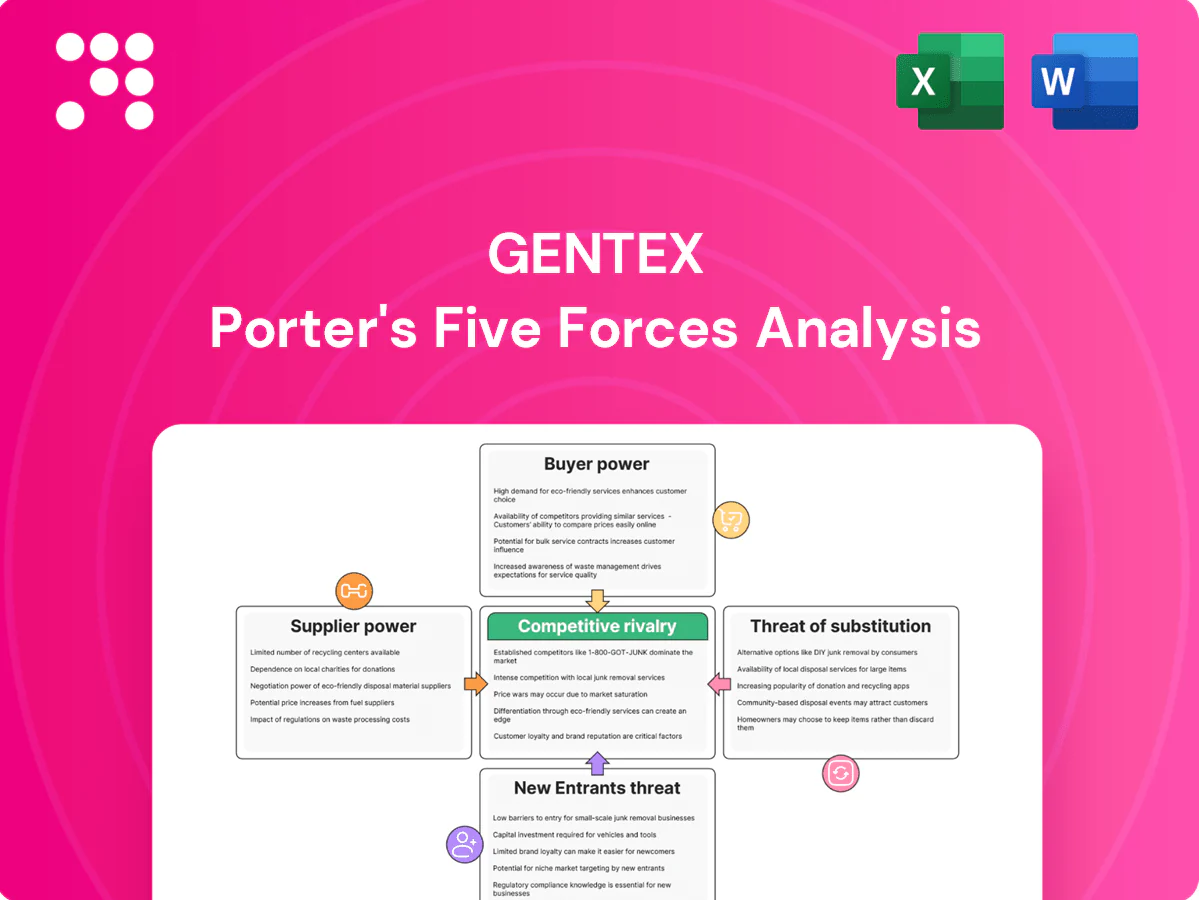

Gentex Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Gentex faces moderate supplier power, high buyer sensitivity, and intense rivalry as automotive OEMs demand tech-led, cost-effective electronic solutions; threat of new entrants is limited but substitute technologies and rapid innovation raise strategic risk. This snapshot highlights key pressure points and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Gentex’s competitive dynamics and market pressures in depth.

