Assicurazioni Generali Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

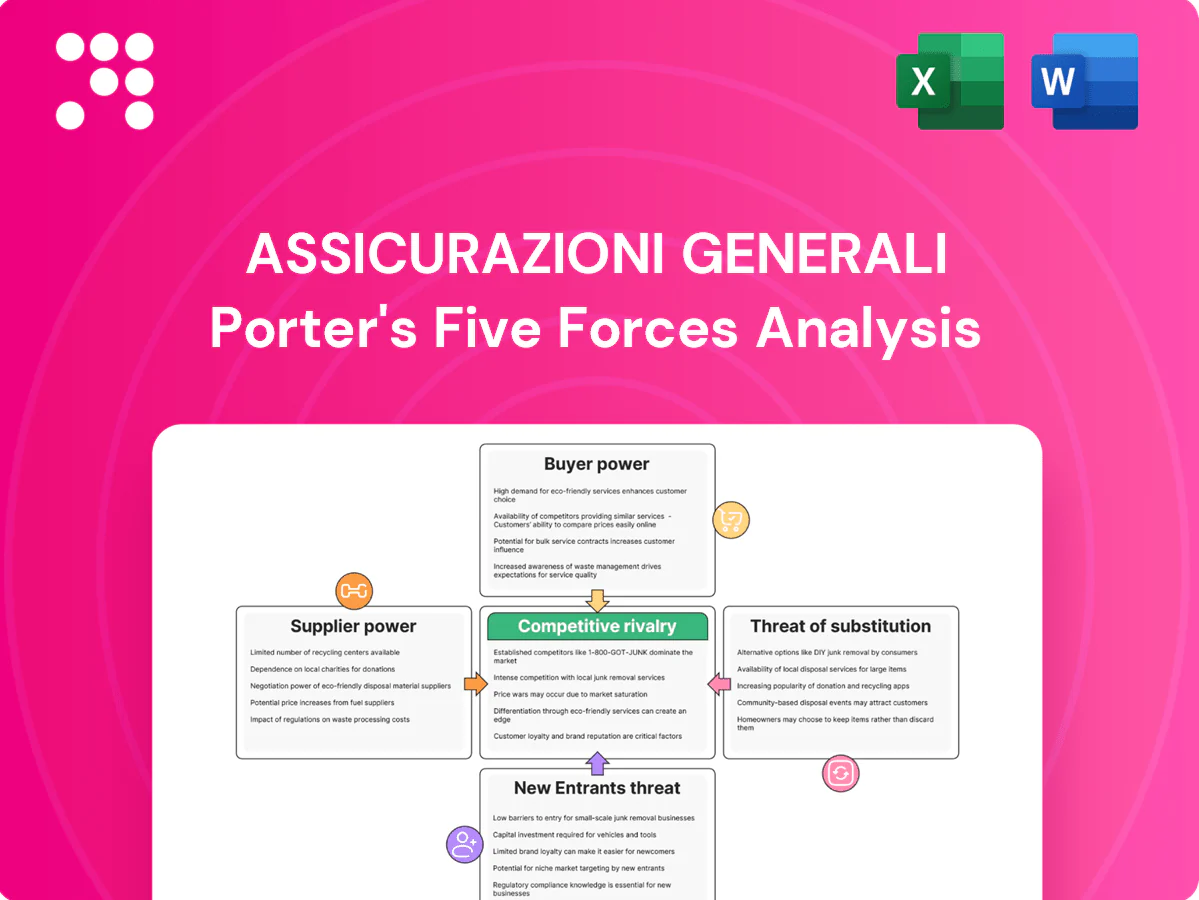

Assicurazioni Generali faces moderate buyer power, tight regulatory and capital pressures, and evolving digital threats that reshape distribution and pricing. Competitive rivalry and insurtech substitutes intensify margin pressures and force strategic repositioning. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Reinsurers influence pricing and capacity

Generali relies on global reinsurers to manage peak risks and optimize capital, ceding a portion of premiums to secure excess-of-loss capacity; industry reports showed property catastrophe rate-on-line rose about 10% in 2023–24, tightening costs and terms. Diversified reinsurer panels and multi-year treaties reduce concentration risk. Rising catastrophe losses and climate trends have increased reinsurer leverage cyclically, pressuring pricing and capacity.

