Gibson, Dunn & Crutcher Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Gibson, Dunn & Crutcher faces nuanced competitive pressures—high buyer sophistication, concentrated top-tier clients, and evolving substitute legal services elevate strategic risk while strong brand and scale limit new entrant threats. This brief teases key force interactions and tactical implications. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Elite talent scarcity

Top-tier partners and associates are scarce across M&A, litigation and IP, giving them outsized leverage; partner pay often exceeds $1m and top associate base salaries reached $215k+ in major US firms in 2024. Compensation competition lifts demands for higher salary, bonuses and expanded support resources, while attrition in large firms runs roughly 15–25% annually. Retention packages, training and culture investments are now mandatory to mitigate departures, concentrating supplier power toward high‑demand lawyers.

Star partner mobility

Portable books of business give rainmakers leverage to negotiate team structures and economics, with Gibson Dunn employing roughly 1,400 lawyers in 2024 and competing for laterals through multi-million-dollar guarantees. Lateral markets remain active, with premium guarantees and flexible compensation common across AmLaw firms. Losing or winning a marquee partner can rapidly shift a practice group’s strength and client flow. This sustains elevated supplier power at the top end.

Legal tech/data vendors

Research and eDiscovery platforms (Lexis/Westlaw account for roughly 70–80% of U.S. legal research use in 2024) are concentrated, creating mission‑critical lock‑in and price inelasticity for premium functionality. Global eDiscovery/analytics market is about $10B in 2024, with advanced modules often costing thousands per user or tens to hundreds of thousands for enterprise deployments. Volume discounts mitigate costs for large firms, but vendor consolidation sustains moderate supplier power.

Expert witnesses niche

Highly specialized expert witnesses for complex litigation are scarce and often conflicted, giving them outsized negotiating leverage; top forensic, valuation and technical experts command premium fees—commonly $500–2,000+/hour and retainers from $25,000–200,000 in 2024. Availability, credibility and scheduling can decisively shape case strategy and outcomes, increasing supplier influence in high-stakes matters.

- Limited supply of niche experts

- Premium fees and large retainers

- Schedule/credibility decisive for strategy

- High supplier bargaining power in major cases

Prime office real estate

Tier-1 locations in global financial/legal hubs remain expensive despite hybrid work, with 2024 prime rents roughly USD 120–140/sq ft in Midtown Manhattan and GBP 150–170/sq ft in London West End; vacancy declines in top assets keep demand concentrated. Long leases and build-outs (often 8–15 years lease terms and fit-out costs commonly USD 300–600/sq ft) create tenant lock-in and limited flexibility. Landlords of prestige buildings retain negotiating leverage on renewal and amenity premiums, sustaining moderate supplier power in physical footprint decisions.

- Prime rents 2024: Midtown ~USD 120–140/sq ft, London West End ~GBP 150–170/sq ft

- Lease terms: commonly 8–15 years; fit-outs USD 300–600/sq ft

- Result: moderate supplier power for office footprint choices

Partner pay >$1M; eDiscovery ~$10B

Top-tier partners/associates scarce, pay >$1M partners and top associate base $215k+ (2024), creating strong supplier leverage. Portable books and Gibson Dunn’s ~1,400 lawyers sustain multi-million-dollar lateral guarantees. Lexis/Westlaw ~70–80% U.S. research share; eDiscovery market ~$10B (2024). Expert witnesses $500–2,000+/hr, retainers $25k–200k, elevating supplier power in major cases.

