Geospace Technologies PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE analysis of Geospace Technologies—three concise perspectives on how political, economic, social, technological, legal, and environmental forces reshape its outlook. Ideal for investors and strategists, this brief shows where risks and opportunities converge. Purchase the full report to access detailed, actionable insights and editable charts for immediate use.

Political factors

Defense spending and procurement cycles

As a defense supplier, Geospace revenue tracks national budgets—US defense spending was about $858B in FY2024—so multi‑year procurements and continuing resolutions can defer orders into later quarters. Shifts toward ISR, border security, and infrastructure monitoring expand addressable markets, while international defense cooperation opens export opportunities but increases bid complexity and compliance costs.

Energy policy and exploration incentives

Oil and gas seismic demand hinges on political stances on drilling permits, leasing, and subsidies; pro-exploration policies historically lift seismic equipment orders while restrictive regimes compress activity and backlogs.

Strategic reserves and energy-security rhetoric drive upstream capex; U.S. crude output near 12.5 mb/d and a Strategic Petroleum Reserve around 366 million barrels (2024) shape investment signals.

State-level U.S. policy matters: Texas alone supplies roughly 40% of U.S. crude, creating regional booms tied to state leasing and permitting cycles.

Trade policy, tariffs, and localization

Tariffs on electronics and batteries, including US Section 301 duties up to 25% and steel/aluminum tariffs at 25%/10%, materially raise component and BOM costs for Geospace, squeezing margins or forcing higher prices.

Localization mandates in key markets drive in‑country assembly or JV formation; US policy incentives such as the CHIPS Act ($52 billion) and Inflation Reduction Act (~$369 billion) favor reshoring.

Geopolitical shifts are redirecting export routes and complicating logistics, increasing strategic inventory and supplier diversification needs.

Export controls and sanctions exposure

Seismic and defense-adjacent technologies used by Geospace are routinely subject to EAR/ITAR and allied export regimes, constraining transfers to sanctioned states such as Russia, Iran and Venezuela; these restrictions curb oilfield and sensing system sales and aftermarket support. Licensing requirements lengthen sales cycles and raise compliance costs, while geopolitical instability increases counterparty and service-delivery risk.

- Regimes: EAR/ITAR compliance mandatory

- Targets: Russia, Iran, Venezuela restricted

- Impact: longer deal cycle, higher compliance spend

- Risk: limited after-sales/service in unstable regions

Public infrastructure and smart city initiatives

- 55B water funding drives utility sensor procurement

- 350B ARP supports local metering upgrades

- Transparency rules tighten vendor compliance

US defense spending and tariffs accelerate reshoring, boosting sensor and procurement demand

US defense spend ~$858B (FY2024) drives multiyear procurements; EAR/ITAR restrict sales to Russia, Iran, Venezuela, lengthening cycles. Tariffs (Section 301 up to 25%, steel/aluminum 25%/10%) raise BOM costs. Infrastructure funds (BIL $1.2T incl. $55B water, ARP $350B) and CHIPS $52B/IRA ~$369B favor reshoring and sensor demand.