Suppliers Bargaining Power

Specialty materials dependence

Gentex relies on electrochromic chemicals, coated glass, optical films and automotive-grade semiconductors that often have fewer than 3 qualified suppliers, increasing supplier leverage. Material purity and batch consistency are essential for safety certifications (IATF/ISO) and failure rates under 0.1% are required. Dual-qualification reduces risk but typically extends qualification timelines by 6–12 months.

Automotive-grade component scarcity

Camera sensors, ASICs, automotive-grade microcontrollers and AEC/Q connectors are concentrated among a handful of global suppliers, creating supplier power that can compress supply during node transitions or supply shocks. Shortages and technology node shifts have pushed lead times into the 20–52 week range, lifting prices and planning risk. Gentex mitigates via inventory buffers and multi-sourcing where feasible.

Certification and compliance lock-in

Certification and compliance lock-in is significant: aerospace/automotive suppliers must meet PPAP submission levels (1–5), AS9100 certification and OEM-specific specs, creating stickiness to approved vendors. Requalifying a new source requires extensive testing and revalidation, raising switching costs and giving approved suppliers negotiation room. Long-term OEM agreements further stabilize terms.

Input cost volatility

Metals, rare coatings and specialty chemicals face pronounced price swings and geopolitical risk; LME copper averaged roughly $9,500/tonne in 2024, underscoring input volatility.

Suppliers often pass costs through via indexed contracts, increasing Gentex margin-compression risk in tight cycles.

Gentex mitigates impact through hedging programs and value-engineering initiatives to preserve gross margins.

- Indexed contracts: higher pass-through risk

- 2024 LME copper ~ $9,500/tonne

- Hedging + value engineering reduce volatility exposure

Limited backward integration

Gentex designs and manufactures extensively but remains dependent on upstream materials and wafers it does not produce; full backward integration is capital intensive and slow, preserving supplier bargaining power. Semiconductor fabs cost billions—TSMC capex 2024 was about $36 billion—making in‑house wafer capacity prohibitive for most suppliers. Strategic partnerships are used to secure capacity and co‑develop specs with key vendors.

- Dependence on external wafers and materials

- Fab builds cost billions (TSMC capex 2024 ≈ $36B)

- Partnerships secure capacity and technical alignment

Concentrated suppliers, 20–52 week lead times raise cost and pass-through risks

Suppliers of electrochromic chemicals, coated glass and automotive semiconductors are highly concentrated, giving vendors strong leverage and high switching costs due to OEM/PPAP requalification. Lead times for key components rose to 20–52 weeks in recent cycles, pressuring margins. Indexed contracts and raw-material volatility (LME copper ~ $9,500/tonne in 2024) raise pass-through risk; hedging and value engineering mitigate exposure.

| Metric | 2024 |

|---|---|

| Supplier concentration | Few suppliers per part |

| Lead times | 20–52 weeks |

| LME copper | $9,500/tonne |

| TSMC capex | $36B |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to Gentex, evaluating substitutes and disruptive threats to its automotive and smart-home product lines and highlighting strategic levers to protect pricing and profitability.

One-sheet Gentex Porter's Five Forces summary for rapid strategic decisions, with customizable pressure levels and a clear spider chart to instantly reveal competitive pain points. Clean, slide-ready layout—no macros—so teams can swap in current data and drop the analysis straight into decks or dashboards.

Customers Bargaining Power

Concentrated OEM customers

Global automakers and Tier‑1 platforms drive large volumes and exert strong pricing pressure—RFQs and annual cost‑down expectations are standard—so losing a platform can meaningfully dent utilization; Gentex reported $1.68B revenue in 2024, reflecting exposure to OEM concentration. Gentex mitigates this through differentiated features (auto‑dimming mirrors, integrated cameras) and consistently high quality scores that help retain business and defend margins.

Design-in switching costs

As of 2024, once a mirror or vision module is validated OEMs avoid mid-cycle supplier changes because retooling costs, integration time and warranty exposure sharply raise program risk, reducing buyer leverage post-award. At model refresh the competitive process resets as OEMs solicit new architectures and cost targets. Roadmaps and co-development partnerships increase likelihood of re-awards by embedding suppliers into vehicle design cycles.

