G-III SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

G-III’s SWOT highlights strong brand licenses and diversified channels but flags margin pressure from cost inflation and retail exposure; opportunities include direct-to-consumer growth and international expansion while competitors and inventory risk pose threats. Discover the full, editable SWOT report—purchase to access detailed analysis, financial context, and strategic recommendations.

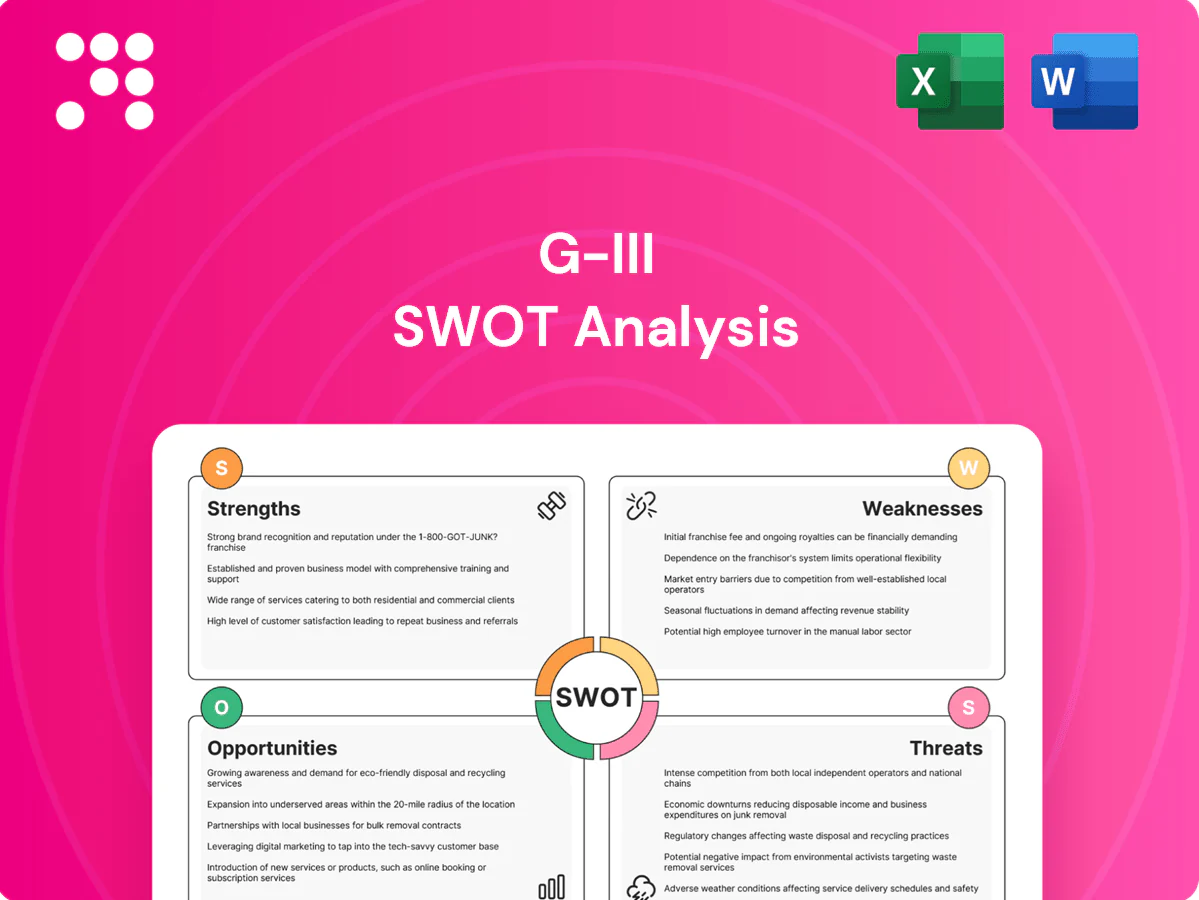

Strengths

Diverse brand portfolio

G-III’s ownership, licensing and private‑label development across entry to premium segments diversifies risk and reduces reliance on any single brand lifecycle; fiscal 2024 net sales were about $2.7 billion, reflecting the portfolio’s revenue resilience. This breadth lets G-III tailor assortments to major retailers’ cadence and seasonal needs. A wide brand mix also strengthens bargaining power with suppliers and key accounts.

