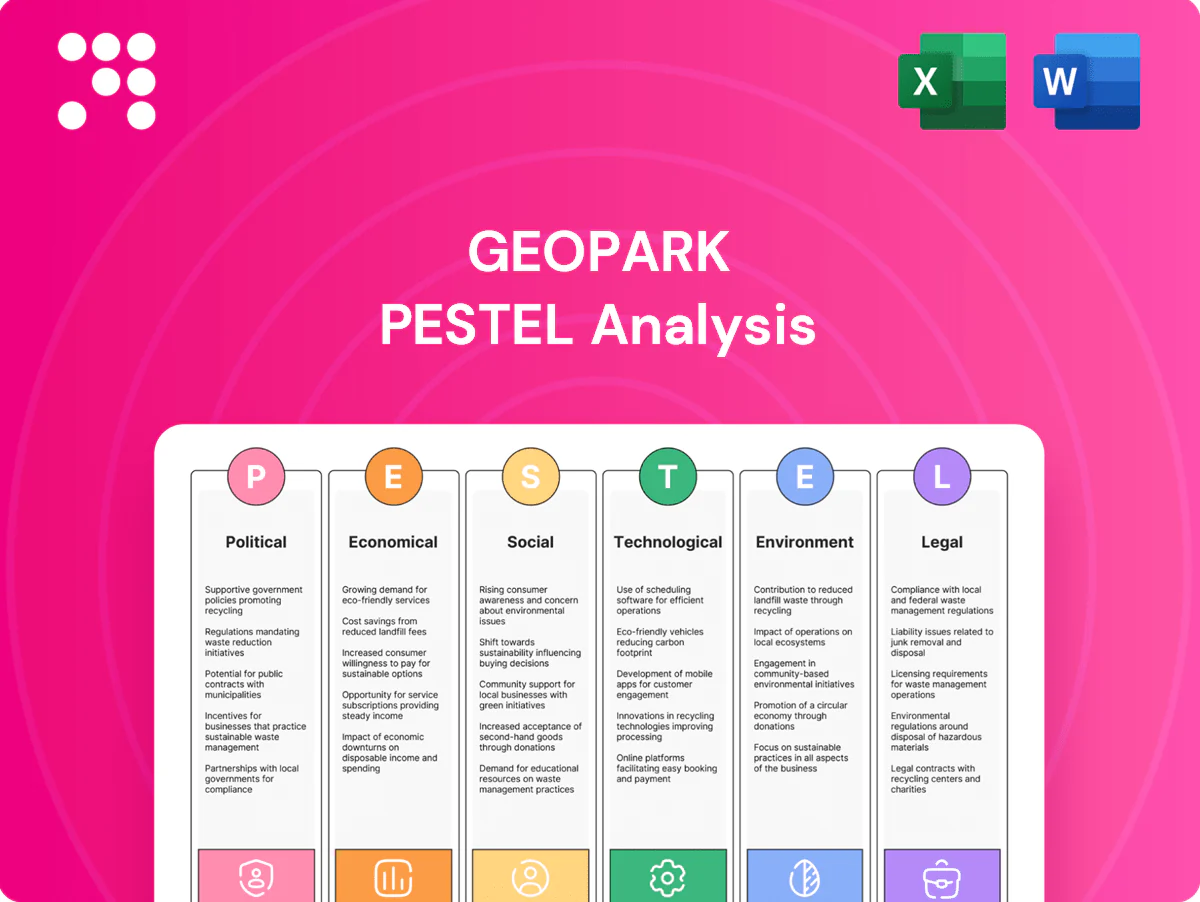

GeoPark PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social expectations, technological advances, legal frameworks, and environmental pressures converge to shape GeoPark’s strategic outlook—our concise PESTLE highlights key risks and opportunities. Buy the full analysis to unlock in-depth, actionable insights you can use immediately.

Political factors

Regulatory stability across host countries

GeoPark operates in Colombia, Ecuador, Brazil and Chile, each with distinct upstream regimes, royalty frameworks and licensing processes; royalties in the region commonly range 10–25%. Policy shifts after elections can change fiscal terms, exploration incentives or local content rules, materially affecting project economics. Stable, transparent regulation lowers project risk and cost of capital. Continuous monitoring and local engagement help anticipate reforms and adapt development plans.

