General Mills Porter's Five Forces Analysis

From Overview to Strategy Blueprint

General Mills faces intense competitive rivalry from large CPG peers and private labels, moderate buyer power driven by retail consolidation, low supplier leverage, a limited threat of new entrants due to scale requirements, and moderate substitution pressure from private-label and niche healthy brands. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore General Mills’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity input concentration

General Mills sources key inputs like grains, dairy, oils and proteins from large global commodity markets, diluting individual supplier leverage. Weather shocks and geopolitical disruptions in 2024 increased tightness and triggered price spikes in several crops. Hedging and multi-sourcing reduce but do not eliminate exposure. Continued agri-commodity volatility can shift bargaining power back to upstream suppliers.

Packaging and specialty inputs

Specialty ingredients, flavors, cultures and packaging resins/board often come from a narrow supplier set, with qualification times often exceeding 6 months, raising switching costs and modestly increasing supplier power; co-manufacturers for niche SKUs gain leverage when capacity is tight. Long-term contracts blunt volatility, but 2023–24 supply bottlenecks pushed input-cost pressure into the mid-single-digit percent range, shifting terms toward suppliers.

Scale and procurement leverage

General Mills' presence in over 100 countries and roughly $20 billion in 2024 net sales gives it aggregated buying power that pressures suppliers. Volume commitments, competitive bidding and should-cost analytics have driven procurement savings and compress supplier margins. Regional sourcing across multiple continents reduces single-supplier dependency. The company secures favorable lead times and premium service levels unavailable to smaller peers.

Logistics and energy dependencies

Freight, warehousing and energy materially raise General Mills delivered costs; the company cited persistent logistics inflation in FY24 as a key headwind, with U.S. diesel prices up roughly 15% year‑over‑year in 2024 (EIA), boosting carrier leverage when capacity tightens.

Network optimization and SKU rationalization mitigate some pressure but cannot erase systemic fuel or carrier constraints; surcharge pass‑through succeeds more in branded, inelastic categories than in commoditized channels.

- Freight exposure

- Diesel +15% (2024, EIA)

- Network offsets limited

- Surcharges easier in tight categories

ESG and compliance constraints

Rising 2024 sustainability standards (deforestation-free oils, regenerative agriculture) narrow eligible supplier pools, raising traceability and certification barriers that increase costs and bolster pricing power for compliant suppliers; General Mills FY2024 net sales were about $20.1 billion.

- Eligible suppliers: smaller pool, higher vetting

- Costs: certification/traceability increase input prices

- Mitigation: supplier co-investment to expand sustainable supply

Supplier squeeze: $20.1B sales, diesel +15% and mid-single-digit cost push

Supplier power is moderate: commodity scale and $20.1B 2024 sales give General Mills buying leverage, but 2023–24 crop shocks, hedging limits and narrow suppliers for specialties raise switching costs. Logistics (U.S. diesel +15% in 2024, EIA) and sustainability rules boost supplier negotiating leverage. Long-term contracts and multi-sourcing partially offset pressure.

| Metric | 2024 |

|---|---|

| Net sales | $20.1B |

| Diesel YoY | +15% (EIA) |

| Input-cost push | mid-single-digit % |

What is included in the product

Tailored Porter's Five Forces analysis of General Mills uncovering competitive intensity, buyer and supplier leverage, threat of substitutes, and entry barriers, with strategic insights on disruptive threats and pricing power to inform investor and management decisions.

Clear one-sheet Porter's Five Forces for General Mills—customize pressure levels and view an instant spider chart to pinpoint competitive pain points, ready to paste into pitch decks or integrate into dashboards without macros.

Customers Bargaining Power

Retailer consolidation

Large chains and mass merchandisers command shelf-space and demand disproportionate trade spend, with Walmart alone representing roughly 25% of US grocery sales in 2024, forcing suppliers to fund promotions and slotting fees. Their scale enables tougher pricing, slotting, and merchandising terms that compress margins. General Mills must meet these requirements to secure visibility and distribution, intensifying buyer power in mature categories.

