Gehring Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

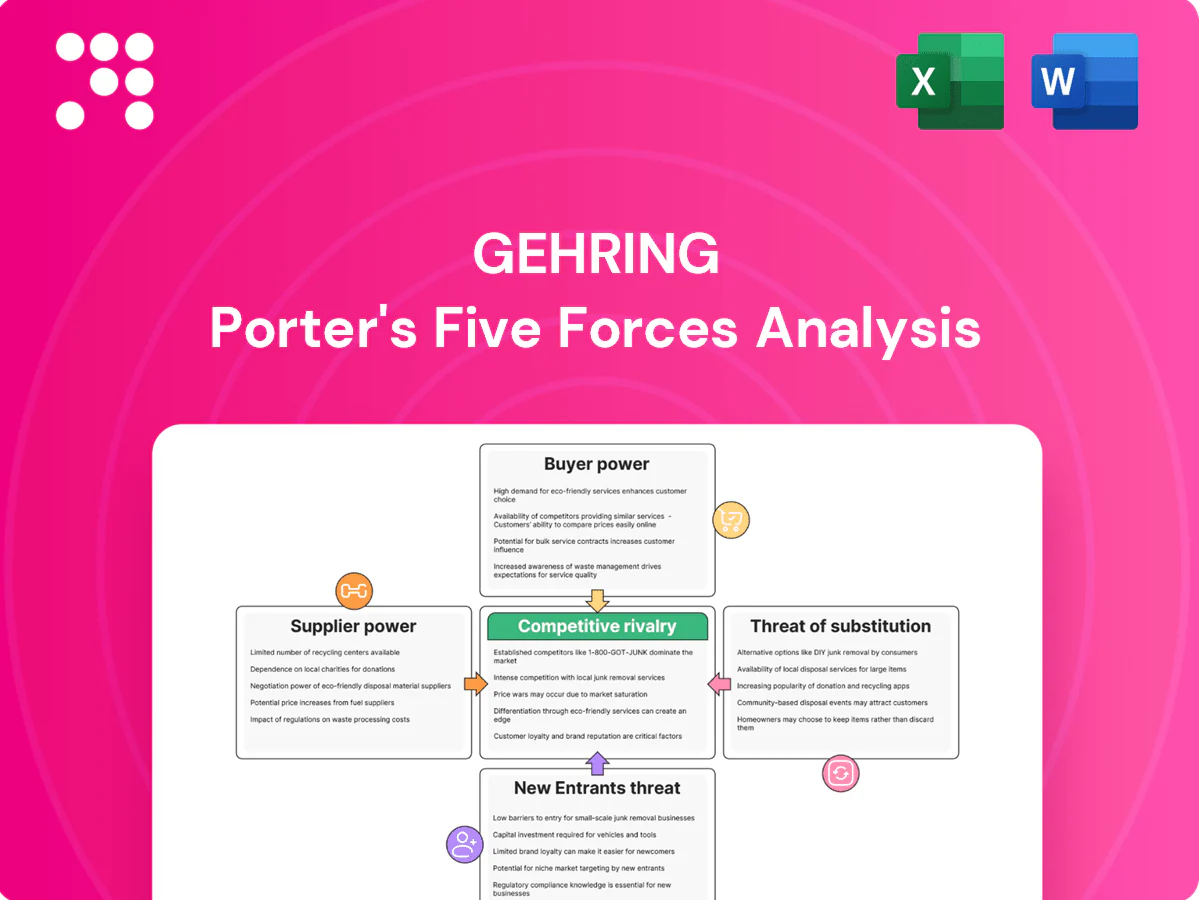

Gehring’s Porter’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitor rivalry, new entrant risks, and substitute threats shaping its market position. This brief teases actionable trends and strategic implications. Unlock the full Porter’s Five Forces Analysis for a force-by-force breakdown, visuals, and ready-to-use insights.

Suppliers Bargaining Power

Critical superabrasives

CBN and diamond superabrasives are concentrated among a few global suppliers such as Element Six and Henan Huanghe, giving them outsized leverage on price and lead times. Quality consistency directly affects surface finish and cycle time, making substitution difficult and risky. Qualification cycles and process certifications commonly span months, raising switching costs. Dual-sourcing can reduce supply risk but often sacrifices peak performance.