| Item | 2024/25 |

|---|---|

| Defense | $858B |

| SPR | 366M bbl |

| Tariffs | 25%/25%/10% |

| Infra/Stimulus | $1.2T/$350B/$55B |

What is included in the product

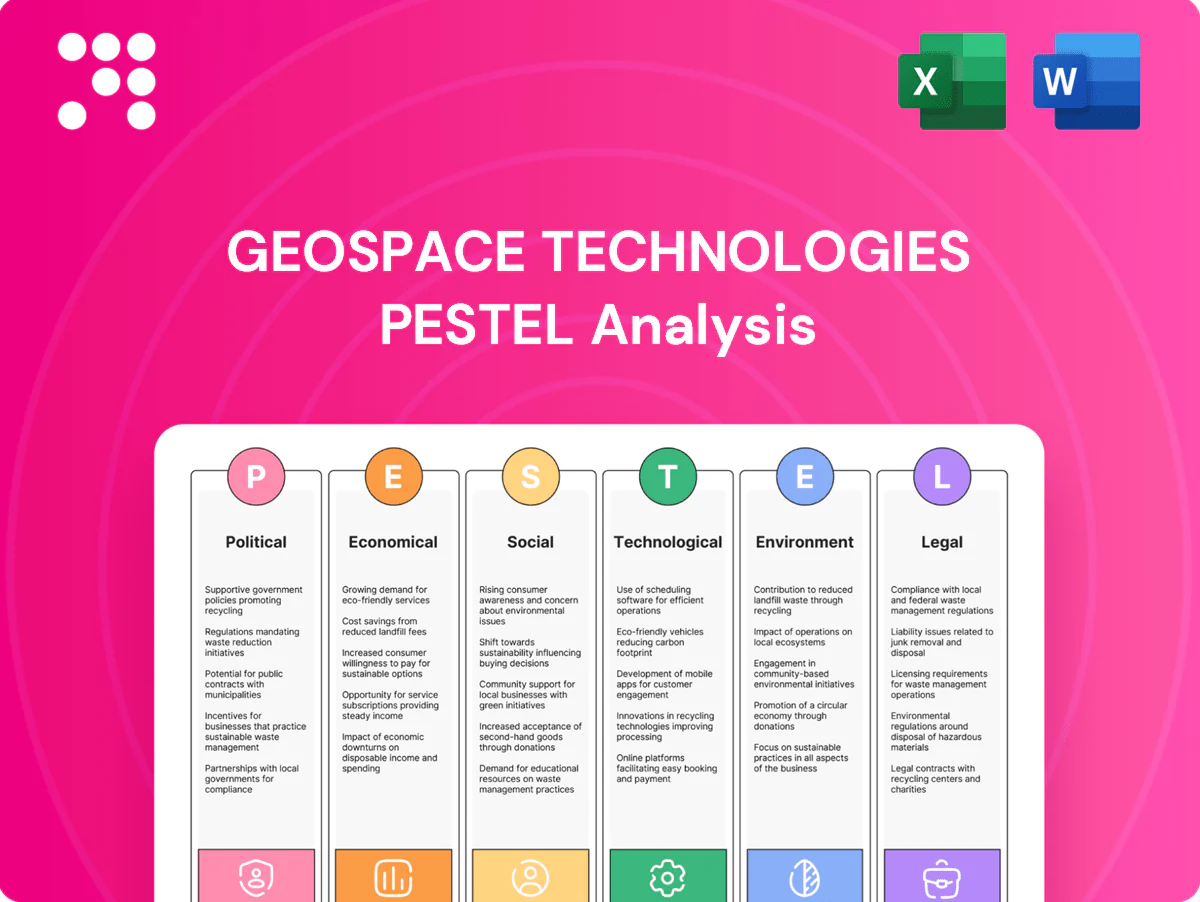

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Geospace Technologies, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clear implications to help executives, investors and consultants identify risks and strategic opportunities.

A concise, visually segmented PESTLE summary of Geospace Technologies that highlights external risks and opportunities for quick reference in meetings, easily modified with notes and dropped into presentations or shared across teams to support planning and client reports.

Economic factors

Oil price and E&P capex cyclicality

Seismic equipment orders move with E&P capex: global upstream spending recovery drove order swings after 2020 and with Brent averaging roughly $85/bbl in 2024 and trading near $80–83/bbl in H1 2025 backlog and utilization have shifted sharply. Geospace diversification into industrial, defense and healthcare cushions cyclicality but energy exposure remains; long‑lead projects (6–18 months) create a lag between price moves and bookings.

Interest rates and capital access

Higher benchmark rates (federal funds 5.25–5.50% mid‑2025) raise customer WACC, delaying discretionary sensor and monitoring upgrades and slowing GEO replacement cycles.

Rising rates increase Geospace’s inventory financing and working capital costs as commercial credit and SOFR‑linked loans remain elevated.

Budget‑constrained municipalities—in a roughly $4 trillion municipal bond market—may defer metering projects when borrowing costs spike; rate cuts can unlock pent‑up replacement demand.

Supply chain costs and component availability

Semiconductor lead times remain elevated at roughly 20 weeks and PCB lead times commonly run 8–12 weeks, while specialty cable lead times often exceed 12 weeks, constraining Geospace production. Freight costs averaged about USD 3,000 per 40ft container in 2024 (Drewry), squeezing margins and delivery reliability. Multi-sourcing and higher inventory levels raise working capital needs but lower stockout risk. A stronger USD in 2024 reduced import costs but pressured export competitiveness.

