Gemfields Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

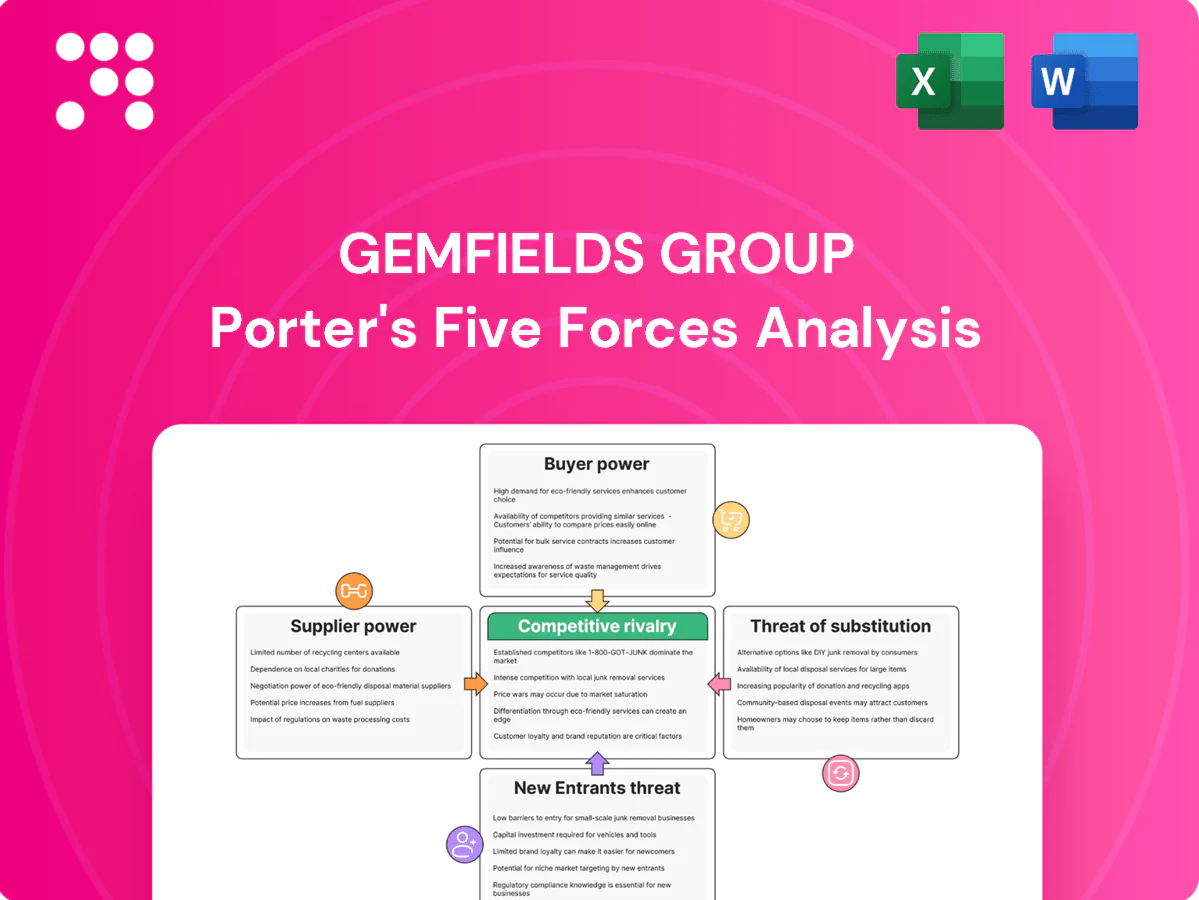

Gemfields Group faces concentrated supplier power in colored gemstones, moderate buyer bargaining from auction-dependent channels, and significant regulatory and substitution risks that shape margins and growth potential. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, strategic implications, and data-driven recommendations. Get the full report to inform investment or strategy with consultant-grade insights.

Suppliers Bargaining Power

Concentrated mining rights and permits

Host governments in Zambia and Mozambique control mining licences, land access and fiscal terms; Gemfields operates Kagem (emeralds) in Zambia and Montepuez (rubies) in Mozambique as of 2024, giving states high leverage over operations.