Buyer access to alternatives

OEMs can dual-source mirrors and ADAS components, increasing buyer leverage as suppliers vie for platform wins. Benchmarking and teardowns by OEMs and tier-1s keep pricing disciplined and accelerate cost convergence. Buyers frequently trade features for cost targets, pressuring margins. Gentex counters with deep integration, proven reliability, and patented IP that raise switching costs.

Aftermarket and aviation mix

Aviation window customers and fire protection channels are dispersed and push on lifecycle costs and certifications; airlines and airframers prioritize reliability and support, reducing pure price pressure. Gentex reported fiscal 2024 net sales of $1.37 billion, with aviation and aftermarket a smaller, higher-margin mix. Aftermarket margins and service agreements shift value toward lifecycle revenues.

- Concentrated buyers: low

- Lifecycle focus: high

- 2024 net sales: 1.37B

- Aftermarket: higher margin, smaller scale

Quality and warranty leverage

OEMs tie pricing and future awards to PPM, field returns and software update responsiveness; many OEMs target PPM <50 and field return rates <0.5%, with software SLAs of 30–90 days, creating direct financial exposure. Buyers demand concessions for deviations; strong operations and data-driven quality analytics reduce penalty risk and protect margins.

- PPM target: <50

- Field returns: <0.5%

- Software SLA: 30–90 days

- Data-driven QC lowers penalty exposure

OEM concentration pressures pricing; quality, features and dual-sourcing protect margins

Large OEMs exert strong pricing pressure—Gentex reported $1.68B revenue in 2024 and OEM concentration can sharply affect utilization; differentiated features and quality defend margins. Post‑award switching costs are high but dual‑sourcing and teardowns keep pricing disciplined; Gentex cites fiscal 2024 aviation/net sales $1.37B. OEM targets: PPM <50, field returns <0.5%, software SLA 30–90 days.

| Metric | 2024 |

|---|---|

| Total revenue | $1.68B |

| Aviation/net sales | $1.37B |

| PPM target | <50 |

| Field returns | <0.5% |

| Software SLA | 30–90 days |

What You See Is What You Get

Gentex Porter's Five Forces Analysis

This preview shows the exact Gentex Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, edits, or samples. The report examines supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, with data-driven insights and practical implications. It's fully formatted, professionally written, and ready for instant download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Gentex faces moderate supplier power, high buyer sensitivity, and intense rivalry as automotive OEMs demand tech-led, cost-effective electronic solutions; threat of new entrants is limited but substitute technologies and rapid innovation raise strategic risk. This snapshot highlights key pressure points and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Gentex’s competitive dynamics and market pressures in depth.

Suppliers Bargaining Power

Specialty materials dependence

Gentex relies on electrochromic chemicals, coated glass, optical films and automotive-grade semiconductors that often have fewer than 3 qualified suppliers, increasing supplier leverage. Material purity and batch consistency are essential for safety certifications (IATF/ISO) and failure rates under 0.1% are required. Dual-qualification reduces risk but typically extends qualification timelines by 6–12 months.

Automotive-grade component scarcity

Camera sensors, ASICs, automotive-grade microcontrollers and AEC/Q connectors are concentrated among a handful of global suppliers, creating supplier power that can compress supply during node transitions or supply shocks. Shortages and technology node shifts have pushed lead times into the 20–52 week range, lifting prices and planning risk. Gentex mitigates via inventory buffers and multi-sourcing where feasible.

Certification and compliance lock-in

Certification and compliance lock-in is significant: aerospace/automotive suppliers must meet PPAP submission levels (1–5), AS9100 certification and OEM-specific specs, creating stickiness to approved vendors. Requalifying a new source requires extensive testing and revalidation, raising switching costs and giving approved suppliers negotiation room. Long-term OEM agreements further stabilize terms.

Input cost volatility

Metals, rare coatings and specialty chemicals face pronounced price swings and geopolitical risk; LME copper averaged roughly $9,500/tonne in 2024, underscoring input volatility.

