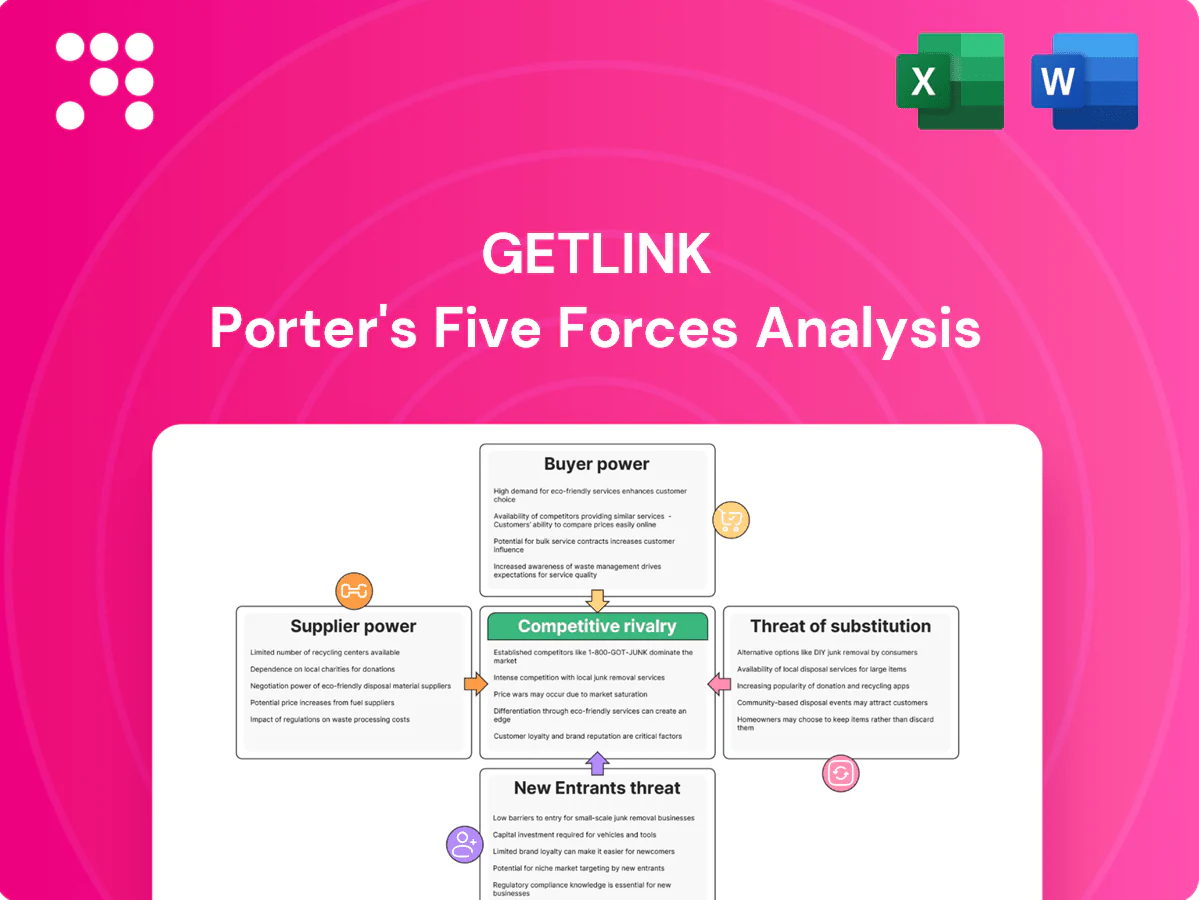

Getlink Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Getlink faces moderate buyer power, steady supplier influence, and barriers shaped by infrastructure and regulation; substitutes are limited but tech and modal shifts pose emerging threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Getlink’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized tunnel systems vendors

Highly specialized signaling, ventilation, safety and fire systems for the 50.45 km bi‑national Channel Tunnel (opened 1994) create few qualified suppliers, raising switching costs due to certification and integration risks across UK and French regimes. Vendors thus hold pricing and lifecycle‑service leverage against Getlink, though multi‑year framework contracts and Euronext‑listed procurement practices mitigate but do not eliminate dependence.

Energy and grid operators

Getlink relies on traction power and grid stability on both sides of the Channel, exposing operations to RTE and NGESO system constraints and tariff regimes; ElecLink (1 GW interconnector, operational since 2022) adds optionality but ties flows to those rules. Price volatility and regulatory charges can be passed into operating costs. Demand management and hedging programs are used to partly offset supplier power.

