Geospace Technologies Porter's Five Forces Analysis

Don't Miss the Bigger Picture

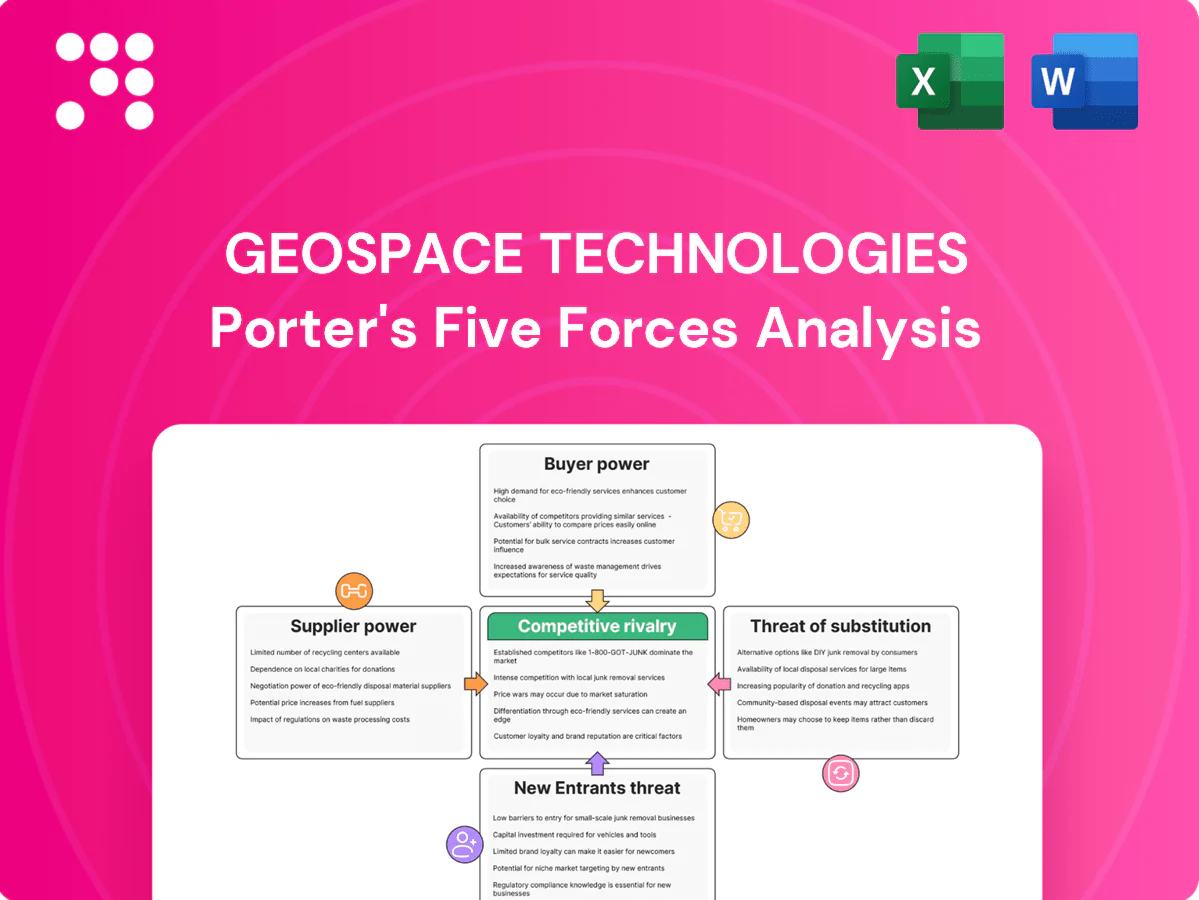

Geospace Technologies faces moderate buyer power and niche supplier leverage, while industry rivalry hinges on specialized geophysical equipment and services; barriers to entry are medium due to technical know-how, and substitute threats remain limited. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Geospace Technologies’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized components concentration

Key inputs such as piezoelectric elements, ruggedized connectors, FPGAs/ASICs and defense-grade electronics are sourced from a narrow supplier base—TSMC and top foundries held roughly 50%+ of foundry share in 2024—concentrating leverage. Supplier concentration raises switching costs and single-source exposure, with semiconductor lead times often 10–20 weeks in tight cycles, pressuring margins. Dual-sourcing and design-for-substitution reduce but do not eliminate supplier bargaining power.

