Genus Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

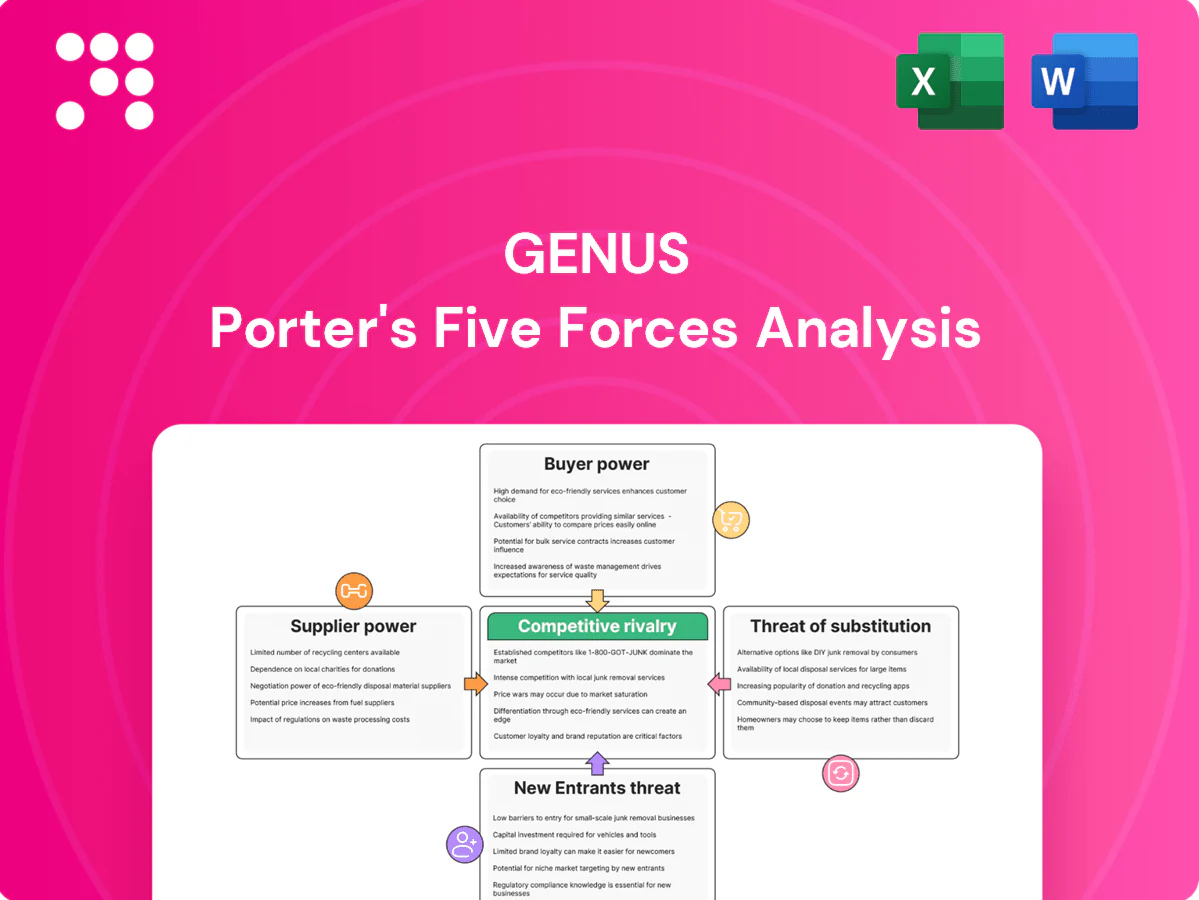

Genus faces nuanced competitive pressures across supplier bargaining, buyer power, substitute products, new entrants, and industry rivalry that shape its strategic choices and margins. This snapshot highlights key tensions but omits force-by-force ratings and tailored implications. Unlock the full Porter's Five Forces Analysis to explore Genus’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of elite genetic donors

Genus relies on scarce, time‑intensive elite donors from nucleus herds that take years to build, with dairy generation intervals around 3–4 years, giving upstream providers some leverage over access and terms. Genus’ owned nucleus assets and closed‑breeding programs across multiple global sites mitigate supplier dependence, and long genetic cycles reduce renegotiation frequency, moderating supplier power.