Critical tech and cloud vendors

Core policy admin, cloud, cybersecurity and AI providers are concentrated—top three cloud vendors control about 65% of IaaS/PaaS market (2024)—creating material switching costs and vendor lock‑in that raise migration risk and supplier leverage over pricing and SLAs. Generali mitigates this via multi‑cloud deployment, modular stacks and expanding in‑house tech teams. Regulatory pressure, notably DORA (operational resilience rules effective 2025), further constrains vendor substitution and mandates robust oversight.

Data and analytics providers

Access to credit bureaus, telematics, geospatial and health data sharpens Generali’s underwriting, while proprietary datasets command premium pricing and restrictive licenses that raise supplier leverage. Generali mitigates this by investing in internal data lakes and strategic partnerships to diversify sources. Privacy and localization rules, notably GDPR across 27 EU countries, constrain supplier pools and increase their bargaining power.

Specialist service networks

Healthcare providers, repair shops and loss adjusters materially influence claims cost and customer experience; Generali serves about 61 million customers (2023), giving it bargaining leverage in key markets.

In certain locales limited high-quality networks can command better rates and service-level agreements, tightening supplier power where alternatives are sparse.

Generali uses preferred provider networks, DRG-based tariffs and managed-care models, leveraging scale and client steerage to secure favorable terms and SLAs.

- 61 million customers (2023)

- Preferred networks, DRGs, managed care

- Scale + steerage = better rates & SLAs

Skilled actuarial and tech talent

Actuarial, data science and cyber talent are scarce and mobile, raising supplier leverage via wage inflation and retention packages; the global cybersecurity workforce gap remained about 3.4 million in 2024. Generali’s global brand, training initiatives and hybrid work attract and retain talent, with the Group employing ≈72,000 staff in 2024. Outsourcing and centers of excellence diversify the talent base, lowering concentration risk.

- Talent scarcity: cybersecurity gap ≈3.4M (2024)

- Retention pressure: rising pay and packages

- Mitigants: Generali training, hybrid work, outsourcing

Suppliers tighten; insurer counters with 61M scale, multi-cloud, data lakes

Suppliers (reinsurers, cloud, data, healthcare providers, talent) exert moderate-to-high power: reinsurer pricing rose ≈10% 2023–24; top 3 cloud vendors hold ≈65% IaaS/PaaS (2024); cybersecurity workforce gap ≈3.4M (2024). Generali offsets via scale (61M customers, 2023), multi‑cloud, in‑house data lakes and preferred networks; 72,000 employees (2024).

| Supplier | Power drivers | Mitigants | Data |

|---|---|---|---|

| Reinsurers | Capacity & pricing | Diversified panels | Rate-on-line +10% (2023–24) |

| Cloud/data | Concentration, licensing | Multi-cloud, internal lakes | Top3 ≈65% IaaS/PaaS (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Assicurazioni Generali, providing a detailed assessment of each Porter’s force with industry data and strategic implications. Identifies disruptive threats, substitutes, and buyer/supplier power that shape the company’s pricing power, margins, and defensive barriers to entry.

One-sheet Porter's Five Forces for Assicurazioni Generali—quickly benchmark rivalry, reinsurer/buyer power, insurtech threats and regulatory pressure to simplify strategic decisions and slide-ready outputs.

Customers Bargaining Power

Retail customers are fragmented

Retail customers are fragmented—Assicurazioni Generali serves around 65 million clients worldwide (2023), so individual policyholders lack scale to negotiate bespoke terms. Price sensitivity is high, but real switching costs exist via underwriting, medical checks and loyalty benefits, softening churn. Strong brand trust and claims service reduce pure price competition, and cross-selling/bundling of life, P&C and health further diminishes buyer power.