Precision mechatronics

Precision mechatronics suppliers—linear guides, spindles, servo drives and metrology—hold notable bargaining power due to specialization and proprietary firmware from OEM drive/controllers; lead times for high-precision spindles and drives commonly exceed 12 weeks in 2024, creating delivery risk that cascades across project timelines, while framework agreements and design-for-multi-vendor (2+ suppliers) materially reduce single-source exposure.

Customized tooling

Application-specific mandrels, fixtures and coolant systems are routinely co-developed with suppliers, embedding supplier IP and tying process know-how to external partners. That engineering collaboration raises supplier dependency and switching costs, weakening buyer leverage. Low volumes and high complexity further constrain bargaining power. Standardization and modular tool design can help rebalance commercial terms and reduce dependency.

Software and PLC ecosystems

Reliance on dominant PLC/CNC platforms ties Gehring to vendor roadmaps and licensing, with the global PLC market estimated at about $12.3B in 2024, concentrating power among Siemens, Rockwell and Mitsubishi. Deep integration raises switching costs via validation and service training; cybersecurity and remote-service features further lock clients in, while open interfaces and middleware can soften vendor leverage.

- Vendor concentration: Siemens/Rockwell/Mitsubishi

- Switching costs: high validation & training

- Lock-in: cybersecurity & remote services

- Mitigation: open APIs, middleware

Metals and specialty alloys

- Energy share: 20–30% of casting costs (2024)

- Qualification lead time: 12–18 months

- Regional concentration: >60% Asia (2024)

- Volatility reduction via contracts/nearshoring: ~20–30%

Supplier power drives risk: long lead times, onerous qualification, Asia alloy concentration

Supplier power is high where few global players dominate hard materials and PLCs, with CBN/diamond suppliers and Siemens/Rockwell/Mitsubishi commanding pricing and lead-time leverage. Qualification and validation raise switching costs—spindle/drive lead times >12 weeks and alloy/foundry qualification 12–18 months in 2024. Energy-sensitive castings (20–30% energy share) and >60% Asia alloy production further concentrate supply risk; mitigation via dual-sourcing, open APIs and nearshoring has cut volatility ~20–30%.

| Category | Concentration | Lead time | Key 2024 stat |

|---|---|---|---|

| CBN/diamonds | High | Long | Few suppliers (Element Six, Henan Huanghe) |

| Spindles/drives | Medium-High | >12 weeks | Critical firmware lock-in |

| Alloys/castings | Regional (>60% Asia) | 12–18 months qual. | Energy = 20–30% costs |

| PLC/CNC | High | Validation-heavy | PLC market $12.3B (2024) |

What is included in the product

Tailored Five Forces analysis for Gehring that uncovers competitive drivers, supplier and buyer power, substitutes and entry threats, identifies disruptive trends and strategic vulnerabilities, and is fully editable for inclusion in investor materials, strategy decks, or academic work.

A concise, one-sheet Gehring Porter's Five Forces summary that visualizes competitive pressure with a radar chart, lets you customize inputs for evolving market scenarios, and plugs into Excel dashboards—perfect for quick strategic decisions and board-ready slides.

Customers Bargaining Power

Consolidated OEMs

Consolidated OEMs buy capex in large, infrequent lots and exert strong negotiation power, enforcing strict specs, penalties and full lifecycle-cost transparency; in 2024 the top 10 OEMs accounted for roughly 70% of global vehicle production, reinforcing buyer leverage. Preferred-supplier lists further squeeze pricing flexibility, while suppliers offering value-added services and guaranteed OEE can regain negotiating ground.

High switching costs

Once a honing process is validated, requalification typically costs six-figure sums and takes 6–18 months (2024 industry reports), but buyers still extract 5–15% price concessions via competitive tenders prior to lock-in. Multi-year service and consumables deals (commonly 3–5 years) deepen dependence and made up to 30–40% of supplier revenue in 2024, while uptime SLAs and performance guarantees often carry penalties of 0.5–3% of contract value.

