Gordon Food Service Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Gordon Food Service faces moderate supplier power, intense buyer negotiation, and specific substitute and entrant risks that shape its margin outlook; competitive rivalry is fueled by scale and service differentiation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications. Purchase the complete report to inform investment or strategy decisions.

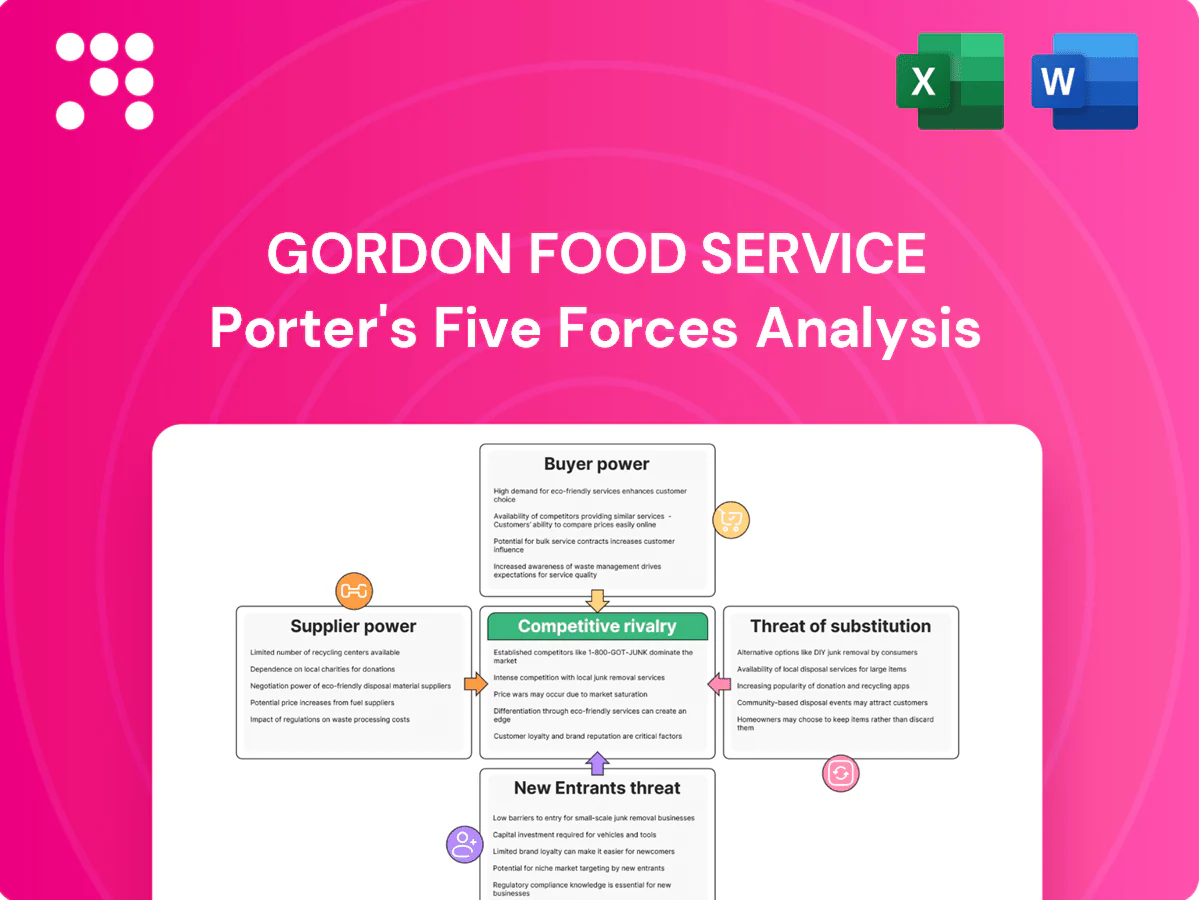

Suppliers Bargaining Power

Consolidated protein and dairy suppliers

Large meat packers and dairy processors are relatively consolidated—USDA data show the top four beef packers account for roughly 85% of U.S. steer and heifer slaughter—giving suppliers clear pricing leverage on core protein categories. Volatile feed and energy costs drive rapid price resets that distributors must pass through. Gordon offsets exposure via scale, long-term contracts and category diversification, but supplier-driven margin pressure remains material.

