Getinge Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

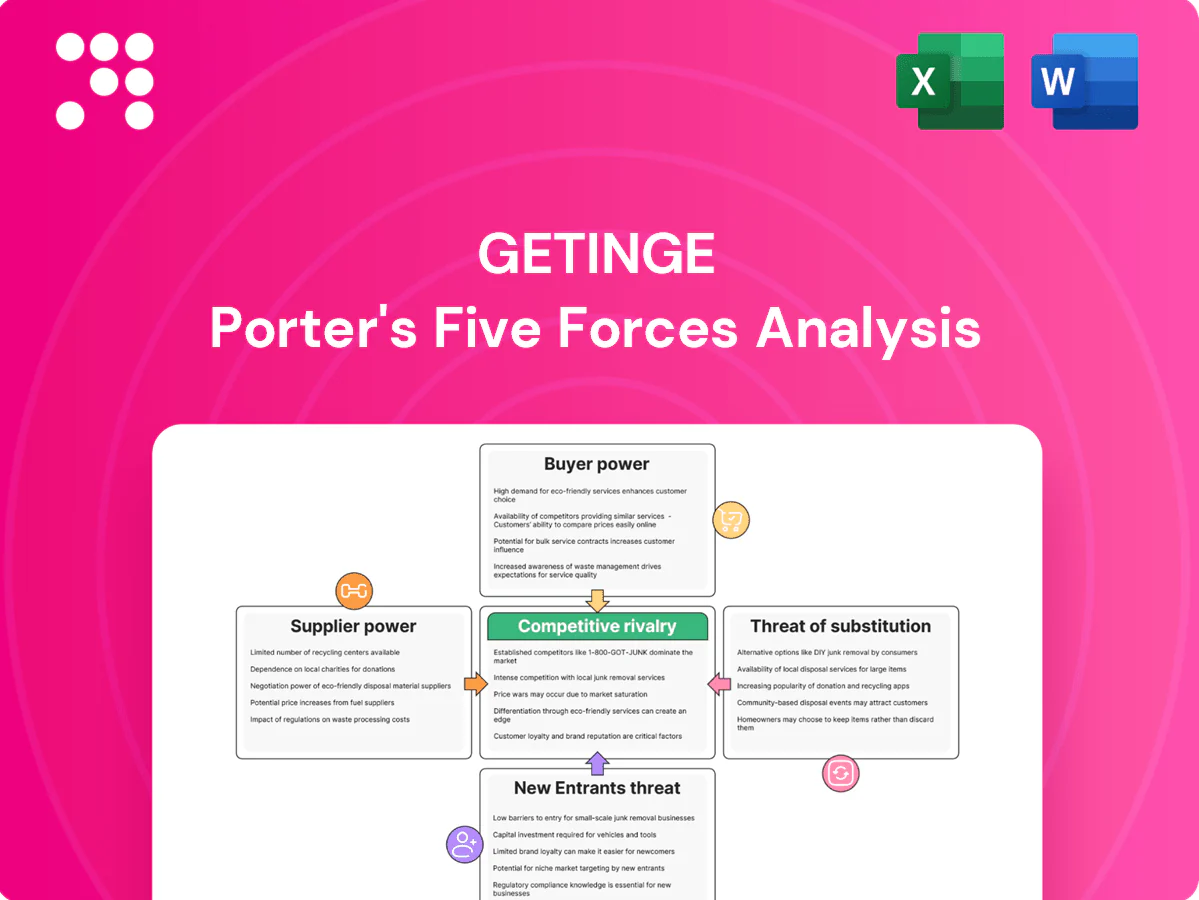

Getinge faces moderate buyer power, technological threats from rivals, and strict regulatory pressures that shape its pricing and innovation strategies. Our snapshot highlights supplier leverage and potential substitute risks but only scratches the surface of competitive intensity and market entry barriers. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Specialized components scarcity

Many critical parts (sterilization chambers, pumps, sensors, ventilator modules) are sourced from niche suppliers with few alternatives, increasing supplier leverage over lead times and pricing. Certification and validation requirements make switching slow and costly, often taking months of requalification. Dual-sourcing can mitigate risk but is frequently infeasible due to qualification barriers and low supplier redundancy.