Defense and industrial demand resilience

Defense and critical‑infrastructure spending is relatively noncyclical, underpinned by global military outlays of about 2.24 trillion USD in 2023 (SIPRI), supporting baseline revenue for Geospace’s sensors and services. Industrial automation and condition‑monitoring purchases often persist in slowdowns when ROI is clear, while healthcare sensing benefits from steady reimbursement pathways, allowing a mix shift into higher‑margin niches to offset volume softness.

- Defense resilience: SIPRI 2023 = 2.24 trillion USD

- Industrial ROI drives sustained demand

- Healthcare sensing supported by reimbursement

- Mix shift to higher‑margin niches offsets volume

Global growth and emerging markets

Emerging-market urbanization—UN projects about 60% urbanization by 2030—drives demand for water metering and infrastructure monitoring, while a World Bank-estimated annual developing-country infrastructure gap of roughly 1.5 trillion USD underscores long-term opportunity. Currency volatility and rising sovereign/credit risk can delay order conversion despite demand, yet regional energy development programs and seismic spending create equipment demand; local partnerships speed market entry and service coverage.

- UN: 60% urban by 2030

- World Bank: ~1.5T USD infrastructure gap

- Currency/credit risk: can delay conversions

- Regional energy programs: boost seismic equipment demand

- Local partners: accelerate penetration

US defense spending and tariffs accelerate reshoring, boosting sensor and procurement demand

Seismic orders track E&P capex; Brent ~80–83 USD/bbl in H1 2025 and upstream recovery shifted backlog. Higher rates (Fed 5.25–5.50% mid‑2025) raise WACC, slowing discretionary buys; elevated input lead times and freight ($3,000/40ft in 2024) pressure working capital. Defense, healthcare and industrial spending (SIPRI 2023 = 2.24T USD) provide resilience.

| Metric | Value |

|---|---|

| Brent H1 2025 | 80–83 USD/bbl |

| Fed funds | 5.25–5.50% |

| Freight 2024 | ~3,000 USD/40ft |

| SIPRI 2023 | 2.24T USD |

What You See Is What You Get

Geospace Technologies PESTLE Analysis

The Geospace Technologies PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the file you’ll download instantly after payment. No placeholders, no teasers—this is the final, professional report.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE analysis of Geospace Technologies—three concise perspectives on how political, economic, social, technological, legal, and environmental forces reshape its outlook. Ideal for investors and strategists, this brief shows where risks and opportunities converge. Purchase the full report to access detailed, actionable insights and editable charts for immediate use.

Political factors

Defense spending and procurement cycles

As a defense supplier, Geospace revenue tracks national budgets—US defense spending was about $858B in FY2024—so multi‑year procurements and continuing resolutions can defer orders into later quarters. Shifts toward ISR, border security, and infrastructure monitoring expand addressable markets, while international defense cooperation opens export opportunities but increases bid complexity and compliance costs.

Energy policy and exploration incentives

Oil and gas seismic demand hinges on political stances on drilling permits, leasing, and subsidies; pro-exploration policies historically lift seismic equipment orders while restrictive regimes compress activity and backlogs.

Strategic reserves and energy-security rhetoric drive upstream capex; U.S. crude output near 12.5 mb/d and a Strategic Petroleum Reserve around 366 million barrels (2024) shape investment signals.

State-level U.S. policy matters: Texas alone supplies roughly 40% of U.S. crude, creating regional booms tied to state leasing and permitting cycles.

Trade policy, tariffs, and localization

Tariffs on electronics and batteries, including US Section 301 duties up to 25% and steel/aluminum tariffs at 25%/10%, materially raise component and BOM costs for Geospace, squeezing margins or forcing higher prices.

Localization mandates in key markets drive in‑country assembly or JV formation; US policy incentives such as the CHIPS Act ($52 billion) and Inflation Reduction Act (~$369 billion) favor reshoring.

Geopolitical shifts are redirecting export routes and complicating logistics, increasing strategic inventory and supplier diversification needs.