Perishable produce seasonality

Produce growers’ bargaining power spikes during weather shocks and seasonal shortages, with U.S. imports covering about 46% of fresh fruit and 23% of fresh vegetables (USDA ERS), tightening supply. Short shelf life—typically under two weeks for many fresh items—limits inventory buffering and increases supplier leverage during disruptions. Gordon Food Service mitigates via multi-sourcing and import programs, yet spot-market purchases can surge in peak shortages.

Branded CPG and non-food vendors

Recognized branded CPGs secure shelf and menu presence, enabling firmer pricing and rebate-driven contract terms with distributors and operators. Distributors like Gordon Food Service depend on brand pull to meet operator demand, which elevates supplier bargaining power. Private label and vendor consolidation partially offset this pressure, with private label penetration around 17% of U.S. grocery sales in 2024.

Logistics and packaging inputs

Packaging, refrigerants and fuel suppliers materially drive cost-to-serve in cold-chain distribution; U.S. diesel averaged roughly $3.80/gal in 2024, increasing linehaul sensitivity and margin exposure. When freight or packaging markets tighten, suppliers have pushed through surcharges and peak-season fuel/FSR add-ons, pressuring gross margins. Gordon Food Service mitigation includes long-term supply contracts and expanded in-house logistics to absorb spot volatility.

- fuel — ~3.80 $/gal (U.S. average, 2024)

- packaging/refrigerants — supplier surcharges spike during tightness, raising cost-to-serve

- mitigation — long-term contracts + in-house logistics reduce pass-through and volatility

Risk of supply disruptions

Food safety recalls, import constraints and disease outbreaks in 2024 amplified supplier leverage for Gordon Food Service, forcing distributors to accept narrower margins and higher lead-time risk to maintain fill rates; supply shocks repeatedly shifted negotiating power to available suppliers. Supplier scorecards and contingency sourcing lowered exposure but could not fully eliminate episodic shortages.

- Recall-driven leverage

- Import constraints

- Disease outbreak risk

- Fill-rate concessions

- Scorecards + contingency = risk reduction

Suppliers wield leverage: top-4 beef ≈85%, imports pressure supply chain

Suppliers hold meaningful leverage: top-four beef packers ≈85% share, produce imports ~46% fruit/23% veg (USDA ERS), and branded CPGs sustain pricing power; fuel averaged $3.80/gal (2024) adding linehaul cost pressure. Gordon uses scale, long-term contracts, private-label (~17% grocery share) and multi-sourcing to mitigate but episodic recalls and outbreaks raise supplier bargaining power.

| Metric | Value (2024) |

|---|---|

| Top‑4 beef share | ≈85% |

| Fruit imports | 46% |

| Veg imports | 23% |

| Diesel | $3.80/gal |

| Private label | 17% |

What is included in the product

Tailored Porter's Five Forces analysis for Gordon Food Service that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market position.

A concise Porter's Five Forces summary for Gordon Food Service—editable scores, instant radar visuals, and clear callouts to pinpoint competitive pain points and guide rapid strategic responses for decks or operational action plans.

Customers Bargaining Power

Large chains and GPO leverage

National chains and GPOs aggregate buying power across nearly 1 million US restaurant locations (National Restaurant Association), aggressively bidding contracts to extract lower prices, rebates, and bespoke service levels. Gordon Food Service, as a top-four US broadline distributor, must compete on total value — logistics, rebates, service — not list price, which systematically compresses distributor margins.

Price-sensitive independent operators

Restaurants and small food businesses run on thin net margins, typically 3–5% in the U.S., heightening price sensitivity. Independents routinely compare quotes across distributors and club stores to protect margins. Switching is operationally feasible, but service reliability, just-in-time delivery and credit terms provide meaningful stickiness for suppliers like Gordon Food Service.

Public sector and healthcare contracts

Public sector RFPs for schools and healthcare demand strict compliance and pricing transparency; K-12 programs served approximately 4.6 billion meals in 2023–24, driving large, predictable volumes for suppliers like Gordon Food Service. Multi-year contracts secure steady demand but restrict pricing flexibility and indexation, often locking margins. Performance penalties and auditability, common in public contracts, materially increase buyer bargaining power and contract enforcement risk.