Specialized lab tech and consumables

Sexed semen sorters, cryopreservation media, genomic sequencing platforms and AI lab consumables are concentrated among a few vendors (Illumina ~65% sequencing FWA 2024; BD/Beckman top flow cytometry vendors), creating supplier leverage. Platform switches (sequencer or cytometer) often require validation and integration costs commonly ranging $50k–$500k plus 3–12 months of risk to throughput. That raises moderate supplier power via switching costs and quality differentiation, but multi-sourcing and in‑house process IP (proprietary sorting and assay protocols) cap that power.

Critical data and bioinformatics platforms

Genomic evaluations rely heavily on software, algorithms and cloud infrastructure, creating potential vendor lock-in from proprietary pipelines and legacy datasets. Genus’ in-house genetics teams and curated breeding data act as a strong counterbalance to platform providers. Adoption of interoperability standards and open-source tools like Nextflow reduces supplier leverage and eases migration.

Animal health, biosecurity, and logistics inputs

Animal health, biosecurity materials, liquid nitrogen and specialized transport are essential and time-sensitive inputs for Genus, but most categories have multiple competing suppliers which constrains supplier pricing power; temporary price spikes can occur during disease outbreaks or logistic shocks. Long-term contracts and high volumes allow Genus to negotiate favorable terms and prioritize continuity of supply.

- Veterinary biologics: multiple suppliers, limited pricing power

- Biosecurity materials: commoditized, competitive market

- Liquid nitrogen & transport: time-sensitive, outbreak-driven spikes

- Mitigation: long-term relationships and volume leverage

External IP and research partnerships

- Royalties: low‑single to mid‑teens %; 2024 R&D ≈ £75m; portfolio breadth cuts single‑source risk

Moderate supplier power: donor scarcity, dominant sequencers (~65%)

Genus faces moderate supplier power: elite donor access and concentrated lab platforms give leverage, but owned nucleus herds and in‑house genetics reduce dependence. Switching costs for sequencers/cytometers ($50k–$500k; 3–12 months) and IP royalties (low‑single to mid‑teens %) raise pressure. 2024 R&D ≈ £75m; Illumina ~65% sequencing share (2024).

| Input | Concentration | Impact | Mitigation |

|---|---|---|---|

| Sequencing | Illumina ~65% (2024) | High switching cost | In‑house pipelines |

| Donors/IP | Scarce donors; patents | Access/royalties | Owned herds; £75m R&D |

What is included in the product

Comprehensive Porter's Five Forces for Genus, detailing competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, plus disruptive risks and strategic levers to protect margins; fully editable for reports.

Genus Porter's Five Forces delivers a one-sheet, customizable summary with instant spider-chart visualization—streamlining strategic pressure assessment for quick decisions and slide-ready reporting.

Customers Bargaining Power

Consolidated large producers

Global pork integrators and large dairy/beef operations are consolidating: in the US the four largest beef packers control roughly 80–85% of slaughter capacity and the top four pork processors about 65–70% (2023–24), giving buyers strong price negotiation, vendor rationalization and performance-based contracting leverage. This elevates buyer power for commoditized SKUs, although Genus’s differentiated genetic gains and measurable ROI limit deep discounting.

High switching ease across genetics

Producers can switch among leading studs and breeding programs with relative ease over multi-year planning horizons, though contract cycles and biosecurity protocols limit immediate moves. Performance transparency and benchmarking platforms in 2024 intensified price comparisons and buyer leverage. Genus' 2024 annual report emphasizes proprietary lines, veterinary service and on-farm support to raise practical switching costs and protect margins.