Export controls and sanctions exposure

Seismic and defense-adjacent technologies used by Geospace are routinely subject to EAR/ITAR and allied export regimes, constraining transfers to sanctioned states such as Russia, Iran and Venezuela; these restrictions curb oilfield and sensing system sales and aftermarket support. Licensing requirements lengthen sales cycles and raise compliance costs, while geopolitical instability increases counterparty and service-delivery risk.

- Regimes: EAR/ITAR compliance mandatory

- Targets: Russia, Iran, Venezuela restricted

- Impact: longer deal cycle, higher compliance spend

- Risk: limited after-sales/service in unstable regions

Public infrastructure and smart city initiatives

- 55B water funding drives utility sensor procurement

- 350B ARP supports local metering upgrades

- Transparency rules tighten vendor compliance

US defense spending and tariffs accelerate reshoring, boosting sensor and procurement demand

US defense spend ~$858B (FY2024) drives multiyear procurements; EAR/ITAR restrict sales to Russia, Iran, Venezuela, lengthening cycles. Tariffs (Section 301 up to 25%, steel/aluminum 25%/10%) raise BOM costs. Infrastructure funds (BIL $1.2T incl. $55B water, ARP $350B) and CHIPS $52B/IRA ~$369B favor reshoring and sensor demand.

| Item | 2024/25 |

|---|---|

| Defense | $858B |

| SPR | 366M bbl |

| Tariffs | 25%/25%/10% |

| Infra/Stimulus | $1.2T/$350B/$55B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Geospace Technologies, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clear implications to help executives, investors and consultants identify risks and strategic opportunities.

A concise, visually segmented PESTLE summary of Geospace Technologies that highlights external risks and opportunities for quick reference in meetings, easily modified with notes and dropped into presentations or shared across teams to support planning and client reports.

Economic factors

Oil price and E&P capex cyclicality

Seismic equipment orders move with E&P capex: global upstream spending recovery drove order swings after 2020 and with Brent averaging roughly $85/bbl in 2024 and trading near $80–83/bbl in H1 2025 backlog and utilization have shifted sharply. Geospace diversification into industrial, defense and healthcare cushions cyclicality but energy exposure remains; long‑lead projects (6–18 months) create a lag between price moves and bookings.

Interest rates and capital access

Higher benchmark rates (federal funds 5.25–5.50% mid‑2025) raise customer WACC, delaying discretionary sensor and monitoring upgrades and slowing GEO replacement cycles.

Rising rates increase Geospace’s inventory financing and working capital costs as commercial credit and SOFR‑linked loans remain elevated.

Budget‑constrained municipalities—in a roughly $4 trillion municipal bond market—may defer metering projects when borrowing costs spike; rate cuts can unlock pent‑up replacement demand.

Supply chain costs and component availability

Semiconductor lead times remain elevated at roughly 20 weeks and PCB lead times commonly run 8–12 weeks, while specialty cable lead times often exceed 12 weeks, constraining Geospace production. Freight costs averaged about USD 3,000 per 40ft container in 2024 (Drewry), squeezing margins and delivery reliability. Multi-sourcing and higher inventory levels raise working capital needs but lower stockout risk. A stronger USD in 2024 reduced import costs but pressured export competitiveness.

Defense and industrial demand resilience

Defense and critical‑infrastructure spending is relatively noncyclical, underpinned by global military outlays of about 2.24 trillion USD in 2023 (SIPRI), supporting baseline revenue for Geospace’s sensors and services. Industrial automation and condition‑monitoring purchases often persist in slowdowns when ROI is clear, while healthcare sensing benefits from steady reimbursement pathways, allowing a mix shift into higher‑margin niches to offset volume softness.

- Defense resilience: SIPRI 2023 = 2.24 trillion USD

- Industrial ROI drives sustained demand

- Healthcare sensing supported by reimbursement

- Mix shift to higher‑margin niches offsets volume

Global growth and emerging markets

Emerging-market urbanization—UN projects about 60% urbanization by 2030—drives demand for water metering and infrastructure monitoring, while a World Bank-estimated annual developing-country infrastructure gap of roughly 1.5 trillion USD underscores long-term opportunity. Currency volatility and rising sovereign/credit risk can delay order conversion despite demand, yet regional energy development programs and seismic spending create equipment demand; local partnerships speed market entry and service coverage.