Omnichannel alternatives increase choice

Omnichannel alternatives — GFS Marketplace, club stores and e-commerce — expand buyer choice and intensify price competition; club stores account for roughly 12% of US grocery sales (2024 est.), pressuring distributors like Gordon Food Service (GFS reported about $12.9B in sales in 2023).

Greater market-price visibility via online platforms reduces information asymmetry, raising buyer bargaining power while GFS counters with loyalty programs, private-label lines and digital ordering tools to lock in customers and protect margins.

- Channels: GFS Marketplace, club stores, e-commerce

- Data: club stores ~12% of US grocery sales (2024 est.); GFS ~$12.9B sales (2023)

- Defenses: loyalty programs, private label, digital ordering

Service-level expectations

Buyers demand high fill rates (typically 95–99%), frequent drops and just-in-time delivery, pressuring Gordon Food Service to sustain near-perfect logistics. Service failures prompt rapid supplier reevaluation and contract shifts, with customers switching after a single major lapse. Offering premium service supports value-based pricing but increases exposure to performance risk and higher operating costs.

- Fill rate target: 95–99%

- Drops: daily or multiple weekly drops expected

- Risk: premium service raises OPEX and failure impact

Concentrated demand and omnichannel retailing squeeze thin-margin foodservice operators

Large chains, GPOs and public RFPs concentrate demand (K‑12 ~4.6B meals 2023–24), driving intense price pressure and contract terms; buyers face thin restaurant margins (~3–5%) and high price sensitivity. Omnichannel options (club stores ~12% US grocery sales 2024) plus price transparency raise bargaining power, while GFS ($12.9B sales 2023) defends via private label, loyalty and logistics to retain customers.

| Metric | Value | Impact |

|---|---|---|

| Club store share | ~12% (2024) | Price pressure |

| GFS sales | $12.9B (2023) | Scale advantage |

| K‑12 meals | 4.6B (2023–24) | Contract volumes |

| Restaurant margins | 3–5% | High price sensitivity |

What You See Is What You Get

Gordon Food Service Porter's Five Forces Analysis

This preview shows the exact Gordon Food Service Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is the complete, professionally formatted file, ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this same document upon payment.

Don't Miss the Bigger Picture

Gordon Food Service faces moderate supplier power, intense buyer negotiation, and specific substitute and entrant risks that shape its margin outlook; competitive rivalry is fueled by scale and service differentiation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications. Purchase the complete report to inform investment or strategy decisions.

Suppliers Bargaining Power

Consolidated protein and dairy suppliers

Large meat packers and dairy processors are relatively consolidated—USDA data show the top four beef packers account for roughly 85% of U.S. steer and heifer slaughter—giving suppliers clear pricing leverage on core protein categories. Volatile feed and energy costs drive rapid price resets that distributors must pass through. Gordon offsets exposure via scale, long-term contracts and category diversification, but supplier-driven margin pressure remains material.

Perishable produce seasonality

Produce growers’ bargaining power spikes during weather shocks and seasonal shortages, with U.S. imports covering about 46% of fresh fruit and 23% of fresh vegetables (USDA ERS), tightening supply. Short shelf life—typically under two weeks for many fresh items—limits inventory buffering and increases supplier leverage during disruptions. Gordon Food Service mitigates via multi-sourcing and import programs, yet spot-market purchases can surge in peak shortages.

Branded CPG and non-food vendors

Recognized branded CPGs secure shelf and menu presence, enabling firmer pricing and rebate-driven contract terms with distributors and operators. Distributors like Gordon Food Service depend on brand pull to meet operator demand, which elevates supplier bargaining power. Private label and vendor consolidation partially offset this pressure, with private label penetration around 17% of U.S. grocery sales in 2024.