Price sensitivity in downturns

Cyclical auto and industrial slowdowns force capex deferrals and deeper discounting, with buyers increasingly favoring retrofits/upgrades over new lines; retrofit projects commonly deliver 10–30% energy savings, which—paired with transparent ROI models—helps defend pricing, while financing packages (US policy rates averaged ~5.3% in 2024) can ease budget constraints and enable purchases.

Customization demands

Clients increasingly demand tailored tooling, automation, and data integration, expanding negotiation scope and adding engineering work; a 2024 industry survey found roughly 72% of industrial buyers prioritize customization over off-the-shelf solutions.

Without modular architectures customization erodes margins as buyers push specifications to shift engineering costs to vendors; platform-based designs preserved 10–20% higher gross margins in 2024 case studies.

- Customization increases scope and price negotiation

- Modular platforms protect margins (10–20% uplift)

- Buyers shift engineering cost via specs

Global service expectations

Multinationals demand rapid global commissioning and spare-parts availability, making service responsiveness a frequent deal-breaker and negotiation point; buyers increasingly require documented MTTR and MTBF targets plus comprehensive digital support. Vendors with strong field networks and remote diagnostics materially lower perceived operational risk and win preferred-supplier status.

- MTTR, MTBF, digital support

- Fast commissioning & spare parts

- Field networks + remote diagnostics

Consolidated OEMs drive 5-15% concessions; modular platforms boost margins 10-20%

Consolidated OEMs (top 10 ≈70% global output in 2024) exert strong leverage, forcing specs, penalties and 5–15% pre-lock-in price concessions; requalification costs six-figure sums and 6–18 months (2024). Multi-year deals (3–5y) made 30–40% supplier revenue; uptime SLAs carry 0.5–3% penalties. Customization (72% buyers prefer, 2024) raises scope; modular platforms preserved 10–20% higher gross margins.

| Metric | 2024 |

|---|---|

| Top10 OEM share | ~70% |

| Price concessions | 5–15% |

| Multi‑yr rev | 30–40% |

| Customization demand | 72% |

| Platform margin uplift | 10–20% |

Same Document Delivered

Gehring Porter's Five Forces Analysis

This preview shows the exact Gehring Porter's Five Forces Analysis you'll receive after purchase—no samples or placeholders. The file is fully formatted and ready to download the moment you buy. You’re viewing the final deliverable, prepared for immediate use. What you see is what you get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Gehring’s Porter’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitor rivalry, new entrant risks, and substitute threats shaping its market position. This brief teases actionable trends and strategic implications. Unlock the full Porter’s Five Forces Analysis for a force-by-force breakdown, visuals, and ready-to-use insights.

Suppliers Bargaining Power

Critical superabrasives

CBN and diamond superabrasives are concentrated among a few global suppliers such as Element Six and Henan Huanghe, giving them outsized leverage on price and lead times. Quality consistency directly affects surface finish and cycle time, making substitution difficult and risky. Qualification cycles and process certifications commonly span months, raising switching costs. Dual-sourcing can reduce supply risk but often sacrifices peak performance.

Precision mechatronics

Precision mechatronics suppliers—linear guides, spindles, servo drives and metrology—hold notable bargaining power due to specialization and proprietary firmware from OEM drive/controllers; lead times for high-precision spindles and drives commonly exceed 12 weeks in 2024, creating delivery risk that cascades across project timelines, while framework agreements and design-for-multi-vendor (2+ suppliers) materially reduce single-source exposure.

Customized tooling

Application-specific mandrels, fixtures and coolant systems are routinely co-developed with suppliers, embedding supplier IP and tying process know-how to external partners. That engineering collaboration raises supplier dependency and switching costs, weakening buyer leverage. Low volumes and high complexity further constrain bargaining power. Standardization and modular tool design can help rebalance commercial terms and reduce dependency.

Software and PLC ecosystems

Reliance on dominant PLC/CNC platforms ties Gehring to vendor roadmaps and licensing, with the global PLC market estimated at about $12.3B in 2024, concentrating power among Siemens, Rockwell and Mitsubishi. Deep integration raises switching costs via validation and service training; cybersecurity and remote-service features further lock clients in, while open interfaces and middleware can soften vendor leverage.