Corporate and institutional buyers are strong

Large corporates, fleets and employee-benefits clients exert strong bargaining power, negotiating coverage, limits and pricing; loss histories and brokered tenders intensify price competition. Global programs spanning 50+ countries increase buyer leverage through jurisdictional coordination. Generali, serving ~70 million customers, counters with risk engineering, captive solutions and dedicated multinational servicing.

Brokers and bancassurance channels shape terms

Brokers and bancassurance partners aggregate demand and steer placement, extracting commissions and service levels; global brokers (Marsh, Aon, WTW) dominate large commercial P&C negotiations and press for pricing and wording concessions. In 2024 Generali leveraged a network of over 50,000 agents plus direct digital channels to counter broker leverage, while bancassurance shelf space and revenue-sharing remained crucial for life and savings inflows.

Digital comparison heightens price transparency

Regulatory protections bolster buyer rights

Regulatory protections such as the EU IDD 14‑day cooling‑off period, conduct rules and mandated claims timelines strengthen buyer rights and constrain pricing flexibility. Remediation risks and required compensations increase the cost of poor service, bolstering customer bargaining power. Generali's 2024 annual report notes continued investment in compliance and customer care to reduce disputes.

- 14‑day cooling‑off (IDD)

- Conduct & claims timelines limit exclusions

- Remediation raises operational costs

- 2024: Generali ongoing compliance/customer care investments

Retail fragmented: 65m clients; aggregators raise transparency, squeeze margins

Retail buyers fragmented (65m clients in 2023), limited negotiation power; switching costs and cross‑sell reduce churn. Large corporates and brokers exert strong leverage via tenders; Generali counters with multinational servicing and 50,000+ agents (2024). Digital aggregators in 2024 increase price transparency, compressing motor/home margins.

| Segment | Bargaining | 2024 data |

|---|---|---|

| Retail | Low | 65m clients (2023) |

| Corporate/Brokers | High | Global tenders |

| Channels | Medium | 50,000+ agents (2024) |

Preview Before You Purchase

Assicurazioni Generali Porter's Five Forces Analysis

This Assicurazioni Generali Porter’s Five Forces analysis preview is the exact, professionally written document you’ll receive upon purchase—no mockups, no placeholders. It’s fully formatted and ready for download and immediate use the moment you buy. The file contains the complete competitive assessment and actionable insights for strategic decision-making.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Assicurazioni Generali faces moderate buyer power, tight regulatory and capital pressures, and evolving digital threats that reshape distribution and pricing. Competitive rivalry and insurtech substitutes intensify margin pressures and force strategic repositioning. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Reinsurers influence pricing and capacity

Generali relies on global reinsurers to manage peak risks and optimize capital, ceding a portion of premiums to secure excess-of-loss capacity; industry reports showed property catastrophe rate-on-line rose about 10% in 2023–24, tightening costs and terms. Diversified reinsurer panels and multi-year treaties reduce concentration risk. Rising catastrophe losses and climate trends have increased reinsurer leverage cyclically, pressuring pricing and capacity.

Critical tech and cloud vendors

Core policy admin, cloud, cybersecurity and AI providers are concentrated—top three cloud vendors control about 65% of IaaS/PaaS market (2024)—creating material switching costs and vendor lock‑in that raise migration risk and supplier leverage over pricing and SLAs. Generali mitigates this via multi‑cloud deployment, modular stacks and expanding in‑house tech teams. Regulatory pressure, notably DORA (operational resilience rules effective 2025), further constrains vendor substitution and mandates robust oversight.

Data and analytics providers

Access to credit bureaus, telematics, geospatial and health data sharpens Generali’s underwriting, while proprietary datasets command premium pricing and restrictive licenses that raise supplier leverage. Generali mitigates this by investing in internal data lakes and strategic partnerships to diversify sources. Privacy and localization rules, notably GDPR across 27 EU countries, constrain supplier pools and increase their bargaining power.