| Category | 2024 Metric |

|---|---|

| Top partner pay | >$1,000,000 |

| Top associate base | $215,000+ |

| Gibson Dunn headcount | ~1,400 lawyers |

| Legal research share | 70–80% |

| eDiscovery market | ~$10B |

| Expert fees | $500–2,000+/hr; retainers $25k–200k |

What is included in the product

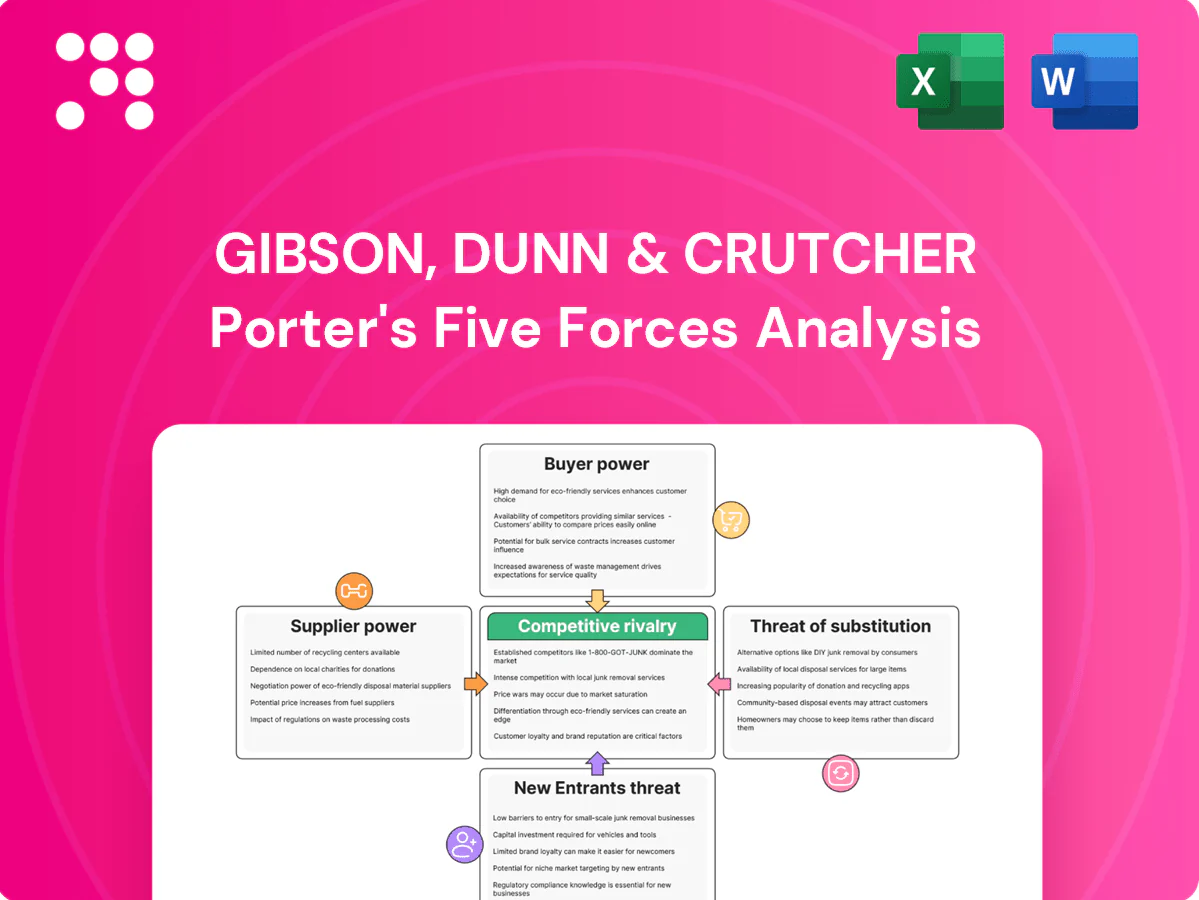

Tailored Porter's Five Forces analysis for Gibson, Dunn & Crutcher uncovering competitive intensity, client bargaining power, supplier influences, threat of substitutes and new entrants, plus strategic levers to protect market position.

Gibson, Dunn & Crutcher's Porter's Five Forces one-sheet—legal‑calibrated pressure levels and a clean radar chart—streamlines strategic decisions for counsel and executives, ready to drop into pitch decks or regulatory submissions.

Customers Bargaining Power

Concentrated corporate clients

Large multinationals and financial institutions control sizable fee wallets, with top corporate clients often directing $10M+ in annual external legal spend to preferred firms.

They can steer matter flow and demand competitive rates and staffing efficiencies, negotiating discounts commonly in the mid-single digits to low double digits.

Multi-year relationships can temper price pressure but expectations on value, responsiveness and alternative staffing remain high, keeping buyer power strong among top clients.

Panels and RFP rigor

Procurement-led panels and AFAs, plus detailed RFP scoring, standardize comparisons and compress pricing—by 2024 roughly 60% of large-company legal RFPs formally scored DEI and outcome metrics—shifting rewards to demonstrable value, benchmarks and innovation; structured sourcing and scorecards therefore elevate buyer leverage and force firms to present clear benchmarks, innovation metrics and DEI outcomes to win work.