Regulatory-locked specifications

Designs tied to MDR/FDA approvals lock specific materials and subsystems, making suppliers sticky; requalifying a new supplier typically requires 6–12 months of testing, filings and clinical risk reviews and can cost up to $500k per device, raising supplier leverage. Regulatory inertia increases supplier influence over pricing and lead times, though multi-year framework agreements can cap annual cost increases to around 3–5%.

Global supply chain exposure

Inputs for Getinge span metals, polymers, electronics and software sourced across regions; East Asia supplied roughly 70% of global electronics production in 2024 while China accounted for about 30% of global manufacturing output in 2024. Geopolitical shocks and export controls in 2024 tightened availability, and logistics bottlenecks pushed lead times up to ~4 weeks, shifting bargaining power to timely suppliers. Inventory buffers mitigated shortages but raised working capital needs, with inventories up an estimated ~4% year-on-year in 2024.

Standard parts vs bespoke trade-off

Where standard components exist, competitive quoting and multiple suppliers reduce supplier power, but bespoke life-science skids and OR integration require specialized vendors, narrowing options and raising leverage for those suppliers. The mix produces moderate average supplier power with pockets of high leverage in customization-heavy lines; strategic partnerships and long-term contracts help stabilize terms and mitigate price volatility.

- Standard parts: low supplier power

- Bespoke skids/OR: high supplier leverage

- Overall: moderate power; partnerships reduce risk

Service and software dependencies

Embedded software, cybersecurity updates and field-service tooling in Getinge systems depend heavily on third-party vendors, creating recurring support and license obligations that extend supplier influence beyond the initial BOM; contractual SLAs are used to mitigate outage and compliance risks.

- Third-party dependency

- Recurring licenses & support

- Vendor-driven lifecycle costs

- Contractual SLAs reduce outage risk

Supply risk: East Asia 70%, China 30%, lead times ~4w

Suppliers hold moderate power: niche parts and regulatory-tied designs create high leverage (requalification 6–12 months, up to 500000 USD); East Asia electronics ~70% (2024), China ~30% manufacturing (2024); lead times ~4 weeks, inventories +4% YoY (2024); multi-year contracts cap price rises ~3–5%.

| Metric | Value (2024) |

|---|---|

| Electronics share | 70% |

| China manufacturing | 30% |

| Lead times | ~4 weeks |

| Inventory YoY | +4% |

| Requal. cost/time | 500000 USD / 6–12m |

What is included in the product

Tailored Porter's Five Forces analysis for Getinge that uncovers competitive drivers, supplier and buyer power, substitutes, and entry barriers affecting its market position. Highlights disruptive threats and strategic levers to protect margins and guide investor or management decisions.

A concise one-sheet Porter’s Five Forces for Getinge that visualizes competitive pressures with a radar chart and lets you swap in current data—ideal for rapid strategic decisions and slide-ready reporting.

Customers Bargaining Power

Consolidated hospital purchasing

Consolidated purchasing via GPOs and national tenders concentrates demand—US GPOs influence procurement for roughly 80–90% of hospitals—sharpening price negotiations against Getinge. Large IDNs and public systems, controlling over half of hospital beds in many markets, pit vendors to extract lower bids. Volume commitments commonly secure discounts of 10–30% plus service concessions. Tender cycles produce step-change pricing, with award-driven price drops often in the low double digits.

High switching and validation costs

Workflow retraining, sterility validation and IT integration create significant lock-in for Getinge customers, as re-certifying protocols and retraining staff interrupt clinical routines and raise costs; downtime risks and strict clinical protocols deter frequent switching, softening buyer power after installation. Multi-year service contracts and long replacement cycles further reinforce continuity.

Total cost of ownership focus

Buyers weigh uptime, consumables, energy and service in purchase decisions, with 2024 industry studies showing transparent TCO modeling can reduce lifecycle costs by up to 25%. Clear TCO models enable negotiation of service levels and uptime guarantees and support unbundling of consumables. Performance‑based contracts, now used in roughly 20% of large hospital procurements in 2024, shift performance and uptime risk to vendors, increasing buyer leverage on lifecycle terms.