Election cycles and resource nationalism

Latin American electoral swings can trigger tougher oil taxation, contract renegotiations or stricter social and environmental obligations; Colombia's 2022 election of Gustavo Petro exemplifies policy-driven sector scrutiny. GeoPark operates across five countries (Colombia, Brazil, Chile, Ecuador, Peru), reducing country concentration risk. Populist agendas may push greater state participation and rent redistribution, impacting project economics and timelines; scenario planning and cross-country diversification mitigate those risks.

Government partners and NOC dynamics

Collaboration with national oil companies such as Ecopetrol (approximately 88% government-owned) and Petroecuador (state-owned) is often essential for access, permits and pipeline rights. Changes in NOC strategies, capex or leadership can shift JV priorities and operating tempo, impacting timelines and cash flow. Strong alignment on HSE and community relations reduces social risk and regulatory interventions. Clear JV governance and defined decision rights cut execution friction and cost overruns.

Security and community-related disruptions

Certain GeoPark basins face protest risks, blockades or localized security incidents that can halt production and logistics, raising the need for rapid response. Coordinated public-sector support and sustained community engagement have reduced downtime where implemented. Planning secure transport, workforce safety protocols and contingency routes is vital; insurance and crisis protocols protect operational continuity.

- Risk: localized protests/blockades

- Mitigation: public-sector coordination

- Operations: secure transport/contingency routes

- Protection: insurance and crisis protocols

Infrastructure and regional integration policy

Pipeline, road and port policies directly affect GeoParks evacuation capacity and product differentials, altering realized prices and logistics risk; cross-border energy integration can open new markets but needs harmonized tariffs and safety rules. Public investment and PPP frameworks determine midstream delivery timelines and capital access, while targeted advocacy for enabling infrastructure improves field netbacks.

- Evacuation capacity impacts realized pricing

- Cross-border integration unlocks markets with coordinated regulation

- Public investment/PPPs set midstream timelines

- Infrastructure advocacy raises field netbacks

E&P in 5 countries faces 10-25% royalties, NOC deals and midstream constraints

GeoPark operates in five countries (Colombia, Brazil, Chile, Ecuador, Peru), facing royalties typically 10–25% and election-driven fiscal shifts (Colombia 2022 election noted). Collaboration with NOCs (Ecopetrol ~88% government-owned; Petroecuador state-owned) affects access and timing. Local protests, midstream constraints and PPP pipelines materially change netbacks and project timelines.

| Metric | Value |

|---|---|

| Countries | 5 |

| Royalties | 10–25% |

| Ecopetrol ownership | ~88% govt |

What is included in the product

Explores how macro-environmental factors uniquely affect GeoPark across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and practical examples to support executives, investors and strategists in risk identification, scenario planning and opportunity capture.

A concise, visually segmented GeoPark PESTLE summary that eases stakeholder alignment by highlighting key external risks and opportunities for meetings or decks, while remaining editable for regional or business-line notes and quick sharing across teams.

Economic factors

Oil price volatility and hedging

Brent volatility — averaging roughly $85–90/bbl in 2024 and swinging between about $70–115/bbl — directly alters GeoPark cash flows, reserves booking and capex prioritization. Disciplined hedging can stabilize budgets and protect downside in down-cycles. Price cycles favor low lifting-cost, fast-payback projects, and a balanced development/exploration portfolio smooths returns.

FX exposure and inflation in Latin America

GeoPark faces currency mismatches as operating costs are paid in local currencies (COP, BRL, CLP) while revenues are predominantly USD-linked, increasing FX sensitivity. Regional inflation and wage pressures raise operating and drilling costs, squeezing margins. The company uses active FX hedging and local procurement to limit volatility. Contractual indexation to USD or inflation benchmarks helps preserve margins.

Access to capital and interest rates

Global rates (US 10-year ~4.3% in mid‑2025) and EM risk premiums (EMBIG ~330 bps) directly tighten bond pricing and temper equity appetite, increasing cost of capital for oil & gas issuers. GeoPark’s strong free cash flow and leverage discipline support competitive financing terms. Transparent ESG metrics expand the investor base, while staggered maturities and liquidity buffers lower refinancing risk.