- Vendor concentration: Siemens/Rockwell/Mitsubishi

- Switching costs: high validation & training

- Lock-in: cybersecurity & remote services

- Mitigation: open APIs, middleware

Metals and specialty alloys

- Energy share: 20–30% of casting costs (2024)

- Qualification lead time: 12–18 months

- Regional concentration: >60% Asia (2024)

- Volatility reduction via contracts/nearshoring: ~20–30%

Supplier power drives risk: long lead times, onerous qualification, Asia alloy concentration

Supplier power is high where few global players dominate hard materials and PLCs, with CBN/diamond suppliers and Siemens/Rockwell/Mitsubishi commanding pricing and lead-time leverage. Qualification and validation raise switching costs—spindle/drive lead times >12 weeks and alloy/foundry qualification 12–18 months in 2024. Energy-sensitive castings (20–30% energy share) and >60% Asia alloy production further concentrate supply risk; mitigation via dual-sourcing, open APIs and nearshoring has cut volatility ~20–30%.

| Category | Concentration | Lead time | Key 2024 stat |

|---|---|---|---|

| CBN/diamonds | High | Long | Few suppliers (Element Six, Henan Huanghe) |

| Spindles/drives | Medium-High | >12 weeks | Critical firmware lock-in |

| Alloys/castings | Regional (>60% Asia) | 12–18 months qual. | Energy = 20–30% costs |

| PLC/CNC | High | Validation-heavy | PLC market $12.3B (2024) |

What is included in the product

Tailored Five Forces analysis for Gehring that uncovers competitive drivers, supplier and buyer power, substitutes and entry threats, identifies disruptive trends and strategic vulnerabilities, and is fully editable for inclusion in investor materials, strategy decks, or academic work.

A concise, one-sheet Gehring Porter's Five Forces summary that visualizes competitive pressure with a radar chart, lets you customize inputs for evolving market scenarios, and plugs into Excel dashboards—perfect for quick strategic decisions and board-ready slides.

Customers Bargaining Power

Consolidated OEMs

Consolidated OEMs buy capex in large, infrequent lots and exert strong negotiation power, enforcing strict specs, penalties and full lifecycle-cost transparency; in 2024 the top 10 OEMs accounted for roughly 70% of global vehicle production, reinforcing buyer leverage. Preferred-supplier lists further squeeze pricing flexibility, while suppliers offering value-added services and guaranteed OEE can regain negotiating ground.

High switching costs

Once a honing process is validated, requalification typically costs six-figure sums and takes 6–18 months (2024 industry reports), but buyers still extract 5–15% price concessions via competitive tenders prior to lock-in. Multi-year service and consumables deals (commonly 3–5 years) deepen dependence and made up to 30–40% of supplier revenue in 2024, while uptime SLAs and performance guarantees often carry penalties of 0.5–3% of contract value.

Price sensitivity in downturns

Cyclical auto and industrial slowdowns force capex deferrals and deeper discounting, with buyers increasingly favoring retrofits/upgrades over new lines; retrofit projects commonly deliver 10–30% energy savings, which—paired with transparent ROI models—helps defend pricing, while financing packages (US policy rates averaged ~5.3% in 2024) can ease budget constraints and enable purchases.

Customization demands

Clients increasingly demand tailored tooling, automation, and data integration, expanding negotiation scope and adding engineering work; a 2024 industry survey found roughly 72% of industrial buyers prioritize customization over off-the-shelf solutions.

Without modular architectures customization erodes margins as buyers push specifications to shift engineering costs to vendors; platform-based designs preserved 10–20% higher gross margins in 2024 case studies.

- Customization increases scope and price negotiation

- Modular platforms protect margins (10–20% uplift)

- Buyers shift engineering cost via specs

Global service expectations

Multinationals demand rapid global commissioning and spare-parts availability, making service responsiveness a frequent deal-breaker and negotiation point; buyers increasingly require documented MTTR and MTBF targets plus comprehensive digital support. Vendors with strong field networks and remote diagnostics materially lower perceived operational risk and win preferred-supplier status.