Outcome-based purchasing

Customers now buy on outcomes—feed efficiency, fertility, calving ease, carcass quality and disease resilience—driving procurement toward warranties, on-farm trials and data-sharing that increase buyer leverage on contract terms. In 2024 Genus reported revenue of £1.1bn, letting buyers press for proof-of-performance; superior EBVs and genomic proof help Genus defend value-based pricing and justify premium margins.

Cyclical end-market sensitivity

Cyclical end-market sensitivity: livestock prices, feed costs (feed typically ~60% of production cost) and disease cycles directly compress customer margins, so in downturns buyers press for lower prices or defer genetic upgrades, increasing buyer power; counter-cyclical traits (survival, feed efficiency) and subscription-like supply programs smooth demand and reduce bargaining pressure.

- Feed ≈60% of costs

- Downturns → deferred upgrades

- Counter-cyclical genetics mitigate volatility

- Subscription programs stabilize orders

Alternative sourcing channels

Alternative sourcing via co-ops, regional studs and private herds gives buyers options beyond global leaders; access to comparable genetics varies by region and species, creating some leverage. Consistency, QA and delivery reliability still favor scaled providers, while Genus’ network across 30+ countries and strong biosecurity in 2024 reduces perceived risk of paying a premium.

- Co-ops/regional studs offer local access

- Buyer leverage varies by region/species

- Scale drives QA and delivery reliability

- Genus 30+ country footprint lowers risk of premium

Consolidation boosts buyer leverage; genetics firm £1.1bn, ≈60% feed cost

Consolidation (top4 beef 80–85%, pork 65–70% in 2023–24) and buyer focus on outcomes raise customer leverage, but Genus’ differentiated genetics, services and £1.1bn 2024 revenue limit deep discounting. Producers can switch over multi-year horizons; feed ≈60% of costs drives sensitivity. Genus’ 30+ country footprint and biosecurity reduce perceived premium risk.

| Metric | 2024 | Buyer power impact |

|---|---|---|

| Genus revenue | £1.1bn | Supports premium |

| Top4 beef/pork | 80–85% / 65–70% | Raises buyer leverage |

| Feed share | ≈60% | Increases price sensitivity |

| Global footprint | 30+ countries | Reduces switching risk |

Same Document Delivered

Genus Porter's Five Forces Analysis

This preview shows the exact Genus Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the professionally written, fully formatted deliverable, ready for download and use the moment you buy. You’re viewing the final file; once payment is completed, you’ll get instant access to this same document. No mockups or samples—this is the real deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Genus faces nuanced competitive pressures across supplier bargaining, buyer power, substitute products, new entrants, and industry rivalry that shape its strategic choices and margins. This snapshot highlights key tensions but omits force-by-force ratings and tailored implications. Unlock the full Porter's Five Forces Analysis to explore Genus’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of elite genetic donors

Genus relies on scarce, time‑intensive elite donors from nucleus herds that take years to build, with dairy generation intervals around 3–4 years, giving upstream providers some leverage over access and terms. Genus’ owned nucleus assets and closed‑breeding programs across multiple global sites mitigate supplier dependence, and long genetic cycles reduce renegotiation frequency, moderating supplier power.

Specialized lab tech and consumables

Sexed semen sorters, cryopreservation media, genomic sequencing platforms and AI lab consumables are concentrated among a few vendors (Illumina ~65% sequencing FWA 2024; BD/Beckman top flow cytometry vendors), creating supplier leverage. Platform switches (sequencer or cytometer) often require validation and integration costs commonly ranging $50k–$500k plus 3–12 months of risk to throughput. That raises moderate supplier power via switching costs and quality differentiation, but multi-sourcing and in‑house process IP (proprietary sorting and assay protocols) cap that power.

Critical data and bioinformatics platforms

Genomic evaluations rely heavily on software, algorithms and cloud infrastructure, creating potential vendor lock-in from proprietary pipelines and legacy datasets. Genus’ in-house genetics teams and curated breeding data act as a strong counterbalance to platform providers. Adoption of interoperability standards and open-source tools like Nextflow reduces supplier leverage and eases migration.