Rolling stock and maintenance providers

Certified cross-Channel locomotives and accredited maintenance providers are scarce, concentrating bargaining power in few OEMs/MROs and forcing Getlink to rely on a limited pool of suppliers.

Safety accreditation and niche expertise command price premiums and prioritization, while lead times for parts and upgrades—often stretching to 6–12 months—create scheduling and capacity risk.

Technical and regulatory constraints cap multi-sourcing options, leaving Getlink exposed to supplier concentration and service continuity vulnerabilities.

Construction and heavy civil contractors

Skilled labor and unions

Binational, safety-critical operations rely on certified, scarce skills, concentrating bargaining power among specialized staff and technicians.

Strong labor representation on both sides of the Channel elevates wage and work-rule leverage, pressuring operating margins.

Industrial action risk can disrupt services and raise contingency and rerouting costs; training pipelines reduce dependence but require multi-year investment to scale.

- Skilled labor concentration

- Cross-border union leverage

- Service-disruption risk

- Long lead time for training

Supplier concentration raises switching costs; 1 GW grid tie and 6–12 month parts risk

Specialized systems, certified locomotives and Tier‑1 tunneling contractors create a concentrated supplier base, raising switching costs and pricing leverage over Getlink. Energy grid dependence (ElecLink 1 GW) and 6–12 month spare‑part lead times amplify risk; multi‑year contracts and hedging partly mitigate but do not remove exposure. EU cohesion funding (€330bn 2021–2027) sustains sector demand and supplier pricing power.

| Metric | Value |

|---|---|

| Tunnel length | 50.45 km |

| ElecLink capacity | 1 GW |

| Spare parts lead time | 6–12 months |

| EU cohesion funding | €330bn (2021–2027) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Getlink, offering detailed assessment of suppliers, buyers, substitutes, new entrants and industry rivalry to inform strategic decisions.

A concise, one-sheet Porter's Five Forces for Getlink — customizable pressure levels and instant radar visualization for scenario testing, ready to drop into decks or link into Excel dashboards without macros.

Customers Bargaining Power

Concentrated rail operators

Eurostar (about 11.5m passengers in 2023) and a handful of freight operators handle the majority of tunnel rail volume, concentrating buying power and strengthening leverage over access charges and slot allocation. The Channel Tunnel’s unique fixed link, with shuttle traffic of ~2.5m vehicles, limits credible switching. Performance SLAs, financial penalties and UK/EU regulatory oversight constrain negotiated terms.

Le Shuttle motorists and logistics

Passenger cars and trucks remain highly price sensitive versus ferries; in 2024 Getlink continued to face direct ferry competition on Channel routes where cross-Channel ferry fares average lower on many leisure routes. Group bookings and large fleets negotiate meaningful discounts—corporate and logistics contracts represented a material share of volumes in recent years. Convenience and high-frequency, rapid transit create switching frictions in peak periods, helping retain customers despite price sensitivity. Dynamic pricing and yield management reduce churn but encourage real-time comparison shopping across channels and operators.

Power traders on ElecLink

ElecLink's 1 GW capacity (operational since 2022) is auctioned to sophisticated market participants.

In 2024 traders arbitraged day-ahead and intraday spreads across interconnectors, exhibiting high price elasticity that limits persistent markups.

Transparent EU/UK market coupling and auction rules cap discretionary pricing; congestion rents on the UK-France link remained highly sensitive to macro conditions and policy in 2024.

Service quality and reliability expectations

Customers demand high availability, punctuality and security, typically expecting availability in excess of 99% for critical rail links; any disruption quickly triggers compensation payments and reputational cost for Getlink.

Buyers leverage KPI-linked penalties in contracts to exert power, and while Getlink’s 2024 investments in resilience (infrastructure, IT, contingency staffing) reduce exposure they cannot eliminate disruption risk.