In-house counsel sophistication

Corporate legal teams are expanding and tightly manage work allocation, with roughly 60% of departments using matter-management platforms in 2024 to unbundle tasks and retain routine work internally. They outsource only complex slices, driving down external fee pools as data-driven matter management benchmarks and SLAs pressure rates and staffing. This expertise materially strengthens buyer power against firms like Gibson Dunn.

Switching across firms

While trust and conflicts create some client stickiness, Gibson Dunn clients can and do shift matters to peer firms; 2024 surveys show buyers prioritize price and flexibility, increasing mobility. Broad panels let clients reassign matters rapidly for performance or fee reasons, and standardized work keeps knowledge-transfer costs low, enhancing buyer leverage.

- Switchability: panel depth enables quick reassignment

- Costs: standardized work limits transfer expense

- Leverage: buyer options raise negotiating power

Global coverage demands

Clients now demand seamless cross-border capability and 24/7 responsiveness; in 2024 roughly 72% of Fortune 1000 legal teams prioritized integrated global platforms, pressuring firms like Gibson Dunn to supply always-on coverage. Gaps in global reach trigger competitive bids from other global players and shift fee and scope negotiations in buyers favor.

- Clients: cross-border + 24/7

- 72%: global platform priority (2024)

- Gaps = competitive bids

- Buyer expectations tighten terms

Top clients drive discounts as 72% of Fortune 1000 favor integrated global legal platforms

Top corporate clients wield strong bargaining power, often directing $10M+ annual legal spend and demanding mid-single to low-double digit discounts. Procurement-led RFPs, AFAs and matter scorecards (60% include DEI/outcome metrics in 2024) compress pricing and reward demonstrable value. In 2024, 72% of Fortune 1000 legal teams prioritize integrated global platforms, raising mobility and lowering switching costs.

| Metric | 2024 |

|---|---|

| RFPs scoring DEI/outcomes | 60% |

| Fortune 1000 global platform priority | 72% |

| Top-client external legal spend | $10M+ |

Full Version Awaits

Gibson, Dunn & Crutcher Porter's Five Forces Analysis

The Gibson, Dunn & Crutcher Porter's Five Forces Analysis evaluates competitive rivalry, client bargaining power, supplier (talent and technology) leverage, threat of new entrants, and substitute legal services to assess firm positioning and profitability. It highlights strategic risks and growth opportunities for partners and investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

A Must-Have Tool for Decision-Makers

Gibson, Dunn & Crutcher faces nuanced competitive pressures—high buyer sophistication, concentrated top-tier clients, and evolving substitute legal services elevate strategic risk while strong brand and scale limit new entrant threats. This brief teases key force interactions and tactical implications. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Elite talent scarcity

Top-tier partners and associates are scarce across M&A, litigation and IP, giving them outsized leverage; partner pay often exceeds $1m and top associate base salaries reached $215k+ in major US firms in 2024. Compensation competition lifts demands for higher salary, bonuses and expanded support resources, while attrition in large firms runs roughly 15–25% annually. Retention packages, training and culture investments are now mandatory to mitigate departures, concentrating supplier power toward high‑demand lawyers.

Star partner mobility

Portable books of business give rainmakers leverage to negotiate team structures and economics, with Gibson Dunn employing roughly 1,400 lawyers in 2024 and competing for laterals through multi-million-dollar guarantees. Lateral markets remain active, with premium guarantees and flexible compensation common across AmLaw firms. Losing or winning a marquee partner can rapidly shift a practice group’s strength and client flow. This sustains elevated supplier power at the top end.

Legal tech/data vendors

Research and eDiscovery platforms (Lexis/Westlaw account for roughly 70–80% of U.S. legal research use in 2024) are concentrated, creating mission‑critical lock‑in and price inelasticity for premium functionality. Global eDiscovery/analytics market is about $10B in 2024, with advanced modules often costing thousands per user or tens to hundreds of thousands for enterprise deployments. Volume discounts mitigate costs for large firms, but vendor consolidation sustains moderate supplier power.

Expert witnesses niche

Highly specialized expert witnesses for complex litigation are scarce and often conflicted, giving them outsized negotiating leverage; top forensic, valuation and technical experts command premium fees—commonly $500–2,000+/hour and retainers from $25,000–200,000 in 2024. Availability, credibility and scheduling can decisively shape case strategy and outcomes, increasing supplier influence in high-stakes matters.