- MTTR, MTBF, digital support

- Fast commissioning & spare parts

- Field networks + remote diagnostics

Consolidated OEMs drive 5-15% concessions; modular platforms boost margins 10-20%

Consolidated OEMs (top 10 ≈70% global output in 2024) exert strong leverage, forcing specs, penalties and 5–15% pre-lock-in price concessions; requalification costs six-figure sums and 6–18 months (2024). Multi-year deals (3–5y) made 30–40% supplier revenue; uptime SLAs carry 0.5–3% penalties. Customization (72% buyers prefer, 2024) raises scope; modular platforms preserved 10–20% higher gross margins.

| Metric | 2024 |

|---|---|

| Top10 OEM share | ~70% |

| Price concessions | 5–15% |

| Multi‑yr rev | 30–40% |

| Customization demand | 72% |

| Platform margin uplift | 10–20% |

Same Document Delivered

Gehring Porter's Five Forces Analysis

This preview shows the exact Gehring Porter's Five Forces Analysis you'll receive after purchase—no samples or placeholders. The file is fully formatted and ready to download the moment you buy. You’re viewing the final deliverable, prepared for immediate use. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Gehring’s Porter’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitor rivalry, new entrant risks, and substitute threats shaping its market position. This brief teases actionable trends and strategic implications. Unlock the full Porter’s Five Forces Analysis for a force-by-force breakdown, visuals, and ready-to-use insights.

Suppliers Bargaining Power

Critical superabrasives

CBN and diamond superabrasives are concentrated among a few global suppliers such as Element Six and Henan Huanghe, giving them outsized leverage on price and lead times. Quality consistency directly affects surface finish and cycle time, making substitution difficult and risky. Qualification cycles and process certifications commonly span months, raising switching costs. Dual-sourcing can reduce supply risk but often sacrifices peak performance.

Precision mechatronics

Precision mechatronics suppliers—linear guides, spindles, servo drives and metrology—hold notable bargaining power due to specialization and proprietary firmware from OEM drive/controllers; lead times for high-precision spindles and drives commonly exceed 12 weeks in 2024, creating delivery risk that cascades across project timelines, while framework agreements and design-for-multi-vendor (2+ suppliers) materially reduce single-source exposure.

Customized tooling

Application-specific mandrels, fixtures and coolant systems are routinely co-developed with suppliers, embedding supplier IP and tying process know-how to external partners. That engineering collaboration raises supplier dependency and switching costs, weakening buyer leverage. Low volumes and high complexity further constrain bargaining power. Standardization and modular tool design can help rebalance commercial terms and reduce dependency.

Software and PLC ecosystems

Reliance on dominant PLC/CNC platforms ties Gehring to vendor roadmaps and licensing, with the global PLC market estimated at about $12.3B in 2024, concentrating power among Siemens, Rockwell and Mitsubishi. Deep integration raises switching costs via validation and service training; cybersecurity and remote-service features further lock clients in, while open interfaces and middleware can soften vendor leverage.

- Vendor concentration: Siemens/Rockwell/Mitsubishi

- Switching costs: high validation & training

- Lock-in: cybersecurity & remote services

- Mitigation: open APIs, middleware

Metals and specialty alloys

- Energy share: 20–30% of casting costs (2024)

- Qualification lead time: 12–18 months

- Regional concentration: >60% Asia (2024)

- Volatility reduction via contracts/nearshoring: ~20–30%

Supplier power drives risk: long lead times, onerous qualification, Asia alloy concentration

Supplier power is high where few global players dominate hard materials and PLCs, with CBN/diamond suppliers and Siemens/Rockwell/Mitsubishi commanding pricing and lead-time leverage. Qualification and validation raise switching costs—spindle/drive lead times >12 weeks and alloy/foundry qualification 12–18 months in 2024. Energy-sensitive castings (20–30% energy share) and >60% Asia alloy production further concentrate supply risk; mitigation via dual-sourcing, open APIs and nearshoring has cut volatility ~20–30%.