Renewal risk, royalty adjustments or local content mandates can rapidly shift cost structures and bargaining power.

Robust compliance and community investment lower permitting risk but do not remove it; political shifts can reprice projects across their lives.

Skilled labor and contractor dependence

Specialized geology, blasting, security and processing expertise is scarce around Gemfields’ remote Mozambique and Zambia operations, increasing supplier leverage.

Union activity and heightened safety standards in Zambia and Mozambique put upward pressure on wages and shift rostering.

Multi-year contractor agreements (commonly 3–5 years) with indexation clauses reduce volatility but lock in costs, while local training pipelines help though ramp-up typically takes 12–18 months.

Equipment, parts, fuel, and energy inputs

For Gemfields Group, heavy-equipment OEMs, diesel suppliers and power providers showed episodic pricing power amid 2023–24 logistics bottlenecks; Brent averaged about $86/bbl in 2024, pushing fuel premia. Lead times on spares stretched, raising downtime costs; dual-sourcing and inventory buffers mitigate but remote-site premia of roughly 10–20% persist. Rising carbon prices (EU ETS ~€85/t in 2024) further reshape bargaining dynamics.

Community and ESG consent

Local communities and NGOs function as critical social-license suppliers for Gemfields Group, able to halt Montepuez and Kagem operations via grievances or protest, increasing operating costs and compensatory obligations; transparent engagement and community development programs reduce friction and legal risk.

- Community influence on continuity

- Grievances can stop operations

- Engagement lowers disruption

- Certification boosts negotiation credibility

Security and logistics corridors

Secure transport, port access and in-country logistics are critical for Montepuez operations, giving vetted providers leverage over Gemfields as Cabo Delgado insurgency persisted into 2024, elevating transit risk and costs. Long-term contracts and diversified routes mitigate dependence, while mandatory insurance for high-value ruby shipments amplifies supplier influence and raises operating margins.

- Secure corridors: increased leverage for vetted carriers

- Regional risk: Cabo Delgado instability continued in 2024

- Mitigation: long-term relationships, route diversification

- Insurance: higher premiums increase supplier power

Host-state leverage, logistics squeeze and fuel stress - Brent $86/bbl

Supplier power is high: host states control licences (Zambia, Mozambique), renewal/royalty risk can reprice projects; logistics insecurity (Cabo Delgado) and scarce specialist inputs raise leverage. Fuel and parts stressed in 2023–24 (Brent ~ $86/bbl in 2024; spares lead times up; remote-site premia ~10–20%). Long-term contracts (3–5 yrs) and local training (12–18 months) partially mitigate.

| Supplier | Power driver | 2024 datapoint |

|---|---|---|

| Host states | Licence, fiscal terms | High leverage |

| Fuel/OEMs | Price & lead times | Brent ~$86/bbl; spares delays |

| Communities | Social licence | Operational stoppage risk |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Gemfields Group, uncovering competitive drivers, supplier and buyer power, and threats from substitutes and new entrants. Highlights barriers protecting incumbents, disruptive risks, pricing influence and strategic implications for investors and management.

One-sheet Porter's Five Forces for Gemfields—fast clarity on competitive pressures and pricing risks, ready to drop into decks or adapt with your own data.

Customers Bargaining Power

Diverse global trade buyers via auctions

Auctions broaden Gemfields' bidder base and enhance price discovery, diluting individual buyer power by creating competitive tension and limiting bilateral discounting. Competitive lots and transparency reduce one-on-one negotiating leverage, though buyer selectivity intensifies for top-quality stones where premium capture remains strong. Post-auction liquidity conditions continue to influence clearing prices and secondary-market realization.

Concentration in cutting and polishing hubs

Large buyers concentrated in India, Thailand and Europe exert strong leverage through volume discounts and extended working-capital terms, though Gemfields’ enhanced disclosure in 2024 has reduced grading asymmetry and moderated that power; pipeline financing arrangements and currency swings can still reweight negotiations, while deep relationships and reliable, consistent supply from Gemfields soften buyer leverage over time.

Product differentiation by origin and ethics

Gemfields leverages provenance from Kagem and Montepuez and documented ESG credentials to lower substitutability and buyer bargaining power, as branded storytelling commands retail premia. Enhanced traceability—laser inscription and chain-of-custody reporting—shifts buyer focus from price to certified value, reducing room for aggressive discounts and strengthening retail pull-through.