Multi-channel reach

G-III operates wholesale, retail and licensing channels—selling through department stores, specialty retailers, e-commerce and owned stores—which helped produce roughly $3.1 billion in net sales in fiscal 2024. Channel diversity spreads risk across partners and captures varied margin pools, insulating margins during retail disruptions. Cross-channel visibility improves trend detection, and combined POS and online data increasingly informs design and inventory allocation.

Category breadth

G-III’s category breadth—strong positions in outerwear, dresses, sportswear and footwear—creates multiple revenue streams, supporting reported net sales of about $3.0 billion in fiscal 2024. Category adjacency enables cohesive merchandising stories and higher average order values through upsell across product lines. It boosts factory utilization and scale buys, lowering unit costs and supporting margins. A broad assortment helps the company withstand category-specific downturns.

Global sourcing and speed-to-market

G-III leverages an established global vendor network and design/sourcing expertise to deliver responsive collections; FY2024 net sales were about $2.6B, underscoring commercial scale.

Scale secures better cost, quality and lead times, enabling faster refresh cycles that reduce trend risk and support private-label and fast-moving licensed programs.

- Responsive sourcing

- Scale: purchasing leverage

- Faster refresh = lower trend exposure

- Agility for private label & licensed lines

Deep retail relationships

Longstanding ties with major department and specialty retailers drive shelf space and collaborative planning, and G-III reported net sales of $2.31 billion for fiscal 2024, underscoring retailer reliance. Co-development with partners improves sell-through by aligning assortments and timing. Shared POS and inventory data enhances allocation and replenishment, while preferred vendor status secures seasonal commitments and advance buys.

- Retail partnerships: collaborative planning

- Co-development: higher sell-through

- Data-sharing: optimized allocation/replenishment

- Preferred vendor: seasonal commitment advantages

Diversified brands and multi-channel distribution underpin resilience with $3.0B FY2024 sales

G-III’s diversified brand portfolio and private‑label/licensing mix drives resilience, supporting FY2024 net sales of about $3.0B and reducing single‑brand risk. Multi‑channel distribution (wholesale, retail, licensing) and deep retailer partnerships bolster shelf space and collaborative planning, with retail sales of $2.31B in FY2024. Scale in sourcing and vendor networks enables faster refresh, lower unit costs and stronger margin leverage.

| Metric | FY2024 |

|---|---|

| Total net sales | ~ $3.0B |

| Retail sales | $2.31B |

| Channels | Wholesale, Retail, Licensing |

What is included in the product

Provides a concise SWOT analysis of G-III, highlighting internal strengths and weaknesses—such as brand portfolio, distribution reach and margin pressures—and external opportunities and threats including retail trends, licensing dynamics, supply-chain risks and competitive pressures shaping its strategic outlook.

Delivers a concise, high-level SWOT for G-III to quickly identify weaknesses and opportunities, speeding stakeholder alignment and remediation planning.

Weaknesses

Department store dependence

Heavy reliance on department-store wholesale exposes G-III to traffic declines and promotional pressure, which in FY2024 left wholesale margins under strain as mall-based peers reported weaker comps; door closures compress unit volume and accelerate margin erosion. Rapid retailer inventory tightening can cut purchase orders quickly, and negotiating leverage typically favors large accounts like Macy’s and Nordstrom, pressuring pricing and terms.

License concentration risk

G-III (NASDAQ: GIII) relies heavily on third-party licensed brands, creating renewal and royalty exposure tied to licensors’ decisions. The strategy is vulnerable to shifts in licensors’ brand direction, and loss or downgrade of a key license would pressure revenue and channel relationships. Minimum guarantees under licenses can strain margins during retail downturns, amplifying cash-flow and profitability risk.