Animal health, biosecurity, and logistics inputs

Animal health, biosecurity materials, liquid nitrogen and specialized transport are essential and time-sensitive inputs for Genus, but most categories have multiple competing suppliers which constrains supplier pricing power; temporary price spikes can occur during disease outbreaks or logistic shocks. Long-term contracts and high volumes allow Genus to negotiate favorable terms and prioritize continuity of supply.

- Veterinary biologics: multiple suppliers, limited pricing power

- Biosecurity materials: commoditized, competitive market

- Liquid nitrogen & transport: time-sensitive, outbreak-driven spikes

- Mitigation: long-term relationships and volume leverage

External IP and research partnerships

- Royalties: low‑single to mid‑teens %; 2024 R&D ≈ £75m; portfolio breadth cuts single‑source risk

Moderate supplier power: donor scarcity, dominant sequencers (~65%)

Genus faces moderate supplier power: elite donor access and concentrated lab platforms give leverage, but owned nucleus herds and in‑house genetics reduce dependence. Switching costs for sequencers/cytometers ($50k–$500k; 3–12 months) and IP royalties (low‑single to mid‑teens %) raise pressure. 2024 R&D ≈ £75m; Illumina ~65% sequencing share (2024).

| Input | Concentration | Impact | Mitigation |

|---|---|---|---|

| Sequencing | Illumina ~65% (2024) | High switching cost | In‑house pipelines |

| Donors/IP | Scarce donors; patents | Access/royalties | Owned herds; £75m R&D |

What is included in the product

Comprehensive Porter's Five Forces for Genus, detailing competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, plus disruptive risks and strategic levers to protect margins; fully editable for reports.

Genus Porter's Five Forces delivers a one-sheet, customizable summary with instant spider-chart visualization—streamlining strategic pressure assessment for quick decisions and slide-ready reporting.

Customers Bargaining Power

Consolidated large producers

Global pork integrators and large dairy/beef operations are consolidating: in the US the four largest beef packers control roughly 80–85% of slaughter capacity and the top four pork processors about 65–70% (2023–24), giving buyers strong price negotiation, vendor rationalization and performance-based contracting leverage. This elevates buyer power for commoditized SKUs, although Genus’s differentiated genetic gains and measurable ROI limit deep discounting.

High switching ease across genetics

Producers can switch among leading studs and breeding programs with relative ease over multi-year planning horizons, though contract cycles and biosecurity protocols limit immediate moves. Performance transparency and benchmarking platforms in 2024 intensified price comparisons and buyer leverage. Genus' 2024 annual report emphasizes proprietary lines, veterinary service and on-farm support to raise practical switching costs and protect margins.

Outcome-based purchasing

Customers now buy on outcomes—feed efficiency, fertility, calving ease, carcass quality and disease resilience—driving procurement toward warranties, on-farm trials and data-sharing that increase buyer leverage on contract terms. In 2024 Genus reported revenue of £1.1bn, letting buyers press for proof-of-performance; superior EBVs and genomic proof help Genus defend value-based pricing and justify premium margins.

Cyclical end-market sensitivity

Cyclical end-market sensitivity: livestock prices, feed costs (feed typically ~60% of production cost) and disease cycles directly compress customer margins, so in downturns buyers press for lower prices or defer genetic upgrades, increasing buyer power; counter-cyclical traits (survival, feed efficiency) and subscription-like supply programs smooth demand and reduce bargaining pressure.

- Feed ≈60% of costs

- Downturns → deferred upgrades

- Counter-cyclical genetics mitigate volatility

- Subscription programs stabilize orders

Alternative sourcing channels

Alternative sourcing via co-ops, regional studs and private herds gives buyers options beyond global leaders; access to comparable genetics varies by region and species, creating some leverage. Consistency, QA and delivery reliability still favor scaled providers, while Genus’ network across 30+ countries and strong biosecurity in 2024 reduces perceived risk of paying a premium.