Logistics and packaging inputs

Packaging, refrigerants and fuel suppliers materially drive cost-to-serve in cold-chain distribution; U.S. diesel averaged roughly $3.80/gal in 2024, increasing linehaul sensitivity and margin exposure. When freight or packaging markets tighten, suppliers have pushed through surcharges and peak-season fuel/FSR add-ons, pressuring gross margins. Gordon Food Service mitigation includes long-term supply contracts and expanded in-house logistics to absorb spot volatility.

- fuel — ~3.80 $/gal (U.S. average, 2024)

- packaging/refrigerants — supplier surcharges spike during tightness, raising cost-to-serve

- mitigation — long-term contracts + in-house logistics reduce pass-through and volatility

Risk of supply disruptions

Food safety recalls, import constraints and disease outbreaks in 2024 amplified supplier leverage for Gordon Food Service, forcing distributors to accept narrower margins and higher lead-time risk to maintain fill rates; supply shocks repeatedly shifted negotiating power to available suppliers. Supplier scorecards and contingency sourcing lowered exposure but could not fully eliminate episodic shortages.

- Recall-driven leverage

- Import constraints

- Disease outbreak risk

- Fill-rate concessions

- Scorecards + contingency = risk reduction

Suppliers wield leverage: top-4 beef ≈85%, imports pressure supply chain

Suppliers hold meaningful leverage: top-four beef packers ≈85% share, produce imports ~46% fruit/23% veg (USDA ERS), and branded CPGs sustain pricing power; fuel averaged $3.80/gal (2024) adding linehaul cost pressure. Gordon uses scale, long-term contracts, private-label (~17% grocery share) and multi-sourcing to mitigate but episodic recalls and outbreaks raise supplier bargaining power.

| Metric | Value (2024) |

|---|---|

| Top‑4 beef share | ≈85% |

| Fruit imports | 46% |

| Veg imports | 23% |

| Diesel | $3.80/gal |

| Private label | 17% |

What is included in the product

Tailored Porter's Five Forces analysis for Gordon Food Service that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market position.

A concise Porter's Five Forces summary for Gordon Food Service—editable scores, instant radar visuals, and clear callouts to pinpoint competitive pain points and guide rapid strategic responses for decks or operational action plans.

Customers Bargaining Power

Large chains and GPO leverage

National chains and GPOs aggregate buying power across nearly 1 million US restaurant locations (National Restaurant Association), aggressively bidding contracts to extract lower prices, rebates, and bespoke service levels. Gordon Food Service, as a top-four US broadline distributor, must compete on total value — logistics, rebates, service — not list price, which systematically compresses distributor margins.

Price-sensitive independent operators

Restaurants and small food businesses run on thin net margins, typically 3–5% in the U.S., heightening price sensitivity. Independents routinely compare quotes across distributors and club stores to protect margins. Switching is operationally feasible, but service reliability, just-in-time delivery and credit terms provide meaningful stickiness for suppliers like Gordon Food Service.

Public sector and healthcare contracts

Public sector RFPs for schools and healthcare demand strict compliance and pricing transparency; K-12 programs served approximately 4.6 billion meals in 2023–24, driving large, predictable volumes for suppliers like Gordon Food Service. Multi-year contracts secure steady demand but restrict pricing flexibility and indexation, often locking margins. Performance penalties and auditability, common in public contracts, materially increase buyer bargaining power and contract enforcement risk.

Omnichannel alternatives increase choice

Omnichannel alternatives — GFS Marketplace, club stores and e-commerce — expand buyer choice and intensify price competition; club stores account for roughly 12% of US grocery sales (2024 est.), pressuring distributors like Gordon Food Service (GFS reported about $12.9B in sales in 2023).

Greater market-price visibility via online platforms reduces information asymmetry, raising buyer bargaining power while GFS counters with loyalty programs, private-label lines and digital ordering tools to lock in customers and protect margins.

- Channels: GFS Marketplace, club stores, e-commerce

- Data: club stores ~12% of US grocery sales (2024 est.); GFS ~$12.9B sales (2023)

- Defenses: loyalty programs, private label, digital ordering

Service-level expectations

Buyers demand high fill rates (typically 95–99%), frequent drops and just-in-time delivery, pressuring Gordon Food Service to sustain near-perfect logistics. Service failures prompt rapid supplier reevaluation and contract shifts, with customers switching after a single major lapse. Offering premium service supports value-based pricing but increases exposure to performance risk and higher operating costs.