Private label alternatives

Retailer private labels—now ~18–19% of US grocery sales in 2024—offer lower-priced substitutes across cereals, baking and snacks, forcing stronger price comparisons and lowering switching costs. Quality gains have increased promotional cadence and pressured list prices; General Mills defends share via brand equity but spent ~$1.2bn on marketing and $400m on innovation in 2024 to sustain premiums.

E-commerce and data transparency

Online marketplaces and click-and-collect raise price transparency and comparability—global retail e-commerce sales reached about 6.3 trillion USD in 2023, amplifying buyer visibility. Algorithmic merchandising and reviews steer traffic to best-value SKUs, concentrating demand. General Mills leverages DTC insights but remains exposed to platform referral fees (commonly 8–15%) and dynamic pricing. Digital shelves boost buyer power unless brands win on search and rich content.

Foodservice and distributor dynamics

Distributors aggregate demand for restaurants, schools and institutions, negotiating volume discounts and leveraging scale; Sysco and US Foods together control roughly 60% of U.S. broadline distribution in 2024, increasing buyer leverage. Menu cost sensitivities limit pass-through, squeezing margins, while contracts and product specs create partial lock-in but frequent rebids keep pressure high; buyer power is moderate to high by channel mix.

- Demand aggregation → stronger price leverage

- Menu price sensitivity → limited cost pass-through

- Contracts/specs → some lock-in, but rebids frequent

- Net buyer power: moderate–high (channel dependent)

Consumer price sensitivity

Inflation-driven spikes in food-at-home prices (peaking near 13% in 2022, easing to roughly 3% in 2024) raised elasticity in categories, pushing promo dependence and volume-driven strategies. Consumers rapidly trade down across brands, pack sizes and channels; loyalty programs and product innovation soften but do not remove price elasticity. Greater household sensitivity amplifies retailer bargaining power versus General Mills.

- Promo reliance up — manufacturers face volume pressure

- Trade-down behavior — private label gains share

- Loyalty/innovation — mitigates but not negates elasticity

- Retailers capture indirect end-buyer leverage

Retail concentration & private labels squeeze margins; e-commerce ≈$6.3T

Large retailers (Walmart ≈25% of US grocery sales in 2024) and mass merchandisers extract shelf, promo and slotting spend, compressing margins; private labels (~18–19% of US grocery, 2024) intensify price pressure. Digital channels (global retail e‑commerce ≈$6.3T in 2023) raise transparency; platform fees 8–15% and distributor concentration (Sysco+US Foods ≈60% broadline, 2024) further boost buyer leverage.