Suppliers often pass costs through via indexed contracts, increasing Gentex margin-compression risk in tight cycles.

Gentex mitigates impact through hedging programs and value-engineering initiatives to preserve gross margins.

- Indexed contracts: higher pass-through risk

- 2024 LME copper ~ $9,500/tonne

- Hedging + value engineering reduce volatility exposure

Limited backward integration

Gentex designs and manufactures extensively but remains dependent on upstream materials and wafers it does not produce; full backward integration is capital intensive and slow, preserving supplier bargaining power. Semiconductor fabs cost billions—TSMC capex 2024 was about $36 billion—making in‑house wafer capacity prohibitive for most suppliers. Strategic partnerships are used to secure capacity and co‑develop specs with key vendors.

- Dependence on external wafers and materials

- Fab builds cost billions (TSMC capex 2024 ≈ $36B)

- Partnerships secure capacity and technical alignment

Concentrated suppliers, 20–52 week lead times raise cost and pass-through risks

Suppliers of electrochromic chemicals, coated glass and automotive semiconductors are highly concentrated, giving vendors strong leverage and high switching costs due to OEM/PPAP requalification. Lead times for key components rose to 20–52 weeks in recent cycles, pressuring margins. Indexed contracts and raw-material volatility (LME copper ~ $9,500/tonne in 2024) raise pass-through risk; hedging and value engineering mitigate exposure.

| Metric | 2024 |

|---|---|

| Supplier concentration | Few suppliers per part |

| Lead times | 20–52 weeks |

| LME copper | $9,500/tonne |

| TSMC capex | $36B |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to Gentex, evaluating substitutes and disruptive threats to its automotive and smart-home product lines and highlighting strategic levers to protect pricing and profitability.

One-sheet Gentex Porter's Five Forces summary for rapid strategic decisions, with customizable pressure levels and a clear spider chart to instantly reveal competitive pain points. Clean, slide-ready layout—no macros—so teams can swap in current data and drop the analysis straight into decks or dashboards.

Customers Bargaining Power

Concentrated OEM customers

Global automakers and Tier‑1 platforms drive large volumes and exert strong pricing pressure—RFQs and annual cost‑down expectations are standard—so losing a platform can meaningfully dent utilization; Gentex reported $1.68B revenue in 2024, reflecting exposure to OEM concentration. Gentex mitigates this through differentiated features (auto‑dimming mirrors, integrated cameras) and consistently high quality scores that help retain business and defend margins.

Design-in switching costs

As of 2024, once a mirror or vision module is validated OEMs avoid mid-cycle supplier changes because retooling costs, integration time and warranty exposure sharply raise program risk, reducing buyer leverage post-award. At model refresh the competitive process resets as OEMs solicit new architectures and cost targets. Roadmaps and co-development partnerships increase likelihood of re-awards by embedding suppliers into vehicle design cycles.

Buyer access to alternatives

OEMs can dual-source mirrors and ADAS components, increasing buyer leverage as suppliers vie for platform wins. Benchmarking and teardowns by OEMs and tier-1s keep pricing disciplined and accelerate cost convergence. Buyers frequently trade features for cost targets, pressuring margins. Gentex counters with deep integration, proven reliability, and patented IP that raise switching costs.

Aftermarket and aviation mix

Aviation window customers and fire protection channels are dispersed and push on lifecycle costs and certifications; airlines and airframers prioritize reliability and support, reducing pure price pressure. Gentex reported fiscal 2024 net sales of $1.37 billion, with aviation and aftermarket a smaller, higher-margin mix. Aftermarket margins and service agreements shift value toward lifecycle revenues.

- Concentrated buyers: low

- Lifecycle focus: high

- 2024 net sales: 1.37B

- Aftermarket: higher margin, smaller scale

Quality and warranty leverage

OEMs tie pricing and future awards to PPM, field returns and software update responsiveness; many OEMs target PPM <50 and field return rates <0.5%, with software SLAs of 30–90 days, creating direct financial exposure. Buyers demand concessions for deviations; strong operations and data-driven quality analytics reduce penalty risk and protect margins.