Infrastructure bottlenecks and differentials

Infrastructure bottlenecks—limited pipeline takeaway and weather-affected roads—raise transport costs and can curtail output; Colombia national oil production hovered around 700 kbpd in 2024, highlighting regional logistics strain. Crude quality and distance to markets materially influence realized prices and differentials; midstream constraints can widen discounts versus Brent. Strategic midstream agreements or capex can lift netbacks, while inventory and flexible offtake arrangements mitigate short-term bottlenecks.

- Pipeline capacity pressure: regional takeaway limits vs ~700 kbpd national production (2024)

- Price impact: quality/distance drive realized differentials

- Mitigants: midstream deals, capex to improve netbacks

- Short-term relief: inventories and flexible offtake

M&A opportunities and portfolio optimization

Dislocations create attractive farm‑ins/acquisition opportunities to add reserves and synergies; GeoPark, which reported average production of about 55,700 boe/d in 2023, can recycle non‑core divestment proceeds into higher‑IRR plays while rigorous screening of geology, fiscal terms and ESG risks preserves value; integration capability is key to capture cost and operational upsides.

- Targeted M&A to add reserves and synergies

- Non‑core divestments recycle capital to higher‑IRR projects

- Strict geological, fiscal and ESG screening

- Strong integration drives cost and ops upside

E&P in 5 countries faces 10-25% royalties, NOC deals and midstream constraints

Brent ~85–90/bbl (2024) drives cash flow and capex prioritization; hedging cushions downside. FX and local inflation (COP, BRL, CLP) raise operating costs; contractual indexation and local procurement mitigate. Higher rates (US 10y ~4.3% mid‑2025) and EMBIG ~330bps raise cost of capital; strong FCF and low leverage support financing. Midstream constraints (Colombia ~700 kbpd 2024) pressure netbacks; targeted M&A recycles capital into high‑IRR plays.

| Metric | Value |

|---|---|

| Brent (2024 avg) | $85–90/bbl |

| GeoPark prod (2023) | 55,700 boe/d |

| Colombia prod (2024) | ~700 kbpd |

| US 10y (mid‑2025) | ~4.3% |

| EMBIG (mid‑2025) | ~330 bps |

Preview the Actual Deliverable

GeoPark PESTLE Analysis

The GeoPark PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the final file with complete content, no placeholders or teasers. After checkout you’ll be able to download this same document immediately, with the layout and analysis exactly as displayed.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social expectations, technological advances, legal frameworks, and environmental pressures converge to shape GeoPark’s strategic outlook—our concise PESTLE highlights key risks and opportunities. Buy the full analysis to unlock in-depth, actionable insights you can use immediately.

Political factors

Regulatory stability across host countries

GeoPark operates in Colombia, Ecuador, Brazil and Chile, each with distinct upstream regimes, royalty frameworks and licensing processes; royalties in the region commonly range 10–25%. Policy shifts after elections can change fiscal terms, exploration incentives or local content rules, materially affecting project economics. Stable, transparent regulation lowers project risk and cost of capital. Continuous monitoring and local engagement help anticipate reforms and adapt development plans.

Election cycles and resource nationalism

Latin American electoral swings can trigger tougher oil taxation, contract renegotiations or stricter social and environmental obligations; Colombia's 2022 election of Gustavo Petro exemplifies policy-driven sector scrutiny. GeoPark operates across five countries (Colombia, Brazil, Chile, Ecuador, Peru), reducing country concentration risk. Populist agendas may push greater state participation and rent redistribution, impacting project economics and timelines; scenario planning and cross-country diversification mitigate those risks.

Government partners and NOC dynamics

Collaboration with national oil companies such as Ecopetrol (approximately 88% government-owned) and Petroecuador (state-owned) is often essential for access, permits and pipeline rights. Changes in NOC strategies, capex or leadership can shift JV priorities and operating tempo, impacting timelines and cash flow. Strong alignment on HSE and community relations reduces social risk and regulatory interventions. Clear JV governance and defined decision rights cut execution friction and cost overruns.

Security and community-related disruptions

Certain GeoPark basins face protest risks, blockades or localized security incidents that can halt production and logistics, raising the need for rapid response. Coordinated public-sector support and sustained community engagement have reduced downtime where implemented. Planning secure transport, workforce safety protocols and contingency routes is vital; insurance and crisis protocols protect operational continuity.