Demand cyclicality in luxury

Macro slowdowns and retail inventory gluts raise buyer power as buyers tighten bids or delay purchases; interest-rate volatility (US federal funds ~5.25–5.50% in 2024) and currency swings erode wholesale appetite, while Gemfields’ lot flexibility and periodic auctions (regular Zambia and Mozambique sales) help manage cycles, though downturns can still compress margins across categories.

- Buyer leverage up in slowdowns

- Rates/currency hurt wholesale demand

- Lot flexibility + auctions = cycle mitigation

- Downturns compress margins

Alternatives from artisanal and informal channels

Informal artisanal channels can undercut prices and occasionally strengthen buyer leverage by offering opportunistic supply; however, inconsistent quality, legality issues, and reputational risk constrain their appeal for premium buyers. In 2024 many luxury buyers intensified requirements for traceability and chain-of-custody, which favors Gemfields’ audited, traceable supply model. As enforcement and due-diligence standards tighten, the practical alternative set for high-end purchasers shrinks further.

- Opportunistic pricing boosts short-term buyer leverage

- Quality/legal/reputational limits deter premium brands

- 2024 traceability demands benefit Gemfields

- Stronger enforcement narrows artisanal alternatives

Auctions widen bidder pools; quality gems and traceability sustain premiums amid buyer leverage

Auctions expand bidder pools and limit bilateral discounting, but top-quality stones concentrate buyer selectivity and sustain premium capture. Large wholesale buyers (India/Thailand/Europe) retain leverage via volume and payment terms, though 2024 traceability and disclosure improvements reduced grading asymmetry. Macro factors—US rates ~5.25–5.50% in 2024—and retail gluts raise buyer bargaining power during downturns.

| Metric | 2024 Data |

|---|---|

| US policy rate | 5.25–5.50% |

| Auction cadence | Regular Zambia & Mozambique sales |

| Traceability | Laser inscription & chain-of-custody adoption ↑ |

Full Version Awaits

Gemfields Group Porter's Five Forces Analysis

This preview shows the exact Gemfields Group Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders. The document displayed is the final deliverable, containing the same in-depth assessment, data and conclusions as the purchased file. No mockups or samples—what you see is what you get instantly upon payment.

From Overview to Strategy Blueprint

Gemfields Group faces concentrated supplier power in colored gemstones, moderate buyer bargaining from auction-dependent channels, and significant regulatory and substitution risks that shape margins and growth potential. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, strategic implications, and data-driven recommendations. Get the full report to inform investment or strategy with consultant-grade insights.

Suppliers Bargaining Power

Concentrated mining rights and permits

Host governments in Zambia and Mozambique control mining licences, land access and fiscal terms; Gemfields operates Kagem (emeralds) in Zambia and Montepuez (rubies) in Mozambique as of 2024, giving states high leverage over operations.

Renewal risk, royalty adjustments or local content mandates can rapidly shift cost structures and bargaining power.

Robust compliance and community investment lower permitting risk but do not remove it; political shifts can reprice projects across their lives.

Skilled labor and contractor dependence

Specialized geology, blasting, security and processing expertise is scarce around Gemfields’ remote Mozambique and Zambia operations, increasing supplier leverage.

Union activity and heightened safety standards in Zambia and Mozambique put upward pressure on wages and shift rostering.

Multi-year contractor agreements (commonly 3–5 years) with indexation clauses reduce volatility but lock in costs, while local training pipelines help though ramp-up typically takes 12–18 months.

Equipment, parts, fuel, and energy inputs

For Gemfields Group, heavy-equipment OEMs, diesel suppliers and power providers showed episodic pricing power amid 2023–24 logistics bottlenecks; Brent averaged about $86/bbl in 2024, pushing fuel premia. Lead times on spares stretched, raising downtime costs; dual-sourcing and inventory buffers mitigate but remote-site premia of roughly 10–20% persist. Rising carbon prices (EU ETS ~€85/t in 2024) further reshape bargaining dynamics.