Clinical outcomes and compliance

If equipment demonstrably improves clinical outcomes or infection control, willingness to pay rises; evidence and guideline endorsements narrow substitution sets and reduce price sensitivity for high-impact systems. CDC estimates 1 in 31 US hospital patients has a healthcare-associated infection on any given day, and HAIs impose multi-billion dollar annual costs, so value dossiers become decisive in procurement negotiations.

- Outcome-driven premiums: lower substitution, higher WTP

- Guideline alignment: narrows vendor pool

- CDC stat: 1 in 31 patients with HAI

- Value dossiers: key negotiation tool

Digital and interoperability demands

Hospitals demand EMR connectivity, robust cybersecurity and analytics; with about 96% of US hospitals using certified EHRs, integration and data-security clauses are standard. CMS FHIR API mandates since 2023 strengthen buyer leverage, creating negotiation points and contractual penalties for non-compliance. A clear digital roadmap and certified interoperability reduce buyer resistance and warranty costs.

- 96% EHR adoption — higher leverage for buyers

- CMS FHIR rules (since 2023) — data standards mandate

- Integration clauses/penalties — negotiation leverage

GPO/IDN buying yields 10–30% discounts; TCO cuts 25%

Buyers concentrate purchasing via GPOs/IDNs (GPOs influence ~80–90% of US hospitals; many IDNs control >50% of beds), driving 10–30% typical volume discounts and step‑change tender price drops. Switching costs and service contracts create lock‑in, but transparent TCO (can cut lifecycle costs ~25%) and 20% use of performance contracts (2024) increase leverage. Clinical value and HAI impact (CDC: 1 in 31 patients) raise WTP for proven systems.

| Metric | Value (2024) |

|---|---|

| GPO influence | 80–90% |

| Volume discounts | 10–30% |

| Perf. contracts | 20% |

| EHR adoption | 96% |

| HAI prevalence | 1 in 31 |

What You See Is What You Get

Getinge Porter's Five Forces Analysis

This preview displays the exact Getinge Porter's Five Forces Analysis you'll receive upon purchase—no mockups, no placeholders. It is the final, professionally formatted document, ready for immediate download and use. What you see here is precisely what will be delivered to you after payment.

A Must-Have Tool for Decision-Makers

Getinge faces moderate buyer power, technological threats from rivals, and strict regulatory pressures that shape its pricing and innovation strategies. Our snapshot highlights supplier leverage and potential substitute risks but only scratches the surface of competitive intensity and market entry barriers. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Specialized components scarcity

Many critical parts (sterilization chambers, pumps, sensors, ventilator modules) are sourced from niche suppliers with few alternatives, increasing supplier leverage over lead times and pricing. Certification and validation requirements make switching slow and costly, often taking months of requalification. Dual-sourcing can mitigate risk but is frequently infeasible due to qualification barriers and low supplier redundancy.

Regulatory-locked specifications

Designs tied to MDR/FDA approvals lock specific materials and subsystems, making suppliers sticky; requalifying a new supplier typically requires 6–12 months of testing, filings and clinical risk reviews and can cost up to $500k per device, raising supplier leverage. Regulatory inertia increases supplier influence over pricing and lead times, though multi-year framework agreements can cap annual cost increases to around 3–5%.

Global supply chain exposure

Inputs for Getinge span metals, polymers, electronics and software sourced across regions; East Asia supplied roughly 70% of global electronics production in 2024 while China accounted for about 30% of global manufacturing output in 2024. Geopolitical shocks and export controls in 2024 tightened availability, and logistics bottlenecks pushed lead times up to ~4 weeks, shifting bargaining power to timely suppliers. Inventory buffers mitigated shortages but raised working capital needs, with inventories up an estimated ~4% year-on-year in 2024.