| Metric | Value (2024) |

|---|---|

| Walmart share | ≈25% US grocery |

| Private label | ≈18–19% US grocery |

| Marketing / Innovation spend | $1.2B / $400M |

| Distributor concentration | Sysco+US Foods ≈60% |

| Inflation (food at home) | ≈3% |

Preview the Actual Deliverable

General Mills Porter's Five Forces Analysis

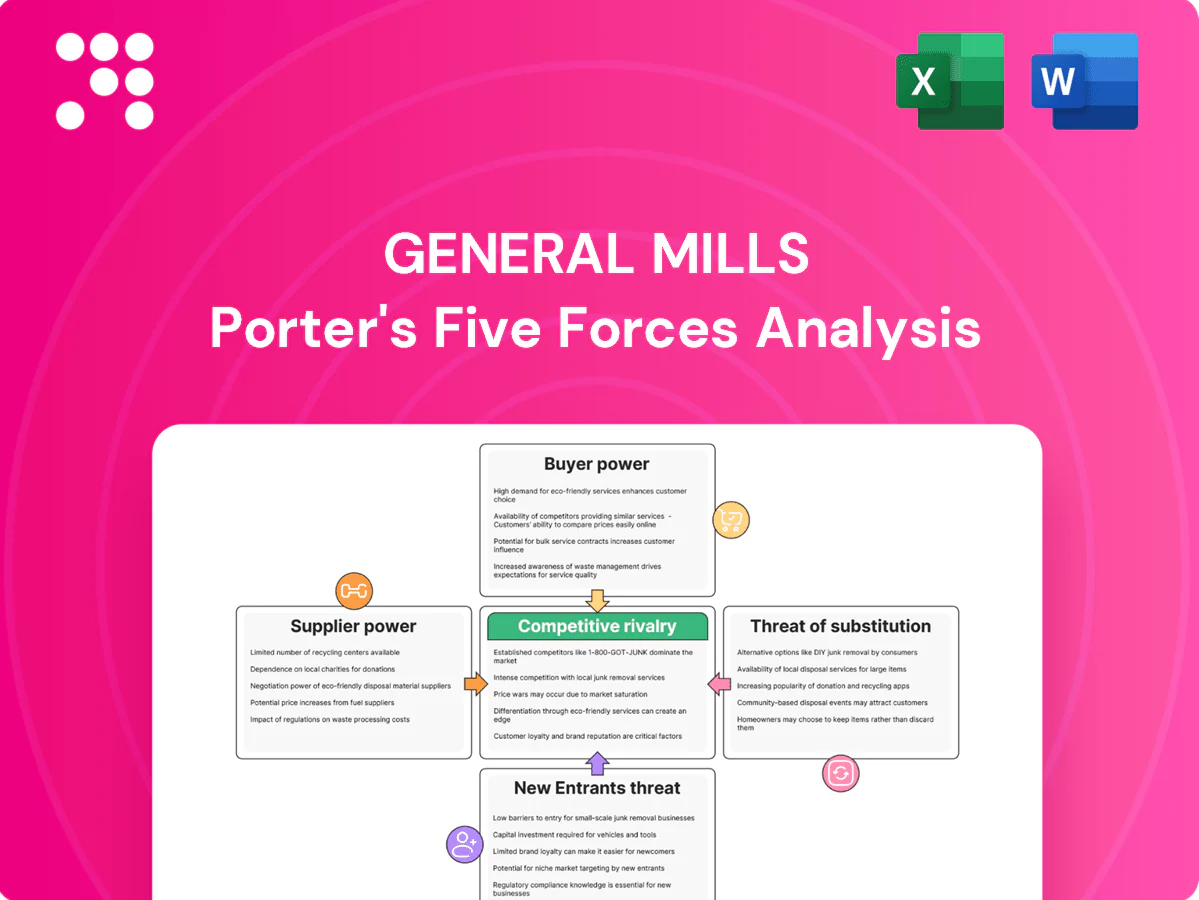

This preview shows the exact Porter's Five Forces analysis of General Mills you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes, with actionable strategic insights. You're looking at the actual document; once you buy, you'll get instant access to this same file.

From Overview to Strategy Blueprint

General Mills faces intense competitive rivalry from large CPG peers and private labels, moderate buyer power driven by retail consolidation, low supplier leverage, a limited threat of new entrants due to scale requirements, and moderate substitution pressure from private-label and niche healthy brands. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore General Mills’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity input concentration

General Mills sources key inputs like grains, dairy, oils and proteins from large global commodity markets, diluting individual supplier leverage. Weather shocks and geopolitical disruptions in 2024 increased tightness and triggered price spikes in several crops. Hedging and multi-sourcing reduce but do not eliminate exposure. Continued agri-commodity volatility can shift bargaining power back to upstream suppliers.

Packaging and specialty inputs

Specialty ingredients, flavors, cultures and packaging resins/board often come from a narrow supplier set, with qualification times often exceeding 6 months, raising switching costs and modestly increasing supplier power; co-manufacturers for niche SKUs gain leverage when capacity is tight. Long-term contracts blunt volatility, but 2023–24 supply bottlenecks pushed input-cost pressure into the mid-single-digit percent range, shifting terms toward suppliers.

Scale and procurement leverage

General Mills' presence in over 100 countries and roughly $20 billion in 2024 net sales gives it aggregated buying power that pressures suppliers. Volume commitments, competitive bidding and should-cost analytics have driven procurement savings and compress supplier margins. Regional sourcing across multiple continents reduces single-supplier dependency. The company secures favorable lead times and premium service levels unavailable to smaller peers.

Logistics and energy dependencies

Freight, warehousing and energy materially raise General Mills delivered costs; the company cited persistent logistics inflation in FY24 as a key headwind, with U.S. diesel prices up roughly 15% year‑over‑year in 2024 (EIA), boosting carrier leverage when capacity tightens.