- Fill rate target: 95–99%

- Drops: daily or multiple weekly drops expected

- Risk: premium service raises OPEX and failure impact

Concentrated demand and omnichannel retailing squeeze thin-margin foodservice operators

Large chains, GPOs and public RFPs concentrate demand (K‑12 ~4.6B meals 2023–24), driving intense price pressure and contract terms; buyers face thin restaurant margins (~3–5%) and high price sensitivity. Omnichannel options (club stores ~12% US grocery sales 2024) plus price transparency raise bargaining power, while GFS ($12.9B sales 2023) defends via private label, loyalty and logistics to retain customers.

| Metric | Value | Impact |

|---|---|---|

| Club store share | ~12% (2024) | Price pressure |

| GFS sales | $12.9B (2023) | Scale advantage |

| K‑12 meals | 4.6B (2023–24) | Contract volumes |

| Restaurant margins | 3–5% | High price sensitivity |

What You See Is What You Get

Gordon Food Service Porter's Five Forces Analysis

This preview shows the exact Gordon Food Service Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is the complete, professionally formatted file, ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this same document upon payment.

Description

Don't Miss the Bigger Picture

Gordon Food Service faces moderate supplier power, intense buyer negotiation, and specific substitute and entrant risks that shape its margin outlook; competitive rivalry is fueled by scale and service differentiation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications. Purchase the complete report to inform investment or strategy decisions.

Suppliers Bargaining Power

Consolidated protein and dairy suppliers

Large meat packers and dairy processors are relatively consolidated—USDA data show the top four beef packers account for roughly 85% of U.S. steer and heifer slaughter—giving suppliers clear pricing leverage on core protein categories. Volatile feed and energy costs drive rapid price resets that distributors must pass through. Gordon offsets exposure via scale, long-term contracts and category diversification, but supplier-driven margin pressure remains material.

Perishable produce seasonality

Produce growers’ bargaining power spikes during weather shocks and seasonal shortages, with U.S. imports covering about 46% of fresh fruit and 23% of fresh vegetables (USDA ERS), tightening supply. Short shelf life—typically under two weeks for many fresh items—limits inventory buffering and increases supplier leverage during disruptions. Gordon Food Service mitigates via multi-sourcing and import programs, yet spot-market purchases can surge in peak shortages.

Branded CPG and non-food vendors

Recognized branded CPGs secure shelf and menu presence, enabling firmer pricing and rebate-driven contract terms with distributors and operators. Distributors like Gordon Food Service depend on brand pull to meet operator demand, which elevates supplier bargaining power. Private label and vendor consolidation partially offset this pressure, with private label penetration around 17% of U.S. grocery sales in 2024.

Logistics and packaging inputs

Packaging, refrigerants and fuel suppliers materially drive cost-to-serve in cold-chain distribution; U.S. diesel averaged roughly $3.80/gal in 2024, increasing linehaul sensitivity and margin exposure. When freight or packaging markets tighten, suppliers have pushed through surcharges and peak-season fuel/FSR add-ons, pressuring gross margins. Gordon Food Service mitigation includes long-term supply contracts and expanded in-house logistics to absorb spot volatility.

- fuel — ~3.80 $/gal (U.S. average, 2024)

- packaging/refrigerants — supplier surcharges spike during tightness, raising cost-to-serve

- mitigation — long-term contracts + in-house logistics reduce pass-through and volatility

Risk of supply disruptions

Food safety recalls, import constraints and disease outbreaks in 2024 amplified supplier leverage for Gordon Food Service, forcing distributors to accept narrower margins and higher lead-time risk to maintain fill rates; supply shocks repeatedly shifted negotiating power to available suppliers. Supplier scorecards and contingency sourcing lowered exposure but could not fully eliminate episodic shortages.