Specialist service networks

Healthcare providers, repair shops and loss adjusters materially influence claims cost and customer experience; Generali serves about 61 million customers (2023), giving it bargaining leverage in key markets.

In certain locales limited high-quality networks can command better rates and service-level agreements, tightening supplier power where alternatives are sparse.

Generali uses preferred provider networks, DRG-based tariffs and managed-care models, leveraging scale and client steerage to secure favorable terms and SLAs.

- 61 million customers (2023)

- Preferred networks, DRGs, managed care

- Scale + steerage = better rates & SLAs

Skilled actuarial and tech talent

Actuarial, data science and cyber talent are scarce and mobile, raising supplier leverage via wage inflation and retention packages; the global cybersecurity workforce gap remained about 3.4 million in 2024. Generali’s global brand, training initiatives and hybrid work attract and retain talent, with the Group employing ≈72,000 staff in 2024. Outsourcing and centers of excellence diversify the talent base, lowering concentration risk.

- Talent scarcity: cybersecurity gap ≈3.4M (2024)

- Retention pressure: rising pay and packages

- Mitigants: Generali training, hybrid work, outsourcing

Suppliers tighten; insurer counters with 61M scale, multi-cloud, data lakes

Suppliers (reinsurers, cloud, data, healthcare providers, talent) exert moderate-to-high power: reinsurer pricing rose ≈10% 2023–24; top 3 cloud vendors hold ≈65% IaaS/PaaS (2024); cybersecurity workforce gap ≈3.4M (2024). Generali offsets via scale (61M customers, 2023), multi‑cloud, in‑house data lakes and preferred networks; 72,000 employees (2024).

| Supplier | Power drivers | Mitigants | Data |

|---|---|---|---|

| Reinsurers | Capacity & pricing | Diversified panels | Rate-on-line +10% (2023–24) |

| Cloud/data | Concentration, licensing | Multi-cloud, internal lakes | Top3 ≈65% IaaS/PaaS (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Assicurazioni Generali, providing a detailed assessment of each Porter’s force with industry data and strategic implications. Identifies disruptive threats, substitutes, and buyer/supplier power that shape the company’s pricing power, margins, and defensive barriers to entry.

One-sheet Porter's Five Forces for Assicurazioni Generali—quickly benchmark rivalry, reinsurer/buyer power, insurtech threats and regulatory pressure to simplify strategic decisions and slide-ready outputs.

Customers Bargaining Power

Retail customers are fragmented

Retail customers are fragmented—Assicurazioni Generali serves around 65 million clients worldwide (2023), so individual policyholders lack scale to negotiate bespoke terms. Price sensitivity is high, but real switching costs exist via underwriting, medical checks and loyalty benefits, softening churn. Strong brand trust and claims service reduce pure price competition, and cross-selling/bundling of life, P&C and health further diminishes buyer power.

Corporate and institutional buyers are strong

Large corporates, fleets and employee-benefits clients exert strong bargaining power, negotiating coverage, limits and pricing; loss histories and brokered tenders intensify price competition. Global programs spanning 50+ countries increase buyer leverage through jurisdictional coordination. Generali, serving ~70 million customers, counters with risk engineering, captive solutions and dedicated multinational servicing.

Brokers and bancassurance channels shape terms

Brokers and bancassurance partners aggregate demand and steer placement, extracting commissions and service levels; global brokers (Marsh, Aon, WTW) dominate large commercial P&C negotiations and press for pricing and wording concessions. In 2024 Generali leveraged a network of over 50,000 agents plus direct digital channels to counter broker leverage, while bancassurance shelf space and revenue-sharing remained crucial for life and savings inflows.

Digital comparison heightens price transparency

Regulatory protections bolster buyer rights

Regulatory protections such as the EU IDD 14‑day cooling‑off period, conduct rules and mandated claims timelines strengthen buyer rights and constrain pricing flexibility. Remediation risks and required compensations increase the cost of poor service, bolstering customer bargaining power. Generali's 2024 annual report notes continued investment in compliance and customer care to reduce disputes.