Margin volatility

Promotional retailing and volatile freight and input costs can compress G-III’s gross margins, a key risk for a company reporting fiscal 2024 net sales of roughly $3.1 billion. Fashion misses drive markdowns and elevated returns, eroding realized margin. Operational complexity across brands and categories raises overhead, while shifts toward lower-margin channels such as off-price and digital can dilute overall profitability.

Inventory and fashion risk

Seasonality and trend-driven assortments raise obsolescence risk; G-III carried about $1.1 billion in inventory as of Jan 31, 2024, exposing the firm to markdowns. Long supplier lead times (commonly 4–6 months) can misalign supply with demand, forcing off-price clearances and amplifying forecast errors across the wholesale pipeline.

- Inventory: $1.1B (Jan 31, 2024)

- Lead times: 4–6 months

- Overstock → off-price clearance

- Forecast errors ripple through wholesale

Limited DTC scale vs peers

G-III’s owned retail and e-commerce footprint remains smaller than many brand-led peers, limiting first-party data capture and full-price sell-through and reducing visibility into consumer trends. Heavy reliance on wholesale partners constrains cohesive brand storytelling and customer experience control. A lower direct-to-consumer mix restricts potential margin expansion from higher-margin owned channels.

- Smaller owned retail/e‑commerce vs peers

- Weak first-party data capture

- Partner dependence limits brand storytelling

- Lower DTC mix caps margin upside

Wholesale, mall exposure trim margins despite $3.1B sales; $1.1B inventory

Heavy wholesale dependence and mall exposure compressed FY2024 margins despite $3.1B sales; door closures and retailer leverage accelerate margin pressure. Reliance on licensed brands creates renewal and royalty risk; $1.1B inventory and 4–6 month lead times raise obsolescence and markdown risk. Smaller owned retail/e‑comm limits first‑party data and margin expansion.

| Metric | Value |

|---|---|

| FY2024 sales | $3.1B |

| Inventory (Jan 31, 2024) | $1.1B |

| Lead time | 4–6 months |

Full Version Awaits

G-III SWOT Analysis

This is the actual G-III SWOT analysis document you’ll receive upon purchase—no surprises, just professional, structured content. The preview below is taken directly from the full report; buying unlocks the editable, complete version with in-depth strengths, weaknesses, opportunities, and threats. The full file is ready to download immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

G-III’s SWOT highlights strong brand licenses and diversified channels but flags margin pressure from cost inflation and retail exposure; opportunities include direct-to-consumer growth and international expansion while competitors and inventory risk pose threats. Discover the full, editable SWOT report—purchase to access detailed analysis, financial context, and strategic recommendations.

Strengths

Diverse brand portfolio

G-III’s ownership, licensing and private‑label development across entry to premium segments diversifies risk and reduces reliance on any single brand lifecycle; fiscal 2024 net sales were about $2.7 billion, reflecting the portfolio’s revenue resilience. This breadth lets G-III tailor assortments to major retailers’ cadence and seasonal needs. A wide brand mix also strengthens bargaining power with suppliers and key accounts.

Multi-channel reach

G-III operates wholesale, retail and licensing channels—selling through department stores, specialty retailers, e-commerce and owned stores—which helped produce roughly $3.1 billion in net sales in fiscal 2024. Channel diversity spreads risk across partners and captures varied margin pools, insulating margins during retail disruptions. Cross-channel visibility improves trend detection, and combined POS and online data increasingly informs design and inventory allocation.

Category breadth

G-III’s category breadth—strong positions in outerwear, dresses, sportswear and footwear—creates multiple revenue streams, supporting reported net sales of about $3.0 billion in fiscal 2024. Category adjacency enables cohesive merchandising stories and higher average order values through upsell across product lines. It boosts factory utilization and scale buys, lowering unit costs and supporting margins. A broad assortment helps the company withstand category-specific downturns.