- Availability target: >99%

- KPI penalties: common in contracts

- Disruption → compensation + reputational damage

- 2024 resilience capex raised risk mitigation but not removal

Regulatory-influenced pricing

- Regulators: ORR (UK), Autorité de régulation des transports (France)

- Effect: limits unilateral pricing; grants buyer recourse

- Timing: regulatory dispute resolution prolongs tariff adjustments

- Impact: compliance costs increase transparency and buyer leverage

Concentrated buyers and fleet deals constrain pricing despite >99% availability and regulation

Concentrated buyers (Eurostar: 11.5m pax 2023; shuttle ~2.5m vehicles) and large fleet contracts give customers strong leverage over access charges and slots, reinforced by KPI penalties and >99% availability expectations. Ferry price sensitivity and real-time price comparison limit sustained markups despite Getlink’s peak-period switching frictions. Regulatory oversight (ORR, ART) and market coupling cap unilateral pricing power.

| Metric | Value |

|---|---|

| Eurostar passengers 2023 | 11.5m |

| Shuttle vehicles 2023 | ~2.5m |

| Availability target | >99% |

| ElecLink capacity | 1 GW |

| Regulatory bodies | ORR / ART |

Preview Before You Purchase

Getlink Porter's Five Forces Analysis

This Getlink Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no samples or placeholders. It contains the complete strategic assessment, clear force-by-force evaluation, and actionable insights ready for download and use. Purchase grants instant access to this identical file for immediate incorporation into your decision-making or reports.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Getlink faces moderate buyer power, steady supplier influence, and barriers shaped by infrastructure and regulation; substitutes are limited but tech and modal shifts pose emerging threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Getlink’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized tunnel systems vendors

Highly specialized signaling, ventilation, safety and fire systems for the 50.45 km bi‑national Channel Tunnel (opened 1994) create few qualified suppliers, raising switching costs due to certification and integration risks across UK and French regimes. Vendors thus hold pricing and lifecycle‑service leverage against Getlink, though multi‑year framework contracts and Euronext‑listed procurement practices mitigate but do not eliminate dependence.

Energy and grid operators

Getlink relies on traction power and grid stability on both sides of the Channel, exposing operations to RTE and NGESO system constraints and tariff regimes; ElecLink (1 GW interconnector, operational since 2022) adds optionality but ties flows to those rules. Price volatility and regulatory charges can be passed into operating costs. Demand management and hedging programs are used to partly offset supplier power.

Rolling stock and maintenance providers

Certified cross-Channel locomotives and accredited maintenance providers are scarce, concentrating bargaining power in few OEMs/MROs and forcing Getlink to rely on a limited pool of suppliers.

Safety accreditation and niche expertise command price premiums and prioritization, while lead times for parts and upgrades—often stretching to 6–12 months—create scheduling and capacity risk.

Technical and regulatory constraints cap multi-sourcing options, leaving Getlink exposed to supplier concentration and service continuity vulnerabilities.

Construction and heavy civil contractors

Skilled labor and unions

Binational, safety-critical operations rely on certified, scarce skills, concentrating bargaining power among specialized staff and technicians.

Strong labor representation on both sides of the Channel elevates wage and work-rule leverage, pressuring operating margins.

Industrial action risk can disrupt services and raise contingency and rerouting costs; training pipelines reduce dependence but require multi-year investment to scale.

- Skilled labor concentration

- Cross-border union leverage

- Service-disruption risk

- Long lead time for training

Supplier concentration raises switching costs; 1 GW grid tie and 6–12 month parts risk

Specialized systems, certified locomotives and Tier‑1 tunneling contractors create a concentrated supplier base, raising switching costs and pricing leverage over Getlink. Energy grid dependence (ElecLink 1 GW) and 6–12 month spare‑part lead times amplify risk; multi‑year contracts and hedging partly mitigate but do not remove exposure. EU cohesion funding (€330bn 2021–2027) sustains sector demand and supplier pricing power.

| Metric | Value |

|---|---|

| Tunnel length | 50.45 km |

| ElecLink capacity | 1 GW |

| Spare parts lead time | 6–12 months |

| EU cohesion funding | €330bn (2021–2027) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Getlink, offering detailed assessment of suppliers, buyers, substitutes, new entrants and industry rivalry to inform strategic decisions.

A concise, one-sheet Porter's Five Forces for Getlink — customizable pressure levels and instant radar visualization for scenario testing, ready to drop into decks or link into Excel dashboards without macros.

Customers Bargaining Power

Concentrated rail operators

Eurostar (about 11.5m passengers in 2023) and a handful of freight operators handle the majority of tunnel rail volume, concentrating buying power and strengthening leverage over access charges and slot allocation. The Channel Tunnel’s unique fixed link, with shuttle traffic of ~2.5m vehicles, limits credible switching. Performance SLAs, financial penalties and UK/EU regulatory oversight constrain negotiated terms.