Standard parts vs bespoke trade-off

Where standard components exist, competitive quoting and multiple suppliers reduce supplier power, but bespoke life-science skids and OR integration require specialized vendors, narrowing options and raising leverage for those suppliers. The mix produces moderate average supplier power with pockets of high leverage in customization-heavy lines; strategic partnerships and long-term contracts help stabilize terms and mitigate price volatility.

- Standard parts: low supplier power

- Bespoke skids/OR: high supplier leverage

- Overall: moderate power; partnerships reduce risk

Service and software dependencies

Embedded software, cybersecurity updates and field-service tooling in Getinge systems depend heavily on third-party vendors, creating recurring support and license obligations that extend supplier influence beyond the initial BOM; contractual SLAs are used to mitigate outage and compliance risks.

- Third-party dependency

- Recurring licenses & support

- Vendor-driven lifecycle costs

- Contractual SLAs reduce outage risk

Supply risk: East Asia 70%, China 30%, lead times ~4w

Suppliers hold moderate power: niche parts and regulatory-tied designs create high leverage (requalification 6–12 months, up to 500000 USD); East Asia electronics ~70% (2024), China ~30% manufacturing (2024); lead times ~4 weeks, inventories +4% YoY (2024); multi-year contracts cap price rises ~3–5%.

| Metric | Value (2024) |

|---|---|

| Electronics share | 70% |

| China manufacturing | 30% |

| Lead times | ~4 weeks |

| Inventory YoY | +4% |

| Requal. cost/time | 500000 USD / 6–12m |

What is included in the product

Tailored Porter's Five Forces analysis for Getinge that uncovers competitive drivers, supplier and buyer power, substitutes, and entry barriers affecting its market position. Highlights disruptive threats and strategic levers to protect margins and guide investor or management decisions.

A concise one-sheet Porter’s Five Forces for Getinge that visualizes competitive pressures with a radar chart and lets you swap in current data—ideal for rapid strategic decisions and slide-ready reporting.

Customers Bargaining Power

Consolidated hospital purchasing

Consolidated purchasing via GPOs and national tenders concentrates demand—US GPOs influence procurement for roughly 80–90% of hospitals—sharpening price negotiations against Getinge. Large IDNs and public systems, controlling over half of hospital beds in many markets, pit vendors to extract lower bids. Volume commitments commonly secure discounts of 10–30% plus service concessions. Tender cycles produce step-change pricing, with award-driven price drops often in the low double digits.

High switching and validation costs

Workflow retraining, sterility validation and IT integration create significant lock-in for Getinge customers, as re-certifying protocols and retraining staff interrupt clinical routines and raise costs; downtime risks and strict clinical protocols deter frequent switching, softening buyer power after installation. Multi-year service contracts and long replacement cycles further reinforce continuity.

Total cost of ownership focus

Buyers weigh uptime, consumables, energy and service in purchase decisions, with 2024 industry studies showing transparent TCO modeling can reduce lifecycle costs by up to 25%. Clear TCO models enable negotiation of service levels and uptime guarantees and support unbundling of consumables. Performance‑based contracts, now used in roughly 20% of large hospital procurements in 2024, shift performance and uptime risk to vendors, increasing buyer leverage on lifecycle terms.

Clinical outcomes and compliance

If equipment demonstrably improves clinical outcomes or infection control, willingness to pay rises; evidence and guideline endorsements narrow substitution sets and reduce price sensitivity for high-impact systems. CDC estimates 1 in 31 US hospital patients has a healthcare-associated infection on any given day, and HAIs impose multi-billion dollar annual costs, so value dossiers become decisive in procurement negotiations.

- Outcome-driven premiums: lower substitution, higher WTP

- Guideline alignment: narrows vendor pool

- CDC stat: 1 in 31 patients with HAI

- Value dossiers: key negotiation tool

Digital and interoperability demands

Hospitals demand EMR connectivity, robust cybersecurity and analytics; with about 96% of US hospitals using certified EHRs, integration and data-security clauses are standard. CMS FHIR API mandates since 2023 strengthen buyer leverage, creating negotiation points and contractual penalties for non-compliance. A clear digital roadmap and certified interoperability reduce buyer resistance and warranty costs.