In-house manufacturing offsets

Geospace’s in-house design and build capabilities cut reliance on external suppliers for critical assemblies, supporting its FY2023 revenue base of about $106.6M and improving quality control and cost visibility. Vertical integration gives bargaining leverage in pricing and delivery negotiations, though it necessitates sustained capex and specialized process expertise to maintain competitive advantage.

Certification and compliance constraints

ITAR control by the DDTC and defense-specific certifications like AS9100 and ISO 9001 constrain Geospace’s supplier pool to qualified vendors, raising suppliers’ leverage. Compliance obligations and required traceability hinder rapid supplier switching and prolong lead times, increasing supplier power. Mandatory audits and batch traceability add cost and cycle time. Long-term agreements are often used to trade price for assured compliance and continuity.

Commodity inputs volatility

Commodity inputs—copper, specialty alloys and battery materials—leave Geospace exposed to swings; in 2024 battery-material markets remained volatile, amplifying input-cost risk. Suppliers can impose surcharges or minimum-buy terms; hedging and inventory buffers reduce price shock but lock up working capital, while customer pricing clauses often lag cost moves.

- Supplier leverage: surcharges/minimum buys

- Risk dampeners: hedging, inventory (capital tie-up)

- Timing gap: customer pricing lags costs

Geopolitical and logistics risks

Export controls and tariffs enacted through 2024 (notably expanded semiconductor controls) constrict access to specialty electronics and raise component lead times, while freight disruptions intermittently spiked expediting costs by roughly 25% in 2024 for electronics supply chains.

Extended global chains increase delivery risk and rush-shipping spend; regional qualification of alternates improves resilience but added ~10–15% sourcing overhead in 2024, and nearshoring plus higher safety stocks bolstered continuity at a 2–4% rise in annual working-capital cost.

- Export controls: tighter semiconductor and dual-use restrictions in 2024

- Freight/expedite: ~25% spike in 2024 peak expediting costs

- Regional qualification: +10–15% overhead in 2024

- Continuity measures: nearshoring and safety stock → +2–4% working-capital cost

Foundry dominance, 10-20 week lead times and +25% expedite costs squeeze margins

Supplier power is high: narrow sources for piezoelectrics, defense electronics and foundries (top foundries ~50%+ share in 2024) raise switching costs and 10–20 week lead times, pressuring margins. Geospace’s in-house build and vertical integration lower reliance but require capex. Compliance, export controls and commodity volatility (expedite +25% in 2024) sustain supplier leverage.

| Metric | 2024/Latest |

|---|---|

| Top foundry share | ~50%+ |

| Semiconductor lead times | 10–20 weeks |

| Expedite cost spike | ~+25% |

| Regional sourcing overhead | +10–15% |

| Working-capital rise | +2–4% |

| FY2023 revenue | $106.6M |

What is included in the product

Tailored Porter’s Five Forces analysis for Geospace Technologies revealing competitive intensity, supplier and buyer power, threat of substitutes and entrants, and disruptive forces shaping pricing, margins, and strategic positioning.

A concise one-sheet Porter's Five Forces for Geospace Technologies that highlights supplier, buyer, entrant, substitute, and competitive pressures—easy to customize, paste into decks, and update as market data shifts.

Customers Bargaining Power

Customer concentration

Large E&P firms, seismic contractors, and defense agencies account for a substantial share of Geospace Technologies’ demand, giving buyers leverage to push for aggressive pricing and contractual terms. The scale of these customers means loss of a major program can materially impact revenue and margins. Geospace’s diversification into industrial sensors and healthcare devices mitigates but does not eliminate customer concentration risk.

Tender-driven procurement

Formal RFPs and 6–18 month sales cycles in tender-driven procurement shift negotiating leverage to buyers; public procurement represents about 15% of global GDP per World Bank estimates, concentrating buyer power. Competitive bidding compresses margins and lengthens receivables. Offering value-added specs and lifecycle support enables premium pricing. Post-award change orders can add revenue but remain uncertain and timing-dependent.