Network optimization and SKU rationalization mitigate some pressure but cannot erase systemic fuel or carrier constraints; surcharge pass‑through succeeds more in branded, inelastic categories than in commoditized channels.

- Freight exposure

- Diesel +15% (2024, EIA)

- Network offsets limited

- Surcharges easier in tight categories

ESG and compliance constraints

Rising 2024 sustainability standards (deforestation-free oils, regenerative agriculture) narrow eligible supplier pools, raising traceability and certification barriers that increase costs and bolster pricing power for compliant suppliers; General Mills FY2024 net sales were about $20.1 billion.

- Eligible suppliers: smaller pool, higher vetting

- Costs: certification/traceability increase input prices

- Mitigation: supplier co-investment to expand sustainable supply

Supplier squeeze: $20.1B sales, diesel +15% and mid-single-digit cost push

Supplier power is moderate: commodity scale and $20.1B 2024 sales give General Mills buying leverage, but 2023–24 crop shocks, hedging limits and narrow suppliers for specialties raise switching costs. Logistics (U.S. diesel +15% in 2024, EIA) and sustainability rules boost supplier negotiating leverage. Long-term contracts and multi-sourcing partially offset pressure.

| Metric | 2024 |

|---|---|

| Net sales | $20.1B |

| Diesel YoY | +15% (EIA) |

| Input-cost push | mid-single-digit % |

What is included in the product

Tailored Porter's Five Forces analysis of General Mills uncovering competitive intensity, buyer and supplier leverage, threat of substitutes, and entry barriers, with strategic insights on disruptive threats and pricing power to inform investor and management decisions.

Clear one-sheet Porter's Five Forces for General Mills—customize pressure levels and view an instant spider chart to pinpoint competitive pain points, ready to paste into pitch decks or integrate into dashboards without macros.

Customers Bargaining Power

Retailer consolidation

Large chains and mass merchandisers command shelf-space and demand disproportionate trade spend, with Walmart alone representing roughly 25% of US grocery sales in 2024, forcing suppliers to fund promotions and slotting fees. Their scale enables tougher pricing, slotting, and merchandising terms that compress margins. General Mills must meet these requirements to secure visibility and distribution, intensifying buyer power in mature categories.

Private label alternatives

Retailer private labels—now ~18–19% of US grocery sales in 2024—offer lower-priced substitutes across cereals, baking and snacks, forcing stronger price comparisons and lowering switching costs. Quality gains have increased promotional cadence and pressured list prices; General Mills defends share via brand equity but spent ~$1.2bn on marketing and $400m on innovation in 2024 to sustain premiums.

E-commerce and data transparency

Online marketplaces and click-and-collect raise price transparency and comparability—global retail e-commerce sales reached about 6.3 trillion USD in 2023, amplifying buyer visibility. Algorithmic merchandising and reviews steer traffic to best-value SKUs, concentrating demand. General Mills leverages DTC insights but remains exposed to platform referral fees (commonly 8–15%) and dynamic pricing. Digital shelves boost buyer power unless brands win on search and rich content.

Foodservice and distributor dynamics

Distributors aggregate demand for restaurants, schools and institutions, negotiating volume discounts and leveraging scale; Sysco and US Foods together control roughly 60% of U.S. broadline distribution in 2024, increasing buyer leverage. Menu cost sensitivities limit pass-through, squeezing margins, while contracts and product specs create partial lock-in but frequent rebids keep pressure high; buyer power is moderate to high by channel mix.

- Demand aggregation → stronger price leverage

- Menu price sensitivity → limited cost pass-through

- Contracts/specs → some lock-in, but rebids frequent

- Net buyer power: moderate–high (channel dependent)

Consumer price sensitivity

Inflation-driven spikes in food-at-home prices (peaking near 13% in 2022, easing to roughly 3% in 2024) raised elasticity in categories, pushing promo dependence and volume-driven strategies. Consumers rapidly trade down across brands, pack sizes and channels; loyalty programs and product innovation soften but do not remove price elasticity. Greater household sensitivity amplifies retailer bargaining power versus General Mills.