- UN: 60% urban by 2030

- World Bank: ~1.5T USD infrastructure gap

- Currency/credit risk: can delay conversions

- Regional energy programs: boost seismic equipment demand

- Local partners: accelerate penetration

US defense spending and tariffs accelerate reshoring, boosting sensor and procurement demand

Seismic orders track E&P capex; Brent ~80–83 USD/bbl in H1 2025 and upstream recovery shifted backlog. Higher rates (Fed 5.25–5.50% mid‑2025) raise WACC, slowing discretionary buys; elevated input lead times and freight ($3,000/40ft in 2024) pressure working capital. Defense, healthcare and industrial spending (SIPRI 2023 = 2.24T USD) provide resilience.

| Metric | Value |

|---|---|

| Brent H1 2025 | 80–83 USD/bbl |

| Fed funds | 5.25–5.50% |

| Freight 2024 | ~3,000 USD/40ft |

| SIPRI 2023 | 2.24T USD |

What You See Is What You Get

Geospace Technologies PESTLE Analysis

The Geospace Technologies PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the file you’ll download instantly after payment. No placeholders, no teasers—this is the final, professional report.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE analysis of Geospace Technologies—three concise perspectives on how political, economic, social, technological, legal, and environmental forces reshape its outlook. Ideal for investors and strategists, this brief shows where risks and opportunities converge. Purchase the full report to access detailed, actionable insights and editable charts for immediate use.

Political factors

Defense spending and procurement cycles

As a defense supplier, Geospace revenue tracks national budgets—US defense spending was about $858B in FY2024—so multi‑year procurements and continuing resolutions can defer orders into later quarters. Shifts toward ISR, border security, and infrastructure monitoring expand addressable markets, while international defense cooperation opens export opportunities but increases bid complexity and compliance costs.

Energy policy and exploration incentives

Oil and gas seismic demand hinges on political stances on drilling permits, leasing, and subsidies; pro-exploration policies historically lift seismic equipment orders while restrictive regimes compress activity and backlogs.

Strategic reserves and energy-security rhetoric drive upstream capex; U.S. crude output near 12.5 mb/d and a Strategic Petroleum Reserve around 366 million barrels (2024) shape investment signals.

State-level U.S. policy matters: Texas alone supplies roughly 40% of U.S. crude, creating regional booms tied to state leasing and permitting cycles.

Trade policy, tariffs, and localization

Tariffs on electronics and batteries, including US Section 301 duties up to 25% and steel/aluminum tariffs at 25%/10%, materially raise component and BOM costs for Geospace, squeezing margins or forcing higher prices.

Localization mandates in key markets drive in‑country assembly or JV formation; US policy incentives such as the CHIPS Act ($52 billion) and Inflation Reduction Act (~$369 billion) favor reshoring.

Geopolitical shifts are redirecting export routes and complicating logistics, increasing strategic inventory and supplier diversification needs.

Export controls and sanctions exposure

Seismic and defense-adjacent technologies used by Geospace are routinely subject to EAR/ITAR and allied export regimes, constraining transfers to sanctioned states such as Russia, Iran and Venezuela; these restrictions curb oilfield and sensing system sales and aftermarket support. Licensing requirements lengthen sales cycles and raise compliance costs, while geopolitical instability increases counterparty and service-delivery risk.

- Regimes: EAR/ITAR compliance mandatory

- Targets: Russia, Iran, Venezuela restricted

- Impact: longer deal cycle, higher compliance spend

- Risk: limited after-sales/service in unstable regions

Public infrastructure and smart city initiatives

- 55B water funding drives utility sensor procurement

- 350B ARP supports local metering upgrades

- Transparency rules tighten vendor compliance

US defense spending and tariffs accelerate reshoring, boosting sensor and procurement demand

US defense spend ~$858B (FY2024) drives multiyear procurements; EAR/ITAR restrict sales to Russia, Iran, Venezuela, lengthening cycles. Tariffs (Section 301 up to 25%, steel/aluminum 25%/10%) raise BOM costs. Infrastructure funds (BIL $1.2T incl. $55B water, ARP $350B) and CHIPS $52B/IRA ~$369B favor reshoring and sensor demand.

| Item | 2024/25 |

|---|---|

| Defense | $858B |

| SPR | 366M bbl |

| Tariffs | 25%/25%/10% |

| Infra/Stimulus | $1.2T/$350B/$55B |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Geospace Technologies, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clear implications to help executives, investors and consultants identify risks and strategic opportunities.