High switching and integration costs

Seismic and monitoring systems tightly couple hardware, firmware and analytics workflows, making full replacements complex; in 2024 many projects reported revalidation times of 4–12 weeks and operational ramp-ups that span months. Calibration, training and ensuring data continuity create switching barriers reinforced by typical multi-year contracts (12–36 months). Buyers favor vendor stickiness for mission-critical reliability, which tempers price pressure when performance is differentiated.

Demand cyclicality

Bargaining power of customers: Demand cyclicality is driven by oil and gas capex swings, with upstream investment around $470B in 2023 and modest 2024 recovery, producing sharp order peaks and troughs; in downturns buyers defer upgrades and press for discounts, while framework agreements and service offerings help smooth utilization and pricing. Defense and industrial contracts provide partial counter-cyclical ballast to revenues.

- High volatility: upstream capex cyclical

- Buyer leverage: discounting in downturns

- Mitigants: framework agreements, services

- Stabilizers: defense/industrial orders

Customization leverage

Defense and industrial clients often demand bespoke specs and compliance, which lengthen development cycles and shift technical and schedule risk to vendors; US defense spending reached about 858 billion USD in FY2024, sustaining demand but raising customer bargaining leverage. Milestone-based payments and recovery of non-recurring engineering costs are key negotiation points, while disciplined program management can convert customization into customer lock-in.

- Customization increases vendor risk and timeline

- Milestone payments and NRE recovery are negotiation levers

- FY2024 US defense budget ~858B USD underpins buyer demands

- Strong program management can create long-term lock-in

Large E&P, seismic and defense buyers drive pricing pressure amid long RFPs and high switching costs

Large E&P firms, seismic contractors and defense agencies account for a substantial share of Geospace Technologies’ demand, giving buyers leverage to press pricing and terms. Tender cycles (RFPs 6–18 months) and multi-year contracts (12–36 months) coexist with high switching costs (revalidation 4–12 weeks). Cyclicality: upstream capex ~$470B in 2023; US defense budget ~$858B FY2024; mitigants: services, framework agreements.

| Metric | Value |

|---|---|

| RFP cycle | 6–18 months |

| Contract length | 12–36 months |

| Revalidation | 4–12 weeks |

| Upstream capex (2023) | $470B |

| US defense FY2024 | $858B |

Full Version Awaits

Geospace Technologies Porter's Five Forces Analysis

This preview shows the exact Geospace Technologies Porter's Five Forces Analysis you'll receive—no placeholders, no mockups. The full document is fully formatted, professionally written, and ready for immediate download upon purchase. Use it as-is for decision-making, presentations, or further research.

Don't Miss the Bigger Picture

Geospace Technologies faces moderate buyer power and niche supplier leverage, while industry rivalry hinges on specialized geophysical equipment and services; barriers to entry are medium due to technical know-how, and substitute threats remain limited. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Geospace Technologies’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized components concentration

Key inputs such as piezoelectric elements, ruggedized connectors, FPGAs/ASICs and defense-grade electronics are sourced from a narrow supplier base—TSMC and top foundries held roughly 50%+ of foundry share in 2024—concentrating leverage. Supplier concentration raises switching costs and single-source exposure, with semiconductor lead times often 10–20 weeks in tight cycles, pressuring margins. Dual-sourcing and design-for-substitution reduce but do not eliminate supplier bargaining power.

In-house manufacturing offsets

Geospace’s in-house design and build capabilities cut reliance on external suppliers for critical assemblies, supporting its FY2023 revenue base of about $106.6M and improving quality control and cost visibility. Vertical integration gives bargaining leverage in pricing and delivery negotiations, though it necessitates sustained capex and specialized process expertise to maintain competitive advantage.

Certification and compliance constraints

ITAR control by the DDTC and defense-specific certifications like AS9100 and ISO 9001 constrain Geospace’s supplier pool to qualified vendors, raising suppliers’ leverage. Compliance obligations and required traceability hinder rapid supplier switching and prolong lead times, increasing supplier power. Mandatory audits and batch traceability add cost and cycle time. Long-term agreements are often used to trade price for assured compliance and continuity.

Commodity inputs volatility

Commodity inputs—copper, specialty alloys and battery materials—leave Geospace exposed to swings; in 2024 battery-material markets remained volatile, amplifying input-cost risk. Suppliers can impose surcharges or minimum-buy terms; hedging and inventory buffers reduce price shock but lock up working capital, while customer pricing clauses often lag cost moves.