- Promo reliance up — manufacturers face volume pressure

- Trade-down behavior — private label gains share

- Loyalty/innovation — mitigates but not negates elasticity

- Retailers capture indirect end-buyer leverage

Retail concentration & private labels squeeze margins; e-commerce ≈$6.3T

Large retailers (Walmart ≈25% of US grocery sales in 2024) and mass merchandisers extract shelf, promo and slotting spend, compressing margins; private labels (~18–19% of US grocery, 2024) intensify price pressure. Digital channels (global retail e‑commerce ≈$6.3T in 2023) raise transparency; platform fees 8–15% and distributor concentration (Sysco+US Foods ≈60% broadline, 2024) further boost buyer leverage.

| Metric | Value (2024) |

|---|---|

| Walmart share | ≈25% US grocery |

| Private label | ≈18–19% US grocery |

| Marketing / Innovation spend | $1.2B / $400M |

| Distributor concentration | Sysco+US Foods ≈60% |

| Inflation (food at home) | ≈3% |

Preview the Actual Deliverable

General Mills Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of General Mills you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes, with actionable strategic insights. You're looking at the actual document; once you buy, you'll get instant access to this same file.

Description

From Overview to Strategy Blueprint

General Mills faces intense competitive rivalry from large CPG peers and private labels, moderate buyer power driven by retail consolidation, low supplier leverage, a limited threat of new entrants due to scale requirements, and moderate substitution pressure from private-label and niche healthy brands. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore General Mills’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity input concentration

General Mills sources key inputs like grains, dairy, oils and proteins from large global commodity markets, diluting individual supplier leverage. Weather shocks and geopolitical disruptions in 2024 increased tightness and triggered price spikes in several crops. Hedging and multi-sourcing reduce but do not eliminate exposure. Continued agri-commodity volatility can shift bargaining power back to upstream suppliers.

Packaging and specialty inputs

Specialty ingredients, flavors, cultures and packaging resins/board often come from a narrow supplier set, with qualification times often exceeding 6 months, raising switching costs and modestly increasing supplier power; co-manufacturers for niche SKUs gain leverage when capacity is tight. Long-term contracts blunt volatility, but 2023–24 supply bottlenecks pushed input-cost pressure into the mid-single-digit percent range, shifting terms toward suppliers.

Scale and procurement leverage

General Mills' presence in over 100 countries and roughly $20 billion in 2024 net sales gives it aggregated buying power that pressures suppliers. Volume commitments, competitive bidding and should-cost analytics have driven procurement savings and compress supplier margins. Regional sourcing across multiple continents reduces single-supplier dependency. The company secures favorable lead times and premium service levels unavailable to smaller peers.

Logistics and energy dependencies

Freight, warehousing and energy materially raise General Mills delivered costs; the company cited persistent logistics inflation in FY24 as a key headwind, with U.S. diesel prices up roughly 15% year‑over‑year in 2024 (EIA), boosting carrier leverage when capacity tightens.

Network optimization and SKU rationalization mitigate some pressure but cannot erase systemic fuel or carrier constraints; surcharge pass‑through succeeds more in branded, inelastic categories than in commoditized channels.

- Freight exposure

- Diesel +15% (2024, EIA)

- Network offsets limited

- Surcharges easier in tight categories

ESG and compliance constraints

Rising 2024 sustainability standards (deforestation-free oils, regenerative agriculture) narrow eligible supplier pools, raising traceability and certification barriers that increase costs and bolster pricing power for compliant suppliers; General Mills FY2024 net sales were about $20.1 billion.

- Eligible suppliers: smaller pool, higher vetting

- Costs: certification/traceability increase input prices

- Mitigation: supplier co-investment to expand sustainable supply

Supplier squeeze: $20.1B sales, diesel +15% and mid-single-digit cost push

Supplier power is moderate: commodity scale and $20.1B 2024 sales give General Mills buying leverage, but 2023–24 crop shocks, hedging limits and narrow suppliers for specialties raise switching costs. Logistics (U.S. diesel +15% in 2024, EIA) and sustainability rules boost supplier negotiating leverage. Long-term contracts and multi-sourcing partially offset pressure.

| Metric | 2024 |

|---|---|

| Net sales | $20.1B |

| Diesel YoY | +15% (EIA) |

| Input-cost push | mid-single-digit % |

What is included in the product

Tailored Porter's Five Forces analysis of General Mills uncovering competitive intensity, buyer and supplier leverage, threat of substitutes, and entry barriers, with strategic insights on disruptive threats and pricing power to inform investor and management decisions.