- PPM target: <50

- Field returns: <0.5%

- Software SLA: 30–90 days

- Data-driven QC lowers penalty exposure

OEM concentration pressures pricing; quality, features and dual-sourcing protect margins

Large OEMs exert strong pricing pressure—Gentex reported $1.68B revenue in 2024 and OEM concentration can sharply affect utilization; differentiated features and quality defend margins. Post‑award switching costs are high but dual‑sourcing and teardowns keep pricing disciplined; Gentex cites fiscal 2024 aviation/net sales $1.37B. OEM targets: PPM <50, field returns <0.5%, software SLA 30–90 days.

| Metric | 2024 |

|---|---|

| Total revenue | $1.68B |

| Aviation/net sales | $1.37B |

| PPM target | <50 |

| Field returns | <0.5% |

| Software SLA | 30–90 days |

What You See Is What You Get

Gentex Porter's Five Forces Analysis

This preview shows the exact Gentex Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, edits, or samples. The report examines supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, with data-driven insights and practical implications. It's fully formatted, professionally written, and ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Gentex faces moderate supplier power, high buyer sensitivity, and intense rivalry as automotive OEMs demand tech-led, cost-effective electronic solutions; threat of new entrants is limited but substitute technologies and rapid innovation raise strategic risk. This snapshot highlights key pressure points and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Gentex’s competitive dynamics and market pressures in depth.

Suppliers Bargaining Power

Specialty materials dependence

Gentex relies on electrochromic chemicals, coated glass, optical films and automotive-grade semiconductors that often have fewer than 3 qualified suppliers, increasing supplier leverage. Material purity and batch consistency are essential for safety certifications (IATF/ISO) and failure rates under 0.1% are required. Dual-qualification reduces risk but typically extends qualification timelines by 6–12 months.

Automotive-grade component scarcity

Camera sensors, ASICs, automotive-grade microcontrollers and AEC/Q connectors are concentrated among a handful of global suppliers, creating supplier power that can compress supply during node transitions or supply shocks. Shortages and technology node shifts have pushed lead times into the 20–52 week range, lifting prices and planning risk. Gentex mitigates via inventory buffers and multi-sourcing where feasible.

Certification and compliance lock-in

Certification and compliance lock-in is significant: aerospace/automotive suppliers must meet PPAP submission levels (1–5), AS9100 certification and OEM-specific specs, creating stickiness to approved vendors. Requalifying a new source requires extensive testing and revalidation, raising switching costs and giving approved suppliers negotiation room. Long-term OEM agreements further stabilize terms.

Input cost volatility

Metals, rare coatings and specialty chemicals face pronounced price swings and geopolitical risk; LME copper averaged roughly $9,500/tonne in 2024, underscoring input volatility.

Suppliers often pass costs through via indexed contracts, increasing Gentex margin-compression risk in tight cycles.

Gentex mitigates impact through hedging programs and value-engineering initiatives to preserve gross margins.

- Indexed contracts: higher pass-through risk

- 2024 LME copper ~ $9,500/tonne

- Hedging + value engineering reduce volatility exposure

Limited backward integration

Gentex designs and manufactures extensively but remains dependent on upstream materials and wafers it does not produce; full backward integration is capital intensive and slow, preserving supplier bargaining power. Semiconductor fabs cost billions—TSMC capex 2024 was about $36 billion—making in‑house wafer capacity prohibitive for most suppliers. Strategic partnerships are used to secure capacity and co‑develop specs with key vendors.