- 96% EHR adoption — higher leverage for buyers

- CMS FHIR rules (since 2023) — data standards mandate

- Integration clauses/penalties — negotiation leverage

GPO/IDN buying yields 10–30% discounts; TCO cuts 25%

Buyers concentrate purchasing via GPOs/IDNs (GPOs influence ~80–90% of US hospitals; many IDNs control >50% of beds), driving 10–30% typical volume discounts and step‑change tender price drops. Switching costs and service contracts create lock‑in, but transparent TCO (can cut lifecycle costs ~25%) and 20% use of performance contracts (2024) increase leverage. Clinical value and HAI impact (CDC: 1 in 31 patients) raise WTP for proven systems.

| Metric | Value (2024) |

|---|---|

| GPO influence | 80–90% |

| Volume discounts | 10–30% |

| Perf. contracts | 20% |

| EHR adoption | 96% |

| HAI prevalence | 1 in 31 |

What You See Is What You Get

Getinge Porter's Five Forces Analysis

This preview displays the exact Getinge Porter's Five Forces Analysis you'll receive upon purchase—no mockups, no placeholders. It is the final, professionally formatted document, ready for immediate download and use. What you see here is precisely what will be delivered to you after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Getinge faces moderate buyer power, technological threats from rivals, and strict regulatory pressures that shape its pricing and innovation strategies. Our snapshot highlights supplier leverage and potential substitute risks but only scratches the surface of competitive intensity and market entry barriers. This preview is just the beginning—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Specialized components scarcity

Many critical parts (sterilization chambers, pumps, sensors, ventilator modules) are sourced from niche suppliers with few alternatives, increasing supplier leverage over lead times and pricing. Certification and validation requirements make switching slow and costly, often taking months of requalification. Dual-sourcing can mitigate risk but is frequently infeasible due to qualification barriers and low supplier redundancy.

Regulatory-locked specifications

Designs tied to MDR/FDA approvals lock specific materials and subsystems, making suppliers sticky; requalifying a new supplier typically requires 6–12 months of testing, filings and clinical risk reviews and can cost up to $500k per device, raising supplier leverage. Regulatory inertia increases supplier influence over pricing and lead times, though multi-year framework agreements can cap annual cost increases to around 3–5%.

Global supply chain exposure

Inputs for Getinge span metals, polymers, electronics and software sourced across regions; East Asia supplied roughly 70% of global electronics production in 2024 while China accounted for about 30% of global manufacturing output in 2024. Geopolitical shocks and export controls in 2024 tightened availability, and logistics bottlenecks pushed lead times up to ~4 weeks, shifting bargaining power to timely suppliers. Inventory buffers mitigated shortages but raised working capital needs, with inventories up an estimated ~4% year-on-year in 2024.

Standard parts vs bespoke trade-off

Where standard components exist, competitive quoting and multiple suppliers reduce supplier power, but bespoke life-science skids and OR integration require specialized vendors, narrowing options and raising leverage for those suppliers. The mix produces moderate average supplier power with pockets of high leverage in customization-heavy lines; strategic partnerships and long-term contracts help stabilize terms and mitigate price volatility.

- Standard parts: low supplier power

- Bespoke skids/OR: high supplier leverage

- Overall: moderate power; partnerships reduce risk

Service and software dependencies

Embedded software, cybersecurity updates and field-service tooling in Getinge systems depend heavily on third-party vendors, creating recurring support and license obligations that extend supplier influence beyond the initial BOM; contractual SLAs are used to mitigate outage and compliance risks.

- Third-party dependency

- Recurring licenses & support

- Vendor-driven lifecycle costs

- Contractual SLAs reduce outage risk

Supply risk: East Asia 70%, China 30%, lead times ~4w

Suppliers hold moderate power: niche parts and regulatory-tied designs create high leverage (requalification 6–12 months, up to 500000 USD); East Asia electronics ~70% (2024), China ~30% manufacturing (2024); lead times ~4 weeks, inventories +4% YoY (2024); multi-year contracts cap price rises ~3–5%.

| Metric | Value (2024) |

|---|---|

| Electronics share | 70% |

| China manufacturing | 30% |

| Lead times | ~4 weeks |

| Inventory YoY | +4% |

| Requal. cost/time | 500000 USD / 6–12m |

What is included in the product

Tailored Porter's Five Forces analysis for Getinge that uncovers competitive drivers, supplier and buyer power, substitutes, and entry barriers affecting its market position. Highlights disruptive threats and strategic levers to protect margins and guide investor or management decisions.