Global sourcing and speed-to-market

G-III leverages an established global vendor network and design/sourcing expertise to deliver responsive collections; FY2024 net sales were about $2.6B, underscoring commercial scale.

Scale secures better cost, quality and lead times, enabling faster refresh cycles that reduce trend risk and support private-label and fast-moving licensed programs.

- Responsive sourcing

- Scale: purchasing leverage

- Faster refresh = lower trend exposure

- Agility for private label & licensed lines

Deep retail relationships

Longstanding ties with major department and specialty retailers drive shelf space and collaborative planning, and G-III reported net sales of $2.31 billion for fiscal 2024, underscoring retailer reliance. Co-development with partners improves sell-through by aligning assortments and timing. Shared POS and inventory data enhances allocation and replenishment, while preferred vendor status secures seasonal commitments and advance buys.

- Retail partnerships: collaborative planning

- Co-development: higher sell-through

- Data-sharing: optimized allocation/replenishment

- Preferred vendor: seasonal commitment advantages

Diversified brands and multi-channel distribution underpin resilience with $3.0B FY2024 sales

G-III’s diversified brand portfolio and private‑label/licensing mix drives resilience, supporting FY2024 net sales of about $3.0B and reducing single‑brand risk. Multi‑channel distribution (wholesale, retail, licensing) and deep retailer partnerships bolster shelf space and collaborative planning, with retail sales of $2.31B in FY2024. Scale in sourcing and vendor networks enables faster refresh, lower unit costs and stronger margin leverage.

| Metric | FY2024 |

|---|---|

| Total net sales | ~ $3.0B |

| Retail sales | $2.31B |

| Channels | Wholesale, Retail, Licensing |

What is included in the product

Provides a concise SWOT analysis of G-III, highlighting internal strengths and weaknesses—such as brand portfolio, distribution reach and margin pressures—and external opportunities and threats including retail trends, licensing dynamics, supply-chain risks and competitive pressures shaping its strategic outlook.

Delivers a concise, high-level SWOT for G-III to quickly identify weaknesses and opportunities, speeding stakeholder alignment and remediation planning.

Weaknesses

Department store dependence

Heavy reliance on department-store wholesale exposes G-III to traffic declines and promotional pressure, which in FY2024 left wholesale margins under strain as mall-based peers reported weaker comps; door closures compress unit volume and accelerate margin erosion. Rapid retailer inventory tightening can cut purchase orders quickly, and negotiating leverage typically favors large accounts like Macy’s and Nordstrom, pressuring pricing and terms.

License concentration risk

G-III (NASDAQ: GIII) relies heavily on third-party licensed brands, creating renewal and royalty exposure tied to licensors’ decisions. The strategy is vulnerable to shifts in licensors’ brand direction, and loss or downgrade of a key license would pressure revenue and channel relationships. Minimum guarantees under licenses can strain margins during retail downturns, amplifying cash-flow and profitability risk.

Margin volatility

Promotional retailing and volatile freight and input costs can compress G-III’s gross margins, a key risk for a company reporting fiscal 2024 net sales of roughly $3.1 billion. Fashion misses drive markdowns and elevated returns, eroding realized margin. Operational complexity across brands and categories raises overhead, while shifts toward lower-margin channels such as off-price and digital can dilute overall profitability.

Inventory and fashion risk

Seasonality and trend-driven assortments raise obsolescence risk; G-III carried about $1.1 billion in inventory as of Jan 31, 2024, exposing the firm to markdowns. Long supplier lead times (commonly 4–6 months) can misalign supply with demand, forcing off-price clearances and amplifying forecast errors across the wholesale pipeline.

- Inventory: $1.1B (Jan 31, 2024)

- Lead times: 4–6 months

- Overstock → off-price clearance

- Forecast errors ripple through wholesale

Limited DTC scale vs peers

G-III’s owned retail and e-commerce footprint remains smaller than many brand-led peers, limiting first-party data capture and full-price sell-through and reducing visibility into consumer trends. Heavy reliance on wholesale partners constrains cohesive brand storytelling and customer experience control. A lower direct-to-consumer mix restricts potential margin expansion from higher-margin owned channels.