Community and ESG consent

Local communities and NGOs function as critical social-license suppliers for Gemfields Group, able to halt Montepuez and Kagem operations via grievances or protest, increasing operating costs and compensatory obligations; transparent engagement and community development programs reduce friction and legal risk.

- Community influence on continuity

- Grievances can stop operations

- Engagement lowers disruption

- Certification boosts negotiation credibility

Security and logistics corridors

Secure transport, port access and in-country logistics are critical for Montepuez operations, giving vetted providers leverage over Gemfields as Cabo Delgado insurgency persisted into 2024, elevating transit risk and costs. Long-term contracts and diversified routes mitigate dependence, while mandatory insurance for high-value ruby shipments amplifies supplier influence and raises operating margins.

- Secure corridors: increased leverage for vetted carriers

- Regional risk: Cabo Delgado instability continued in 2024

- Mitigation: long-term relationships, route diversification

- Insurance: higher premiums increase supplier power

Host-state leverage, logistics squeeze and fuel stress - Brent $86/bbl

Supplier power is high: host states control licences (Zambia, Mozambique), renewal/royalty risk can reprice projects; logistics insecurity (Cabo Delgado) and scarce specialist inputs raise leverage. Fuel and parts stressed in 2023–24 (Brent ~ $86/bbl in 2024; spares lead times up; remote-site premia ~10–20%). Long-term contracts (3–5 yrs) and local training (12–18 months) partially mitigate.

| Supplier | Power driver | 2024 datapoint |

|---|---|---|

| Host states | Licence, fiscal terms | High leverage |

| Fuel/OEMs | Price & lead times | Brent ~$86/bbl; spares delays |

| Communities | Social licence | Operational stoppage risk |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Gemfields Group, uncovering competitive drivers, supplier and buyer power, and threats from substitutes and new entrants. Highlights barriers protecting incumbents, disruptive risks, pricing influence and strategic implications for investors and management.

One-sheet Porter's Five Forces for Gemfields—fast clarity on competitive pressures and pricing risks, ready to drop into decks or adapt with your own data.

Customers Bargaining Power

Diverse global trade buyers via auctions

Auctions broaden Gemfields' bidder base and enhance price discovery, diluting individual buyer power by creating competitive tension and limiting bilateral discounting. Competitive lots and transparency reduce one-on-one negotiating leverage, though buyer selectivity intensifies for top-quality stones where premium capture remains strong. Post-auction liquidity conditions continue to influence clearing prices and secondary-market realization.

Concentration in cutting and polishing hubs

Large buyers concentrated in India, Thailand and Europe exert strong leverage through volume discounts and extended working-capital terms, though Gemfields’ enhanced disclosure in 2024 has reduced grading asymmetry and moderated that power; pipeline financing arrangements and currency swings can still reweight negotiations, while deep relationships and reliable, consistent supply from Gemfields soften buyer leverage over time.

Product differentiation by origin and ethics

Gemfields leverages provenance from Kagem and Montepuez and documented ESG credentials to lower substitutability and buyer bargaining power, as branded storytelling commands retail premia. Enhanced traceability—laser inscription and chain-of-custody reporting—shifts buyer focus from price to certified value, reducing room for aggressive discounts and strengthening retail pull-through.

Demand cyclicality in luxury

Macro slowdowns and retail inventory gluts raise buyer power as buyers tighten bids or delay purchases; interest-rate volatility (US federal funds ~5.25–5.50% in 2024) and currency swings erode wholesale appetite, while Gemfields’ lot flexibility and periodic auctions (regular Zambia and Mozambique sales) help manage cycles, though downturns can still compress margins across categories.

- Buyer leverage up in slowdowns

- Rates/currency hurt wholesale demand

- Lot flexibility + auctions = cycle mitigation

- Downturns compress margins

Alternatives from artisanal and informal channels

Informal artisanal channels can undercut prices and occasionally strengthen buyer leverage by offering opportunistic supply; however, inconsistent quality, legality issues, and reputational risk constrain their appeal for premium buyers. In 2024 many luxury buyers intensified requirements for traceability and chain-of-custody, which favors Gemfields’ audited, traceable supply model. As enforcement and due-diligence standards tighten, the practical alternative set for high-end purchasers shrinks further.

