, training, and lifecycle management

Installation, calibration, and preventive maintenance maximize equipment uptime (clinical uptime often >95%) and cut emergency repairs by up to 40%. Remote monitoring and field service resolve ~30% of issues remotely, reducing downtime and service costs. Education programs upskill thousands of clinicians and biomedical engineers annually, while structured upgrade paths extend asset life and improve ROI.

- uptime: >95%

- remote fixes: ~30%

- repair reduction: up to 40%

- training: thousands/year

AI MRI: scan time down 50%, radiologist +20-30%, $19.8B backing

Continuous R&D (AI MRI accel up to 50%, radiologist productivity +20–30%) and global manufacturing/support (50,000 employees; 160+ countries, 2024) fund cloud-native platforms, HEOR, and coordinated FDA/EMA filings; 2024 revenue ~$19.8B underpins product, regulatory and service investments. Field services deliver >95% uptime, ~30% remote fixes, and training for thousands annually.

| Metric | 2024 / Impact |

|---|---|

| Revenue | $19.8B |

| Employees | ~50,000 |

| Global reach | 160+ countries |

| MRI time reduction | up to 50% |

| Radiologist productivity | +20–30% |

| Uptime | >95% |

| Remote fixes | ~30% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual GE HealthCare Technologies Business Model Canvas you'll receive—no mockup or sample. Upon purchase you'll download the complete, editable file (Word and Excel), formatted exactly as shown, ready to present, edit, and apply.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic blueprint of a leading medical-tech business model and recurring revenue.

Unlock the full strategic blueprint behind GE HealthCare Technologies' business model. This concise Business Model Canvas reveals how the firm creates value, scales medical technology, and captures recurring revenue—ideal for investors, consultants, and founders. Download the complete Word/Excel canvas for a section-by-section, actionable playbook you can apply today.

Partnerships

Academic and clinical research institutions

Collaborations with leading hospitals and universities accelerate clinical validation and co-development of imaging protocols, AI algorithms, and workflows, leveraging GE HealthCare’s scale (FY 2024 revenue ~$18.5B) to access diverse multi‑site datasets that improve model generalizability and regulatory robustness; joint publications and trials boost clinician and payer credibility and shorten time‑to‑evidence for new indications.

Pharmaceutical and biotech companies

Alliances with pharmaceutical and biotech companies support companion diagnostics, imaging biomarkers and CDx development across oncology and cardiology, with GE HealthCare collaborating in over 100 programs by 2024. Co-creation in drug discovery and bioprocessing enables end-to-end solutions from target ID to manufacturing, while integrated cell and gene therapy programs use process analytics for real-time monitoring across clinical sites. Revenue sharing and milestone models, often structured 50/50 to 70/30, align incentives and accelerate go-to-market timelines.

Suppliers and contract manufacturers

Strategic sourcing of semiconductors, detectors, probes and contrast agents ensures quality and continuity for GE HealthCare Technologies, which was spun off from GE in 2023. Dual-sourcing and contract manufacturer partnerships provide capacity flexibility and cost efficiency. Co-engineering with suppliers improves manufacturability and reliability of critical subsystems. Long-term supply agreements stabilize pricing and lead times.

Cloud, AI, and interoperability partners

Partnerships with hyperscalers (AWS, Azure, Google Cloud) enable secure hosting, advanced analytics and HL7/FHIR integration, supported by a 2024 Gartner finding that the big three hold ~65% of cloud IaaS market. App marketplaces expand imaging and monitoring ecosystems while cybersecurity partners harden devices and networks; US regulation in 2024 mandates FHIR APIs, easing interoperability.

- Hyperscalers: secure hosting, analytics, FHIR

- Marketplaces: broaden apps for imaging/monitoring

- Cybersecurity: device/network hardening

- Alliances: reduce deployment friction, boost adoption

Distributors, group purchasing organizations, and government agencies

Channel partners extend GE HealthCare reach in fragmented and emerging markets, supporting distribution in areas where direct sales are costly; GE HealthCare reported 2024 revenue of about $20 billion, underscoring scale advantages.

GPOs, which serve over 80% of US hospitals, and public tenders streamline procurement and improve price competitiveness for capital equipment.

Public health agencies enable large-scale screening and vaccination programs reaching millions; local partners aid regulatory navigation and provide after-sales coverage and spare-parts logistics.