- Smaller owned retail/e‑commerce vs peers

- Weak first-party data capture

- Partner dependence limits brand storytelling

- Lower DTC mix caps margin upside

Wholesale, mall exposure trim margins despite $3.1B sales; $1.1B inventory

Heavy wholesale dependence and mall exposure compressed FY2024 margins despite $3.1B sales; door closures and retailer leverage accelerate margin pressure. Reliance on licensed brands creates renewal and royalty risk; $1.1B inventory and 4–6 month lead times raise obsolescence and markdown risk. Smaller owned retail/e‑comm limits first‑party data and margin expansion.

| Metric | Value |

|---|---|

| FY2024 sales | $3.1B |

| Inventory (Jan 31, 2024) | $1.1B |

| Lead time | 4–6 months |

Full Version Awaits

G-III SWOT Analysis

This is the actual G-III SWOT analysis document you’ll receive upon purchase—no surprises, just professional, structured content. The preview below is taken directly from the full report; buying unlocks the editable, complete version with in-depth strengths, weaknesses, opportunities, and threats. The full file is ready to download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

G-III’s SWOT highlights strong brand licenses and diversified channels but flags margin pressure from cost inflation and retail exposure; opportunities include direct-to-consumer growth and international expansion while competitors and inventory risk pose threats. Discover the full, editable SWOT report—purchase to access detailed analysis, financial context, and strategic recommendations.

Strengths

Diverse brand portfolio

G-III’s ownership, licensing and private‑label development across entry to premium segments diversifies risk and reduces reliance on any single brand lifecycle; fiscal 2024 net sales were about $2.7 billion, reflecting the portfolio’s revenue resilience. This breadth lets G-III tailor assortments to major retailers’ cadence and seasonal needs. A wide brand mix also strengthens bargaining power with suppliers and key accounts.

Multi-channel reach

G-III operates wholesale, retail and licensing channels—selling through department stores, specialty retailers, e-commerce and owned stores—which helped produce roughly $3.1 billion in net sales in fiscal 2024. Channel diversity spreads risk across partners and captures varied margin pools, insulating margins during retail disruptions. Cross-channel visibility improves trend detection, and combined POS and online data increasingly informs design and inventory allocation.

Category breadth

G-III’s category breadth—strong positions in outerwear, dresses, sportswear and footwear—creates multiple revenue streams, supporting reported net sales of about $3.0 billion in fiscal 2024. Category adjacency enables cohesive merchandising stories and higher average order values through upsell across product lines. It boosts factory utilization and scale buys, lowering unit costs and supporting margins. A broad assortment helps the company withstand category-specific downturns.

Global sourcing and speed-to-market

G-III leverages an established global vendor network and design/sourcing expertise to deliver responsive collections; FY2024 net sales were about $2.6B, underscoring commercial scale.

Scale secures better cost, quality and lead times, enabling faster refresh cycles that reduce trend risk and support private-label and fast-moving licensed programs.

- Responsive sourcing

- Scale: purchasing leverage

- Faster refresh = lower trend exposure

- Agility for private label & licensed lines

Deep retail relationships

Longstanding ties with major department and specialty retailers drive shelf space and collaborative planning, and G-III reported net sales of $2.31 billion for fiscal 2024, underscoring retailer reliance. Co-development with partners improves sell-through by aligning assortments and timing. Shared POS and inventory data enhances allocation and replenishment, while preferred vendor status secures seasonal commitments and advance buys.