- Dependence on external wafers and materials

- Fab builds cost billions (TSMC capex 2024 ≈ $36B)

- Partnerships secure capacity and technical alignment

Concentrated suppliers, 20–52 week lead times raise cost and pass-through risks

Suppliers of electrochromic chemicals, coated glass and automotive semiconductors are highly concentrated, giving vendors strong leverage and high switching costs due to OEM/PPAP requalification. Lead times for key components rose to 20–52 weeks in recent cycles, pressuring margins. Indexed contracts and raw-material volatility (LME copper ~ $9,500/tonne in 2024) raise pass-through risk; hedging and value engineering mitigate exposure.

| Metric | 2024 |

|---|---|

| Supplier concentration | Few suppliers per part |

| Lead times | 20–52 weeks |

| LME copper | $9,500/tonne |

| TSMC capex | $36B |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks specific to Gentex, evaluating substitutes and disruptive threats to its automotive and smart-home product lines and highlighting strategic levers to protect pricing and profitability.

One-sheet Gentex Porter's Five Forces summary for rapid strategic decisions, with customizable pressure levels and a clear spider chart to instantly reveal competitive pain points. Clean, slide-ready layout—no macros—so teams can swap in current data and drop the analysis straight into decks or dashboards.

Customers Bargaining Power

Concentrated OEM customers

Global automakers and Tier‑1 platforms drive large volumes and exert strong pricing pressure—RFQs and annual cost‑down expectations are standard—so losing a platform can meaningfully dent utilization; Gentex reported $1.68B revenue in 2024, reflecting exposure to OEM concentration. Gentex mitigates this through differentiated features (auto‑dimming mirrors, integrated cameras) and consistently high quality scores that help retain business and defend margins.

Design-in switching costs

As of 2024, once a mirror or vision module is validated OEMs avoid mid-cycle supplier changes because retooling costs, integration time and warranty exposure sharply raise program risk, reducing buyer leverage post-award. At model refresh the competitive process resets as OEMs solicit new architectures and cost targets. Roadmaps and co-development partnerships increase likelihood of re-awards by embedding suppliers into vehicle design cycles.

Buyer access to alternatives

OEMs can dual-source mirrors and ADAS components, increasing buyer leverage as suppliers vie for platform wins. Benchmarking and teardowns by OEMs and tier-1s keep pricing disciplined and accelerate cost convergence. Buyers frequently trade features for cost targets, pressuring margins. Gentex counters with deep integration, proven reliability, and patented IP that raise switching costs.

Aftermarket and aviation mix

Aviation window customers and fire protection channels are dispersed and push on lifecycle costs and certifications; airlines and airframers prioritize reliability and support, reducing pure price pressure. Gentex reported fiscal 2024 net sales of $1.37 billion, with aviation and aftermarket a smaller, higher-margin mix. Aftermarket margins and service agreements shift value toward lifecycle revenues.

- Concentrated buyers: low

- Lifecycle focus: high

- 2024 net sales: 1.37B

- Aftermarket: higher margin, smaller scale

Quality and warranty leverage

OEMs tie pricing and future awards to PPM, field returns and software update responsiveness; many OEMs target PPM <50 and field return rates <0.5%, with software SLAs of 30–90 days, creating direct financial exposure. Buyers demand concessions for deviations; strong operations and data-driven quality analytics reduce penalty risk and protect margins.

- PPM target: <50

- Field returns: <0.5%

- Software SLA: 30–90 days

- Data-driven QC lowers penalty exposure

OEM concentration pressures pricing; quality, features and dual-sourcing protect margins

Large OEMs exert strong pricing pressure—Gentex reported $1.68B revenue in 2024 and OEM concentration can sharply affect utilization; differentiated features and quality defend margins. Post‑award switching costs are high but dual‑sourcing and teardowns keep pricing disciplined; Gentex cites fiscal 2024 aviation/net sales $1.37B. OEM targets: PPM <50, field returns <0.5%, software SLA 30–90 days.

| Metric | 2024 |

|---|---|

| Total revenue | $1.68B |

| Aviation/net sales | $1.37B |

| PPM target | <50 |

| Field returns | <0.5% |

| Software SLA | 30–90 days |

What You See Is What You Get

Gentex Porter's Five Forces Analysis

This preview shows the exact Gentex Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, edits, or samples. The report examines supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, with data-driven insights and practical implications. It's fully formatted, professionally written, and ready for instant download and use.