- Supplier leverage: surcharges/minimum buys

- Risk dampeners: hedging, inventory (capital tie-up)

- Timing gap: customer pricing lags costs

Geopolitical and logistics risks

Export controls and tariffs enacted through 2024 (notably expanded semiconductor controls) constrict access to specialty electronics and raise component lead times, while freight disruptions intermittently spiked expediting costs by roughly 25% in 2024 for electronics supply chains.

Extended global chains increase delivery risk and rush-shipping spend; regional qualification of alternates improves resilience but added ~10–15% sourcing overhead in 2024, and nearshoring plus higher safety stocks bolstered continuity at a 2–4% rise in annual working-capital cost.

- Export controls: tighter semiconductor and dual-use restrictions in 2024

- Freight/expedite: ~25% spike in 2024 peak expediting costs

- Regional qualification: +10–15% overhead in 2024

- Continuity measures: nearshoring and safety stock → +2–4% working-capital cost

Foundry dominance, 10-20 week lead times and +25% expedite costs squeeze margins

Supplier power is high: narrow sources for piezoelectrics, defense electronics and foundries (top foundries ~50%+ share in 2024) raise switching costs and 10–20 week lead times, pressuring margins. Geospace’s in-house build and vertical integration lower reliance but require capex. Compliance, export controls and commodity volatility (expedite +25% in 2024) sustain supplier leverage.

| Metric | 2024/Latest |

|---|---|

| Top foundry share | ~50%+ |

| Semiconductor lead times | 10–20 weeks |

| Expedite cost spike | ~+25% |

| Regional sourcing overhead | +10–15% |

| Working-capital rise | +2–4% |

| FY2023 revenue | $106.6M |

What is included in the product

Tailored Porter’s Five Forces analysis for Geospace Technologies revealing competitive intensity, supplier and buyer power, threat of substitutes and entrants, and disruptive forces shaping pricing, margins, and strategic positioning.

A concise one-sheet Porter's Five Forces for Geospace Technologies that highlights supplier, buyer, entrant, substitute, and competitive pressures—easy to customize, paste into decks, and update as market data shifts.

Customers Bargaining Power

Customer concentration

Large E&P firms, seismic contractors, and defense agencies account for a substantial share of Geospace Technologies’ demand, giving buyers leverage to push for aggressive pricing and contractual terms. The scale of these customers means loss of a major program can materially impact revenue and margins. Geospace’s diversification into industrial sensors and healthcare devices mitigates but does not eliminate customer concentration risk.

Tender-driven procurement

Formal RFPs and 6–18 month sales cycles in tender-driven procurement shift negotiating leverage to buyers; public procurement represents about 15% of global GDP per World Bank estimates, concentrating buyer power. Competitive bidding compresses margins and lengthens receivables. Offering value-added specs and lifecycle support enables premium pricing. Post-award change orders can add revenue but remain uncertain and timing-dependent.

High switching and integration costs

Seismic and monitoring systems tightly couple hardware, firmware and analytics workflows, making full replacements complex; in 2024 many projects reported revalidation times of 4–12 weeks and operational ramp-ups that span months. Calibration, training and ensuring data continuity create switching barriers reinforced by typical multi-year contracts (12–36 months). Buyers favor vendor stickiness for mission-critical reliability, which tempers price pressure when performance is differentiated.

Demand cyclicality

Bargaining power of customers: Demand cyclicality is driven by oil and gas capex swings, with upstream investment around $470B in 2023 and modest 2024 recovery, producing sharp order peaks and troughs; in downturns buyers defer upgrades and press for discounts, while framework agreements and service offerings help smooth utilization and pricing. Defense and industrial contracts provide partial counter-cyclical ballast to revenues.

- High volatility: upstream capex cyclical

- Buyer leverage: discounting in downturns

- Mitigants: framework agreements, services

- Stabilizers: defense/industrial orders

Customization leverage

Defense and industrial clients often demand bespoke specs and compliance, which lengthen development cycles and shift technical and schedule risk to vendors; US defense spending reached about 858 billion USD in FY2024, sustaining demand but raising customer bargaining leverage. Milestone-based payments and recovery of non-recurring engineering costs are key negotiation points, while disciplined program management can convert customization into customer lock-in.