- Co-ops/regional studs offer local access

- Buyer leverage varies by region/species

- Scale drives QA and delivery reliability

- Genus 30+ country footprint lowers risk of premium

Consolidation boosts buyer leverage; genetics firm £1.1bn, ≈60% feed cost

Consolidation (top4 beef 80–85%, pork 65–70% in 2023–24) and buyer focus on outcomes raise customer leverage, but Genus’ differentiated genetics, services and £1.1bn 2024 revenue limit deep discounting. Producers can switch over multi-year horizons; feed ≈60% of costs drives sensitivity. Genus’ 30+ country footprint and biosecurity reduce perceived premium risk.

| Metric | 2024 | Buyer power impact |

|---|---|---|

| Genus revenue | £1.1bn | Supports premium |

| Top4 beef/pork | 80–85% / 65–70% | Raises buyer leverage |

| Feed share | ≈60% | Increases price sensitivity |

| Global footprint | 30+ countries | Reduces switching risk |

Same Document Delivered

Genus Porter's Five Forces Analysis

This preview shows the exact Genus Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the professionally written, fully formatted deliverable, ready for download and use the moment you buy. You’re viewing the final file; once payment is completed, you’ll get instant access to this same document. No mockups or samples—this is the real deliverable.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Genus faces nuanced competitive pressures across supplier bargaining, buyer power, substitute products, new entrants, and industry rivalry that shape its strategic choices and margins. This snapshot highlights key tensions but omits force-by-force ratings and tailored implications. Unlock the full Porter's Five Forces Analysis to explore Genus’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of elite genetic donors

Genus relies on scarce, time‑intensive elite donors from nucleus herds that take years to build, with dairy generation intervals around 3–4 years, giving upstream providers some leverage over access and terms. Genus’ owned nucleus assets and closed‑breeding programs across multiple global sites mitigate supplier dependence, and long genetic cycles reduce renegotiation frequency, moderating supplier power.

Specialized lab tech and consumables

Sexed semen sorters, cryopreservation media, genomic sequencing platforms and AI lab consumables are concentrated among a few vendors (Illumina ~65% sequencing FWA 2024; BD/Beckman top flow cytometry vendors), creating supplier leverage. Platform switches (sequencer or cytometer) often require validation and integration costs commonly ranging $50k–$500k plus 3–12 months of risk to throughput. That raises moderate supplier power via switching costs and quality differentiation, but multi-sourcing and in‑house process IP (proprietary sorting and assay protocols) cap that power.

Critical data and bioinformatics platforms

Genomic evaluations rely heavily on software, algorithms and cloud infrastructure, creating potential vendor lock-in from proprietary pipelines and legacy datasets. Genus’ in-house genetics teams and curated breeding data act as a strong counterbalance to platform providers. Adoption of interoperability standards and open-source tools like Nextflow reduces supplier leverage and eases migration.

Animal health, biosecurity, and logistics inputs

Animal health, biosecurity materials, liquid nitrogen and specialized transport are essential and time-sensitive inputs for Genus, but most categories have multiple competing suppliers which constrains supplier pricing power; temporary price spikes can occur during disease outbreaks or logistic shocks. Long-term contracts and high volumes allow Genus to negotiate favorable terms and prioritize continuity of supply.

- Veterinary biologics: multiple suppliers, limited pricing power

- Biosecurity materials: commoditized, competitive market

- Liquid nitrogen & transport: time-sensitive, outbreak-driven spikes

- Mitigation: long-term relationships and volume leverage

External IP and research partnerships

- Royalties: low‑single to mid‑teens %; 2024 R&D ≈ £75m; portfolio breadth cuts single‑source risk

Moderate supplier power: donor scarcity, dominant sequencers (~65%)

Genus faces moderate supplier power: elite donor access and concentrated lab platforms give leverage, but owned nucleus herds and in‑house genetics reduce dependence. Switching costs for sequencers/cytometers ($50k–$500k; 3–12 months) and IP royalties (low‑single to mid‑teens %) raise pressure. 2024 R&D ≈ £75m; Illumina ~65% sequencing share (2024).

| Input | Concentration | Impact | Mitigation |

|---|---|---|---|

| Sequencing | Illumina ~65% (2024) | High switching cost | In‑house pipelines |

| Donors/IP | Scarce donors; patents | Access/royalties | Owned herds; £75m R&D |

What is included in the product

Comprehensive Porter's Five Forces for Genus, detailing competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, plus disruptive risks and strategic levers to protect margins; fully editable for reports.