- Risk: localized protests/blockades

- Mitigation: public-sector coordination

- Operations: secure transport/contingency routes

- Protection: insurance and crisis protocols

Infrastructure and regional integration policy

Pipeline, road and port policies directly affect GeoParks evacuation capacity and product differentials, altering realized prices and logistics risk; cross-border energy integration can open new markets but needs harmonized tariffs and safety rules. Public investment and PPP frameworks determine midstream delivery timelines and capital access, while targeted advocacy for enabling infrastructure improves field netbacks.

- Evacuation capacity impacts realized pricing

- Cross-border integration unlocks markets with coordinated regulation

- Public investment/PPPs set midstream timelines

- Infrastructure advocacy raises field netbacks

E&P in 5 countries faces 10-25% royalties, NOC deals and midstream constraints

GeoPark operates in five countries (Colombia, Brazil, Chile, Ecuador, Peru), facing royalties typically 10–25% and election-driven fiscal shifts (Colombia 2022 election noted). Collaboration with NOCs (Ecopetrol ~88% government-owned; Petroecuador state-owned) affects access and timing. Local protests, midstream constraints and PPP pipelines materially change netbacks and project timelines.

| Metric | Value |

|---|---|

| Countries | 5 |

| Royalties | 10–25% |

| Ecopetrol ownership | ~88% govt |

What is included in the product

Explores how macro-environmental factors uniquely affect GeoPark across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and practical examples to support executives, investors and strategists in risk identification, scenario planning and opportunity capture.

A concise, visually segmented GeoPark PESTLE summary that eases stakeholder alignment by highlighting key external risks and opportunities for meetings or decks, while remaining editable for regional or business-line notes and quick sharing across teams.

Economic factors

Oil price volatility and hedging

Brent volatility — averaging roughly $85–90/bbl in 2024 and swinging between about $70–115/bbl — directly alters GeoPark cash flows, reserves booking and capex prioritization. Disciplined hedging can stabilize budgets and protect downside in down-cycles. Price cycles favor low lifting-cost, fast-payback projects, and a balanced development/exploration portfolio smooths returns.

FX exposure and inflation in Latin America

GeoPark faces currency mismatches as operating costs are paid in local currencies (COP, BRL, CLP) while revenues are predominantly USD-linked, increasing FX sensitivity. Regional inflation and wage pressures raise operating and drilling costs, squeezing margins. The company uses active FX hedging and local procurement to limit volatility. Contractual indexation to USD or inflation benchmarks helps preserve margins.

Access to capital and interest rates

Global rates (US 10-year ~4.3% in mid‑2025) and EM risk premiums (EMBIG ~330 bps) directly tighten bond pricing and temper equity appetite, increasing cost of capital for oil & gas issuers. GeoPark’s strong free cash flow and leverage discipline support competitive financing terms. Transparent ESG metrics expand the investor base, while staggered maturities and liquidity buffers lower refinancing risk.

Infrastructure bottlenecks and differentials

Infrastructure bottlenecks—limited pipeline takeaway and weather-affected roads—raise transport costs and can curtail output; Colombia national oil production hovered around 700 kbpd in 2024, highlighting regional logistics strain. Crude quality and distance to markets materially influence realized prices and differentials; midstream constraints can widen discounts versus Brent. Strategic midstream agreements or capex can lift netbacks, while inventory and flexible offtake arrangements mitigate short-term bottlenecks.

- Pipeline capacity pressure: regional takeaway limits vs ~700 kbpd national production (2024)

- Price impact: quality/distance drive realized differentials

- Mitigants: midstream deals, capex to improve netbacks

- Short-term relief: inventories and flexible offtake

M&A opportunities and portfolio optimization

Dislocations create attractive farm‑ins/acquisition opportunities to add reserves and synergies; GeoPark, which reported average production of about 55,700 boe/d in 2023, can recycle non‑core divestment proceeds into higher‑IRR plays while rigorous screening of geology, fiscal terms and ESG risks preserves value; integration capability is key to capture cost and operational upsides.