- Limited supply of niche experts

- Premium fees and large retainers

- Schedule/credibility decisive for strategy

- High supplier bargaining power in major cases

Prime office real estate

Tier-1 locations in global financial/legal hubs remain expensive despite hybrid work, with 2024 prime rents roughly USD 120–140/sq ft in Midtown Manhattan and GBP 150–170/sq ft in London West End; vacancy declines in top assets keep demand concentrated. Long leases and build-outs (often 8–15 years lease terms and fit-out costs commonly USD 300–600/sq ft) create tenant lock-in and limited flexibility. Landlords of prestige buildings retain negotiating leverage on renewal and amenity premiums, sustaining moderate supplier power in physical footprint decisions.

- Prime rents 2024: Midtown ~USD 120–140/sq ft, London West End ~GBP 150–170/sq ft

- Lease terms: commonly 8–15 years; fit-outs USD 300–600/sq ft

- Result: moderate supplier power for office footprint choices

Partner pay >$1M; eDiscovery ~$10B

Top-tier partners/associates scarce, pay >$1M partners and top associate base $215k+ (2024), creating strong supplier leverage. Portable books and Gibson Dunn’s ~1,400 lawyers sustain multi-million-dollar lateral guarantees. Lexis/Westlaw ~70–80% U.S. research share; eDiscovery market ~$10B (2024). Expert witnesses $500–2,000+/hr, retainers $25k–200k, elevating supplier power in major cases.

| Category | 2024 Metric |

|---|---|

| Top partner pay | >$1,000,000 |

| Top associate base | $215,000+ |

| Gibson Dunn headcount | ~1,400 lawyers |

| Legal research share | 70–80% |

| eDiscovery market | ~$10B |

| Expert fees | $500–2,000+/hr; retainers $25k–200k |

What is included in the product

Tailored Porter's Five Forces analysis for Gibson, Dunn & Crutcher uncovering competitive intensity, client bargaining power, supplier influences, threat of substitutes and new entrants, plus strategic levers to protect market position.

Gibson, Dunn & Crutcher's Porter's Five Forces one-sheet—legal‑calibrated pressure levels and a clean radar chart—streamlines strategic decisions for counsel and executives, ready to drop into pitch decks or regulatory submissions.

Customers Bargaining Power

Concentrated corporate clients

Large multinationals and financial institutions control sizable fee wallets, with top corporate clients often directing $10M+ in annual external legal spend to preferred firms.

They can steer matter flow and demand competitive rates and staffing efficiencies, negotiating discounts commonly in the mid-single digits to low double digits.

Multi-year relationships can temper price pressure but expectations on value, responsiveness and alternative staffing remain high, keeping buyer power strong among top clients.

Panels and RFP rigor

Procurement-led panels and AFAs, plus detailed RFP scoring, standardize comparisons and compress pricing—by 2024 roughly 60% of large-company legal RFPs formally scored DEI and outcome metrics—shifting rewards to demonstrable value, benchmarks and innovation; structured sourcing and scorecards therefore elevate buyer leverage and force firms to present clear benchmarks, innovation metrics and DEI outcomes to win work.

In-house counsel sophistication

Corporate legal teams are expanding and tightly manage work allocation, with roughly 60% of departments using matter-management platforms in 2024 to unbundle tasks and retain routine work internally. They outsource only complex slices, driving down external fee pools as data-driven matter management benchmarks and SLAs pressure rates and staffing. This expertise materially strengthens buyer power against firms like Gibson Dunn.

Switching across firms

While trust and conflicts create some client stickiness, Gibson Dunn clients can and do shift matters to peer firms; 2024 surveys show buyers prioritize price and flexibility, increasing mobility. Broad panels let clients reassign matters rapidly for performance or fee reasons, and standardized work keeps knowledge-transfer costs low, enhancing buyer leverage.

- Switchability: panel depth enables quick reassignment

- Costs: standardized work limits transfer expense

- Leverage: buyer options raise negotiating power

Global coverage demands

Clients now demand seamless cross-border capability and 24/7 responsiveness; in 2024 roughly 72% of Fortune 1000 legal teams prioritized integrated global platforms, pressuring firms like Gibson Dunn to supply always-on coverage. Gaps in global reach trigger competitive bids from other global players and shift fee and scope negotiations in buyers favor.