A concise one-sheet Porter’s Five Forces for Getinge that visualizes competitive pressures with a radar chart and lets you swap in current data—ideal for rapid strategic decisions and slide-ready reporting.

Customers Bargaining Power

Consolidated hospital purchasing

Consolidated purchasing via GPOs and national tenders concentrates demand—US GPOs influence procurement for roughly 80–90% of hospitals—sharpening price negotiations against Getinge. Large IDNs and public systems, controlling over half of hospital beds in many markets, pit vendors to extract lower bids. Volume commitments commonly secure discounts of 10–30% plus service concessions. Tender cycles produce step-change pricing, with award-driven price drops often in the low double digits.

High switching and validation costs

Workflow retraining, sterility validation and IT integration create significant lock-in for Getinge customers, as re-certifying protocols and retraining staff interrupt clinical routines and raise costs; downtime risks and strict clinical protocols deter frequent switching, softening buyer power after installation. Multi-year service contracts and long replacement cycles further reinforce continuity.

Total cost of ownership focus

Buyers weigh uptime, consumables, energy and service in purchase decisions, with 2024 industry studies showing transparent TCO modeling can reduce lifecycle costs by up to 25%. Clear TCO models enable negotiation of service levels and uptime guarantees and support unbundling of consumables. Performance‑based contracts, now used in roughly 20% of large hospital procurements in 2024, shift performance and uptime risk to vendors, increasing buyer leverage on lifecycle terms.

Clinical outcomes and compliance

If equipment demonstrably improves clinical outcomes or infection control, willingness to pay rises; evidence and guideline endorsements narrow substitution sets and reduce price sensitivity for high-impact systems. CDC estimates 1 in 31 US hospital patients has a healthcare-associated infection on any given day, and HAIs impose multi-billion dollar annual costs, so value dossiers become decisive in procurement negotiations.

- Outcome-driven premiums: lower substitution, higher WTP

- Guideline alignment: narrows vendor pool

- CDC stat: 1 in 31 patients with HAI

- Value dossiers: key negotiation tool

Digital and interoperability demands

Hospitals demand EMR connectivity, robust cybersecurity and analytics; with about 96% of US hospitals using certified EHRs, integration and data-security clauses are standard. CMS FHIR API mandates since 2023 strengthen buyer leverage, creating negotiation points and contractual penalties for non-compliance. A clear digital roadmap and certified interoperability reduce buyer resistance and warranty costs.

- 96% EHR adoption — higher leverage for buyers

- CMS FHIR rules (since 2023) — data standards mandate

- Integration clauses/penalties — negotiation leverage

GPO/IDN buying yields 10–30% discounts; TCO cuts 25%

Buyers concentrate purchasing via GPOs/IDNs (GPOs influence ~80–90% of US hospitals; many IDNs control >50% of beds), driving 10–30% typical volume discounts and step‑change tender price drops. Switching costs and service contracts create lock‑in, but transparent TCO (can cut lifecycle costs ~25%) and 20% use of performance contracts (2024) increase leverage. Clinical value and HAI impact (CDC: 1 in 31 patients) raise WTP for proven systems.

| Metric | Value (2024) |

|---|---|

| GPO influence | 80–90% |

| Volume discounts | 10–30% |

| Perf. contracts | 20% |

| EHR adoption | 96% |

| HAI prevalence | 1 in 31 |

What You See Is What You Get

Getinge Porter's Five Forces Analysis

This preview displays the exact Getinge Porter's Five Forces Analysis you'll receive upon purchase—no mockups, no placeholders. It is the final, professionally formatted document, ready for immediate download and use. What you see here is precisely what will be delivered to you after payment.