- 14‑day cooling‑off (IDD)

- Conduct & claims timelines limit exclusions

- Remediation raises operational costs

- 2024: Generali ongoing compliance/customer care investments

Retail fragmented: 65m clients; aggregators raise transparency, squeeze margins

Retail buyers fragmented (65m clients in 2023), limited negotiation power; switching costs and cross‑sell reduce churn. Large corporates and brokers exert strong leverage via tenders; Generali counters with multinational servicing and 50,000+ agents (2024). Digital aggregators in 2024 increase price transparency, compressing motor/home margins.

| Segment | Bargaining | 2024 data |

|---|---|---|

| Retail | Low | 65m clients (2023) |

| Corporate/Brokers | High | Global tenders |

| Channels | Medium | 50,000+ agents (2024) |

Preview Before You Purchase

Assicurazioni Generali Porter's Five Forces Analysis

This Assicurazioni Generali Porter’s Five Forces analysis preview is the exact, professionally written document you’ll receive upon purchase—no mockups, no placeholders. It’s fully formatted and ready for download and immediate use the moment you buy. The file contains the complete competitive assessment and actionable insights for strategic decision-making.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Assicurazioni Generali faces moderate buyer power, tight regulatory and capital pressures, and evolving digital threats that reshape distribution and pricing. Competitive rivalry and insurtech substitutes intensify margin pressures and force strategic repositioning. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Reinsurers influence pricing and capacity

Generali relies on global reinsurers to manage peak risks and optimize capital, ceding a portion of premiums to secure excess-of-loss capacity; industry reports showed property catastrophe rate-on-line rose about 10% in 2023–24, tightening costs and terms. Diversified reinsurer panels and multi-year treaties reduce concentration risk. Rising catastrophe losses and climate trends have increased reinsurer leverage cyclically, pressuring pricing and capacity.

Critical tech and cloud vendors

Core policy admin, cloud, cybersecurity and AI providers are concentrated—top three cloud vendors control about 65% of IaaS/PaaS market (2024)—creating material switching costs and vendor lock‑in that raise migration risk and supplier leverage over pricing and SLAs. Generali mitigates this via multi‑cloud deployment, modular stacks and expanding in‑house tech teams. Regulatory pressure, notably DORA (operational resilience rules effective 2025), further constrains vendor substitution and mandates robust oversight.

Data and analytics providers

Access to credit bureaus, telematics, geospatial and health data sharpens Generali’s underwriting, while proprietary datasets command premium pricing and restrictive licenses that raise supplier leverage. Generali mitigates this by investing in internal data lakes and strategic partnerships to diversify sources. Privacy and localization rules, notably GDPR across 27 EU countries, constrain supplier pools and increase their bargaining power.

Specialist service networks

Healthcare providers, repair shops and loss adjusters materially influence claims cost and customer experience; Generali serves about 61 million customers (2023), giving it bargaining leverage in key markets.

In certain locales limited high-quality networks can command better rates and service-level agreements, tightening supplier power where alternatives are sparse.

Generali uses preferred provider networks, DRG-based tariffs and managed-care models, leveraging scale and client steerage to secure favorable terms and SLAs.

- 61 million customers (2023)

- Preferred networks, DRGs, managed care

- Scale + steerage = better rates & SLAs

Skilled actuarial and tech talent

Actuarial, data science and cyber talent are scarce and mobile, raising supplier leverage via wage inflation and retention packages; the global cybersecurity workforce gap remained about 3.4 million in 2024. Generali’s global brand, training initiatives and hybrid work attract and retain talent, with the Group employing ≈72,000 staff in 2024. Outsourcing and centers of excellence diversify the talent base, lowering concentration risk.