- Customization increases vendor risk and timeline

- Milestone payments and NRE recovery are negotiation levers

- FY2024 US defense budget ~858B USD underpins buyer demands

- Strong program management can create long-term lock-in

Large E&P, seismic and defense buyers drive pricing pressure amid long RFPs and high switching costs

Large E&P firms, seismic contractors and defense agencies account for a substantial share of Geospace Technologies’ demand, giving buyers leverage to press pricing and terms. Tender cycles (RFPs 6–18 months) and multi-year contracts (12–36 months) coexist with high switching costs (revalidation 4–12 weeks). Cyclicality: upstream capex ~$470B in 2023; US defense budget ~$858B FY2024; mitigants: services, framework agreements.

| Metric | Value |

|---|---|

| RFP cycle | 6–18 months |

| Contract length | 12–36 months |

| Revalidation | 4–12 weeks |

| Upstream capex (2023) | $470B |

| US defense FY2024 | $858B |

Full Version Awaits

Geospace Technologies Porter's Five Forces Analysis

This preview shows the exact Geospace Technologies Porter's Five Forces Analysis you'll receive—no placeholders, no mockups. The full document is fully formatted, professionally written, and ready for immediate download upon purchase. Use it as-is for decision-making, presentations, or further research.

Description

Don't Miss the Bigger Picture

Geospace Technologies faces moderate buyer power and niche supplier leverage, while industry rivalry hinges on specialized geophysical equipment and services; barriers to entry are medium due to technical know-how, and substitute threats remain limited. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Geospace Technologies’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized components concentration

Key inputs such as piezoelectric elements, ruggedized connectors, FPGAs/ASICs and defense-grade electronics are sourced from a narrow supplier base—TSMC and top foundries held roughly 50%+ of foundry share in 2024—concentrating leverage. Supplier concentration raises switching costs and single-source exposure, with semiconductor lead times often 10–20 weeks in tight cycles, pressuring margins. Dual-sourcing and design-for-substitution reduce but do not eliminate supplier bargaining power.

In-house manufacturing offsets

Geospace’s in-house design and build capabilities cut reliance on external suppliers for critical assemblies, supporting its FY2023 revenue base of about $106.6M and improving quality control and cost visibility. Vertical integration gives bargaining leverage in pricing and delivery negotiations, though it necessitates sustained capex and specialized process expertise to maintain competitive advantage.

Certification and compliance constraints

ITAR control by the DDTC and defense-specific certifications like AS9100 and ISO 9001 constrain Geospace’s supplier pool to qualified vendors, raising suppliers’ leverage. Compliance obligations and required traceability hinder rapid supplier switching and prolong lead times, increasing supplier power. Mandatory audits and batch traceability add cost and cycle time. Long-term agreements are often used to trade price for assured compliance and continuity.

Commodity inputs volatility

Commodity inputs—copper, specialty alloys and battery materials—leave Geospace exposed to swings; in 2024 battery-material markets remained volatile, amplifying input-cost risk. Suppliers can impose surcharges or minimum-buy terms; hedging and inventory buffers reduce price shock but lock up working capital, while customer pricing clauses often lag cost moves.

- Supplier leverage: surcharges/minimum buys

- Risk dampeners: hedging, inventory (capital tie-up)

- Timing gap: customer pricing lags costs

Geopolitical and logistics risks

Export controls and tariffs enacted through 2024 (notably expanded semiconductor controls) constrict access to specialty electronics and raise component lead times, while freight disruptions intermittently spiked expediting costs by roughly 25% in 2024 for electronics supply chains.

Extended global chains increase delivery risk and rush-shipping spend; regional qualification of alternates improves resilience but added ~10–15% sourcing overhead in 2024, and nearshoring plus higher safety stocks bolstered continuity at a 2–4% rise in annual working-capital cost.