- Recall-driven leverage

- Import constraints

- Disease outbreak risk

- Fill-rate concessions

- Scorecards + contingency = risk reduction

Suppliers wield leverage: top-4 beef ≈85%, imports pressure supply chain

Suppliers hold meaningful leverage: top-four beef packers ≈85% share, produce imports ~46% fruit/23% veg (USDA ERS), and branded CPGs sustain pricing power; fuel averaged $3.80/gal (2024) adding linehaul cost pressure. Gordon uses scale, long-term contracts, private-label (~17% grocery share) and multi-sourcing to mitigate but episodic recalls and outbreaks raise supplier bargaining power.

| Metric | Value (2024) |

|---|---|

| Top‑4 beef share | ≈85% |

| Fruit imports | 46% |

| Veg imports | 23% |

| Diesel | $3.80/gal |

| Private label | 17% |

What is included in the product

Tailored Porter's Five Forces analysis for Gordon Food Service that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market position.

A concise Porter's Five Forces summary for Gordon Food Service—editable scores, instant radar visuals, and clear callouts to pinpoint competitive pain points and guide rapid strategic responses for decks or operational action plans.

Customers Bargaining Power

Large chains and GPO leverage

National chains and GPOs aggregate buying power across nearly 1 million US restaurant locations (National Restaurant Association), aggressively bidding contracts to extract lower prices, rebates, and bespoke service levels. Gordon Food Service, as a top-four US broadline distributor, must compete on total value — logistics, rebates, service — not list price, which systematically compresses distributor margins.

Price-sensitive independent operators

Restaurants and small food businesses run on thin net margins, typically 3–5% in the U.S., heightening price sensitivity. Independents routinely compare quotes across distributors and club stores to protect margins. Switching is operationally feasible, but service reliability, just-in-time delivery and credit terms provide meaningful stickiness for suppliers like Gordon Food Service.

Public sector and healthcare contracts

Public sector RFPs for schools and healthcare demand strict compliance and pricing transparency; K-12 programs served approximately 4.6 billion meals in 2023–24, driving large, predictable volumes for suppliers like Gordon Food Service. Multi-year contracts secure steady demand but restrict pricing flexibility and indexation, often locking margins. Performance penalties and auditability, common in public contracts, materially increase buyer bargaining power and contract enforcement risk.

Omnichannel alternatives increase choice

Omnichannel alternatives — GFS Marketplace, club stores and e-commerce — expand buyer choice and intensify price competition; club stores account for roughly 12% of US grocery sales (2024 est.), pressuring distributors like Gordon Food Service (GFS reported about $12.9B in sales in 2023).

Greater market-price visibility via online platforms reduces information asymmetry, raising buyer bargaining power while GFS counters with loyalty programs, private-label lines and digital ordering tools to lock in customers and protect margins.

- Channels: GFS Marketplace, club stores, e-commerce

- Data: club stores ~12% of US grocery sales (2024 est.); GFS ~$12.9B sales (2023)

- Defenses: loyalty programs, private label, digital ordering

Service-level expectations

Buyers demand high fill rates (typically 95–99%), frequent drops and just-in-time delivery, pressuring Gordon Food Service to sustain near-perfect logistics. Service failures prompt rapid supplier reevaluation and contract shifts, with customers switching after a single major lapse. Offering premium service supports value-based pricing but increases exposure to performance risk and higher operating costs.

- Fill rate target: 95–99%

- Drops: daily or multiple weekly drops expected

- Risk: premium service raises OPEX and failure impact

Concentrated demand and omnichannel retailing squeeze thin-margin foodservice operators

Large chains, GPOs and public RFPs concentrate demand (K‑12 ~4.6B meals 2023–24), driving intense price pressure and contract terms; buyers face thin restaurant margins (~3–5%) and high price sensitivity. Omnichannel options (club stores ~12% US grocery sales 2024) plus price transparency raise bargaining power, while GFS ($12.9B sales 2023) defends via private label, loyalty and logistics to retain customers.

| Metric | Value | Impact |

|---|---|---|

| Club store share | ~12% (2024) | Price pressure |

| GFS sales | $12.9B (2023) | Scale advantage |

| K‑12 meals | 4.6B (2023–24) | Contract volumes |

| Restaurant margins | 3–5% | High price sensitivity |

What You See Is What You Get

Gordon Food Service Porter's Five Forces Analysis

This preview shows the exact Gordon Food Service Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is the complete, professionally formatted file, ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this same document upon payment.