Le Shuttle motorists and logistics

Passenger cars and trucks remain highly price sensitive versus ferries; in 2024 Getlink continued to face direct ferry competition on Channel routes where cross-Channel ferry fares average lower on many leisure routes. Group bookings and large fleets negotiate meaningful discounts—corporate and logistics contracts represented a material share of volumes in recent years. Convenience and high-frequency, rapid transit create switching frictions in peak periods, helping retain customers despite price sensitivity. Dynamic pricing and yield management reduce churn but encourage real-time comparison shopping across channels and operators.

Power traders on ElecLink

ElecLink's 1 GW capacity (operational since 2022) is auctioned to sophisticated market participants.

In 2024 traders arbitraged day-ahead and intraday spreads across interconnectors, exhibiting high price elasticity that limits persistent markups.

Transparent EU/UK market coupling and auction rules cap discretionary pricing; congestion rents on the UK-France link remained highly sensitive to macro conditions and policy in 2024.

Service quality and reliability expectations

Customers demand high availability, punctuality and security, typically expecting availability in excess of 99% for critical rail links; any disruption quickly triggers compensation payments and reputational cost for Getlink.

Buyers leverage KPI-linked penalties in contracts to exert power, and while Getlink’s 2024 investments in resilience (infrastructure, IT, contingency staffing) reduce exposure they cannot eliminate disruption risk.

- Availability target: >99%

- KPI penalties: common in contracts

- Disruption → compensation + reputational damage

- 2024 resilience capex raised risk mitigation but not removal

Regulatory-influenced pricing

- Regulators: ORR (UK), Autorité de régulation des transports (France)

- Effect: limits unilateral pricing; grants buyer recourse

- Timing: regulatory dispute resolution prolongs tariff adjustments

- Impact: compliance costs increase transparency and buyer leverage

Concentrated buyers and fleet deals constrain pricing despite >99% availability and regulation

Concentrated buyers (Eurostar: 11.5m pax 2023; shuttle ~2.5m vehicles) and large fleet contracts give customers strong leverage over access charges and slots, reinforced by KPI penalties and >99% availability expectations. Ferry price sensitivity and real-time price comparison limit sustained markups despite Getlink’s peak-period switching frictions. Regulatory oversight (ORR, ART) and market coupling cap unilateral pricing power.

| Metric | Value |

|---|---|

| Eurostar passengers 2023 | 11.5m |

| Shuttle vehicles 2023 | ~2.5m |

| Availability target | >99% |

| ElecLink capacity | 1 GW |

| Regulatory bodies | ORR / ART |

Preview Before You Purchase

Getlink Porter's Five Forces Analysis

This Getlink Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no samples or placeholders. It contains the complete strategic assessment, clear force-by-force evaluation, and actionable insights ready for download and use. Purchase grants instant access to this identical file for immediate incorporation into your decision-making or reports.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Getlink faces moderate buyer power, steady supplier influence, and barriers shaped by infrastructure and regulation; substitutes are limited but tech and modal shifts pose emerging threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Getlink’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized tunnel systems vendors

Highly specialized signaling, ventilation, safety and fire systems for the 50.45 km bi‑national Channel Tunnel (opened 1994) create few qualified suppliers, raising switching costs due to certification and integration risks across UK and French regimes. Vendors thus hold pricing and lifecycle‑service leverage against Getlink, though multi‑year framework contracts and Euronext‑listed procurement practices mitigate but do not eliminate dependence.

Energy and grid operators

Getlink relies on traction power and grid stability on both sides of the Channel, exposing operations to RTE and NGESO system constraints and tariff regimes; ElecLink (1 GW interconnector, operational since 2022) adds optionality but ties flows to those rules. Price volatility and regulatory charges can be passed into operating costs. Demand management and hedging programs are used to partly offset supplier power.

Rolling stock and maintenance providers

Certified cross-Channel locomotives and accredited maintenance providers are scarce, concentrating bargaining power in few OEMs/MROs and forcing Getlink to rely on a limited pool of suppliers.

Safety accreditation and niche expertise command price premiums and prioritization, while lead times for parts and upgrades—often stretching to 6–12 months—create scheduling and capacity risk.

Technical and regulatory constraints cap multi-sourcing options, leaving Getlink exposed to supplier concentration and service continuity vulnerabilities.

Construction and heavy civil contractors

Skilled labor and unions

Binational, safety-critical operations rely on certified, scarce skills, concentrating bargaining power among specialized staff and technicians.

Strong labor representation on both sides of the Channel elevates wage and work-rule leverage, pressuring operating margins.

Industrial action risk can disrupt services and raise contingency and rerouting costs; training pipelines reduce dependence but require multi-year investment to scale.