| Category | Concentration | Lead time | Key 2024 stat |

|---|---|---|---|

| CBN/diamonds | High | Long | Few suppliers (Element Six, Henan Huanghe) |

| Spindles/drives | Medium-High | >12 weeks | Critical firmware lock-in |

| Alloys/castings | Regional (>60% Asia) | 12–18 months qual. | Energy = 20–30% costs |

| PLC/CNC | High | Validation-heavy | PLC market $12.3B (2024) |

What is included in the product

Tailored Five Forces analysis for Gehring that uncovers competitive drivers, supplier and buyer power, substitutes and entry threats, identifies disruptive trends and strategic vulnerabilities, and is fully editable for inclusion in investor materials, strategy decks, or academic work.

A concise, one-sheet Gehring Porter's Five Forces summary that visualizes competitive pressure with a radar chart, lets you customize inputs for evolving market scenarios, and plugs into Excel dashboards—perfect for quick strategic decisions and board-ready slides.

Customers Bargaining Power

Consolidated OEMs

Consolidated OEMs buy capex in large, infrequent lots and exert strong negotiation power, enforcing strict specs, penalties and full lifecycle-cost transparency; in 2024 the top 10 OEMs accounted for roughly 70% of global vehicle production, reinforcing buyer leverage. Preferred-supplier lists further squeeze pricing flexibility, while suppliers offering value-added services and guaranteed OEE can regain negotiating ground.

High switching costs

Once a honing process is validated, requalification typically costs six-figure sums and takes 6–18 months (2024 industry reports), but buyers still extract 5–15% price concessions via competitive tenders prior to lock-in. Multi-year service and consumables deals (commonly 3–5 years) deepen dependence and made up to 30–40% of supplier revenue in 2024, while uptime SLAs and performance guarantees often carry penalties of 0.5–3% of contract value.

Price sensitivity in downturns

Cyclical auto and industrial slowdowns force capex deferrals and deeper discounting, with buyers increasingly favoring retrofits/upgrades over new lines; retrofit projects commonly deliver 10–30% energy savings, which—paired with transparent ROI models—helps defend pricing, while financing packages (US policy rates averaged ~5.3% in 2024) can ease budget constraints and enable purchases.

Customization demands

Clients increasingly demand tailored tooling, automation, and data integration, expanding negotiation scope and adding engineering work; a 2024 industry survey found roughly 72% of industrial buyers prioritize customization over off-the-shelf solutions.

Without modular architectures customization erodes margins as buyers push specifications to shift engineering costs to vendors; platform-based designs preserved 10–20% higher gross margins in 2024 case studies.

- Customization increases scope and price negotiation

- Modular platforms protect margins (10–20% uplift)

- Buyers shift engineering cost via specs

Global service expectations

Multinationals demand rapid global commissioning and spare-parts availability, making service responsiveness a frequent deal-breaker and negotiation point; buyers increasingly require documented MTTR and MTBF targets plus comprehensive digital support. Vendors with strong field networks and remote diagnostics materially lower perceived operational risk and win preferred-supplier status.

- MTTR, MTBF, digital support

- Fast commissioning & spare parts

- Field networks + remote diagnostics

Consolidated OEMs drive 5-15% concessions; modular platforms boost margins 10-20%

Consolidated OEMs (top 10 ≈70% global output in 2024) exert strong leverage, forcing specs, penalties and 5–15% pre-lock-in price concessions; requalification costs six-figure sums and 6–18 months (2024). Multi-year deals (3–5y) made 30–40% supplier revenue; uptime SLAs carry 0.5–3% penalties. Customization (72% buyers prefer, 2024) raises scope; modular platforms preserved 10–20% higher gross margins.

| Metric | 2024 |

|---|---|

| Top10 OEM share | ~70% |

| Price concessions | 5–15% |

| Multi‑yr rev | 30–40% |

| Customization demand | 72% |

| Platform margin uplift | 10–20% |

Same Document Delivered

Gehring Porter's Five Forces Analysis

This preview shows the exact Gehring Porter's Five Forces Analysis you'll receive after purchase—no samples or placeholders. The file is fully formatted and ready to download the moment you buy. You’re viewing the final deliverable, prepared for immediate use. What you see is what you get.