- Talent scarcity: cybersecurity gap ≈3.4M (2024)

- Retention pressure: rising pay and packages

- Mitigants: Generali training, hybrid work, outsourcing

Suppliers tighten; insurer counters with 61M scale, multi-cloud, data lakes

Suppliers (reinsurers, cloud, data, healthcare providers, talent) exert moderate-to-high power: reinsurer pricing rose ≈10% 2023–24; top 3 cloud vendors hold ≈65% IaaS/PaaS (2024); cybersecurity workforce gap ≈3.4M (2024). Generali offsets via scale (61M customers, 2023), multi‑cloud, in‑house data lakes and preferred networks; 72,000 employees (2024).

| Supplier | Power drivers | Mitigants | Data |

|---|---|---|---|

| Reinsurers | Capacity & pricing | Diversified panels | Rate-on-line +10% (2023–24) |

| Cloud/data | Concentration, licensing | Multi-cloud, internal lakes | Top3 ≈65% IaaS/PaaS (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Assicurazioni Generali, providing a detailed assessment of each Porter’s force with industry data and strategic implications. Identifies disruptive threats, substitutes, and buyer/supplier power that shape the company’s pricing power, margins, and defensive barriers to entry.

One-sheet Porter's Five Forces for Assicurazioni Generali—quickly benchmark rivalry, reinsurer/buyer power, insurtech threats and regulatory pressure to simplify strategic decisions and slide-ready outputs.

Customers Bargaining Power

Retail customers are fragmented

Retail customers are fragmented—Assicurazioni Generali serves around 65 million clients worldwide (2023), so individual policyholders lack scale to negotiate bespoke terms. Price sensitivity is high, but real switching costs exist via underwriting, medical checks and loyalty benefits, softening churn. Strong brand trust and claims service reduce pure price competition, and cross-selling/bundling of life, P&C and health further diminishes buyer power.

Corporate and institutional buyers are strong

Large corporates, fleets and employee-benefits clients exert strong bargaining power, negotiating coverage, limits and pricing; loss histories and brokered tenders intensify price competition. Global programs spanning 50+ countries increase buyer leverage through jurisdictional coordination. Generali, serving ~70 million customers, counters with risk engineering, captive solutions and dedicated multinational servicing.

Brokers and bancassurance channels shape terms

Brokers and bancassurance partners aggregate demand and steer placement, extracting commissions and service levels; global brokers (Marsh, Aon, WTW) dominate large commercial P&C negotiations and press for pricing and wording concessions. In 2024 Generali leveraged a network of over 50,000 agents plus direct digital channels to counter broker leverage, while bancassurance shelf space and revenue-sharing remained crucial for life and savings inflows.

Digital comparison heightens price transparency

Regulatory protections bolster buyer rights

Regulatory protections such as the EU IDD 14‑day cooling‑off period, conduct rules and mandated claims timelines strengthen buyer rights and constrain pricing flexibility. Remediation risks and required compensations increase the cost of poor service, bolstering customer bargaining power. Generali's 2024 annual report notes continued investment in compliance and customer care to reduce disputes.

- 14‑day cooling‑off (IDD)

- Conduct & claims timelines limit exclusions

- Remediation raises operational costs

- 2024: Generali ongoing compliance/customer care investments

Retail fragmented: 65m clients; aggregators raise transparency, squeeze margins

Retail buyers fragmented (65m clients in 2023), limited negotiation power; switching costs and cross‑sell reduce churn. Large corporates and brokers exert strong leverage via tenders; Generali counters with multinational servicing and 50,000+ agents (2024). Digital aggregators in 2024 increase price transparency, compressing motor/home margins.

| Segment | Bargaining | 2024 data |

|---|---|---|

| Retail | Low | 65m clients (2023) |

| Corporate/Brokers | High | Global tenders |

| Channels | Medium | 50,000+ agents (2024) |

Preview Before You Purchase

Assicurazioni Generali Porter's Five Forces Analysis

This Assicurazioni Generali Porter’s Five Forces analysis preview is the exact, professionally written document you’ll receive upon purchase—no mockups, no placeholders. It’s fully formatted and ready for download and immediate use the moment you buy. The file contains the complete competitive assessment and actionable insights for strategic decision-making.