Genus Porter's Five Forces delivers a one-sheet, customizable summary with instant spider-chart visualization—streamlining strategic pressure assessment for quick decisions and slide-ready reporting.

Customers Bargaining Power

Consolidated large producers

Global pork integrators and large dairy/beef operations are consolidating: in the US the four largest beef packers control roughly 80–85% of slaughter capacity and the top four pork processors about 65–70% (2023–24), giving buyers strong price negotiation, vendor rationalization and performance-based contracting leverage. This elevates buyer power for commoditized SKUs, although Genus’s differentiated genetic gains and measurable ROI limit deep discounting.

High switching ease across genetics

Producers can switch among leading studs and breeding programs with relative ease over multi-year planning horizons, though contract cycles and biosecurity protocols limit immediate moves. Performance transparency and benchmarking platforms in 2024 intensified price comparisons and buyer leverage. Genus' 2024 annual report emphasizes proprietary lines, veterinary service and on-farm support to raise practical switching costs and protect margins.

Outcome-based purchasing

Customers now buy on outcomes—feed efficiency, fertility, calving ease, carcass quality and disease resilience—driving procurement toward warranties, on-farm trials and data-sharing that increase buyer leverage on contract terms. In 2024 Genus reported revenue of £1.1bn, letting buyers press for proof-of-performance; superior EBVs and genomic proof help Genus defend value-based pricing and justify premium margins.

Cyclical end-market sensitivity

Cyclical end-market sensitivity: livestock prices, feed costs (feed typically ~60% of production cost) and disease cycles directly compress customer margins, so in downturns buyers press for lower prices or defer genetic upgrades, increasing buyer power; counter-cyclical traits (survival, feed efficiency) and subscription-like supply programs smooth demand and reduce bargaining pressure.

- Feed ≈60% of costs

- Downturns → deferred upgrades

- Counter-cyclical genetics mitigate volatility

- Subscription programs stabilize orders

Alternative sourcing channels

Alternative sourcing via co-ops, regional studs and private herds gives buyers options beyond global leaders; access to comparable genetics varies by region and species, creating some leverage. Consistency, QA and delivery reliability still favor scaled providers, while Genus’ network across 30+ countries and strong biosecurity in 2024 reduces perceived risk of paying a premium.

- Co-ops/regional studs offer local access

- Buyer leverage varies by region/species

- Scale drives QA and delivery reliability

- Genus 30+ country footprint lowers risk of premium

Consolidation boosts buyer leverage; genetics firm £1.1bn, ≈60% feed cost

Consolidation (top4 beef 80–85%, pork 65–70% in 2023–24) and buyer focus on outcomes raise customer leverage, but Genus’ differentiated genetics, services and £1.1bn 2024 revenue limit deep discounting. Producers can switch over multi-year horizons; feed ≈60% of costs drives sensitivity. Genus’ 30+ country footprint and biosecurity reduce perceived premium risk.

| Metric | 2024 | Buyer power impact |

|---|---|---|

| Genus revenue | £1.1bn | Supports premium |

| Top4 beef/pork | 80–85% / 65–70% | Raises buyer leverage |

| Feed share | ≈60% | Increases price sensitivity |

| Global footprint | 30+ countries | Reduces switching risk |

Same Document Delivered

Genus Porter's Five Forces Analysis

This preview shows the exact Genus Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the professionally written, fully formatted deliverable, ready for download and use the moment you buy. You’re viewing the final file; once payment is completed, you’ll get instant access to this same document. No mockups or samples—this is the real deliverable.