- Clients: cross-border + 24/7

- 72%: global platform priority (2024)

- Gaps = competitive bids

- Buyer expectations tighten terms

Top clients drive discounts as 72% of Fortune 1000 favor integrated global legal platforms

Top corporate clients wield strong bargaining power, often directing $10M+ annual legal spend and demanding mid-single to low-double digit discounts. Procurement-led RFPs, AFAs and matter scorecards (60% include DEI/outcome metrics in 2024) compress pricing and reward demonstrable value. In 2024, 72% of Fortune 1000 legal teams prioritize integrated global platforms, raising mobility and lowering switching costs.

| Metric | 2024 |

|---|---|

| RFPs scoring DEI/outcomes | 60% |

| Fortune 1000 global platform priority | 72% |

| Top-client external legal spend | $10M+ |

Full Version Awaits

Gibson, Dunn & Crutcher Porter's Five Forces Analysis

The Gibson, Dunn & Crutcher Porter's Five Forces Analysis evaluates competitive rivalry, client bargaining power, supplier (talent and technology) leverage, threat of new entrants, and substitute legal services to assess firm positioning and profitability. It highlights strategic risks and growth opportunities for partners and investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Gibson, Dunn & Crutcher faces nuanced competitive pressures—high buyer sophistication, concentrated top-tier clients, and evolving substitute legal services elevate strategic risk while strong brand and scale limit new entrant threats. This brief teases key force interactions and tactical implications. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Elite talent scarcity

Top-tier partners and associates are scarce across M&A, litigation and IP, giving them outsized leverage; partner pay often exceeds $1m and top associate base salaries reached $215k+ in major US firms in 2024. Compensation competition lifts demands for higher salary, bonuses and expanded support resources, while attrition in large firms runs roughly 15–25% annually. Retention packages, training and culture investments are now mandatory to mitigate departures, concentrating supplier power toward high‑demand lawyers.

Star partner mobility

Portable books of business give rainmakers leverage to negotiate team structures and economics, with Gibson Dunn employing roughly 1,400 lawyers in 2024 and competing for laterals through multi-million-dollar guarantees. Lateral markets remain active, with premium guarantees and flexible compensation common across AmLaw firms. Losing or winning a marquee partner can rapidly shift a practice group’s strength and client flow. This sustains elevated supplier power at the top end.

Legal tech/data vendors

Research and eDiscovery platforms (Lexis/Westlaw account for roughly 70–80% of U.S. legal research use in 2024) are concentrated, creating mission‑critical lock‑in and price inelasticity for premium functionality. Global eDiscovery/analytics market is about $10B in 2024, with advanced modules often costing thousands per user or tens to hundreds of thousands for enterprise deployments. Volume discounts mitigate costs for large firms, but vendor consolidation sustains moderate supplier power.

Expert witnesses niche

Highly specialized expert witnesses for complex litigation are scarce and often conflicted, giving them outsized negotiating leverage; top forensic, valuation and technical experts command premium fees—commonly $500–2,000+/hour and retainers from $25,000–200,000 in 2024. Availability, credibility and scheduling can decisively shape case strategy and outcomes, increasing supplier influence in high-stakes matters.

- Limited supply of niche experts

- Premium fees and large retainers

- Schedule/credibility decisive for strategy

- High supplier bargaining power in major cases

Prime office real estate

Tier-1 locations in global financial/legal hubs remain expensive despite hybrid work, with 2024 prime rents roughly USD 120–140/sq ft in Midtown Manhattan and GBP 150–170/sq ft in London West End; vacancy declines in top assets keep demand concentrated. Long leases and build-outs (often 8–15 years lease terms and fit-out costs commonly USD 300–600/sq ft) create tenant lock-in and limited flexibility. Landlords of prestige buildings retain negotiating leverage on renewal and amenity premiums, sustaining moderate supplier power in physical footprint decisions.