- Opportunistic pricing boosts short-term buyer leverage

- Quality/legal/reputational limits deter premium brands

- 2024 traceability demands benefit Gemfields

- Stronger enforcement narrows artisanal alternatives

Auctions widen bidder pools; quality gems and traceability sustain premiums amid buyer leverage

Auctions expand bidder pools and limit bilateral discounting, but top-quality stones concentrate buyer selectivity and sustain premium capture. Large wholesale buyers (India/Thailand/Europe) retain leverage via volume and payment terms, though 2024 traceability and disclosure improvements reduced grading asymmetry. Macro factors—US rates ~5.25–5.50% in 2024—and retail gluts raise buyer bargaining power during downturns.

| Metric | 2024 Data |

|---|---|

| US policy rate | 5.25–5.50% |

| Auction cadence | Regular Zambia & Mozambique sales |

| Traceability | Laser inscription & chain-of-custody adoption ↑ |

Full Version Awaits

Gemfields Group Porter's Five Forces Analysis

This preview shows the exact Gemfields Group Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders. The document displayed is the final deliverable, containing the same in-depth assessment, data and conclusions as the purchased file. No mockups or samples—what you see is what you get instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Gemfields Group faces concentrated supplier power in colored gemstones, moderate buyer bargaining from auction-dependent channels, and significant regulatory and substitution risks that shape margins and growth potential. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, strategic implications, and data-driven recommendations. Get the full report to inform investment or strategy with consultant-grade insights.

Suppliers Bargaining Power

Concentrated mining rights and permits

Host governments in Zambia and Mozambique control mining licences, land access and fiscal terms; Gemfields operates Kagem (emeralds) in Zambia and Montepuez (rubies) in Mozambique as of 2024, giving states high leverage over operations.

Renewal risk, royalty adjustments or local content mandates can rapidly shift cost structures and bargaining power.

Robust compliance and community investment lower permitting risk but do not remove it; political shifts can reprice projects across their lives.

Skilled labor and contractor dependence

Specialized geology, blasting, security and processing expertise is scarce around Gemfields’ remote Mozambique and Zambia operations, increasing supplier leverage.

Union activity and heightened safety standards in Zambia and Mozambique put upward pressure on wages and shift rostering.

Multi-year contractor agreements (commonly 3–5 years) with indexation clauses reduce volatility but lock in costs, while local training pipelines help though ramp-up typically takes 12–18 months.

Equipment, parts, fuel, and energy inputs

For Gemfields Group, heavy-equipment OEMs, diesel suppliers and power providers showed episodic pricing power amid 2023–24 logistics bottlenecks; Brent averaged about $86/bbl in 2024, pushing fuel premia. Lead times on spares stretched, raising downtime costs; dual-sourcing and inventory buffers mitigate but remote-site premia of roughly 10–20% persist. Rising carbon prices (EU ETS ~€85/t in 2024) further reshape bargaining dynamics.

Community and ESG consent

Local communities and NGOs function as critical social-license suppliers for Gemfields Group, able to halt Montepuez and Kagem operations via grievances or protest, increasing operating costs and compensatory obligations; transparent engagement and community development programs reduce friction and legal risk.

- Community influence on continuity

- Grievances can stop operations

- Engagement lowers disruption

- Certification boosts negotiation credibility

Security and logistics corridors

Secure transport, port access and in-country logistics are critical for Montepuez operations, giving vetted providers leverage over Gemfields as Cabo Delgado insurgency persisted into 2024, elevating transit risk and costs. Long-term contracts and diversified routes mitigate dependence, while mandatory insurance for high-value ruby shipments amplifies supplier influence and raises operating margins.