- Channel reach: expands market access in emerging regions

- GPOs/tenders: >80% hospital coverage, better pricing

- Public agencies: enable mass screening programs

- Local partners: regulatory support & after-sales

Clinical-pharma-cloud alliances scale > 100 CDx programs and cover > 80% US hospitals

Clinical and academic collaborations scale multi‑site validation (FY2024 revenue ~$18.5B) and shorten evidence timelines; pharma/biotech alliances support >100 CDx/drug programs and revenue‑share models; suppliers/hyperscalers (big 3 ~65% IaaS) secure components, cloud and FHIR interoperability; channels/GPOs (>80% US hospitals) expand access and pricing leverage.

| Partner | Role | 2024 Metric |

|---|---|---|

| Hospitals/Univ | Validation | Multi‑site datasets |

| Pharma | CDx/co‑dev | >100 programs |

| Hyperscalers | Cloud/FHIR | ~65% IaaS |

| GPOs/Channels | Distribution | >80% US hospitals |

What is included in the product

A concise Business Model Canvas for GE HealthCare Technologies mapping nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned to its imaging, diagnostics, and digital-health strategy. It highlights competitive advantages, revenue drivers, operational enablers, and linked SWOT insights for investor and strategic decision-making.

High-level view of GE HealthCare's business model with editable cells, highlighting how its integrated imaging, AI, services, and financing solutions relieve clinical workflow bottlenecks and cost pressures for providers and health systems.

Activities

R&D in imaging, monitoring, and diagnostics

Continuous R&D across MRI, CT, ultrasound and patient monitoring targets accuracy and speed, with AI-enabled reconstruction cutting MRI acquisition/reconstruction times by up to 50% and improving throughput. AI decision-support tools have shown radiologist productivity gains around 20–30% in real-world pilots. Pipeline work advances molecular imaging and quantitative biomarkers, and hundreds of clinical studies support safety, efficacy and regulatory submissions.

Design, manufacturing, and quality assurance

Lean operations enable GE HealthCare to produce complex capital equipment and consumables at scale, backed by a global footprint serving 160+ countries and over 50,000 employees (2024). Strict QMS and GMP practices ensure reliability and regulatory compliance. Localization of builds reduces tariffs and lead times, while ongoing value engineering cuts COGS without performance loss.

Software development and platform integration

Cloud-native PACS/VNA, workflow orchestration, and analytics unify multimodal data and support DICOM/HL7 FHIR interoperability by design; cybersecurity and privacy are embedded across the stack. Continuous delivery accelerates updates and feature releases, while open APIs enable partners to extend functionality — GE HealthCare reported approximately $19.8 billion revenue in 2024, underpinning these platform investments.

Regulatory, clinical, and market access

Global submissions to FDA, EMA and other authorities are coordinated to meet region-specific data and clinical requirements; GE HealthCare operates in more than 140 countries (2024). Health economics and outcomes research produces value dossiers to support pricing and formulary decisions. Reimbursement strategy maps features to CPT/DRG codes and emerging payment models while post-market surveillance sustains MDR/IVDR and FDA postmarket compliance and customer trust.

- Global submissions: multi-jurisdiction coordination

- HEOR: value dossiers for pricing and adoption

- Reimbursement: CPT/DRG alignment, bundled payments

- Post-market: MDR/IVDR and FDA postmarket surveillance

Service, training, and lifecycle management

Installation, calibration, and preventive maintenance maximize equipment uptime (clinical uptime often >95%) and cut emergency repairs by up to 40%. Remote monitoring and field service resolve ~30% of issues remotely, reducing downtime and service costs. Education programs upskill thousands of clinicians and biomedical engineers annually, while structured upgrade paths extend asset life and improve ROI.

- uptime: >95%

- remote fixes: ~30%

- repair reduction: up to 40%

- training: thousands/year

AI MRI: scan time down 50%, radiologist +20-30%, $19.8B backing

Continuous R&D (AI MRI accel up to 50%, radiologist productivity +20–30%) and global manufacturing/support (50,000 employees; 160+ countries, 2024) fund cloud-native platforms, HEOR, and coordinated FDA/EMA filings; 2024 revenue ~$19.8B underpins product, regulatory and service investments. Field services deliver >95% uptime, ~30% remote fixes, and training for thousands annually.

| Metric | 2024 / Impact |

|---|---|

| Revenue | $19.8B |

| Employees | ~50,000 |

| Global reach | 160+ countries |

| MRI time reduction | up to 50% |

| Radiologist productivity | +20–30% |

| Uptime | >95% |

| Remote fixes | ~30% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual GE HealthCare Technologies Business Model Canvas you'll receive—no mockup or sample. Upon purchase you'll download the complete, editable file (Word and Excel), formatted exactly as shown, ready to present, edit, and apply.