- Retail partnerships: collaborative planning

- Co-development: higher sell-through

- Data-sharing: optimized allocation/replenishment

- Preferred vendor: seasonal commitment advantages

Diversified brands and multi-channel distribution underpin resilience with $3.0B FY2024 sales

G-III’s diversified brand portfolio and private‑label/licensing mix drives resilience, supporting FY2024 net sales of about $3.0B and reducing single‑brand risk. Multi‑channel distribution (wholesale, retail, licensing) and deep retailer partnerships bolster shelf space and collaborative planning, with retail sales of $2.31B in FY2024. Scale in sourcing and vendor networks enables faster refresh, lower unit costs and stronger margin leverage.

| Metric | FY2024 |

|---|---|

| Total net sales | ~ $3.0B |

| Retail sales | $2.31B |

| Channels | Wholesale, Retail, Licensing |

What is included in the product

Provides a concise SWOT analysis of G-III, highlighting internal strengths and weaknesses—such as brand portfolio, distribution reach and margin pressures—and external opportunities and threats including retail trends, licensing dynamics, supply-chain risks and competitive pressures shaping its strategic outlook.

Delivers a concise, high-level SWOT for G-III to quickly identify weaknesses and opportunities, speeding stakeholder alignment and remediation planning.

Weaknesses

Department store dependence

Heavy reliance on department-store wholesale exposes G-III to traffic declines and promotional pressure, which in FY2024 left wholesale margins under strain as mall-based peers reported weaker comps; door closures compress unit volume and accelerate margin erosion. Rapid retailer inventory tightening can cut purchase orders quickly, and negotiating leverage typically favors large accounts like Macy’s and Nordstrom, pressuring pricing and terms.

License concentration risk

G-III (NASDAQ: GIII) relies heavily on third-party licensed brands, creating renewal and royalty exposure tied to licensors’ decisions. The strategy is vulnerable to shifts in licensors’ brand direction, and loss or downgrade of a key license would pressure revenue and channel relationships. Minimum guarantees under licenses can strain margins during retail downturns, amplifying cash-flow and profitability risk.

Margin volatility

Promotional retailing and volatile freight and input costs can compress G-III’s gross margins, a key risk for a company reporting fiscal 2024 net sales of roughly $3.1 billion. Fashion misses drive markdowns and elevated returns, eroding realized margin. Operational complexity across brands and categories raises overhead, while shifts toward lower-margin channels such as off-price and digital can dilute overall profitability.

Inventory and fashion risk

Seasonality and trend-driven assortments raise obsolescence risk; G-III carried about $1.1 billion in inventory as of Jan 31, 2024, exposing the firm to markdowns. Long supplier lead times (commonly 4–6 months) can misalign supply with demand, forcing off-price clearances and amplifying forecast errors across the wholesale pipeline.

- Inventory: $1.1B (Jan 31, 2024)

- Lead times: 4–6 months

- Overstock → off-price clearance

- Forecast errors ripple through wholesale

Limited DTC scale vs peers

G-III’s owned retail and e-commerce footprint remains smaller than many brand-led peers, limiting first-party data capture and full-price sell-through and reducing visibility into consumer trends. Heavy reliance on wholesale partners constrains cohesive brand storytelling and customer experience control. A lower direct-to-consumer mix restricts potential margin expansion from higher-margin owned channels.

- Smaller owned retail/e‑commerce vs peers

- Weak first-party data capture

- Partner dependence limits brand storytelling

- Lower DTC mix caps margin upside

Wholesale, mall exposure trim margins despite $3.1B sales; $1.1B inventory

Heavy wholesale dependence and mall exposure compressed FY2024 margins despite $3.1B sales; door closures and retailer leverage accelerate margin pressure. Reliance on licensed brands creates renewal and royalty risk; $1.1B inventory and 4–6 month lead times raise obsolescence and markdown risk. Smaller owned retail/e‑comm limits first‑party data and margin expansion.

| Metric | Value |

|---|---|

| FY2024 sales | $3.1B |

| Inventory (Jan 31, 2024) | $1.1B |

| Lead time | 4–6 months |

Full Version Awaits

G-III SWOT Analysis

This is the actual G-III SWOT analysis document you’ll receive upon purchase—no surprises, just professional, structured content. The preview below is taken directly from the full report; buying unlocks the editable, complete version with in-depth strengths, weaknesses, opportunities, and threats. The full file is ready to download immediately after checkout.