Clear one-sheet Porter's Five Forces for General Mills—customize pressure levels and view an instant spider chart to pinpoint competitive pain points, ready to paste into pitch decks or integrate into dashboards without macros.

Customers Bargaining Power

Retailer consolidation

Large chains and mass merchandisers command shelf-space and demand disproportionate trade spend, with Walmart alone representing roughly 25% of US grocery sales in 2024, forcing suppliers to fund promotions and slotting fees. Their scale enables tougher pricing, slotting, and merchandising terms that compress margins. General Mills must meet these requirements to secure visibility and distribution, intensifying buyer power in mature categories.

Private label alternatives

Retailer private labels—now ~18–19% of US grocery sales in 2024—offer lower-priced substitutes across cereals, baking and snacks, forcing stronger price comparisons and lowering switching costs. Quality gains have increased promotional cadence and pressured list prices; General Mills defends share via brand equity but spent ~$1.2bn on marketing and $400m on innovation in 2024 to sustain premiums.

E-commerce and data transparency

Online marketplaces and click-and-collect raise price transparency and comparability—global retail e-commerce sales reached about 6.3 trillion USD in 2023, amplifying buyer visibility. Algorithmic merchandising and reviews steer traffic to best-value SKUs, concentrating demand. General Mills leverages DTC insights but remains exposed to platform referral fees (commonly 8–15%) and dynamic pricing. Digital shelves boost buyer power unless brands win on search and rich content.

Foodservice and distributor dynamics

Distributors aggregate demand for restaurants, schools and institutions, negotiating volume discounts and leveraging scale; Sysco and US Foods together control roughly 60% of U.S. broadline distribution in 2024, increasing buyer leverage. Menu cost sensitivities limit pass-through, squeezing margins, while contracts and product specs create partial lock-in but frequent rebids keep pressure high; buyer power is moderate to high by channel mix.

- Demand aggregation → stronger price leverage

- Menu price sensitivity → limited cost pass-through

- Contracts/specs → some lock-in, but rebids frequent

- Net buyer power: moderate–high (channel dependent)

Consumer price sensitivity

Inflation-driven spikes in food-at-home prices (peaking near 13% in 2022, easing to roughly 3% in 2024) raised elasticity in categories, pushing promo dependence and volume-driven strategies. Consumers rapidly trade down across brands, pack sizes and channels; loyalty programs and product innovation soften but do not remove price elasticity. Greater household sensitivity amplifies retailer bargaining power versus General Mills.

- Promo reliance up — manufacturers face volume pressure

- Trade-down behavior — private label gains share

- Loyalty/innovation — mitigates but not negates elasticity

- Retailers capture indirect end-buyer leverage

Retail concentration & private labels squeeze margins; e-commerce ≈$6.3T

Large retailers (Walmart ≈25% of US grocery sales in 2024) and mass merchandisers extract shelf, promo and slotting spend, compressing margins; private labels (~18–19% of US grocery, 2024) intensify price pressure. Digital channels (global retail e‑commerce ≈$6.3T in 2023) raise transparency; platform fees 8–15% and distributor concentration (Sysco+US Foods ≈60% broadline, 2024) further boost buyer leverage.

| Metric | Value (2024) |

|---|---|

| Walmart share | ≈25% US grocery |

| Private label | ≈18–19% US grocery |

| Marketing / Innovation spend | $1.2B / $400M |

| Distributor concentration | Sysco+US Foods ≈60% |

| Inflation (food at home) | ≈3% |

Preview the Actual Deliverable

General Mills Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of General Mills you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes, with actionable strategic insights. You're looking at the actual document; once you buy, you'll get instant access to this same file.