- Targeted M&A to add reserves and synergies

- Non‑core divestments recycle capital to higher‑IRR projects

- Strict geological, fiscal and ESG screening

- Strong integration drives cost and ops upside

E&P in 5 countries faces 10-25% royalties, NOC deals and midstream constraints

Brent ~85–90/bbl (2024) drives cash flow and capex prioritization; hedging cushions downside. FX and local inflation (COP, BRL, CLP) raise operating costs; contractual indexation and local procurement mitigate. Higher rates (US 10y ~4.3% mid‑2025) and EMBIG ~330bps raise cost of capital; strong FCF and low leverage support financing. Midstream constraints (Colombia ~700 kbpd 2024) pressure netbacks; targeted M&A recycles capital into high‑IRR plays.

| Metric | Value |

|---|---|

| Brent (2024 avg) | $85–90/bbl |

| GeoPark prod (2023) | 55,700 boe/d |

| Colombia prod (2024) | ~700 kbpd |

| US 10y (mid‑2025) | ~4.3% |

| EMBIG (mid‑2025) | ~330 bps |

Preview the Actual Deliverable

GeoPark PESTLE Analysis

The GeoPark PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the final file with complete content, no placeholders or teasers. After checkout you’ll be able to download this same document immediately, with the layout and analysis exactly as displayed.

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social expectations, technological advances, legal frameworks, and environmental pressures converge to shape GeoPark’s strategic outlook—our concise PESTLE highlights key risks and opportunities. Buy the full analysis to unlock in-depth, actionable insights you can use immediately.

Political factors

Regulatory stability across host countries

GeoPark operates in Colombia, Ecuador, Brazil and Chile, each with distinct upstream regimes, royalty frameworks and licensing processes; royalties in the region commonly range 10–25%. Policy shifts after elections can change fiscal terms, exploration incentives or local content rules, materially affecting project economics. Stable, transparent regulation lowers project risk and cost of capital. Continuous monitoring and local engagement help anticipate reforms and adapt development plans.

Election cycles and resource nationalism

Latin American electoral swings can trigger tougher oil taxation, contract renegotiations or stricter social and environmental obligations; Colombia's 2022 election of Gustavo Petro exemplifies policy-driven sector scrutiny. GeoPark operates across five countries (Colombia, Brazil, Chile, Ecuador, Peru), reducing country concentration risk. Populist agendas may push greater state participation and rent redistribution, impacting project economics and timelines; scenario planning and cross-country diversification mitigate those risks.

Government partners and NOC dynamics

Collaboration with national oil companies such as Ecopetrol (approximately 88% government-owned) and Petroecuador (state-owned) is often essential for access, permits and pipeline rights. Changes in NOC strategies, capex or leadership can shift JV priorities and operating tempo, impacting timelines and cash flow. Strong alignment on HSE and community relations reduces social risk and regulatory interventions. Clear JV governance and defined decision rights cut execution friction and cost overruns.

Security and community-related disruptions

Certain GeoPark basins face protest risks, blockades or localized security incidents that can halt production and logistics, raising the need for rapid response. Coordinated public-sector support and sustained community engagement have reduced downtime where implemented. Planning secure transport, workforce safety protocols and contingency routes is vital; insurance and crisis protocols protect operational continuity.

- Risk: localized protests/blockades

- Mitigation: public-sector coordination

- Operations: secure transport/contingency routes

- Protection: insurance and crisis protocols

Infrastructure and regional integration policy

Pipeline, road and port policies directly affect GeoParks evacuation capacity and product differentials, altering realized prices and logistics risk; cross-border energy integration can open new markets but needs harmonized tariffs and safety rules. Public investment and PPP frameworks determine midstream delivery timelines and capital access, while targeted advocacy for enabling infrastructure improves field netbacks.

- Evacuation capacity impacts realized pricing

- Cross-border integration unlocks markets with coordinated regulation

- Public investment/PPPs set midstream timelines

- Infrastructure advocacy raises field netbacks

E&P in 5 countries faces 10-25% royalties, NOC deals and midstream constraints

GeoPark operates in five countries (Colombia, Brazil, Chile, Ecuador, Peru), facing royalties typically 10–25% and election-driven fiscal shifts (Colombia 2022 election noted). Collaboration with NOCs (Ecopetrol ~88% government-owned; Petroecuador state-owned) affects access and timing. Local protests, midstream constraints and PPP pipelines materially change netbacks and project timelines.

| Metric | Value |

|---|---|

| Countries | 5 |

| Royalties | 10–25% |

| Ecopetrol ownership | ~88% govt |

What is included in the product

Explores how macro-environmental factors uniquely affect GeoPark across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and practical examples to support executives, investors and strategists in risk identification, scenario planning and opportunity capture.