- Export controls: tighter semiconductor and dual-use restrictions in 2024

- Freight/expedite: ~25% spike in 2024 peak expediting costs

- Regional qualification: +10–15% overhead in 2024

- Continuity measures: nearshoring and safety stock → +2–4% working-capital cost

Foundry dominance, 10-20 week lead times and +25% expedite costs squeeze margins

Supplier power is high: narrow sources for piezoelectrics, defense electronics and foundries (top foundries ~50%+ share in 2024) raise switching costs and 10–20 week lead times, pressuring margins. Geospace’s in-house build and vertical integration lower reliance but require capex. Compliance, export controls and commodity volatility (expedite +25% in 2024) sustain supplier leverage.

| Metric | 2024/Latest |

|---|---|

| Top foundry share | ~50%+ |

| Semiconductor lead times | 10–20 weeks |

| Expedite cost spike | ~+25% |

| Regional sourcing overhead | +10–15% |

| Working-capital rise | +2–4% |

| FY2023 revenue | $106.6M |

What is included in the product

Tailored Porter’s Five Forces analysis for Geospace Technologies revealing competitive intensity, supplier and buyer power, threat of substitutes and entrants, and disruptive forces shaping pricing, margins, and strategic positioning.

A concise one-sheet Porter's Five Forces for Geospace Technologies that highlights supplier, buyer, entrant, substitute, and competitive pressures—easy to customize, paste into decks, and update as market data shifts.

Customers Bargaining Power

Customer concentration

Large E&P firms, seismic contractors, and defense agencies account for a substantial share of Geospace Technologies’ demand, giving buyers leverage to push for aggressive pricing and contractual terms. The scale of these customers means loss of a major program can materially impact revenue and margins. Geospace’s diversification into industrial sensors and healthcare devices mitigates but does not eliminate customer concentration risk.

Tender-driven procurement

Formal RFPs and 6–18 month sales cycles in tender-driven procurement shift negotiating leverage to buyers; public procurement represents about 15% of global GDP per World Bank estimates, concentrating buyer power. Competitive bidding compresses margins and lengthens receivables. Offering value-added specs and lifecycle support enables premium pricing. Post-award change orders can add revenue but remain uncertain and timing-dependent.

High switching and integration costs

Seismic and monitoring systems tightly couple hardware, firmware and analytics workflows, making full replacements complex; in 2024 many projects reported revalidation times of 4–12 weeks and operational ramp-ups that span months. Calibration, training and ensuring data continuity create switching barriers reinforced by typical multi-year contracts (12–36 months). Buyers favor vendor stickiness for mission-critical reliability, which tempers price pressure when performance is differentiated.

Demand cyclicality

Bargaining power of customers: Demand cyclicality is driven by oil and gas capex swings, with upstream investment around $470B in 2023 and modest 2024 recovery, producing sharp order peaks and troughs; in downturns buyers defer upgrades and press for discounts, while framework agreements and service offerings help smooth utilization and pricing. Defense and industrial contracts provide partial counter-cyclical ballast to revenues.

- High volatility: upstream capex cyclical

- Buyer leverage: discounting in downturns

- Mitigants: framework agreements, services

- Stabilizers: defense/industrial orders

Customization leverage

Defense and industrial clients often demand bespoke specs and compliance, which lengthen development cycles and shift technical and schedule risk to vendors; US defense spending reached about 858 billion USD in FY2024, sustaining demand but raising customer bargaining leverage. Milestone-based payments and recovery of non-recurring engineering costs are key negotiation points, while disciplined program management can convert customization into customer lock-in.

- Customization increases vendor risk and timeline

- Milestone payments and NRE recovery are negotiation levers

- FY2024 US defense budget ~858B USD underpins buyer demands

- Strong program management can create long-term lock-in

Large E&P, seismic and defense buyers drive pricing pressure amid long RFPs and high switching costs

Large E&P firms, seismic contractors and defense agencies account for a substantial share of Geospace Technologies’ demand, giving buyers leverage to press pricing and terms. Tender cycles (RFPs 6–18 months) and multi-year contracts (12–36 months) coexist with high switching costs (revalidation 4–12 weeks). Cyclicality: upstream capex ~$470B in 2023; US defense budget ~$858B FY2024; mitigants: services, framework agreements.

| Metric | Value |

|---|---|

| RFP cycle | 6–18 months |

| Contract length | 12–36 months |

| Revalidation | 4–12 weeks |

| Upstream capex (2023) | $470B |

| US defense FY2024 | $858B |

Full Version Awaits

Geospace Technologies Porter's Five Forces Analysis

This preview shows the exact Geospace Technologies Porter's Five Forces Analysis you'll receive—no placeholders, no mockups. The full document is fully formatted, professionally written, and ready for immediate download upon purchase. Use it as-is for decision-making, presentations, or further research.