- Skilled labor concentration

- Cross-border union leverage

- Service-disruption risk

- Long lead time for training

Supplier concentration raises switching costs; 1 GW grid tie and 6–12 month parts risk

Specialized systems, certified locomotives and Tier‑1 tunneling contractors create a concentrated supplier base, raising switching costs and pricing leverage over Getlink. Energy grid dependence (ElecLink 1 GW) and 6–12 month spare‑part lead times amplify risk; multi‑year contracts and hedging partly mitigate but do not remove exposure. EU cohesion funding (€330bn 2021–2027) sustains sector demand and supplier pricing power.

| Metric | Value |

|---|---|

| Tunnel length | 50.45 km |

| ElecLink capacity | 1 GW |

| Spare parts lead time | 6–12 months |

| EU cohesion funding | €330bn (2021–2027) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Getlink, offering detailed assessment of suppliers, buyers, substitutes, new entrants and industry rivalry to inform strategic decisions.

A concise, one-sheet Porter's Five Forces for Getlink — customizable pressure levels and instant radar visualization for scenario testing, ready to drop into decks or link into Excel dashboards without macros.

Customers Bargaining Power

Concentrated rail operators

Eurostar (about 11.5m passengers in 2023) and a handful of freight operators handle the majority of tunnel rail volume, concentrating buying power and strengthening leverage over access charges and slot allocation. The Channel Tunnel’s unique fixed link, with shuttle traffic of ~2.5m vehicles, limits credible switching. Performance SLAs, financial penalties and UK/EU regulatory oversight constrain negotiated terms.

Le Shuttle motorists and logistics

Passenger cars and trucks remain highly price sensitive versus ferries; in 2024 Getlink continued to face direct ferry competition on Channel routes where cross-Channel ferry fares average lower on many leisure routes. Group bookings and large fleets negotiate meaningful discounts—corporate and logistics contracts represented a material share of volumes in recent years. Convenience and high-frequency, rapid transit create switching frictions in peak periods, helping retain customers despite price sensitivity. Dynamic pricing and yield management reduce churn but encourage real-time comparison shopping across channels and operators.

Power traders on ElecLink

ElecLink's 1 GW capacity (operational since 2022) is auctioned to sophisticated market participants.

In 2024 traders arbitraged day-ahead and intraday spreads across interconnectors, exhibiting high price elasticity that limits persistent markups.

Transparent EU/UK market coupling and auction rules cap discretionary pricing; congestion rents on the UK-France link remained highly sensitive to macro conditions and policy in 2024.

Service quality and reliability expectations

Customers demand high availability, punctuality and security, typically expecting availability in excess of 99% for critical rail links; any disruption quickly triggers compensation payments and reputational cost for Getlink.

Buyers leverage KPI-linked penalties in contracts to exert power, and while Getlink’s 2024 investments in resilience (infrastructure, IT, contingency staffing) reduce exposure they cannot eliminate disruption risk.

- Availability target: >99%

- KPI penalties: common in contracts

- Disruption → compensation + reputational damage

- 2024 resilience capex raised risk mitigation but not removal

Regulatory-influenced pricing

- Regulators: ORR (UK), Autorité de régulation des transports (France)

- Effect: limits unilateral pricing; grants buyer recourse

- Timing: regulatory dispute resolution prolongs tariff adjustments

- Impact: compliance costs increase transparency and buyer leverage

Concentrated buyers and fleet deals constrain pricing despite >99% availability and regulation

Concentrated buyers (Eurostar: 11.5m pax 2023; shuttle ~2.5m vehicles) and large fleet contracts give customers strong leverage over access charges and slots, reinforced by KPI penalties and >99% availability expectations. Ferry price sensitivity and real-time price comparison limit sustained markups despite Getlink’s peak-period switching frictions. Regulatory oversight (ORR, ART) and market coupling cap unilateral pricing power.

| Metric | Value |

|---|---|

| Eurostar passengers 2023 | 11.5m |

| Shuttle vehicles 2023 | ~2.5m |

| Availability target | >99% |

| ElecLink capacity | 1 GW |

| Regulatory bodies | ORR / ART |

Preview Before You Purchase

Getlink Porter's Five Forces Analysis

This Getlink Porter's Five Forces Analysis preview is the exact, fully formatted document you'll receive immediately after purchase—no samples or placeholders. It contains the complete strategic assessment, clear force-by-force evaluation, and actionable insights ready for download and use. Purchase grants instant access to this identical file for immediate incorporation into your decision-making or reports.