A concise, visually segmented PESTLE summary of Geospace Technologies that highlights external risks and opportunities for quick reference in meetings, easily modified with notes and dropped into presentations or shared across teams to support planning and client reports.

Economic factors

Oil price and E&P capex cyclicality

Seismic equipment orders move with E&P capex: global upstream spending recovery drove order swings after 2020 and with Brent averaging roughly $85/bbl in 2024 and trading near $80–83/bbl in H1 2025 backlog and utilization have shifted sharply. Geospace diversification into industrial, defense and healthcare cushions cyclicality but energy exposure remains; long‑lead projects (6–18 months) create a lag between price moves and bookings.

Interest rates and capital access

Higher benchmark rates (federal funds 5.25–5.50% mid‑2025) raise customer WACC, delaying discretionary sensor and monitoring upgrades and slowing GEO replacement cycles.

Rising rates increase Geospace’s inventory financing and working capital costs as commercial credit and SOFR‑linked loans remain elevated.

Budget‑constrained municipalities—in a roughly $4 trillion municipal bond market—may defer metering projects when borrowing costs spike; rate cuts can unlock pent‑up replacement demand.

Supply chain costs and component availability

Semiconductor lead times remain elevated at roughly 20 weeks and PCB lead times commonly run 8–12 weeks, while specialty cable lead times often exceed 12 weeks, constraining Geospace production. Freight costs averaged about USD 3,000 per 40ft container in 2024 (Drewry), squeezing margins and delivery reliability. Multi-sourcing and higher inventory levels raise working capital needs but lower stockout risk. A stronger USD in 2024 reduced import costs but pressured export competitiveness.

Defense and industrial demand resilience

Defense and critical‑infrastructure spending is relatively noncyclical, underpinned by global military outlays of about 2.24 trillion USD in 2023 (SIPRI), supporting baseline revenue for Geospace’s sensors and services. Industrial automation and condition‑monitoring purchases often persist in slowdowns when ROI is clear, while healthcare sensing benefits from steady reimbursement pathways, allowing a mix shift into higher‑margin niches to offset volume softness.

- Defense resilience: SIPRI 2023 = 2.24 trillion USD

- Industrial ROI drives sustained demand

- Healthcare sensing supported by reimbursement

- Mix shift to higher‑margin niches offsets volume

Global growth and emerging markets

Emerging-market urbanization—UN projects about 60% urbanization by 2030—drives demand for water metering and infrastructure monitoring, while a World Bank-estimated annual developing-country infrastructure gap of roughly 1.5 trillion USD underscores long-term opportunity. Currency volatility and rising sovereign/credit risk can delay order conversion despite demand, yet regional energy development programs and seismic spending create equipment demand; local partnerships speed market entry and service coverage.

- UN: 60% urban by 2030

- World Bank: ~1.5T USD infrastructure gap

- Currency/credit risk: can delay conversions

- Regional energy programs: boost seismic equipment demand

- Local partners: accelerate penetration

US defense spending and tariffs accelerate reshoring, boosting sensor and procurement demand

Seismic orders track E&P capex; Brent ~80–83 USD/bbl in H1 2025 and upstream recovery shifted backlog. Higher rates (Fed 5.25–5.50% mid‑2025) raise WACC, slowing discretionary buys; elevated input lead times and freight ($3,000/40ft in 2024) pressure working capital. Defense, healthcare and industrial spending (SIPRI 2023 = 2.24T USD) provide resilience.

| Metric | Value |

|---|---|

| Brent H1 2025 | 80–83 USD/bbl |

| Fed funds | 5.25–5.50% |

| Freight 2024 | ~3,000 USD/40ft |

| SIPRI 2023 | 2.24T USD |

What You See Is What You Get

Geospace Technologies PESTLE Analysis

The Geospace Technologies PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the file you’ll download instantly after payment. No placeholders, no teasers—this is the final, professional report.