- Secure corridors: increased leverage for vetted carriers

- Regional risk: Cabo Delgado instability continued in 2024

- Mitigation: long-term relationships, route diversification

- Insurance: higher premiums increase supplier power

Host-state leverage, logistics squeeze and fuel stress - Brent $86/bbl

Supplier power is high: host states control licences (Zambia, Mozambique), renewal/royalty risk can reprice projects; logistics insecurity (Cabo Delgado) and scarce specialist inputs raise leverage. Fuel and parts stressed in 2023–24 (Brent ~ $86/bbl in 2024; spares lead times up; remote-site premia ~10–20%). Long-term contracts (3–5 yrs) and local training (12–18 months) partially mitigate.

| Supplier | Power driver | 2024 datapoint |

|---|---|---|

| Host states | Licence, fiscal terms | High leverage |

| Fuel/OEMs | Price & lead times | Brent ~$86/bbl; spares delays |

| Communities | Social licence | Operational stoppage risk |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Gemfields Group, uncovering competitive drivers, supplier and buyer power, and threats from substitutes and new entrants. Highlights barriers protecting incumbents, disruptive risks, pricing influence and strategic implications for investors and management.

One-sheet Porter's Five Forces for Gemfields—fast clarity on competitive pressures and pricing risks, ready to drop into decks or adapt with your own data.

Customers Bargaining Power

Diverse global trade buyers via auctions

Auctions broaden Gemfields' bidder base and enhance price discovery, diluting individual buyer power by creating competitive tension and limiting bilateral discounting. Competitive lots and transparency reduce one-on-one negotiating leverage, though buyer selectivity intensifies for top-quality stones where premium capture remains strong. Post-auction liquidity conditions continue to influence clearing prices and secondary-market realization.

Concentration in cutting and polishing hubs

Large buyers concentrated in India, Thailand and Europe exert strong leverage through volume discounts and extended working-capital terms, though Gemfields’ enhanced disclosure in 2024 has reduced grading asymmetry and moderated that power; pipeline financing arrangements and currency swings can still reweight negotiations, while deep relationships and reliable, consistent supply from Gemfields soften buyer leverage over time.

Product differentiation by origin and ethics

Gemfields leverages provenance from Kagem and Montepuez and documented ESG credentials to lower substitutability and buyer bargaining power, as branded storytelling commands retail premia. Enhanced traceability—laser inscription and chain-of-custody reporting—shifts buyer focus from price to certified value, reducing room for aggressive discounts and strengthening retail pull-through.

Demand cyclicality in luxury

Macro slowdowns and retail inventory gluts raise buyer power as buyers tighten bids or delay purchases; interest-rate volatility (US federal funds ~5.25–5.50% in 2024) and currency swings erode wholesale appetite, while Gemfields’ lot flexibility and periodic auctions (regular Zambia and Mozambique sales) help manage cycles, though downturns can still compress margins across categories.

- Buyer leverage up in slowdowns

- Rates/currency hurt wholesale demand

- Lot flexibility + auctions = cycle mitigation

- Downturns compress margins

Alternatives from artisanal and informal channels

Informal artisanal channels can undercut prices and occasionally strengthen buyer leverage by offering opportunistic supply; however, inconsistent quality, legality issues, and reputational risk constrain their appeal for premium buyers. In 2024 many luxury buyers intensified requirements for traceability and chain-of-custody, which favors Gemfields’ audited, traceable supply model. As enforcement and due-diligence standards tighten, the practical alternative set for high-end purchasers shrinks further.

- Opportunistic pricing boosts short-term buyer leverage

- Quality/legal/reputational limits deter premium brands

- 2024 traceability demands benefit Gemfields

- Stronger enforcement narrows artisanal alternatives

Auctions widen bidder pools; quality gems and traceability sustain premiums amid buyer leverage

Auctions expand bidder pools and limit bilateral discounting, but top-quality stones concentrate buyer selectivity and sustain premium capture. Large wholesale buyers (India/Thailand/Europe) retain leverage via volume and payment terms, though 2024 traceability and disclosure improvements reduced grading asymmetry. Macro factors—US rates ~5.25–5.50% in 2024—and retail gluts raise buyer bargaining power during downturns.

| Metric | 2024 Data |

|---|---|

| US policy rate | 5.25–5.50% |

| Auction cadence | Regular Zambia & Mozambique sales |

| Traceability | Laser inscription & chain-of-custody adoption ↑ |

Full Version Awaits

Gemfields Group Porter's Five Forces Analysis

This preview shows the exact Gemfields Group Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready for download with no placeholders. The document displayed is the final deliverable, containing the same in-depth assessment, data and conclusions as the purchased file. No mockups or samples—what you see is what you get instantly upon payment.