- Prime rents 2024: Midtown ~USD 120–140/sq ft, London West End ~GBP 150–170/sq ft

- Lease terms: commonly 8–15 years; fit-outs USD 300–600/sq ft

- Result: moderate supplier power for office footprint choices

Partner pay >$1M; eDiscovery ~$10B

Top-tier partners/associates scarce, pay >$1M partners and top associate base $215k+ (2024), creating strong supplier leverage. Portable books and Gibson Dunn’s ~1,400 lawyers sustain multi-million-dollar lateral guarantees. Lexis/Westlaw ~70–80% U.S. research share; eDiscovery market ~$10B (2024). Expert witnesses $500–2,000+/hr, retainers $25k–200k, elevating supplier power in major cases.

| Category | 2024 Metric |

|---|---|

| Top partner pay | >$1,000,000 |

| Top associate base | $215,000+ |

| Gibson Dunn headcount | ~1,400 lawyers |

| Legal research share | 70–80% |

| eDiscovery market | ~$10B |

| Expert fees | $500–2,000+/hr; retainers $25k–200k |

What is included in the product

Tailored Porter's Five Forces analysis for Gibson, Dunn & Crutcher uncovering competitive intensity, client bargaining power, supplier influences, threat of substitutes and new entrants, plus strategic levers to protect market position.

Gibson, Dunn & Crutcher's Porter's Five Forces one-sheet—legal‑calibrated pressure levels and a clean radar chart—streamlines strategic decisions for counsel and executives, ready to drop into pitch decks or regulatory submissions.

Customers Bargaining Power

Concentrated corporate clients

Large multinationals and financial institutions control sizable fee wallets, with top corporate clients often directing $10M+ in annual external legal spend to preferred firms.

They can steer matter flow and demand competitive rates and staffing efficiencies, negotiating discounts commonly in the mid-single digits to low double digits.

Multi-year relationships can temper price pressure but expectations on value, responsiveness and alternative staffing remain high, keeping buyer power strong among top clients.

Panels and RFP rigor

Procurement-led panels and AFAs, plus detailed RFP scoring, standardize comparisons and compress pricing—by 2024 roughly 60% of large-company legal RFPs formally scored DEI and outcome metrics—shifting rewards to demonstrable value, benchmarks and innovation; structured sourcing and scorecards therefore elevate buyer leverage and force firms to present clear benchmarks, innovation metrics and DEI outcomes to win work.

In-house counsel sophistication

Corporate legal teams are expanding and tightly manage work allocation, with roughly 60% of departments using matter-management platforms in 2024 to unbundle tasks and retain routine work internally. They outsource only complex slices, driving down external fee pools as data-driven matter management benchmarks and SLAs pressure rates and staffing. This expertise materially strengthens buyer power against firms like Gibson Dunn.

Switching across firms

While trust and conflicts create some client stickiness, Gibson Dunn clients can and do shift matters to peer firms; 2024 surveys show buyers prioritize price and flexibility, increasing mobility. Broad panels let clients reassign matters rapidly for performance or fee reasons, and standardized work keeps knowledge-transfer costs low, enhancing buyer leverage.

- Switchability: panel depth enables quick reassignment

- Costs: standardized work limits transfer expense

- Leverage: buyer options raise negotiating power

Global coverage demands

Clients now demand seamless cross-border capability and 24/7 responsiveness; in 2024 roughly 72% of Fortune 1000 legal teams prioritized integrated global platforms, pressuring firms like Gibson Dunn to supply always-on coverage. Gaps in global reach trigger competitive bids from other global players and shift fee and scope negotiations in buyers favor.

- Clients: cross-border + 24/7

- 72%: global platform priority (2024)

- Gaps = competitive bids

- Buyer expectations tighten terms

Top clients drive discounts as 72% of Fortune 1000 favor integrated global legal platforms

Top corporate clients wield strong bargaining power, often directing $10M+ annual legal spend and demanding mid-single to low-double digit discounts. Procurement-led RFPs, AFAs and matter scorecards (60% include DEI/outcome metrics in 2024) compress pricing and reward demonstrable value. In 2024, 72% of Fortune 1000 legal teams prioritize integrated global platforms, raising mobility and lowering switching costs.

| Metric | 2024 |

|---|---|

| RFPs scoring DEI/outcomes | 60% |

| Fortune 1000 global platform priority | 72% |

| Top-client external legal spend | $10M+ |

Full Version Awaits

Gibson, Dunn & Crutcher Porter's Five Forces Analysis

The Gibson, Dunn & Crutcher Porter's Five Forces Analysis evaluates competitive rivalry, client bargaining power, supplier (talent and technology) leverage, threat of new entrants, and substitute legal services to assess firm positioning and profitability. It highlights strategic risks and growth opportunities for partners and investors. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.