A concise, visually segmented GeoPark PESTLE summary that eases stakeholder alignment by highlighting key external risks and opportunities for meetings or decks, while remaining editable for regional or business-line notes and quick sharing across teams.

Economic factors

Oil price volatility and hedging

Brent volatility — averaging roughly $85–90/bbl in 2024 and swinging between about $70–115/bbl — directly alters GeoPark cash flows, reserves booking and capex prioritization. Disciplined hedging can stabilize budgets and protect downside in down-cycles. Price cycles favor low lifting-cost, fast-payback projects, and a balanced development/exploration portfolio smooths returns.

FX exposure and inflation in Latin America

GeoPark faces currency mismatches as operating costs are paid in local currencies (COP, BRL, CLP) while revenues are predominantly USD-linked, increasing FX sensitivity. Regional inflation and wage pressures raise operating and drilling costs, squeezing margins. The company uses active FX hedging and local procurement to limit volatility. Contractual indexation to USD or inflation benchmarks helps preserve margins.

Access to capital and interest rates

Global rates (US 10-year ~4.3% in mid‑2025) and EM risk premiums (EMBIG ~330 bps) directly tighten bond pricing and temper equity appetite, increasing cost of capital for oil & gas issuers. GeoPark’s strong free cash flow and leverage discipline support competitive financing terms. Transparent ESG metrics expand the investor base, while staggered maturities and liquidity buffers lower refinancing risk.

Infrastructure bottlenecks and differentials

Infrastructure bottlenecks—limited pipeline takeaway and weather-affected roads—raise transport costs and can curtail output; Colombia national oil production hovered around 700 kbpd in 2024, highlighting regional logistics strain. Crude quality and distance to markets materially influence realized prices and differentials; midstream constraints can widen discounts versus Brent. Strategic midstream agreements or capex can lift netbacks, while inventory and flexible offtake arrangements mitigate short-term bottlenecks.

- Pipeline capacity pressure: regional takeaway limits vs ~700 kbpd national production (2024)

- Price impact: quality/distance drive realized differentials

- Mitigants: midstream deals, capex to improve netbacks

- Short-term relief: inventories and flexible offtake

M&A opportunities and portfolio optimization

Dislocations create attractive farm‑ins/acquisition opportunities to add reserves and synergies; GeoPark, which reported average production of about 55,700 boe/d in 2023, can recycle non‑core divestment proceeds into higher‑IRR plays while rigorous screening of geology, fiscal terms and ESG risks preserves value; integration capability is key to capture cost and operational upsides.

- Targeted M&A to add reserves and synergies

- Non‑core divestments recycle capital to higher‑IRR projects

- Strict geological, fiscal and ESG screening

- Strong integration drives cost and ops upside

E&P in 5 countries faces 10-25% royalties, NOC deals and midstream constraints

Brent ~85–90/bbl (2024) drives cash flow and capex prioritization; hedging cushions downside. FX and local inflation (COP, BRL, CLP) raise operating costs; contractual indexation and local procurement mitigate. Higher rates (US 10y ~4.3% mid‑2025) and EMBIG ~330bps raise cost of capital; strong FCF and low leverage support financing. Midstream constraints (Colombia ~700 kbpd 2024) pressure netbacks; targeted M&A recycles capital into high‑IRR plays.

| Metric | Value |

|---|---|

| Brent (2024 avg) | $85–90/bbl |

| GeoPark prod (2023) | 55,700 boe/d |

| Colombia prod (2024) | ~700 kbpd |

| US 10y (mid‑2025) | ~4.3% |

| EMBIG (mid‑2025) | ~330 bps |

Preview the Actual Deliverable

GeoPark PESTLE Analysis

The GeoPark PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the final file with complete content, no placeholders or teasers. After checkout you’ll be able to download this same document immediately, with the layout and analysis exactly as displayed.